Micron at 6x Earnings: The Most Expensive Mistake

Every value screener in the world is flashing green on MU after a +650% year. Here's why the P/E is lying, and which two metrics tell the truth.

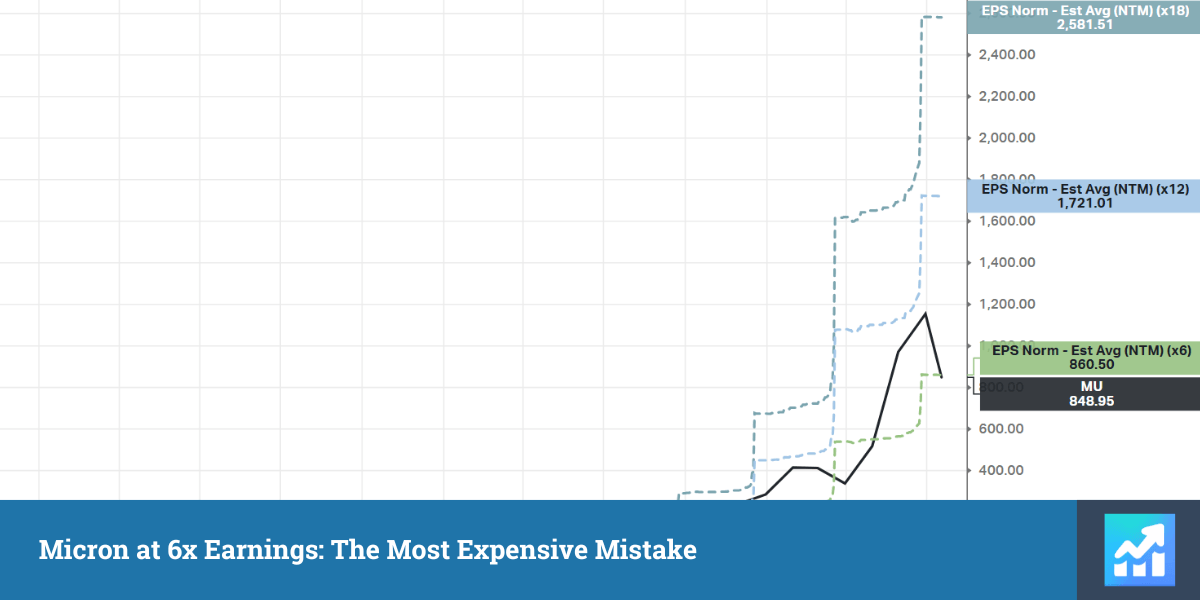

On paper, Micron is the best stock in the market. It returned +650% in a year. Gross margin jumped from 39% to 85% - the most extreme profit explosion in the memory industry’s history. It trades at 6x forward earnings, a third of Microsoft’s multiple, with a PEG of 0.04 and net cash on the balance sheet. Forty of forty-five analysts say Buy, with an average target 65% above today’s price.

I looked at all of that - and decided not to buy. Not at this price, not even close.

Here’s the short version: memory is a commodity, and commodity cyclicals look cheapest at precisely the moment they are most dangerous. A commodity is a product sold on price alone - nobody cares whose chip is inside.

The 6x P/E is not a discount - it is the market telling you it does not believe these earnings will survive. The analyst target range says the same thing louder: $361 to $2,200. The street cannot agree whether this stock should halve or double.

Below: why the P/E is lying and which two metrics tell the truth, the three signals that will mark the top of this cycle, what I’d do if I already held MU - and the exact price where I’d buy Micron aggressively with both hands.