On Holding: High Gross Margin, Geographic Expansion, and Appealing Valuation

A comprehensive analysis of On Holding AG (ONON).

Content:

• Company Overview

• Market Overview

• Economic Moat

• Business Strategy

• Capital Allocation

• Advantages

• Disadvantages

• Competitors

• Past

• Future

• Current Valuation

• Fair Price

• Checklist

• Due Diligence

• Investment Thesis

Company Overview

IPO Date: Sep 15, 2021

Market Cap: ~$16.23B

Sector: Consumer Cyclical

Industry: Footwear & Accessories

Type: Mid Growth

Total Number of Employees: ~3,200

Next earnings report: Mar 3rd, 2026 (estimated, pre-market)

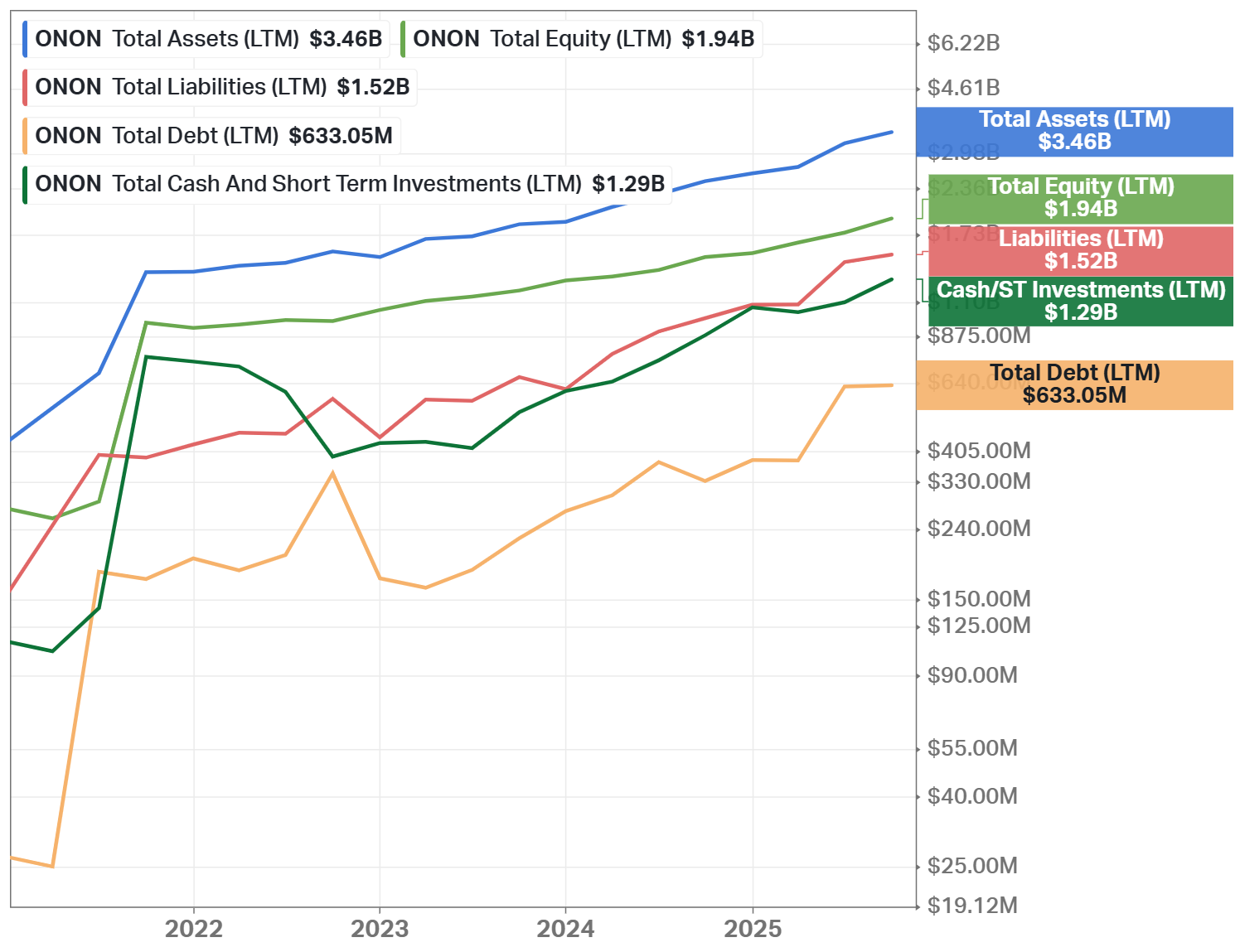

Total Debt: $633M

Cash & Investments: $1.29B

Beta: 2.15

Website: www.on.com

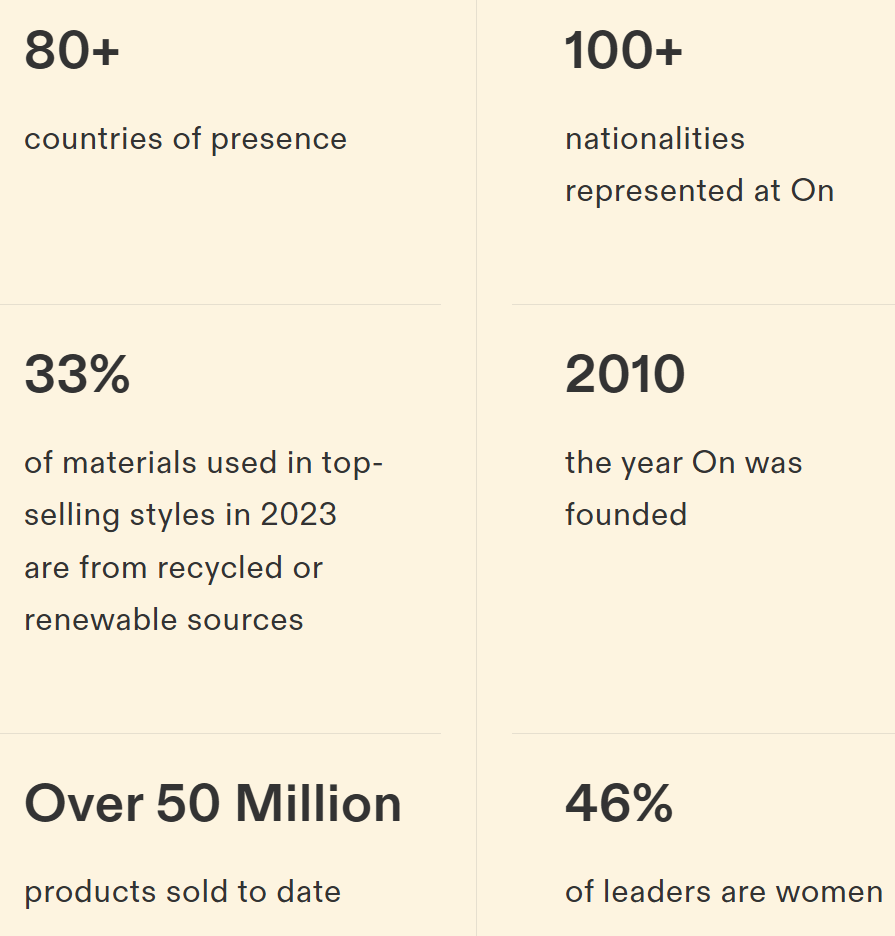

On Holding AG (NYSE: ONON) is a Swiss premium sportswear company founded in 2010 by former professional triathlete Olivier Bernhard, together with David Allemann and Caspar Coppetti. The company was built around proprietary CloudTec® cushioning technology, designed to reduce impact and improve running efficiency. On focuses primarily on performance footwear while steadily expanding into premium apparel and accessories (representing approximately 7% of total revenue) to build a complete sportswear ecosystem.

On’s Chief Innovation Officer Scott Maguire:

Innovation at On is about obsessively making the best possible products that push the limits of sensation and performance. The fusion of SURREAL foam and CloudTec cushioning is our superpower. This is a fundamental enhancement to our core technology that we believe will elevate the experience for runners of all kinds.

To Read: The On story

On sells its products in more than 80 countries through a balanced mix of direct-to-consumer (DTO) and wholesale channels. This hybrid model allows the company to control brand experience while reaching global scale. The company operates flagship and brand stores in cities such as Zurich, New York, Tokyo, and Palo Alto, which serve as both retail and marketing hubs.

Co-Founder Caspar Coppetti:

From the first prototype in the Swiss Alps to the global stage, On was built on the belief that performance can be redefined when form and function come together in new ways. The fusion of SURREAL foam and CloudTec cushioning will revolutionize the running sensation for years to come.

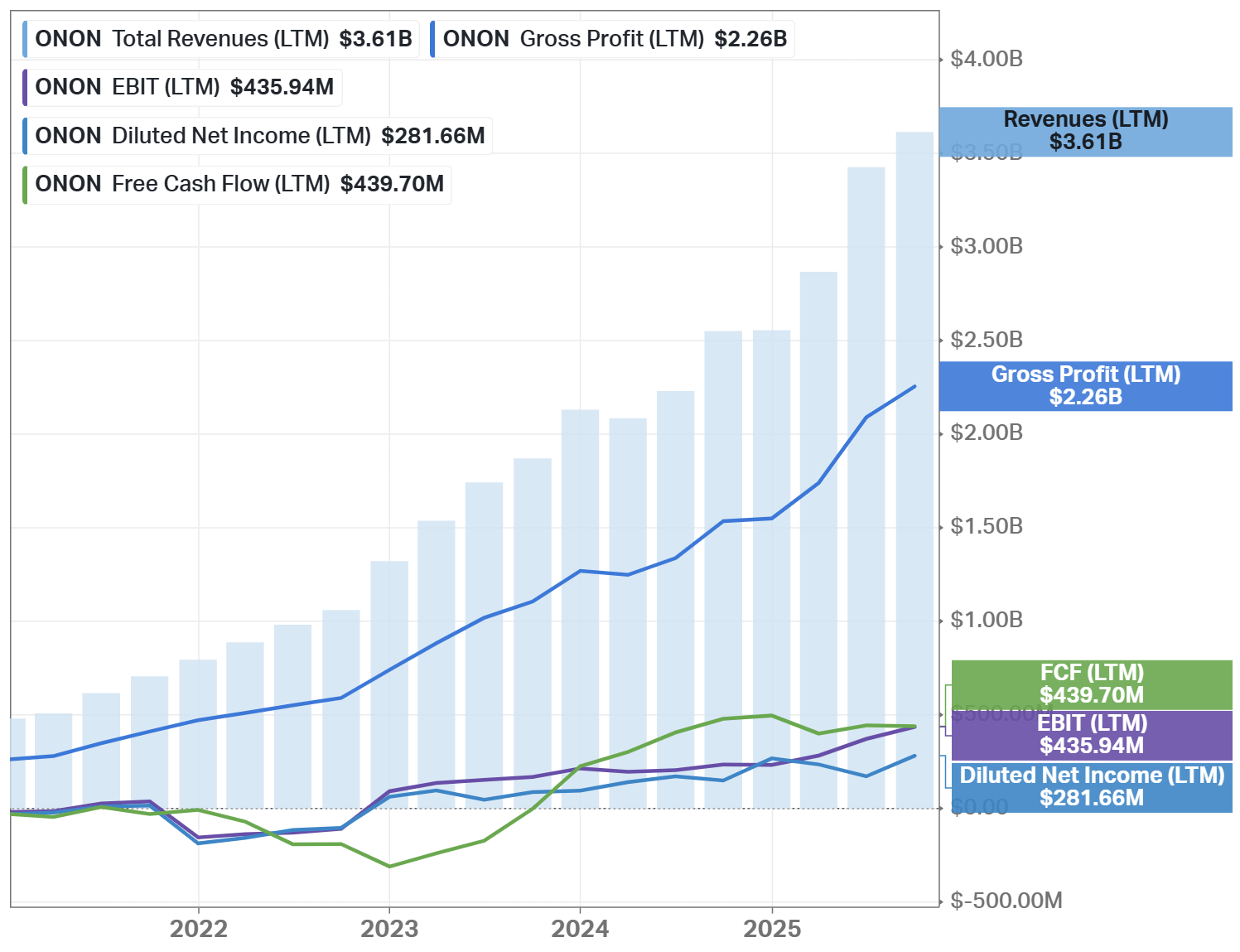

In Q3 2025, On reported net sales of CHF 794.4 million, representing 24.9% year-over-year growth and 34.5% growth on a constant currency basis. Footwear remained the largest revenue contributor, while apparel showed accelerating momentum. Growth was broad-based across regions and channels, confirming strong global demand.

The company is led by Martin Hoffmann, who serves as both CEO and CFO. Hoffmann joined On in 2013 and has a strong background in finance and operations. Under his leadership, the company expanded gross margins, improved adjusted EBITDA, and maintained a conservative balance sheet, while continuing to invest heavily in innovation and brand development.

On’s clients include elite athletes, professional runners, and premium lifestyle consumers. The brand sponsors top athletes such as Hellen Obiri. It serves everyday consumers through its digital platform and premium retail partners.

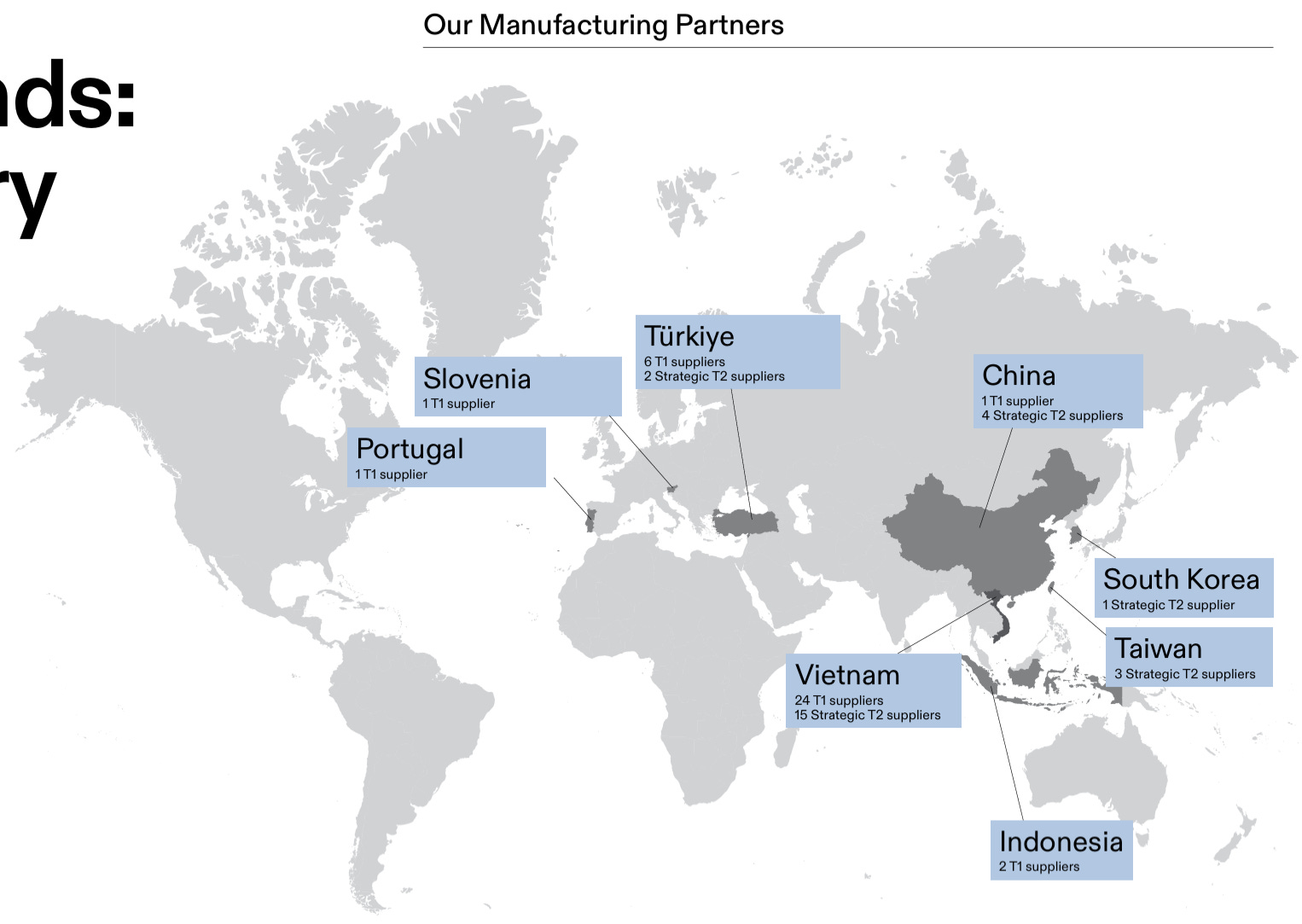

Manufacturing is outsourced to third-party partners (primarily in Vietnam and China), while product design, R&D, and quality control remain in-house.

Market Overview

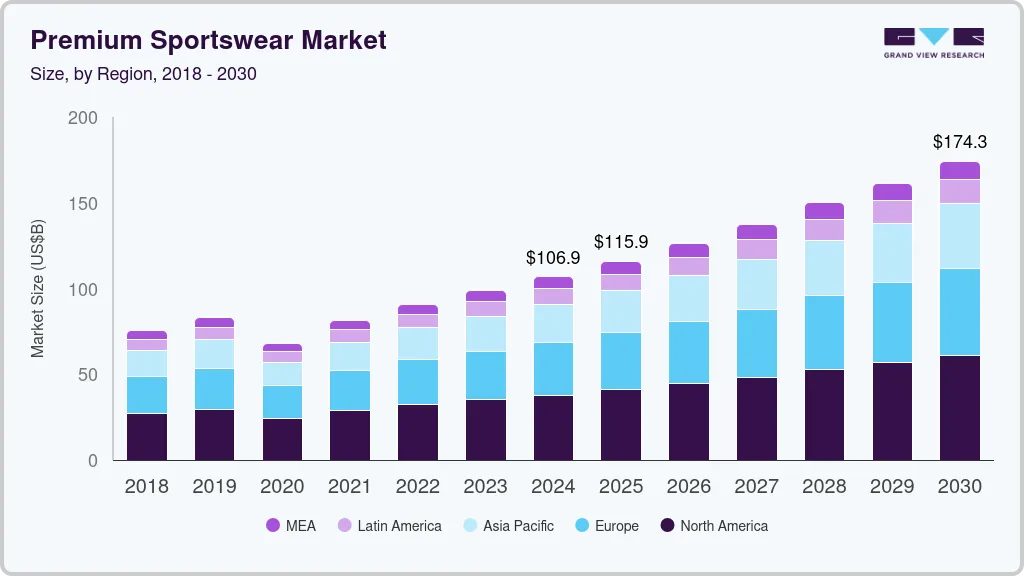

According to Grand View Research, the global premium sportswear market size was estimated at USD 106.9 billion in 2024 and is anticipated to reach USD 174.3 billion by 2030, growing at a CAGR of 8.5% from 2025 to 2030. The research from Deep Market Insights shows a similar number: 8.9%. And according to another research firm (Research and Markets), the CAGR until 2030 is 6.5%.

The market is driven by factors such as rising health consciousness, increasing participation in fitness activities, and the growing trend of athleisure, where high-end athletic apparel is worn in both workout and casual settings.

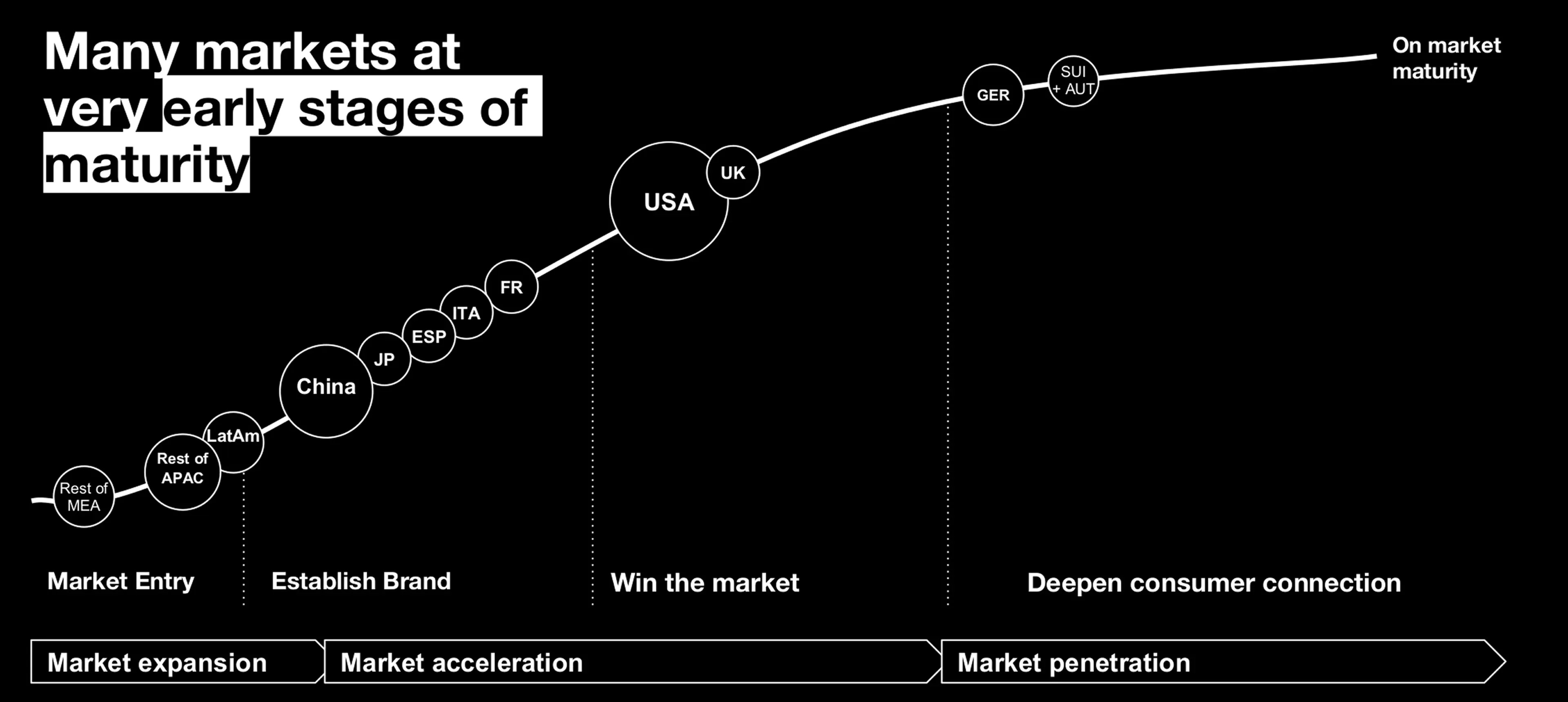

According to On’s presentation (PDF), they are still at an early stage of market maturity in many regions. Markets such as China, Japan, Southern Europe, Latin America, and parts of Asia-Pacific are shown in the early phases of brand establishment and market acceleration. Even in the United States, which is On’s largest market today, the brand is positioned in the “win the market” phase rather than full maturity. This indicates that On’s current revenue base reflects partial penetration, with significant room to grow through deeper consumer connection, broader distribution, and repeat purchases over time.

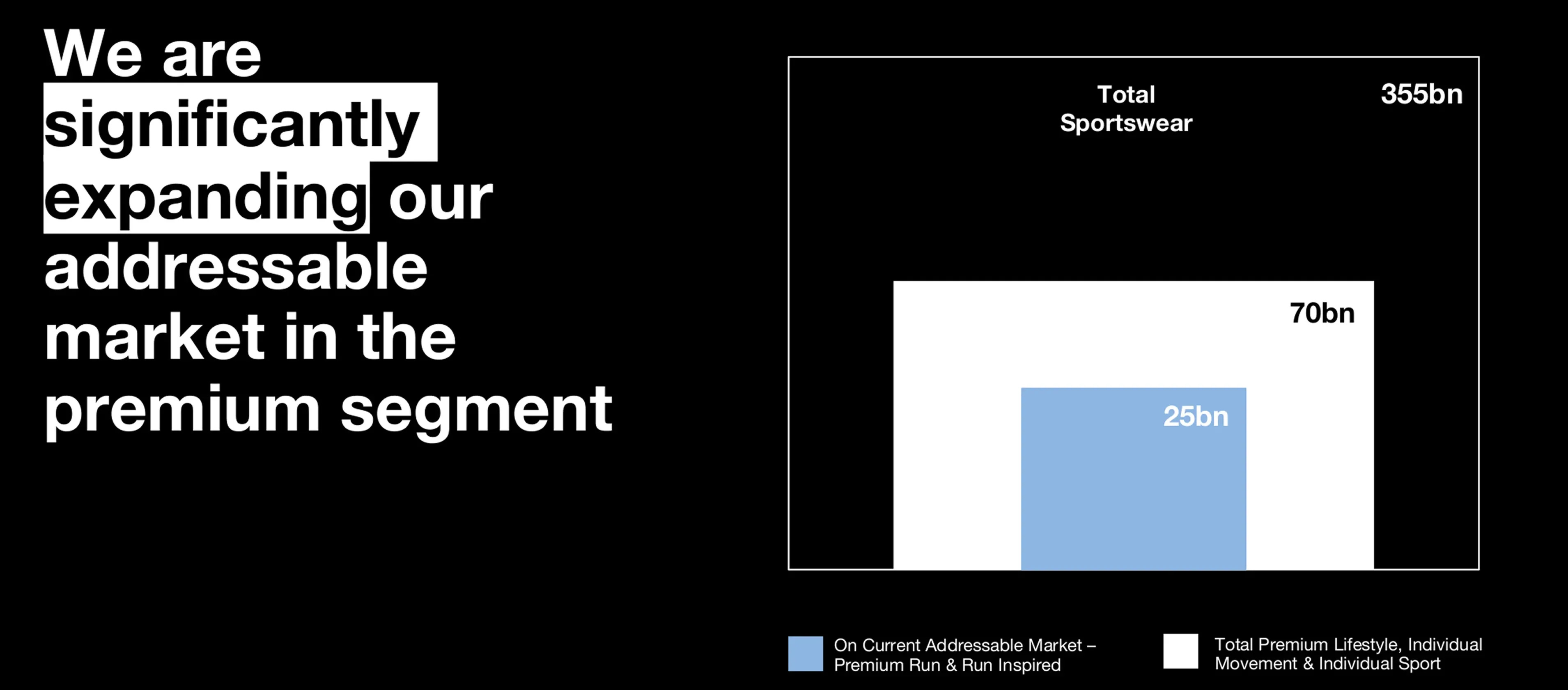

According to the presentation, On’s addressable market (premium segment) is about $25 billion. The total global sportswear is shown at approximately $355 billion, while the broader premium lifestyle, individual movement, and individual sport segment is estimated at around $70 billion.

Analyst’s Note:

The latest company presentation (the PDF URL above) is dated as of 2023, so it is a bit outdated for the moment. The next investor presentation is expected soon in January.

Economic Moat

The company has a narrow economic moat supported by innovation, brand strength, and premium pricing. As already mentioned, its proprietary CloudTec® technology differentiates the brand and supports pricing power, contributing to a 65.7% gross margin in Q3 2025, materially higher than most mass-market competitors.

Another innovation - LightSpray™ technology, which automates spray-on uppers, reducing material waste and production time. This improves cost efficiency while supporting sustainability targets, making the technology strategically valuable.

Brand credibility strengthens customer trust. As I mentioned earlier, On-sponsored athlete Hellen Obiri won the New York City Marathon in both 2023 and 2024, and On athletes secured gold medals at the World Athletics Championships.

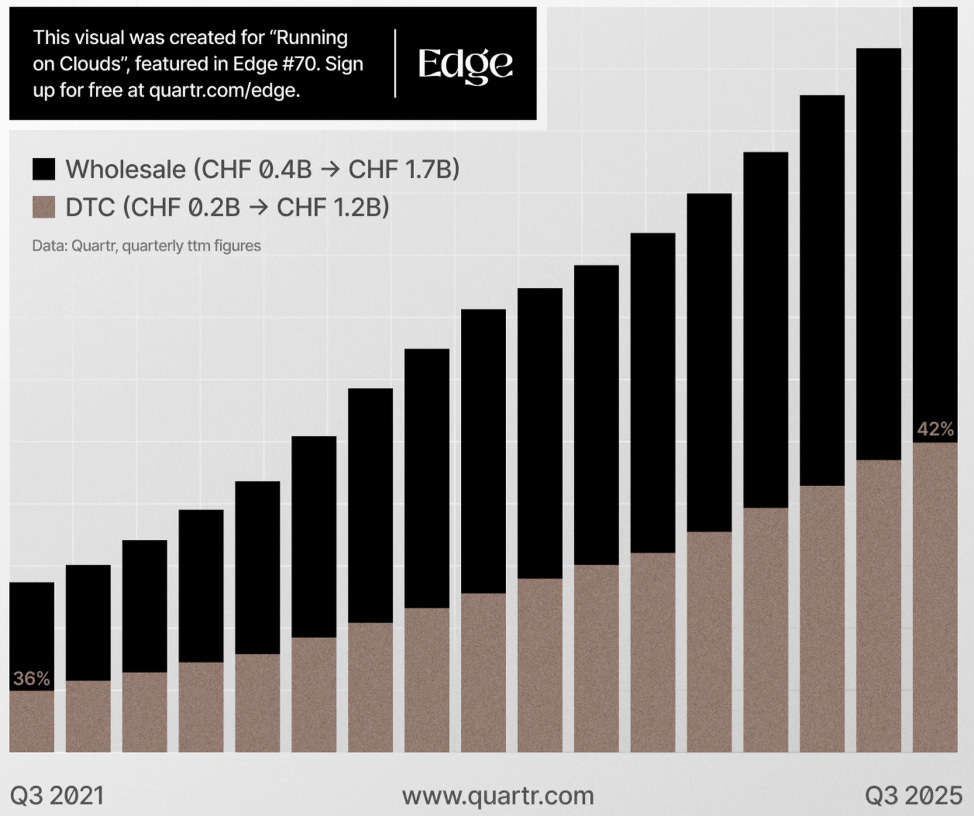

DTC growth increases switching costs. DTC sales reached CHF 314.7 million in Q3 2025, improving control over pricing, customer data, and brand experience, which deepens long-term relationships.

Business Strategy

On’s strategy focuses on premium positioning, innovation-led growth, and global expansion. Footwear remains the core of the business, while apparel and accessories are scaled to increase customer lifetime value and reduce reliance on a single category.

In Q3 2025, apparel sales grew 86.9% year-over-year, significantly faster than footwear. This confirms strong product acceptance and supports long-term category diversification.

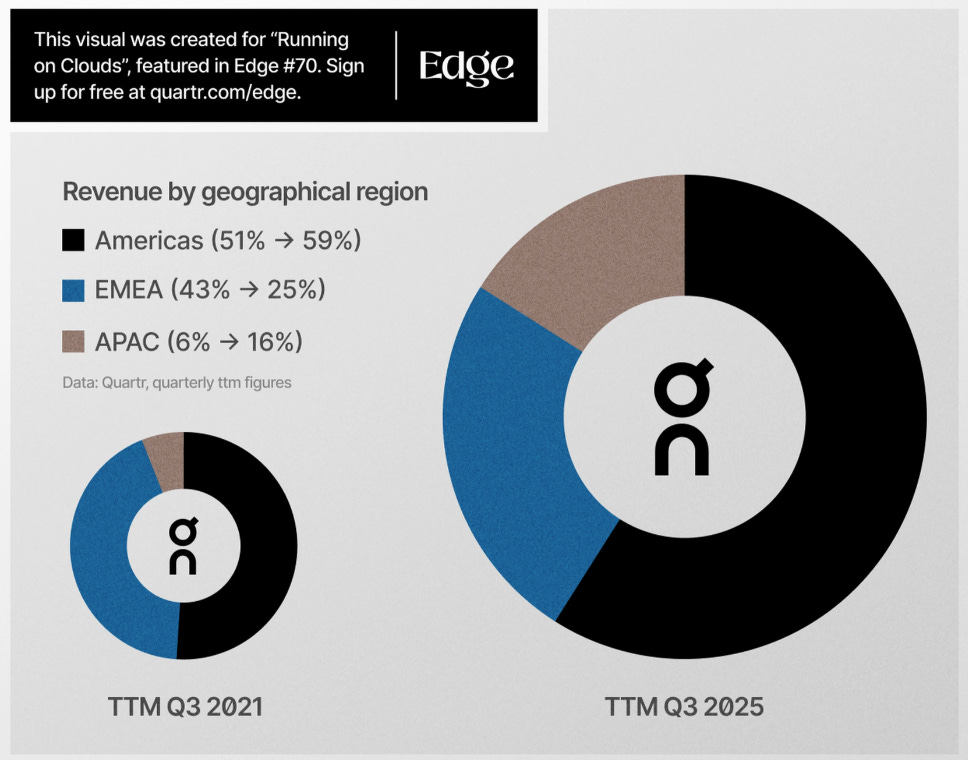

Asia-Pacific expansion is a key growth region. The region delivered over 90% growth, reducing dependence on mature Western markets and expanding long-term optionality.

On also prioritizes DTC expansion. The company improves margin quality and customer engagement.

Operational discipline. Management avoids aggressive discounting and focuses on supply-chain efficiency, digital capabilities, and selective retail expansion to protect premium brand perception.

Capital Allocation

As I wrote above, On follows a conservative and disciplined capital allocation strategy. As of September 30, 2025, the company held CHF 961.8 million in cash and cash equivalents, providing strong financial flexibility and downside protection.

Capital is primarily allocated to innovation, brand marketing, and DTC infrastructure rather than debt-funded expansion.

Analyst’s Note:

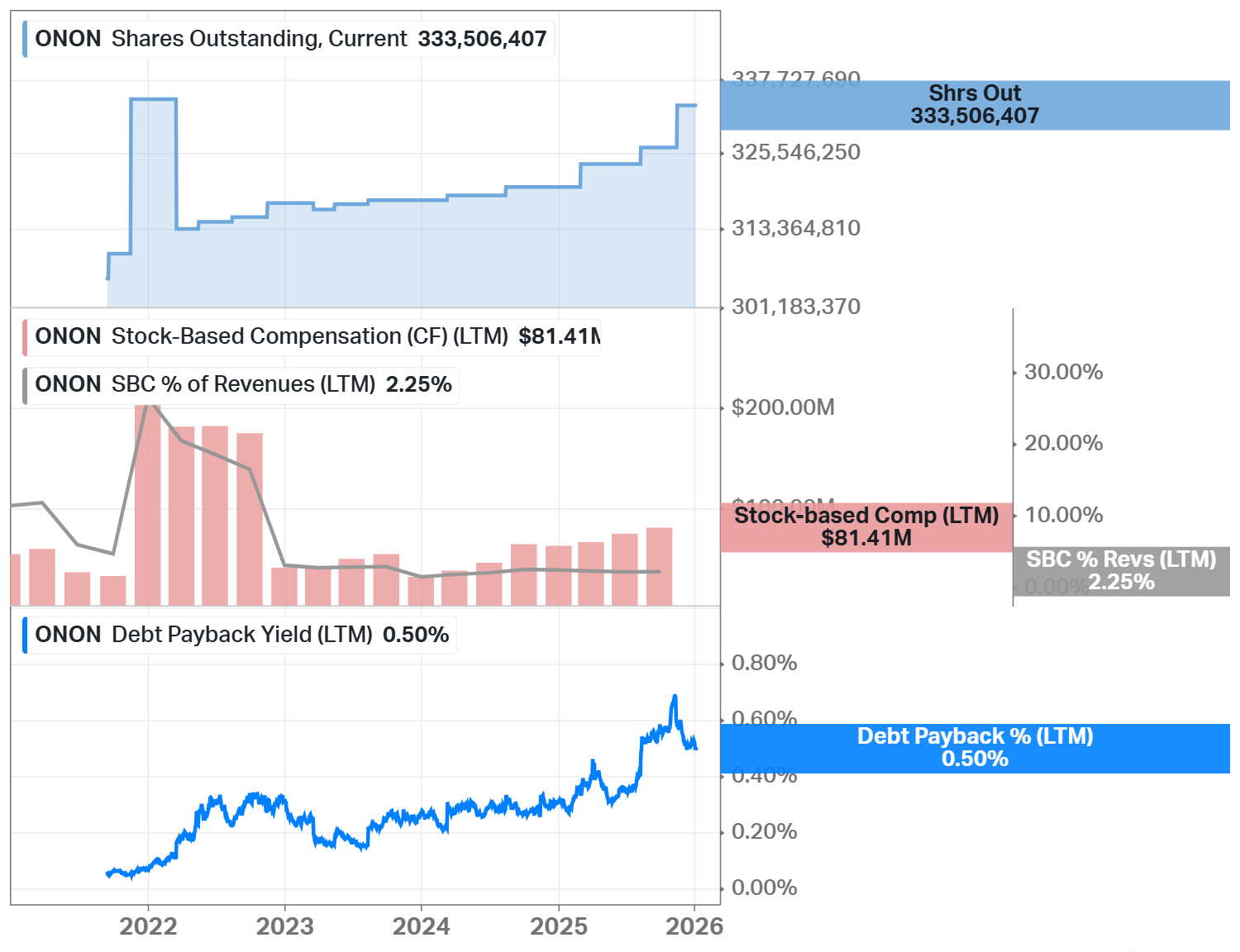

Since I use Koyfin’s data for my charts, the shares outstanding (the chart below) have been increasing, but other resources show that the number decreased during the latest quarter, so in the sections Checklist and Due Diligence, I decided to choose the decreasing option.

Limited reliance on debt reduces financial risk and preserves optionality. Over time, strong cash generation could support selective shareholder returns once growth investments normalize.

On has not engaged in share buyback activity and does not pay dividends. The company is currently focused on growth rather than returning capital to shareholders.

Advantages

Analyst’s Note:

Below, I repeat the numbers I already provided above to emphasize my point of view regarding the company’s advantages.

Strong and consistent revenue growth. Net sales increased 24.9% year-over-year in Q3 2025, supported by demand across regions and channels. This confirms the brand resonates globally and is not limited to niche performance runners.

High gross margins. The 65.7% gross margin reflects premium pricing and strong brand equity. This allows continued investment in innovation and marketing while maintaining profitability.

Product diversification. Apparel sales grew 86.9% year-over-year, reducing dependence on footwear. Over time, this supports higher customer lifetime value and more stable revenue.

Geographic diversification. Asia-Pacific growth above 90% shows strong traction outside Europe and North America. This reduces regional concentration risk and expands long-term growth potential.

Brand credibility. Roger Federer, a shareholder and long-term collaborator, adds global visibility and trust, while elite athletes’ wins strengthen performance authenticity.

To Read: How Roger Federer’s On Investment Made Him a Billionaire

Disadvantages

Premium consumer demand. During economic slowdowns, discretionary spending on high-priced footwear and apparel may decline faster than in mass-market segments.

Operating expenses continue to rise as the company invests in growth. Marketing, retail expansion, and technology spending support long-term positioning but may pressure margins if growth slows.

Foreign exchange volatility affects reported results. Global operations expose the company to currency movements that can distort short-term financial performance.

Apparel and accessories remain smaller contributors to total revenue. Despite high growth, execution risk remains as these categories scale.

Competition from global sportswear leaders remains intense. Larger rivals benefit from scale, marketing budgets, and distribution power, which can pressure pricing and market share.

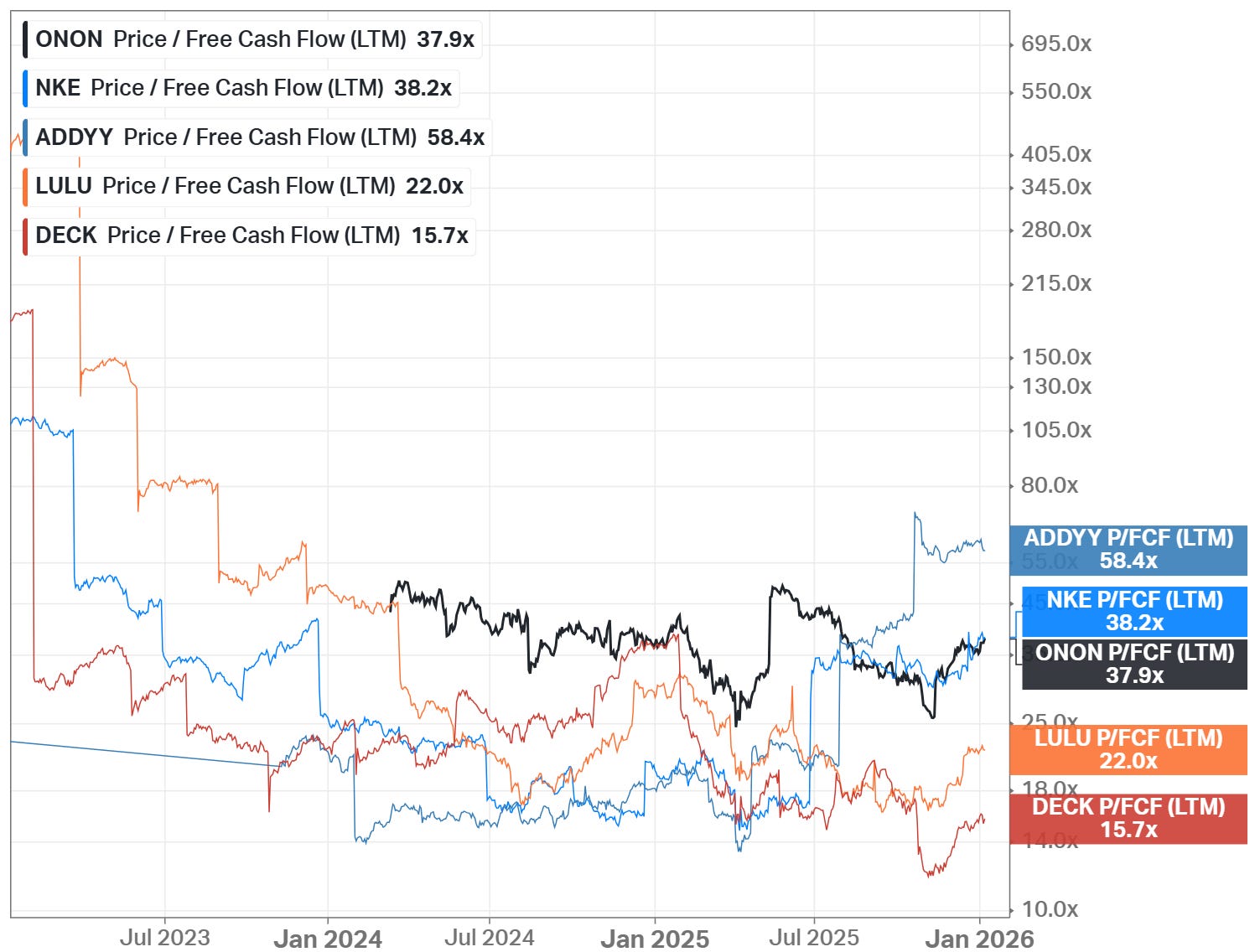

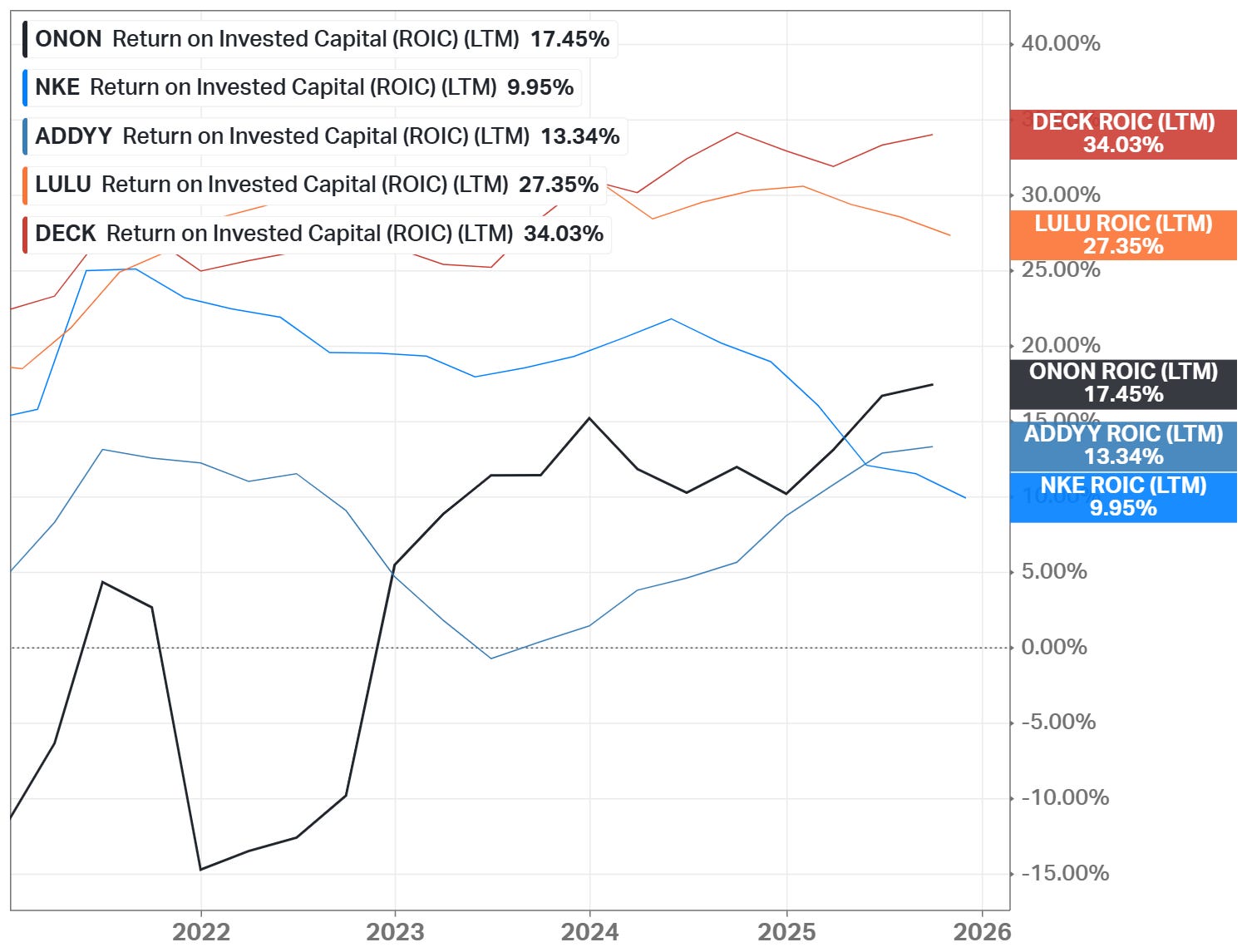

Competitors

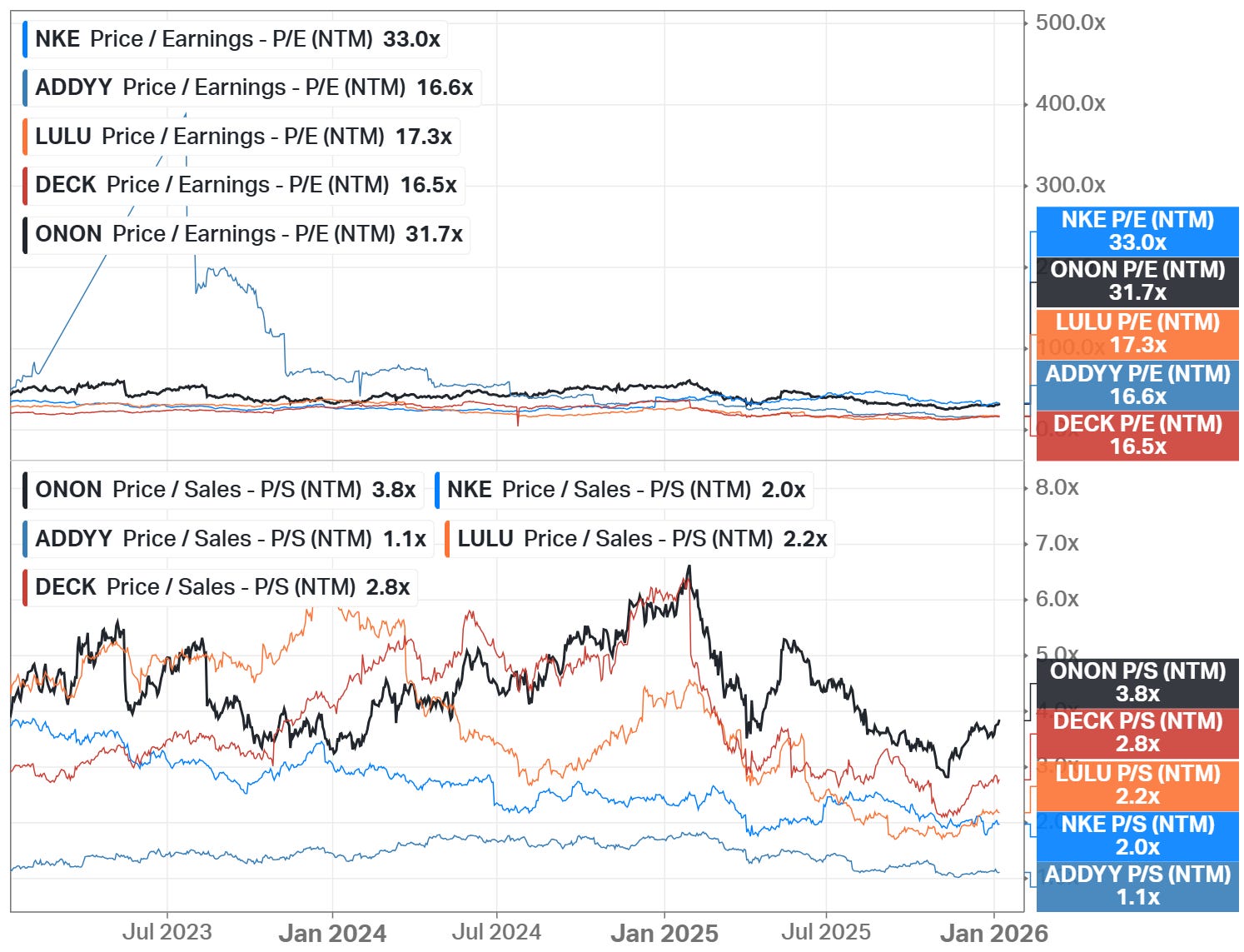

Nike (NYSE: NKE) dominates global sportswear through scale and distribution. Compared to Nike, On is much smaller but grows faster and operates at higher gross margins due to its premium focus. Nike targets mass-market volume, while On prioritizes performance-driven and premium consumers.

Adidas (ADS.DE, OTC: ADDYY) competes directly in performance footwear and apparel. Adidas benefits from global scale, but On differentiates through proprietary technology and stronger pricing power in the premium segment.

Deckers Outdoor (NYSE: DECK), through its HOKA brand, is one of On’s closest competitors in performance running. Both target serious runners, but On positions itself higher on design and lifestyle appeal, while HOKA focuses more on maximal cushioning and performance-first messaging.

Lululemon Athletica (NASDAQ: LULU) overlaps mainly in premium apparel rather than footwear. While Lululemon has strong brand loyalty, On’s footwear-led ecosystem and technical credibility create differentiation as apparel expands.

In my view, while competition is intense, On stands out through innovation, premium positioning, disciplined execution, and strong global momentum, even though its scale remains smaller than industry leaders.

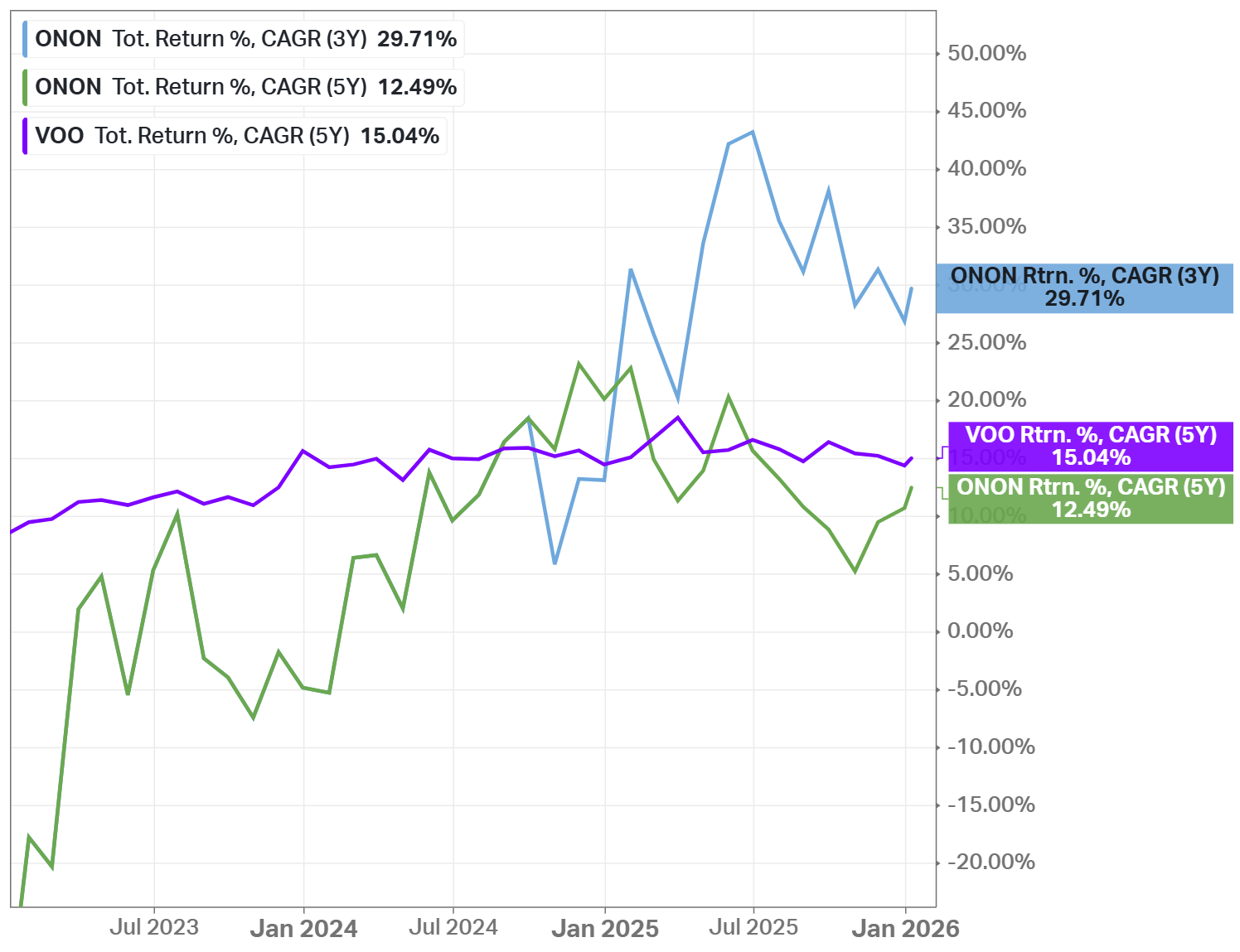

Past

Since the company went IPO only in 2021, I used only 3- and 5-year periods. The stock overperforms the S&P 500 on the 3-year period, and underperforms on the 5-year period.

Below are some significant recent events.

Raised Annual Targets: On Holding raised its annual revenue target after reporting a blowout quarter with strong demand for its running shoes, despite price increases.

Leadership Transition: On announced that its Chief Operating Officer, Sam Wenger, will step down at the end of the first quarter of 2026, and Scott Maguire, who joined On in 2025 with experience at Specialized Bicycle Components and Dyson, will take over expanded operational responsibilities.

Institutional Buying and Ownership Growth: Major institutional investors such as Winslow Capital, Sands Capital, Norges Bank, Ameriprise Financial, and State Street expanded their stakes in ONON.

No Deep Holiday Discounts Strategy: On executives indicated that the company would not offer deep discounts during holiday promotional periods despite strong sales growth, choosing to prioritize brand value and margin protection amid high demand.

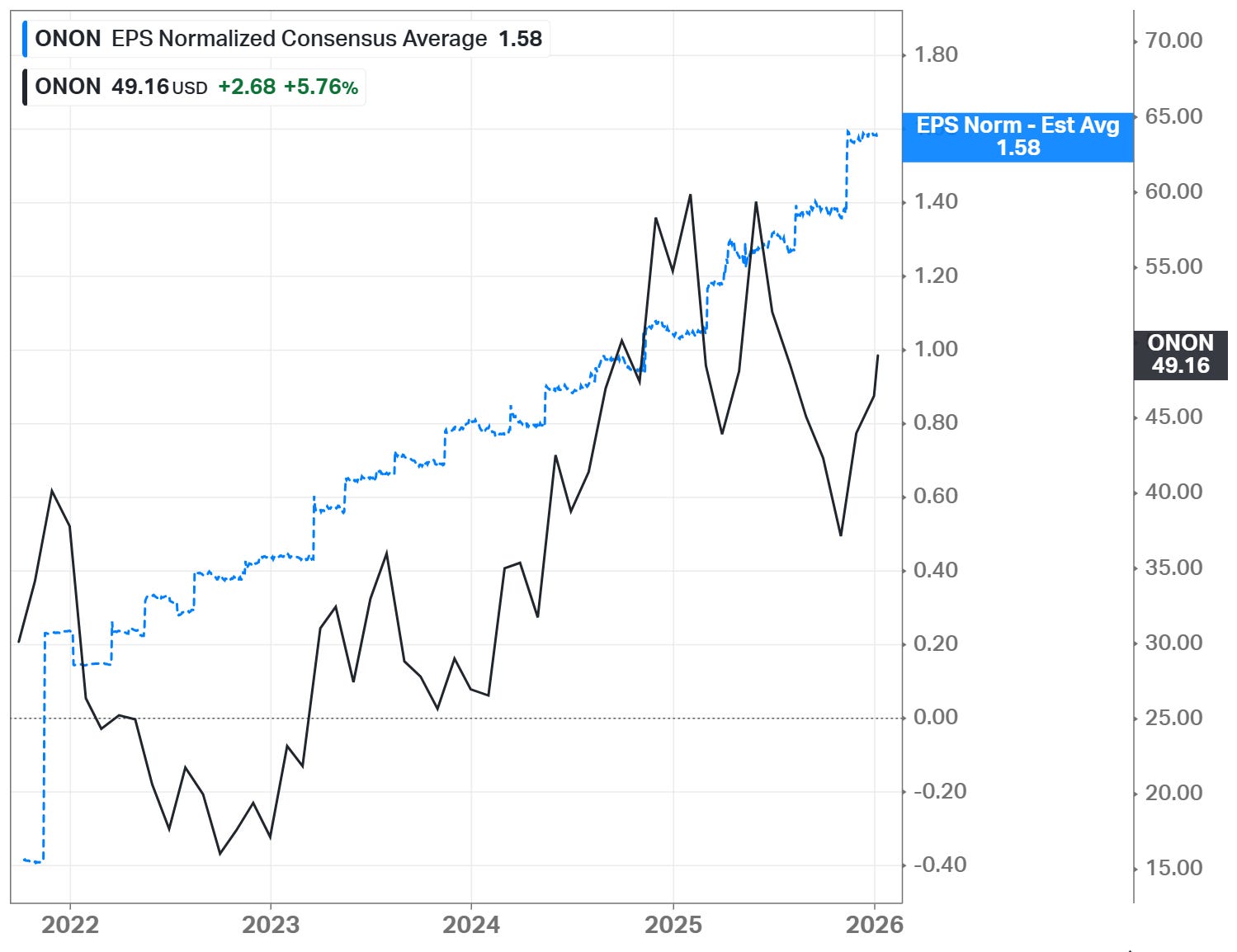

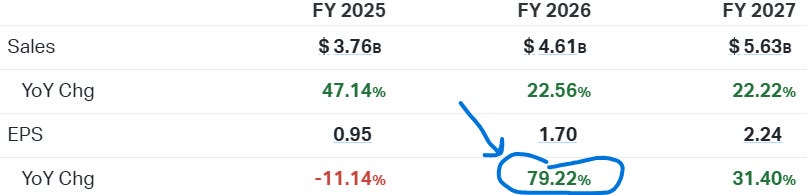

Future

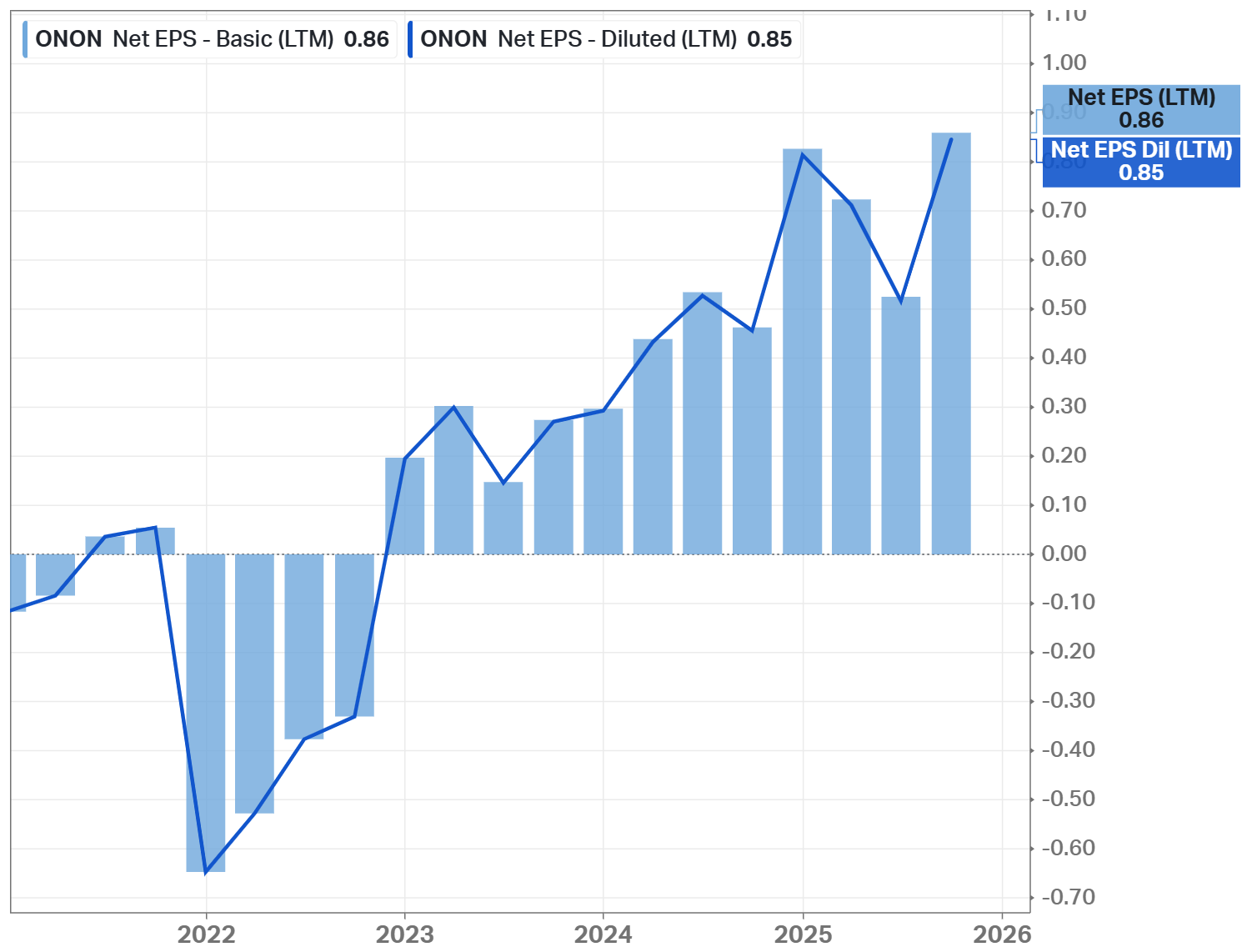

Below is the 3-year forecast for future sales and EPS growth. Pay attention to the EPS growth rebound in FY 2026 and the high value in FY 2027.

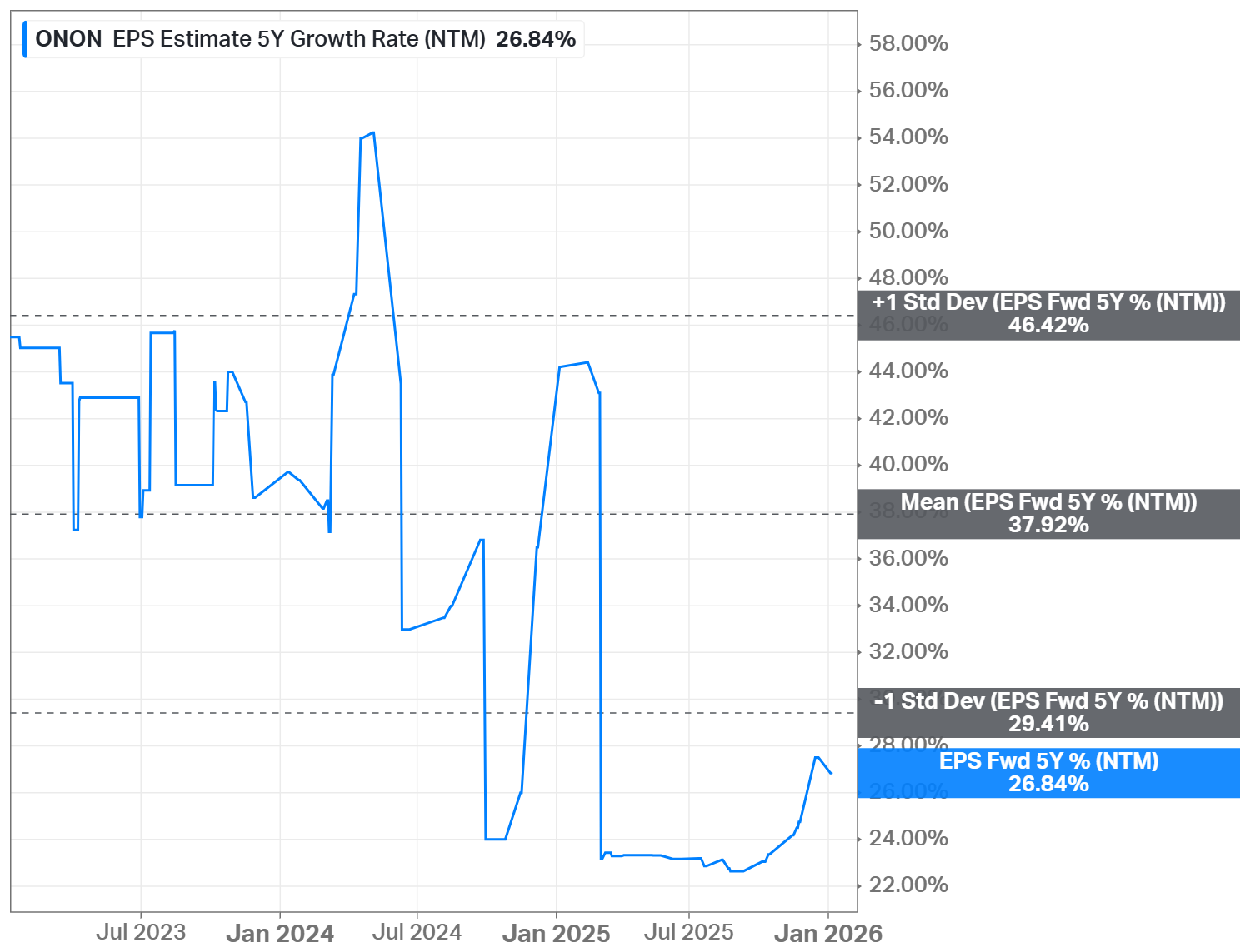

In addition, below is the EPS growth rate estimate for the next 5 years (CARG).

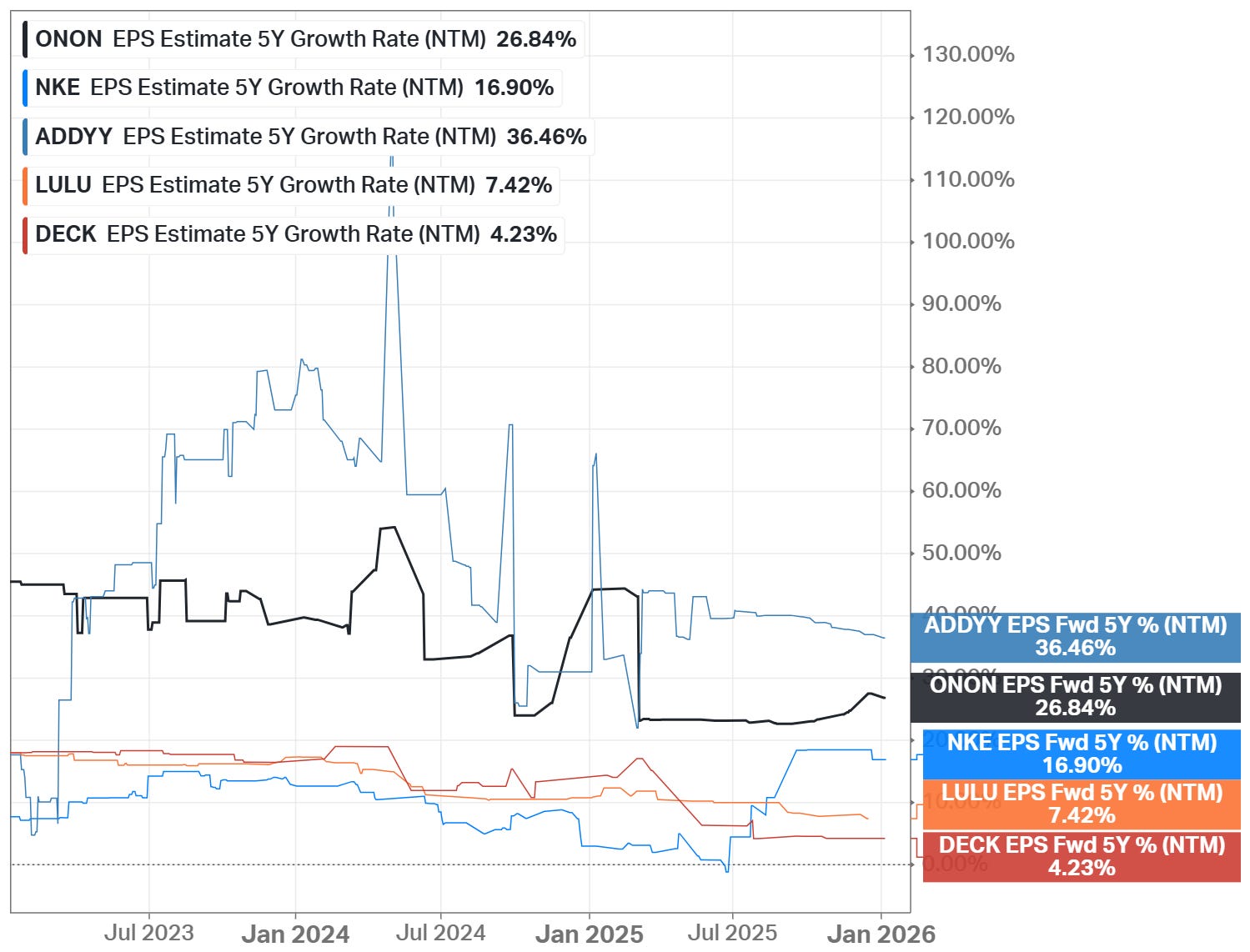

Comparison of the EPS growth rate with the competitors:

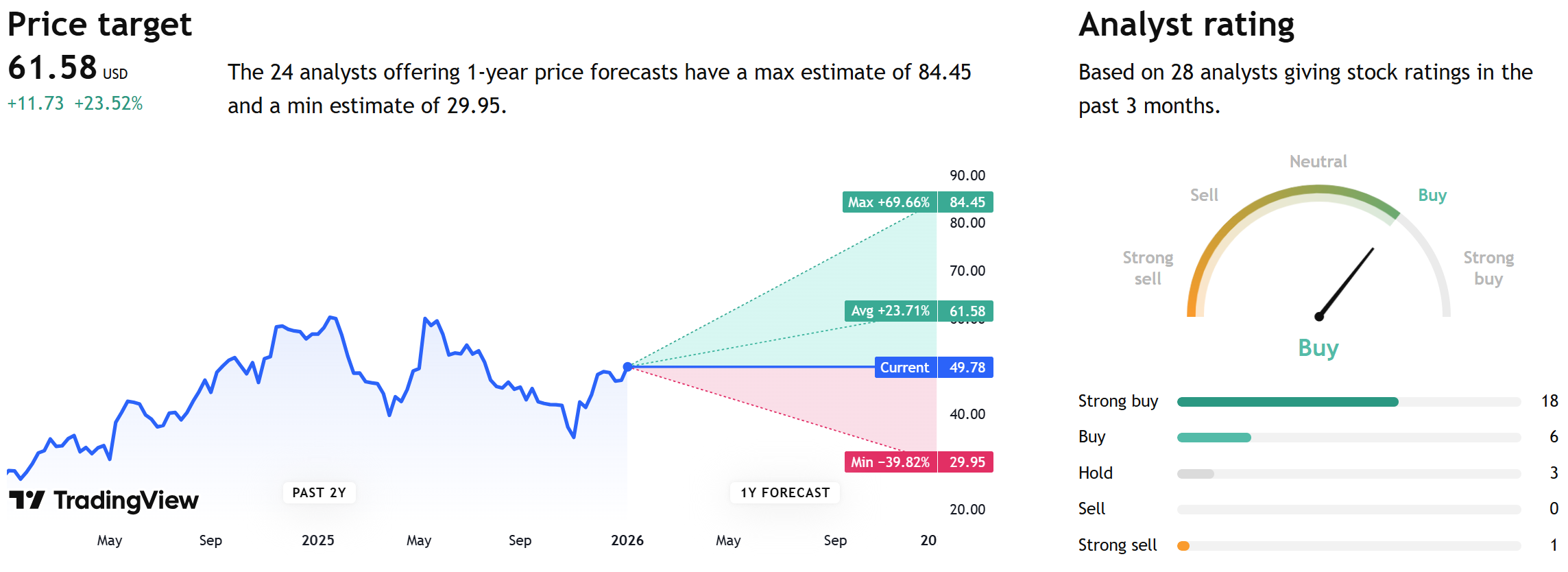

Based on 1-year price targets offered by other analysts, the average price target for ONON comes to $61.58. The average price target represents an increase of 23.71%.

Current Valuation

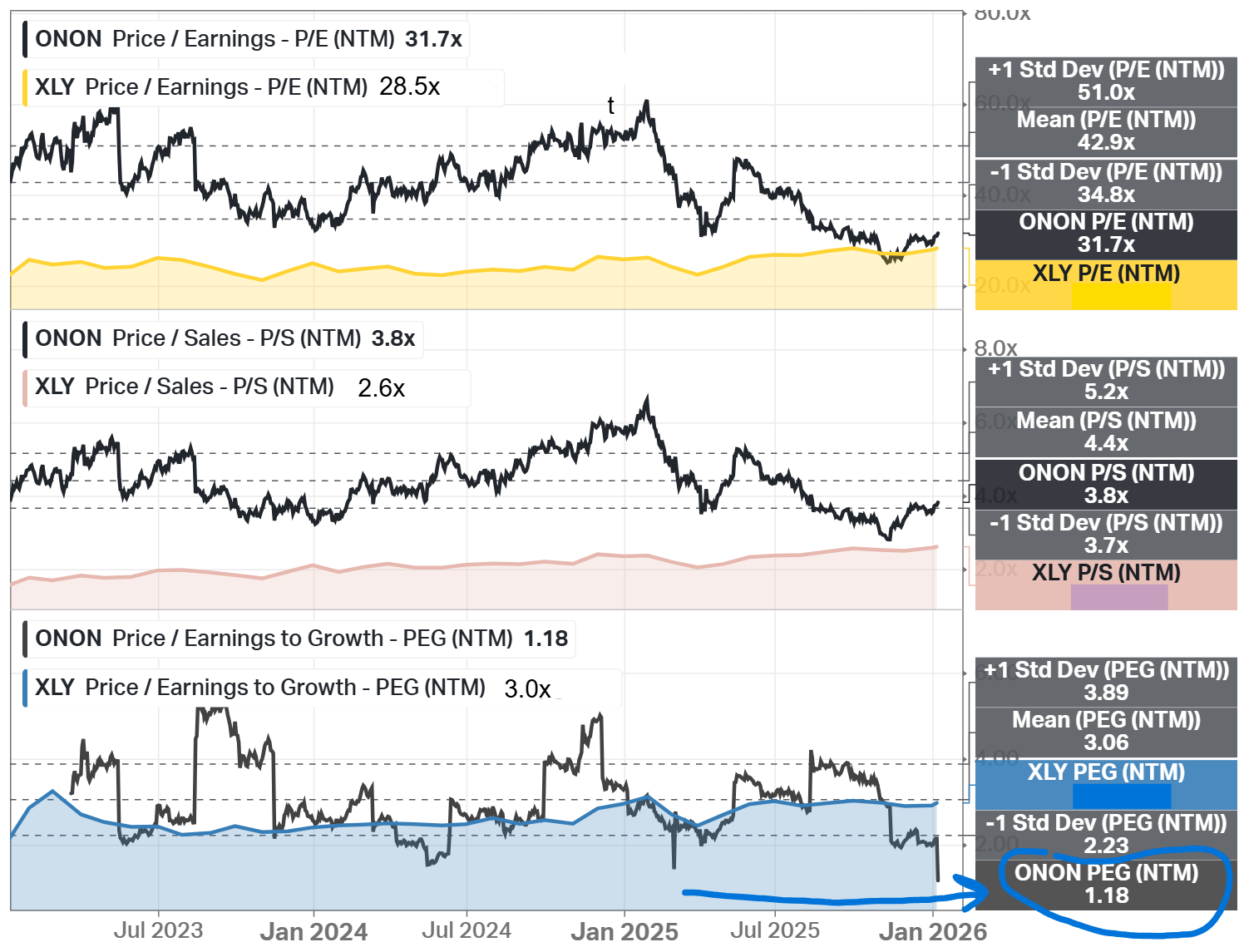

Below you will find charts with the current 3-year average valuation comparison, along with the comparison to the sector (Consumer Discretionary). The company trades below its 3-year averages. The current PEG ratio is only 1.18.

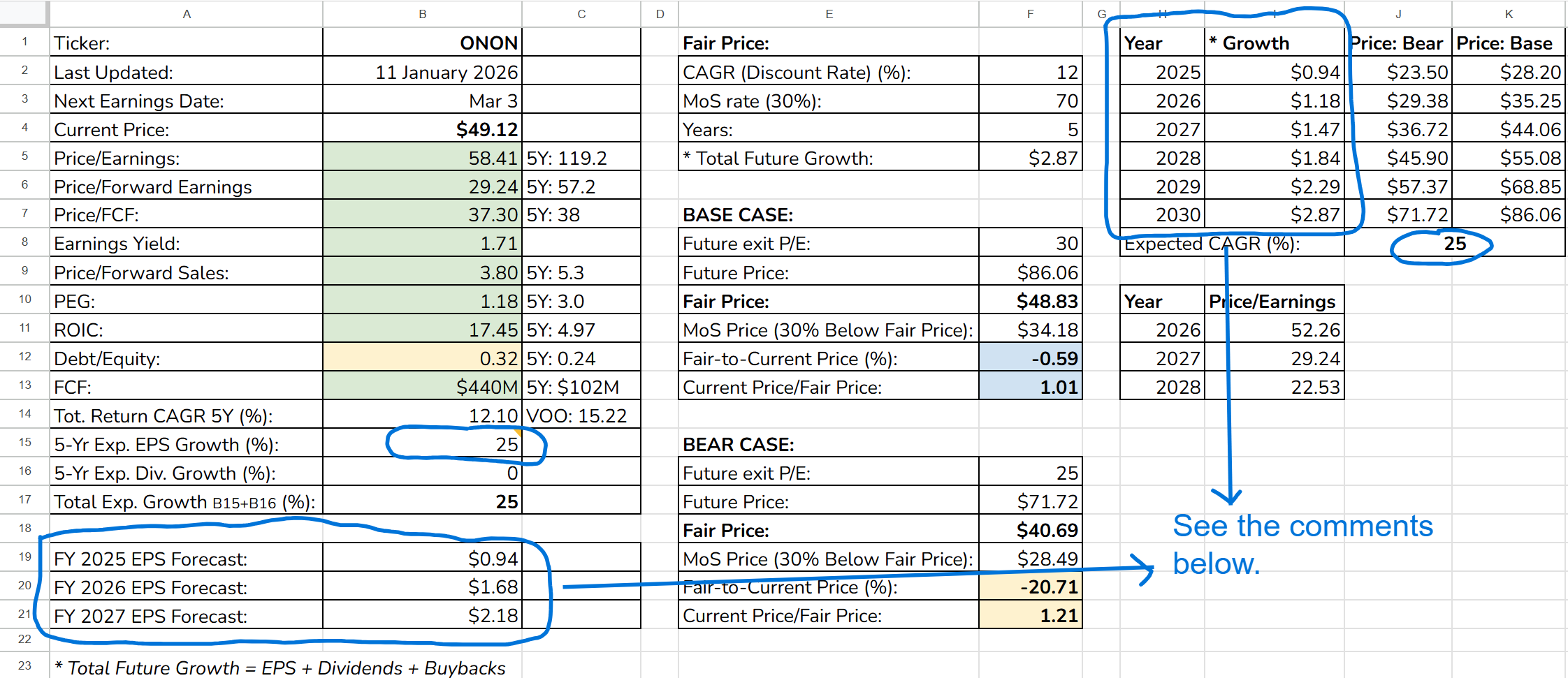

Fair Price

The Long-Term Pick’s Fair Price (Base Case) for ONON is $48.83. The current price of $49.12 is higher by less than 1%, so the stock is fairly valued.

Fair-to-Current Price (%): -0.59%

Current Price/Fair Price: 1.01

I used:

Discount Rate: 12%

Margin of Safety: 30%

Years: 5

Future EPS Growth Rate: 25% (explanations below)

Future Dividend Yield: 0%

Total Future Annual Growth Rate: 25 + 0 = 25%

As the exit Price/Earnings ratio for the Base Case, I used 30, since this is a growth business. For the Bear Case, I subtracted 5 from the Base Case. Notably, the stock has never traded below a Price/Earnings ratio of 40.

Usually, my maximum 5-Yr Expected EPS Growth value is 20, so even if a stock has more than this value, I always set 20. In the case of On, I used 25, since with my default value of 20, there would be a big gap in future EPS representation year-over-year (the right part in the screenshot above). Even with a value of 25, pay attention that my future EPS projection (the right part in the screenshot above) is still below the levels for the next three financial years (the left part in the screenshot above).

Checklist

Profitability:

✅ Gross margin at least 40%: 62.4%

❌ Net margin at least 10%: 7.8%

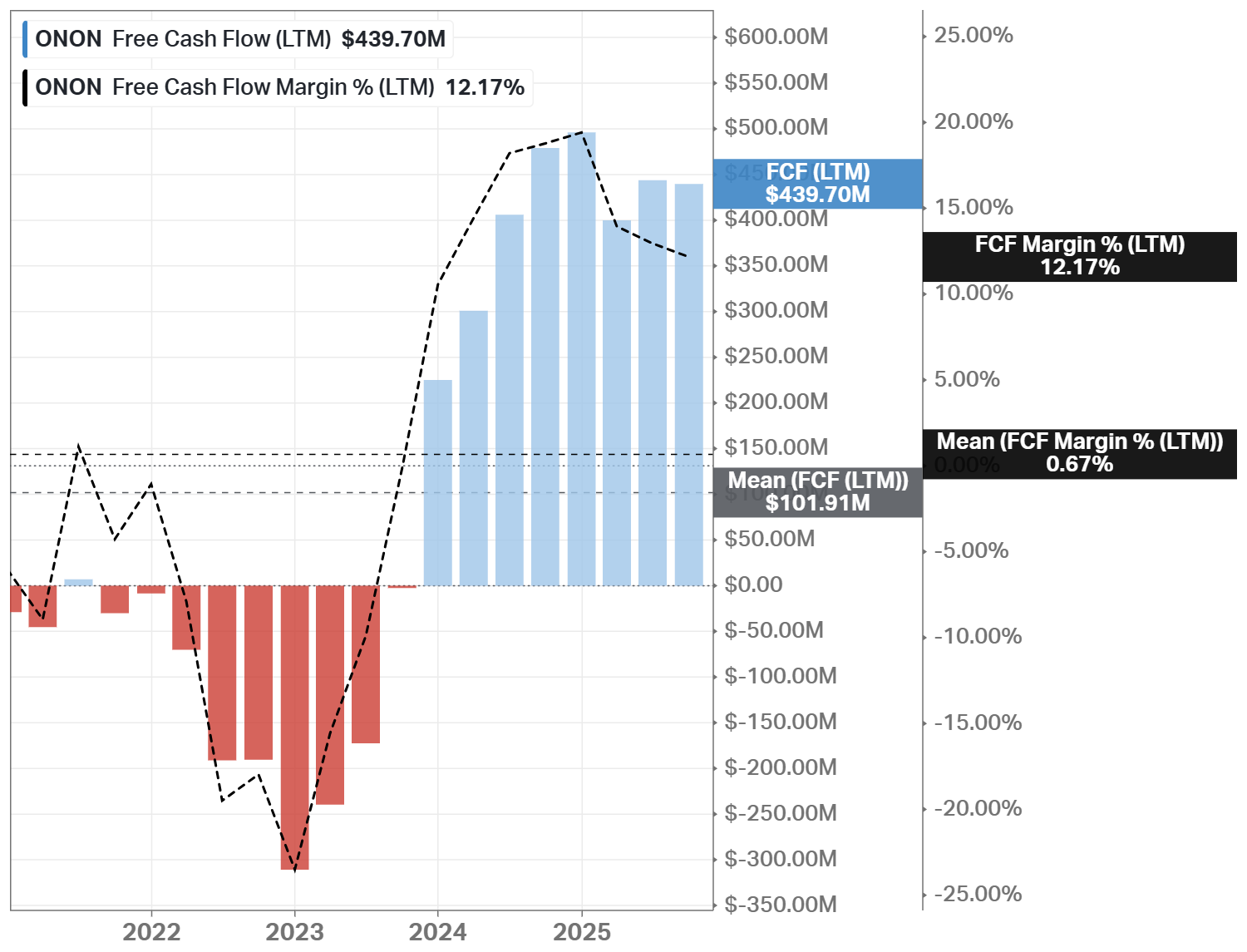

✅ FCF margin at least 10%: 12.0%

✅ Management (ROIC, ROCE, ROE, ROA): Yes (All above 10%, except ROA)

✅ Piotroski F-Score: 7 of 9 (Not passed: Lower Leverage yoy, Higher Current Ratio yoy)

❌ EPS surprises in the last 5 years: No (Missed in 2021 and 2023; Based on TradingView’s data)

✅ EPS growth YoY 5 years in a row: Yes (Based on TradingView’s data)

Valuation and Advantage:

✅ Valuation below its 5-year averages: Yes

❌ Valuation below the sector: No

✅ Does it have a moat: Yes (narrow)

❌ Outperformed the S&P 500 CAGR: No (3-year yes, but 5-year didn’t)

Shares:

✅ Insider ownership at least 5%: Yes (9.54%)

✅ Less shares outstanding YoY: No

❌ Insider buys last six months: No

Price:

✅ 1-year stock price forecast is above 10%: +23%

✅ Next 5-year EPS growth estimates (CAGR) is above 10%: Yes (26%)

❌ DCF Value: $46; Overvalued by 9% (5 years, discount rate: 10%, terminal growth: 3%, model: Net Income)

Due Diligence

Profitability (6.5 of 10):

✅ Exceptional Gross Margin: 62%

✅ Strong 3-Year Average Gross Margin: 59%

✅ Gross Margin is Increasing: 56% → 62% (in the last 3 years)

🟨 Healthy Operating Margin: 12%

❌ Low 3-Year Average Operating Margin: 8%

✅ Operating Margin is Increasing: 7% → 12% (in the last 3 years)

❌ Low Net Margin: 8%

❌ Low 3-Year Average Net Margin: 5%

✅ Net Margin is Increasing: 5% → 8% (in the last 3 years)

🟨 Positive ROE: 17%

🟨 Positive 3-Year Average ROE: 10%

✅ ROE is Increasing: 6% → 17% (in the last 3 years)

✅ Exceptional ROIC: 26%

🟨 Positive 3-Year Average ROIC: 14%

✅ ROIC is Increasing: 9% → 26% (in the last 3 years)

Solvency (9 of 10):

✅ High Interest Coverage: 17.73 (earns more than enough operating income to safely cover interest payments on its debt)

✅ Short-Term Solvency: short-term assets (2B CHF) exceed its short-term liabilities (686m CHF)

✅ Long-Term Solvency: long-term assets (3B CHF) exceed its long-term liabilities (1B CHF)

✅ Negative Net Debt: –470.8m CHF (holds more cash than total debt)

✅ Low Debt-to-Equity Ratio: 0.31 (limited reliance on debt financing)

✅ High Altman Z-Score: 9.27 (well above the distress threshold, indicating very low bankruptcy risk)

Investment Thesis

On Holding presents an attractive long-term entry point as the stock trades below its three-year average valuation and near my fair price estimate, offering a margin of safety for a premium growth business. At the same time, the PEG ratio of 1.18 indicates that the current valuation remains reasonable relative to expected earnings growth.

The company’s growth outlook remains strong, supported by continued geographic expansion, especially in Asia-Pacific, where revenue growth exceeded 90% year-over-year in recent quarters. This region is still at an early stage of market maturity for On, suggesting a long runway for brand penetration and repeat purchases. Expansion in Asia-Pacific also reduces reliance on more mature Western markets.

On’s gross margin above 60%, the highest among its main competitors, reflects premium positioning, pricing power, and strong brand equity. Improving operating efficiency is further visible in the rising return on invested capital, which increased materially over the past three years. This combination shows that growth is becoming more profitable rather than more capital-intensive.

The business is also becoming more diversified. While footwear remains the core, apparel is now a fast-growing category, increasing customer lifetime value and reducing dependence on a single product line. At the same time, management follows a conservative and disciplined capital allocation strategy, supported by a strong cash position and limited debt, which lowers financial risk.

Finally, On’s brand credibility is strengthened by elite athletic success and high-profile partnerships, while analyst expectations point to strong EPS growth in FY2026 and FY2027.

Taken together, the combination of attractive valuation, expanding global presence, improving returns, and disciplined execution supports a compelling long-term investment case.

This is not a financial or investing recommendation. It is solely for educational purposes.

Koyfin was used for charts in this analysis. Use this URL to get a special pricing offer of 20% off all Koyfin plans.