Adobe: Volatile But Reliable And Undervalued By 20%

Adobe is a global leader in creative software and digital marketing, known for innovative tools like Photoshop, Acrobat, and Firefly.

Adobe (ADBE) is a leading software company that allows individuals and organizations to create, manage, and enhance digital content. Known for its innovative products like Photoshop, Acrobat, and Illustrator, Adobe has set the standard for creative software globally. The company also has a strong presence in the digital marketing space through Adobe Experience Cloud. Adobe operates in over 20 countries, delivering progressive solutions to professionals and enterprises. Focusing on AI and cloud-based solutions should help maintain its leadership in digital content creation.

Content:

💡 Investment Thesis

❓ Why Price Is Down

🧐 Company Overview

🏰 Economic Moat

🚀 Business Strategy

🏛️ Capital Allocation

✅ Advantages

❌ Disadvantages

🥇 Competitors

⏮️ Past

📶 Future

💲Current Valuation

🏷️ Fair Price

☑️ Checklist

✍️ Due Diligence

💡 Investment Thesis

Adobe is a dominant player in the creative software and digital marketing industries, backed by a comprehensive portfolio of market-leading products. Has a wide economic moat built on high switching costs and industry-standard tools. Strong brand loyalty among creative professionals and enterprises worldwide.

Strategic focus on innovation, particularly in AI with tools like Firefly, positions Adobe to capture the growing demand for AI-powered creative solutions. Its transition to a subscription-based revenue model ensures stable and predictable cash flows. Over the past decade, Adobe has successfully expanded into digital marketing and e-commerce through acquisitions such as Omniture, Magento, and Marketo, creating new revenue streams and cross-selling opportunities.

However, Adobe faces near-term challenges, including increased competition from low-cost alternatives like Canva and Stability AI, as well as slower-than-expected AI monetization. The company's fiscal 2025 outlook, which fell short of market expectations, has impacted investor sentiment. Yet, with a PEG ratio of 1.40, Adobe offers a compelling long-term upside for patient investors.

Trading below its 5-year average valuation metrics and with a fair price estimate of $527 (almost 20% upside from current levels), the company presents an attractive entry point. While near-term volatility may persist, Adobe’s leadership in creative software, its ongoing AI innovation, and its strategic approach to capital allocation make it a strong candidate for long-term investment.

➡️ Additional materials: PDF/PNG Quick Analysis and Additional Article - In the additional article for patrons, there is a lite version of the analysis with an accent on Adobe’s subscription-based transition. Use the promo code 2025 to receive 60% off your first month of subscription.

❓ Why Price Is Down

Adobe’s stock price has recently gone down mainly because the company gave a disappointing outlook for its future earnings. Although Adobe reported better-than-expected earnings for the last quarter, its forecast for fiscal 2025 was lower than what many investors hoped for. There are also concerns about how well Adobe is using AI to boost its sales, as it seems to be taking longer than expected. With increasing competition from cheaper alternatives, investors are worried about Adobe's future growth.

🧐 Company Overview

Incorporated: 1982

IPO: 1986

Sector: Technology

Industry: Software

Stock Style: Large Core

Market Cap: $194.13 Bil

Total Number of Employees: 29,945

Website: https://www.adobe.com

Earnings Date: Mar 12, 2025Founded in 1982, Adobe has grown into an over $194 billion (at the moment of publication) market leader in the software industry. Its revenue reached $21.51 billion in fiscal 2024, marking an 11% increase year-over-year. The company operates through three main segments: Digital Media, Digital Experience, and Publishing. Their core products include Creative Cloud, Document Cloud, and Adobe Experience Cloud, which serve diverse audiences ranging from individual creators to large-scale enterprises. Its headquarters are in San Jose, California, but its presence spans more than 20 countries, including major markets like Germany, India, and Japan.

Adobe's CEO, Shantanu Narayen since taking the role in 2007, has led Adobe through significant changes, including the transition to a subscription-based revenue model and the expansion into digital marketing. His leadership has positioned Adobe as an innovation leader, particularly in AI and cloud-based technologies. Narayen’s recent recognition with the Global Lifetime Achievement Award highlights his contributions to the tech industry and Adobe’s ongoing success.

🏰 Economic Moat

Adobe has a wide economic moat due to its high switching costs and industry-standard products. Creative professionals worldwide depend on Adobe tools like Photoshop, Illustrator, and Premiere Pro, which are deeply integrated into workflows. Switching to alternative platforms often involves significant time and financial costs, making Adobe necessary for many users and companies.

The PDF format, a base of Adobe Document Cloud, has become the global standard for digital documents. With Acrobat as its leading PDF editor, Adobe is dominant in this market. The prevalence of its tools across industries strengthens Adobe’s competitive advantage.

🚀 Business Strategy

Adobe's business strategy is based on innovation, acquisitions, and expanding its customer base. The company continues to enhance its offerings with AI-powered tools like Firefly, which streamline creative processes. Adobe Express, launched in 2023, targets non-professional users with affordable and easy-to-use tools, broadening its reach.

Acquisitions remain a base of Adobe’s growth strategy. The company has successfully entered new markets, such as digital marketing, through strategic purchases like Omniture (Adobe Analytics), Magento (Adobe Commerce), and Marketo (a complete AI-powered marketing automation platform that helps teams scale personalized buyer engagement and grow predictable pipeline and revenue). These acquisitions not only expand Adobe’s portfolio but also create cross-selling opportunities, driving revenue growth.

By transitioning to a subscription-based model, Adobe ensures stable and predictable revenue streams. This approach allows the company to continuously innovate while maintaining strong financial health.

Core business segments:

Digital Media: Adobe's largest segment focuses on customer creation, management, and engagement with digital content. It includes flagship products such as Adobe Creative Cloud, which provides a suite of tools for design, video editing, photography, and more. Popular applications under this umbrella include Photoshop, Illustrator, Premiere Pro, and After Effects. Adobe Acrobat and Adobe Sign for document management and e-signature solutions also fall under this segment, facilitating document collaboration and workflow efficiency.

Digital Experience: This segment targets enterprises, providing them with solutions to create, manage, and optimize customer experiences across various channels. It encompasses Adobe Experience Cloud, which offers a suite of analytics, content management, advertising, and campaign management solutions. Components include Adobe Experience Manager, Adobe Analytics, Adobe Target, and more. This segment is designed to help businesses deliver personalized and consistent customer experiences, thereby improving customer engagement and conversion rates.

To read: About Adobe

Publishing and Advertising: Adobe's legacy business segment includes various solutions for technical document publishing, e-learning solutions, and Web conferencing. Products such as Adobe Captivate, Adobe Connect, and Adobe FrameMaker are part of this segment. Additionally, this segment includes Adobe's advertising solutions, which integrate with its other offerings to enhance the effectiveness of digital ad campaigns.

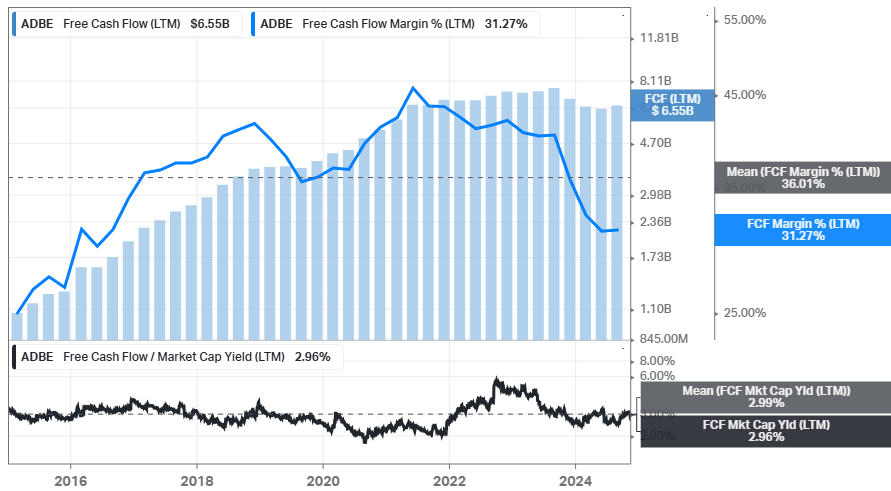

🏛️ Capital Allocation

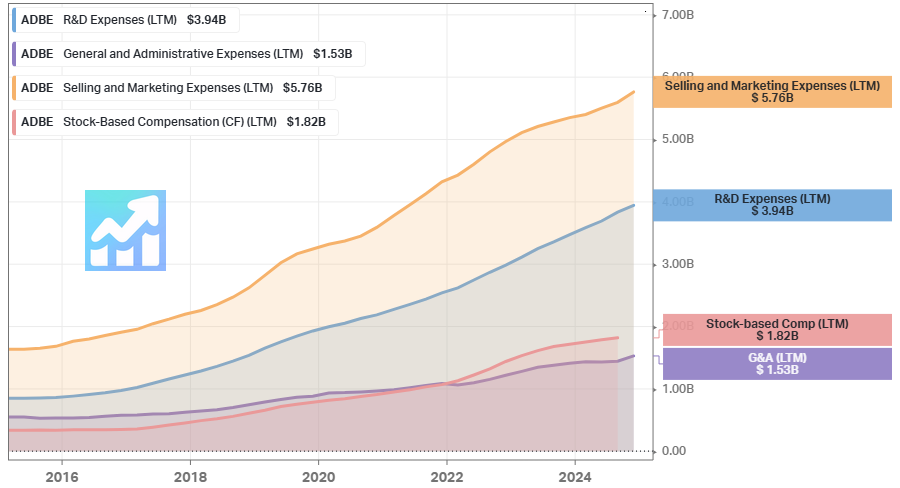

Adobe excels in capital allocation, balancing investments in innovation with shareholder returns. The company repurchased 17.5 million shares in 2024, reflecting confidence in its growth prospects. The company continues to focus on research and development, particularly in AI and machine learning, to maintain its competitive advantage. Doesn’t pay dividends.

As I wrote above (Business Strategy), acquisitions also play a key role in Adobe’s strategy. The company targets small to medium-sized businesses that complement its existing portfolio. This approach ensures that acquisitions align with Adobe’s long-term goals while minimizing risks.

But overall shareholder yield is lower than the buyback yield on the chart above due to the company’s stock-based compensation program:

✅ Advantages

Dominance in Creative Software: Adobe’s Creative Cloud suite, featuring Photoshop, Illustrator, and Premiere Pro, remains the industry standard for professionals worldwide. Its tools are used across various fields, including graphic design, video production, and photography, making it a market leader.

To read: Adobe’s new AI tool can turn anyone into an infographics wiz

Recurring Revenue Model: Adobe’s shift to a subscription model has ensured consistent cash flow. This recurring revenue provides financial stability and supports the company’s ongoing investments in innovation.

Global Presence: Operating in more than 20 countries, Adobe has a diversified revenue base. This international reach helps the company mitigate risks associated with economic slowdowns in any single region.

Focus on Innovation: Adobe’s investment in AI and machine learning keeps it ahead of the curve. Tools like Firefly demonstrate the company’s ability to adapt to new trends and meet the evolving needs of its customers.

Loyal Customer Base: With its products deeply integrated into professional workflows, Adobe owns strong brand loyalty. This customer trust reduces the risk of revenue loss from competition.

❌ Disadvantages

Currency Volatility: With 25.1% of revenue coming from Europe in 2024, Adobe is vulnerable to currency fluctuations, which can impact its financial performance.

Overdependence on Core Products: A significant portion of Adobe’s revenue comes from Creative Cloud and Acrobat. This reliance makes the company susceptible to market changes affecting these products.

Rising Competition: Competitors in the AI and creative software spaces, such as Stability AI and Canva, are increasingly challenging Adobe’s market share. This competition could pressure Adobe to innovate faster.

Integration Challenges: Assimilating acquired companies like Marketo and Magento into Adobe’s ecosystem can be complex. Any integration issues could impact operational efficiency and revenue growth.

Geopolitical Risks: Geopolitical tensions could disrupt Adobe's business operations, particularly in regions where the company relies on third-party data centers and cloud infrastructure providers.

🥇 Competitors

While Microsoft, Salesforce, and Oracle may be competitors to Adobe, they are not direct competitors across all areas. Adobe primarily focuses on creative software, document management, and digital marketing, while these companies have broader or different focuses. Direct competitors such as Canva and Stability AI target Adobe's core offerings more directly.

Microsoft (MSFT) competes directly with Adobe in document management (e.g., Microsoft Word vs. Adobe Acrobat) and, to some extent, creative software (e.g., Microsoft Designer). However, Microsoft primarily focuses on productivity tools and enterprise solutions, whereas Adobe specializes in creative and digital marketing tools. This makes Microsoft a partial competitor rather than a direct one in Adobe’s core segments.

Salesforce (CRM) is a direct competitor to Adobe’s Experience Cloud in the digital marketing and customer experience space. Both companies offer tools for managing customer journeys and marketing analytics. However, Salesforce does not compete with Adobe in creative software or document management, so their competition is limited to specific segments.

Oracle (ORCL) competes with Adobe in digital marketing and analytics, where Oracle offers enterprise solutions that overlap with Adobe Experience Cloud. However, Oracle is not involved in creative software or document management, making it an indirect competitor with overlapping areas in enterprise markets.

Canva (Private) is one of Adobe’s most direct competitors in the design software space, especially among non-professional users. Canva’s user-friendly interface and affordable pricing attract small businesses and casual creators. While Canva excels in simplicity and accessibility, Adobe remains the go-to solution for professionals requiring advanced features. Adobe’s Creative Cloud Express (formerly Spark) is its response to Canva, targeting a broader audience with simplified tools.

Figma (Private) directly competes with Adobe’s UX/UI design tools, particularly Adobe XD. As a cloud-based collaborative platform, Figma is popular among designers for its real-time team collaboration features. It appeals to modern design teams who prioritize ease of use and accessibility. While Adobe attempted to acquire Figma for $20 billion in 2023, the deal was terminated due to regulatory concerns. Figma remains a strong independent competitor, pushing Adobe to improve collaboration capabilities within its own design tools.

Stability AI (Private) competes with Adobe in the generative AI space. Its open-source models like Stable Diffusion are popular among developers and artists. Adobe’s Firefly, however, differentiates itself with commercial safety and integration into Adobe's ecosystem. Adobe’s strength lies in its established tools and enterprise adoption, while Stability AI appeals to a tech-savvy and cost-conscious audience.

Affinity (Private) offers cost-effective, one-time-purchase alternatives to Adobe tools like Photoshop and Illustrator. Its products appeal to freelancers and hobbyists who want professional-grade software without the commitment of a subscription. While Adobe leads in features and integration, Affinity’s lower price point and growing community make it a viable competitor.

⏮️ Past

Above is the compound annual growth rate (CAGR) for the ADBE stock over 5-year, 10-year, and 15-year time periods. The 5-year CAGR is very low - only 5.26%, the 10-year CAGR is 19.32%, and the 15-year CAGR is 17.72%. Long-term periods are outperforming the S&P 500 significantly.

Above is a comparison of total returns with the S&P 500 (SPY) on a 10-year period. You may notice that ADBE might be very volatile during some periods.

Latest important news:

December 2024: Adobe reported record revenue of $21.51 billion for FY24, marking an 11% increase year-over-year, driven by strong performance in its Digital Media sector and advancements in AI solutions, particularly the Firefly suite, which saw over 16 billion generations.

December 2024: Partnerships with Box and AWS.

October 2024: Announced the general availability of Adobe GenStudio for Performance Marketing, a new generative AI-first application that aims to accelerate the delivery of global advertising and marketing campaigns.

October 2024: Announced new innovations in Photoshop and Illustrator, including a new Generative Workspace (beta) and powerful 3D workflows, powered by the latest Firefly Image 3 Model.

October 2024: Announced the general availability of the next generation of Frame.io to streamline collaboration for creative teams. It also increases support for video, photography, and design with support for Adobe file formats.

October 2024: Announced the expansion of its Firefly family of creative generative AI models to video, along with new innovations in its Image, Vector, and Design models.

October 2024: Announced new Adobe Express innovations with Creative Cloud and 150+ add-ons with leading social, productivity, and collaboration apps to empower marketing, HR, and sales teams to create on-brand assets.

August 2024: Announced the general availability of Adobe Journey Optimizer (AJO) B2B Edition. The offering aims to activate generative AI to help B2B businesses engage customers with greater precision and boost growth.

August 2024: Announced the latest update for Adobe Express for Education to bring responsible generative AI into the classrooms. Free for K-12, the New Adobe Firefly-powered features aim to help students creatively express themselves with simple text prompts to generate templates, and teachers to provide real-time individual feedback.

📶 Future

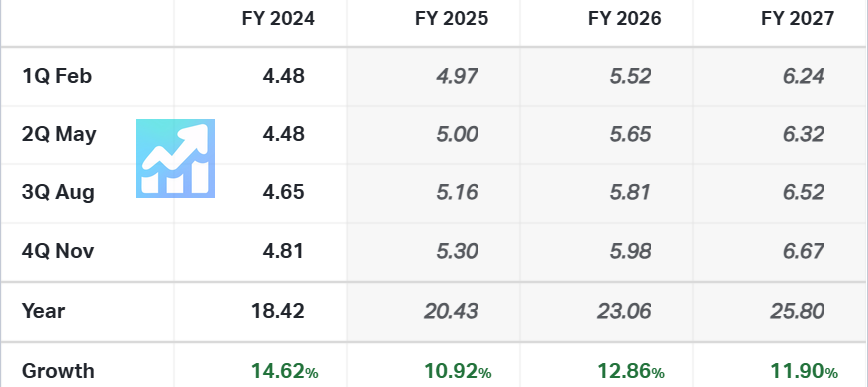

Below is the 3-year forecast for future EPS growth, which is projected to be around 11.90%. This value is lower than in previous years but still remains high.

Sales are projected to grow at a 9.77% annual rate until FY 2027. This value is lower than 10%, but personally, I believe the company will be able to beat the 10% level during the coming years.

Based on 1-year price targets offered by other analysts, the average price target for ADBE comes to $586.29. The forecasts range from a low of $425.00 to a high of $700.00. The average price target represents an increase of 36.17%.

Adobe has provided its revenue forecast (PDF) for fiscal year 2025, projecting total revenue between $23.30 billion and $23.55 billion. This estimate is lower than analysts' expectations, which were around $23.78 billion. The company anticipates facing a $200 million decrease due to foreign exchange effects and a shift towards subscription models from constant offerings.

In terms of earnings, Adobe expects adjusted earnings per share to be between $20.20 and $20.50. Despite the challenges, Adobe's leadership remains optimistic about its strategic focus on AI and cloud services, which they believe will drive future growth.

However, as I already wrote (Why Price Is Down), the disappointing forecast has led to a decline in Adobe's stock price as investors react to the potential impacts of increasing competition in the market.

💲Current Valuation

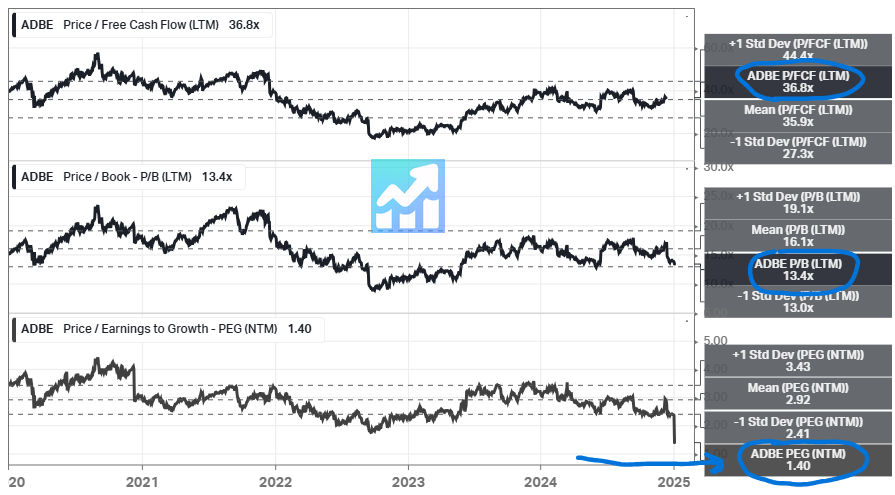

In terms of Price/Sales, Price/Earnings, and Price/Forward Earnings ratios, the company is currently trading below its 5-year average levels. Also, it is worth noting that Price/Forward Earnings and Price/Sales are low.

The PEG ratio is the lowest for the last 5-year period (1.40). In addition, below is a comparison with the software industry (IGV - iShares Expanded Tech-Software Sector ETF).

As shown in the charts above, ADBE is currently trading below the software industry.

🏷️ Fair Price

The Long-Term Pick's Fair Price (Base Case) for ADBE is $527. The current price of $422.63 is lower by almost 20%.

Fair-to-Current Price (%): 19.79%

Current Price/Fair Price: 0.80

I used:

Discount Rate: 12%

Margin of Safety: 30%

Years: 5

Future EPS Growth Rate: 11% (I lowered the 3-year EPS forecast to 11)

Future Dividend and Buyback Yield: 1.7% (I used the 5-year average shareholder yield)

Total Future Annual Growth Rate: 11 + 1.7 = 12.7%

Reviewing the historical long-term CAGR results (the Past section), my 12.7% CAGR is still below 10- and 15-year values. You may notice that it's bigger than the 5-year CAGR value, which is only 5.26%, but I believe that for such a great company as Adobe, it is doable to return back to "normal existence".

For the Base Case future exit Price/Earnings ratio, I used:

Future EPS Growth Rate x 2 = 25

(I rounded 25.4 to 25) which is still lower than the current Price/Earnings ratio (34.8) and the 5-year average value (47.1). For the Bull Case, I added 5 to the Base Case, and for the Bear Case, I subtracted 5 from the Base Case.

Thank you for being a part of Long-Term Pick! This post is public, so please consider becoming a patron of the project. Use the promo code 2025 to receive 60% off your first month of subscription. This offer is valid until the end of January.

☑️ Checklist

Profitability:

✅ Gross margin at least 40%: 89%

✅ Net margin at least 10%: 26%

✅ FCF margin at least 10%: 13%

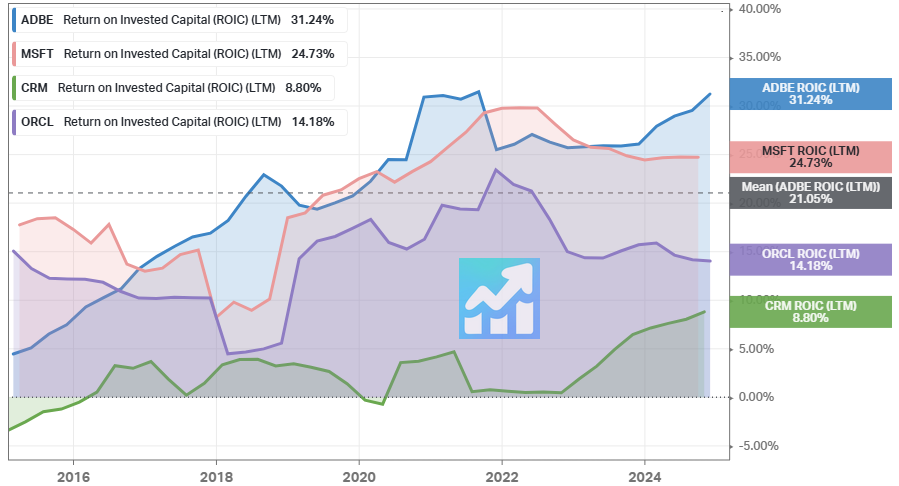

✅ Management (ROIC, ROCE, ROE, ROA): Yes (All above 10%)

🟨 Piotroski F-Score: 6 of 9 (Not passed: Higher ROA yoy, Lower Leverage yoy, Higher Current Ratio yoy)

🟨 Revenue surprises in last 7 years: No (Missed 2022; Based on TradingView's data)

🟨 EPS surprises in last 7 years: No (Missed 2018; Based on TradingView's data)

✅ EPS growth YoY 7 years in a row: Yes

Valuation and Advantage:

✅ Valuation below its 5-yr average: Yes

✅ Does it have a moat: Yes (wide)

Shares:

❌ Insider ownership at least 5%: No (0.21%)

✅ Less shares outstanding YoY: Yes

❌ Insider buys last six months: No

Price:

✅ 1-year stock price forecast is above 10%: +36.17%

✅ Next 5-yr EPS growth estimates (CAGR) is above 10%: Yes (15.05%)

❌ DCF Value: 372; Overvalued by 14% (5 years, discount rate: 10%, terminal growth: 3%, equity model: FCFE)

✅ Short Interest below 5%: Yes (1.55%)

✍️ Due Diligence

Profitability (8 of 10):

✅ Positive Gross Profit: 19.1B USD (for the last twelve months)

✅ Positive Operating Income: 7.7B USD (for the last twelve months)

✅ Positive Net Income: 5.6B USD (for the last twelve months)

✅ Positive Free Cash Flow: 2.9B USD (for the last twelve months)

✅🟨 Positive 1-Year Revenue Growth: 11% (over the past 12 months)

✅🟨 Positive 3-Year Revenue Growth: 11% (per year for the last 3 years)

✅🟨 Positive Revenue Growth Forecast: 10% (per year over the next 3 years)

✅ Exceptional ROE: 37% (for the past 12 months)

✅ Exceptional 3-Year Average ROE: 35% (three-year average)

✅ ROE is Increasing: 34% → 37% (in the last 3 years)

✅ Exceptional ROIC: 29% (for the past 12 months)

✅ Positive 3-Year Average ROIC: 25% (three-year average)

✅ ROIC is Increasing: 25% → 29% (in the last 3 years)

Solvency (7 of 10):

✅🟨 Short-Term Solvency (short-term assets (11B USD) exceed its short-term liabilities (10.5B USD))

✅ Long-Term Solvency: (long-term assets (30B USD) exceed its long-term liabilities (16B USD))

✅ Negative Net Debt: -3.8B (has more cash and short-term investments (8B USD) than debt (4B USD))

✅ Low Debt-to-Equity: 0.29 (how much debt a company is using to finance its assets relative to the value of shareholders' equity)

✅ High Altman Z-Score: 11.5 (whether a company is headed for bankruptcy - takes into account profitability, leverage, liquidity, solvency, and activity ratios)

This is not a financial or investing recommendation. It is solely for educational purposes.

If you like the content, please hit the like icon, leave a comment, and share the publication with your friends and colleagues - this will motivate the author. If you're ready to support the project and get access to additional materials, visit this page.

Thanks for the in-depth analysis, Bohdan. Adobe might start to build a bottom in the foreseeable future. That's when it could become interesting again. I tested its AI image generator recently and was impressed.