Opera: AI Integration, Gaming Browser, and Recurring Dividends

A comprehensive analysis of Opera (OPRA).

Content:

• Company Overview

• Market Overview

• Economic Moat

• Business Strategy

• Capital Allocation

• Advantages

• Disadvantages

• Competitors

• Past

• Future

• Current Valuation

• Fair Price

• Checklist

• Due Diligence

• Investment Thesis

Company Overview

IPO Date: Jul 27, 2018

Market Cap: ~$1.76B

Sector: Communication Services

Industry: Internet Content & Information

Type: Mid-Cap Core

Total Number of Employees: ~650

Next earnings report: October 30, 2025 (estimated)

Total Debt: $9.73M

Cash & Investments: $133.82M

Beta: 0.96

Website: www.opera.com

Opera Limited (OPRA) is a global software and internet company that focuses on delivering browsers and AI-driven products to millions of users. Founded in 1995 in Oslo, Norway, Opera is publicly traded on Nasdaq under the ticker symbol OPRA. The company has expanded its reach through a broad portfolio of browsers, each designed for specific user groups. Opera One serves as the flagship product, Opera GX is built for gamers, Opera Mini is designed for low-data consumption, and Opera Neon brings new agentic browsing features. Opera also provides versions for both iOS and Android devices, ensuring presence across platforms.

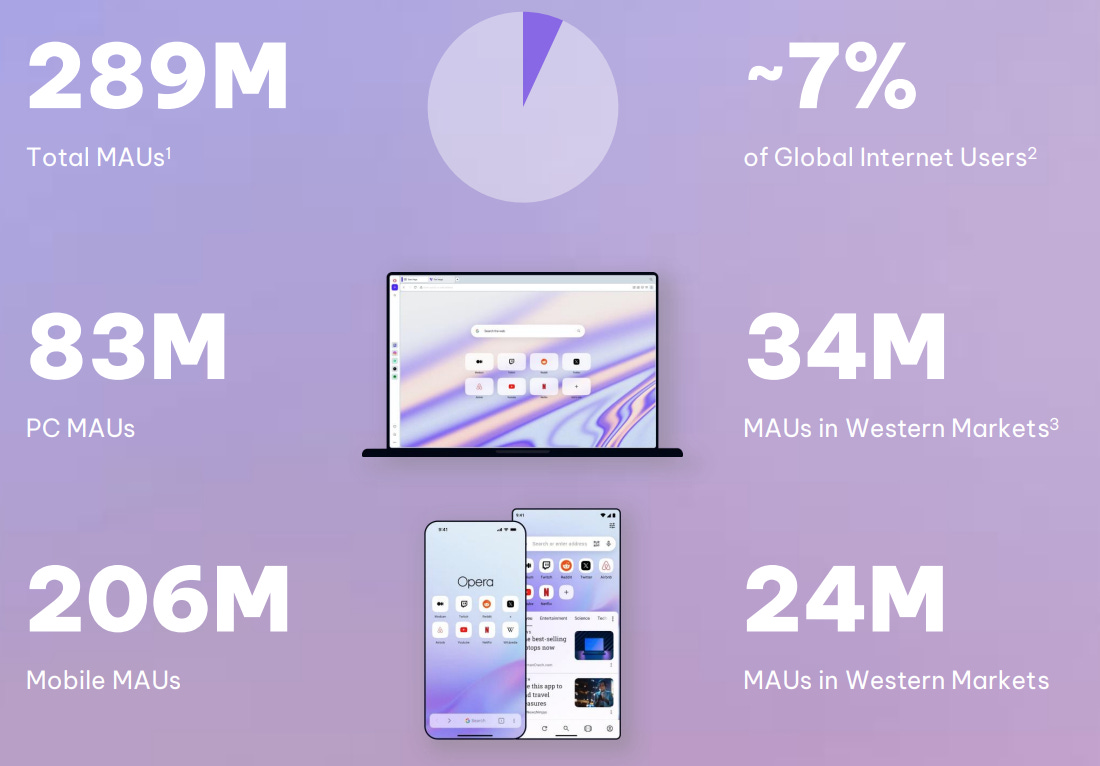

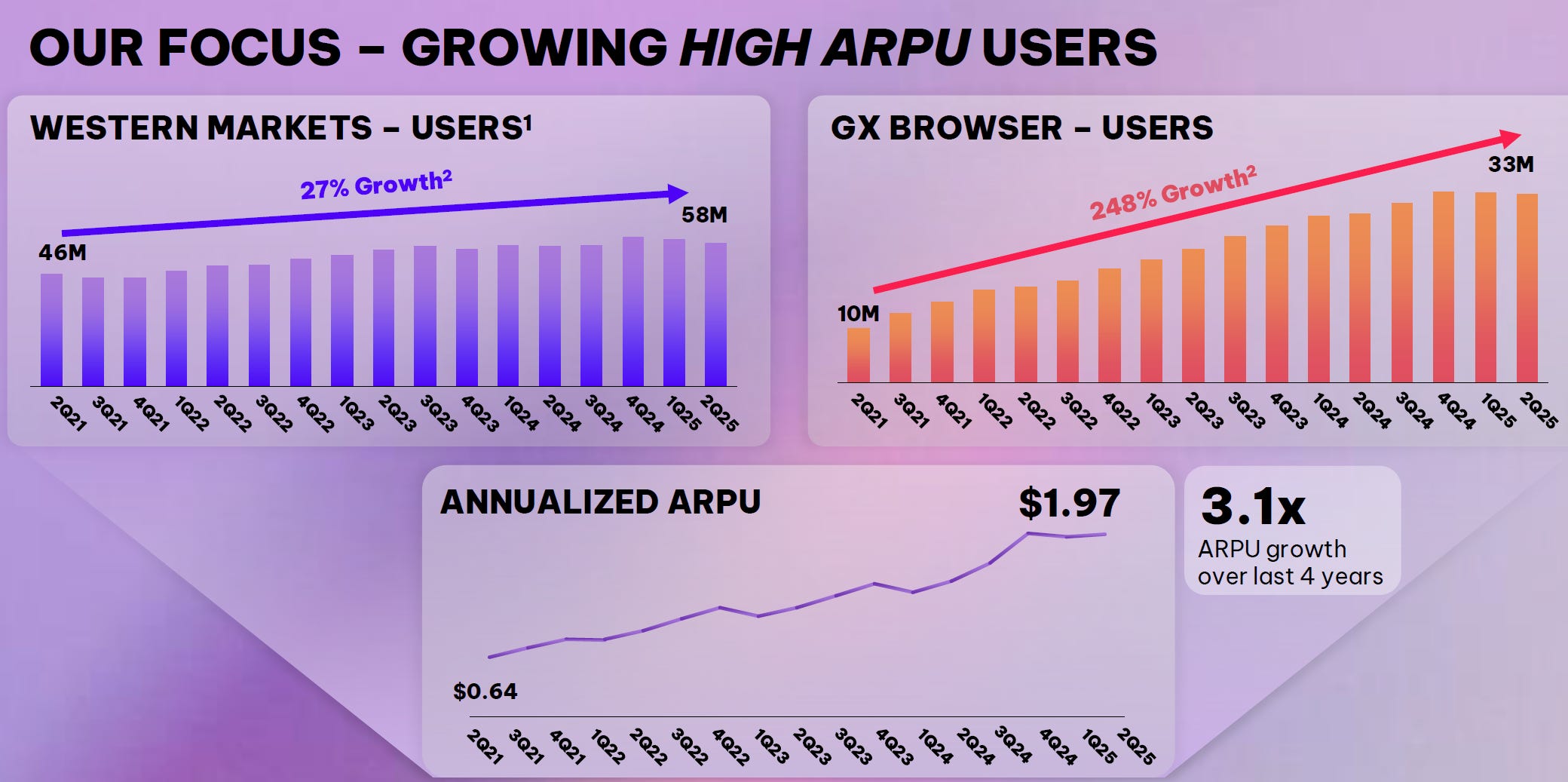

By the second quarter of 2025, Opera had 289 million monthly active users. Of these, 83 million were desktop users and 206 million were mobile users. In Western markets alone, the company served 58 million monthly users. This wide base represents about 7% of global internet users outside of China.

The company is managed by Co-CEOs Yahui Zhou, who has been in the role for 9 years, and Lin Song, who has been with Opera for 23 years. Opera also has a geographic presence across Europe, with offices in countries such as France, Germany, Norway, Poland, Spain, Sweden, and the UK.

Market Overview

To Read: Web Browser Statistics 2025: Market Share, User Preferences, and Future Outlook

According to Global Growth Insights, the global browser software market size was $5.85B in 2024 and is projected to touch $6.23B in 2025, reaching $9.96B by 2034. This is about a CAGR of 6.05% during the forecast period from 2025 to 2034. With over 34% market activity transitioning to mobile environments.

Another source (Data Insights Market) gives a similar number: about $5.11B in 2025, with a CAGR of 4.8% from 2025 to 2033.

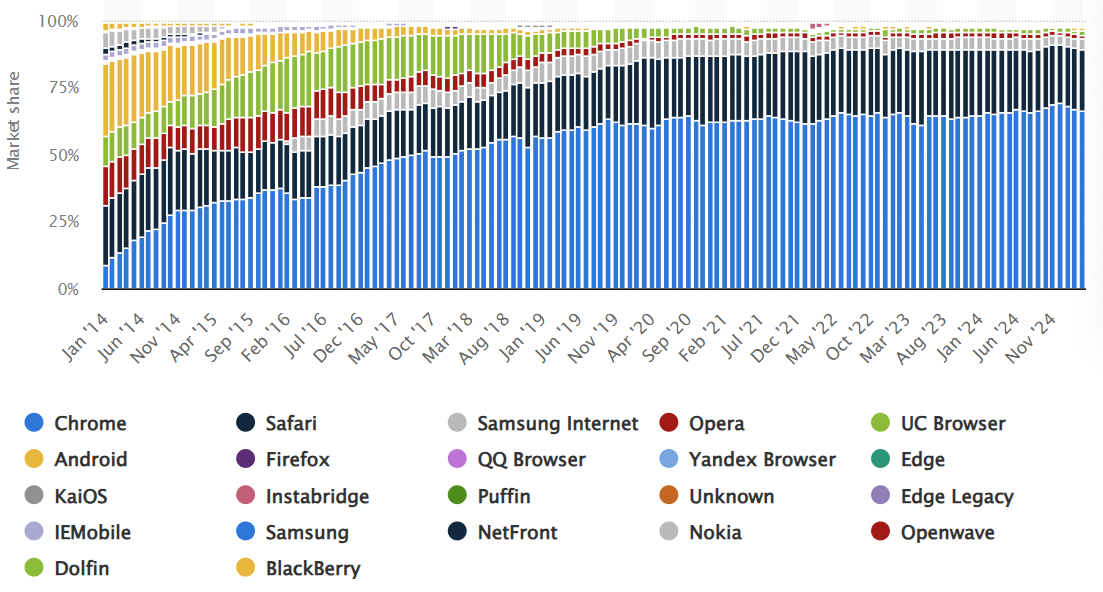

According to StatCounter, Chrome dominates the market with 69.23% of market share, and Opera has 1.85% of market share.

Market share held by leading mobile internet browsers worldwide from January 2014 to March 2025:

Economic Moat

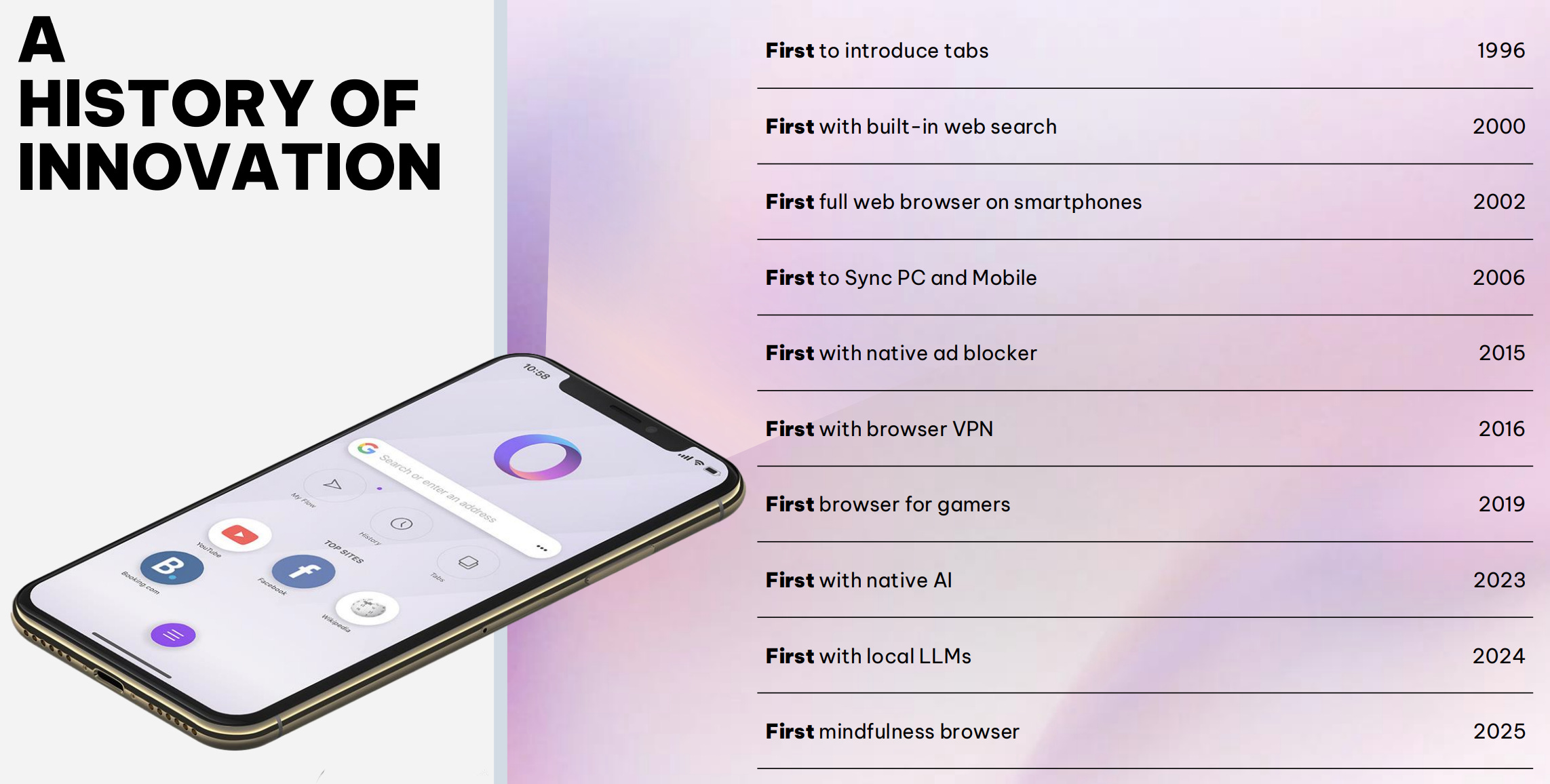

Opera’s narrow moat is built on its long history of innovation, brand strength, and deep partnerships. The company is recognized for introducing first-to-market features that later became industry standards.

It was the first to launch tabs in 1996, built-in search in 2000, mobile browsing in 2002, synchronization between PC and mobile in 2006, built-in ad blocker in 2015, VPN in 2016, and the world’s first gaming browser in 2019. More recent milestones include the integration of ChatGPT in 2023, local large language models in 2024, and the announcement of Opera Neon in 2025.

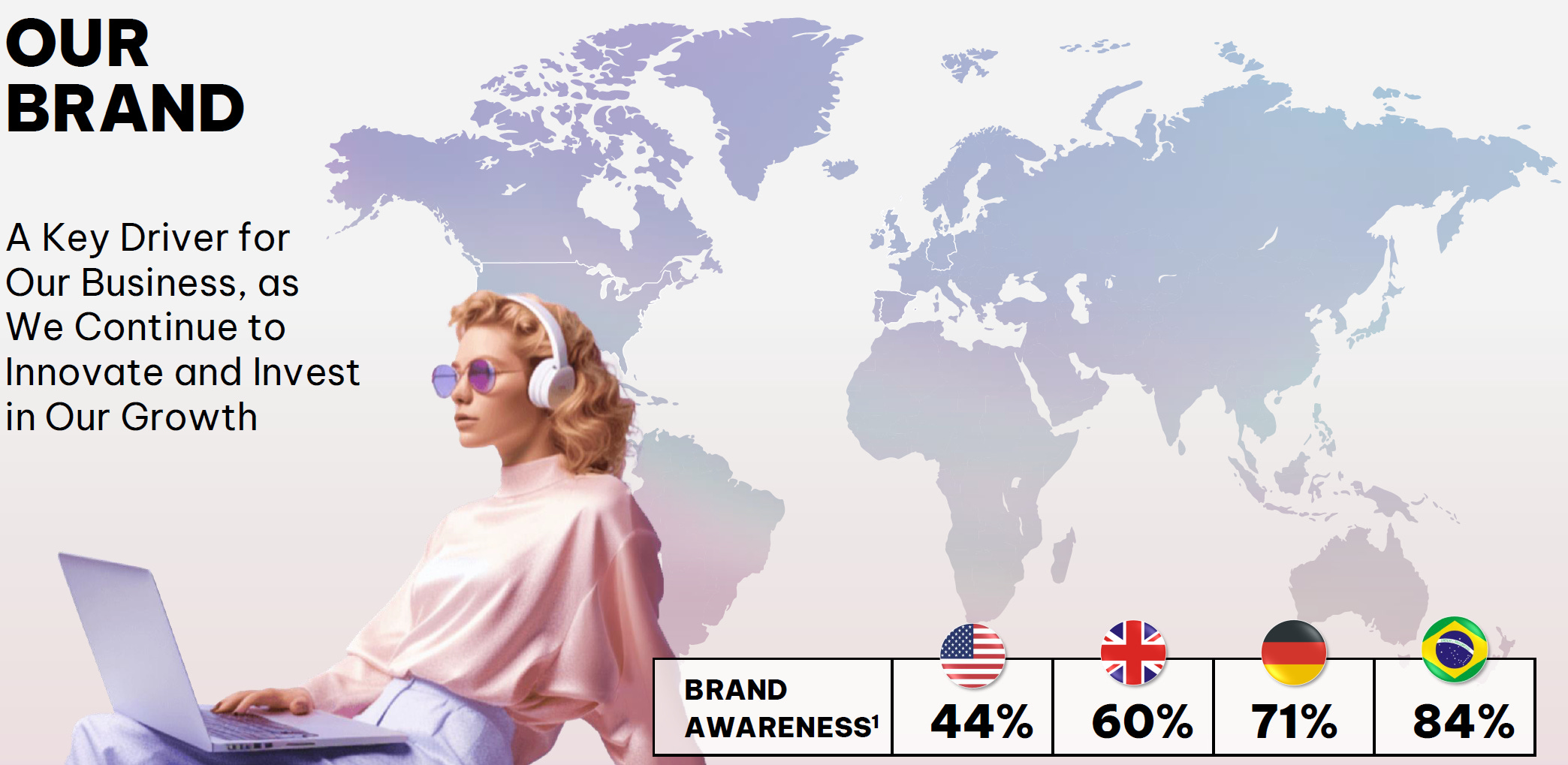

Brand awareness is another important part of its moat. Surveys show Opera has 44% recognition in the United States, 60% in the UK, 71% in Germany, and 84% in Brazil. These figures reflect Opera’s ability to position itself as a recognized alternative to mainstream browsers.

Finally, Opera benefits from long-term business relationships. Its partnership with Google for search monetization has lasted for more than 20 years. This provides a steady flow of revenue while Opera differentiates itself through niche products such as GX and innovative features like the Aria AI engine.

Business Strategy

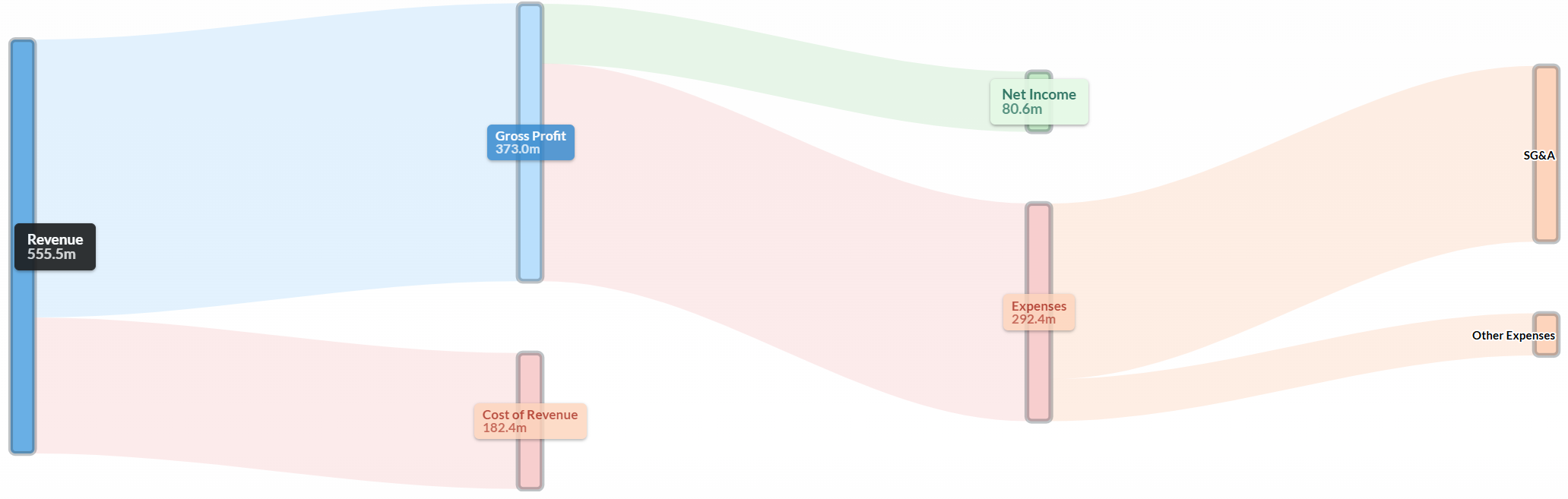

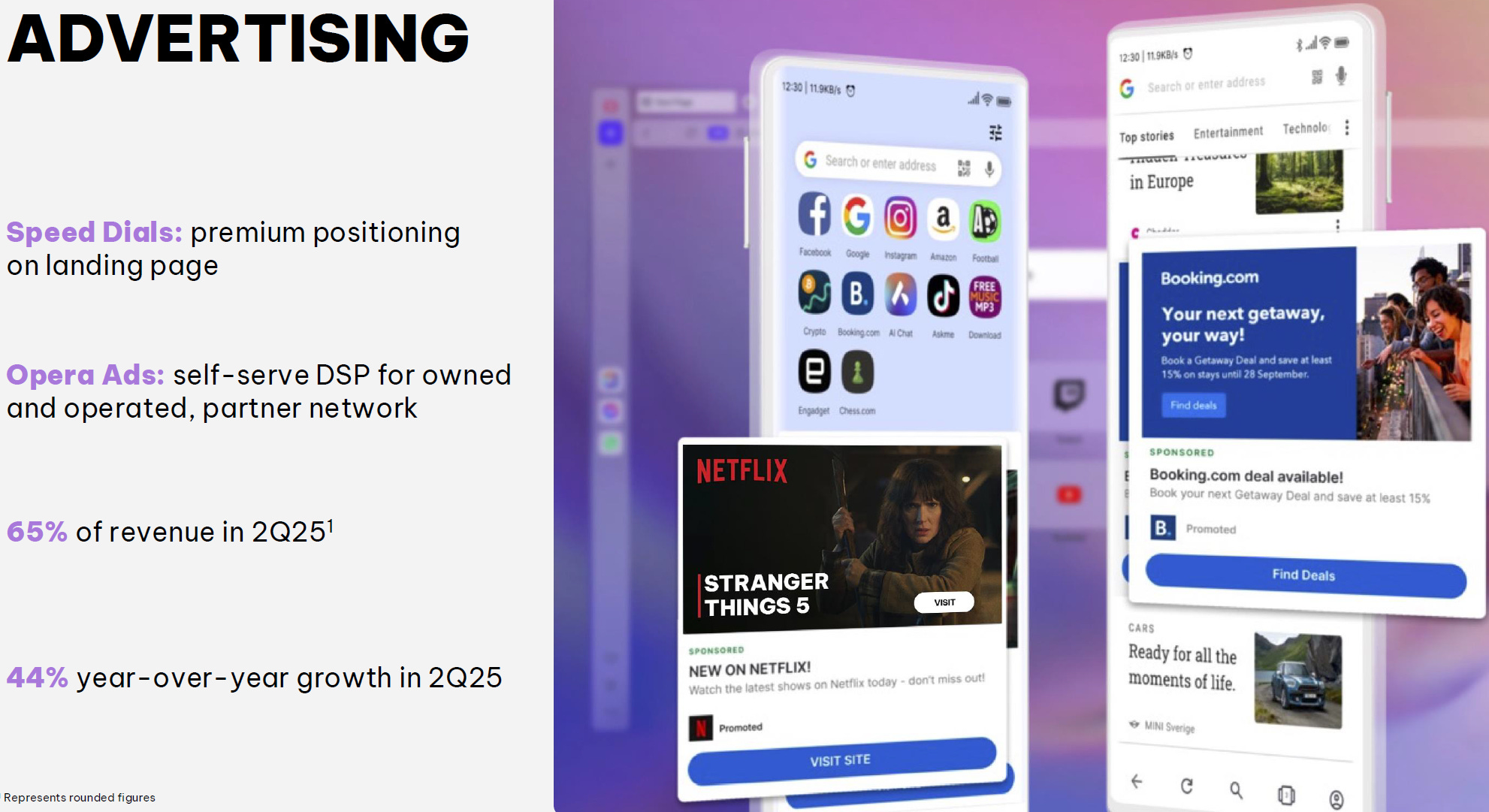

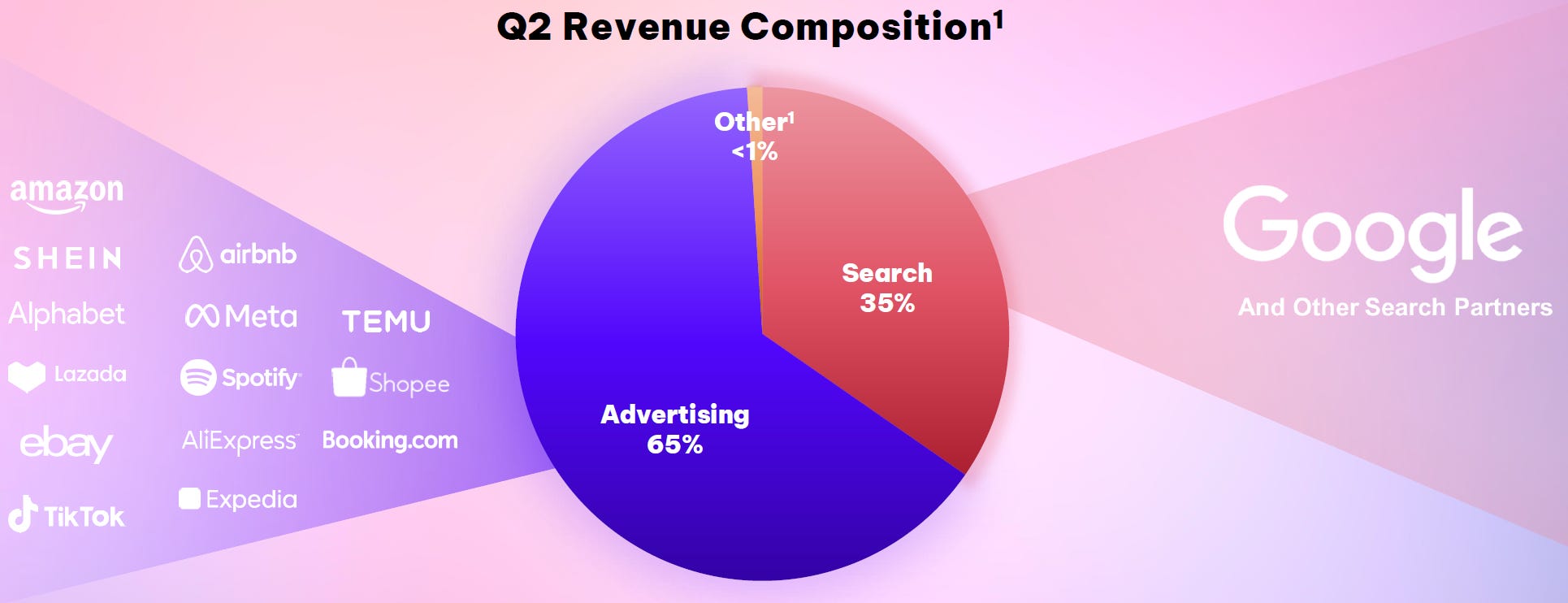

Opera’s business strategy focuses on profitable growth while expanding its ecosystem of products. In Q2 2025, advertising generated 65% of revenue, while search accounted for 35%. Advertising revenue grew by 44% year-over-year, supported by demand from e-commerce partners, while search revenue grew by 11%.

A key strategic goal is to increase revenue per user. Opera’s annualized ARPU reached $1.97 in Q2 2025, up 35% from the year before. This growth is the result of Opera’s focus on high-value regions. In Western markets, the user base has grown to 58 million, with higher ARPU compared to emerging regions. Opera GX has 33 million users and the highest ARPU among all Opera products.

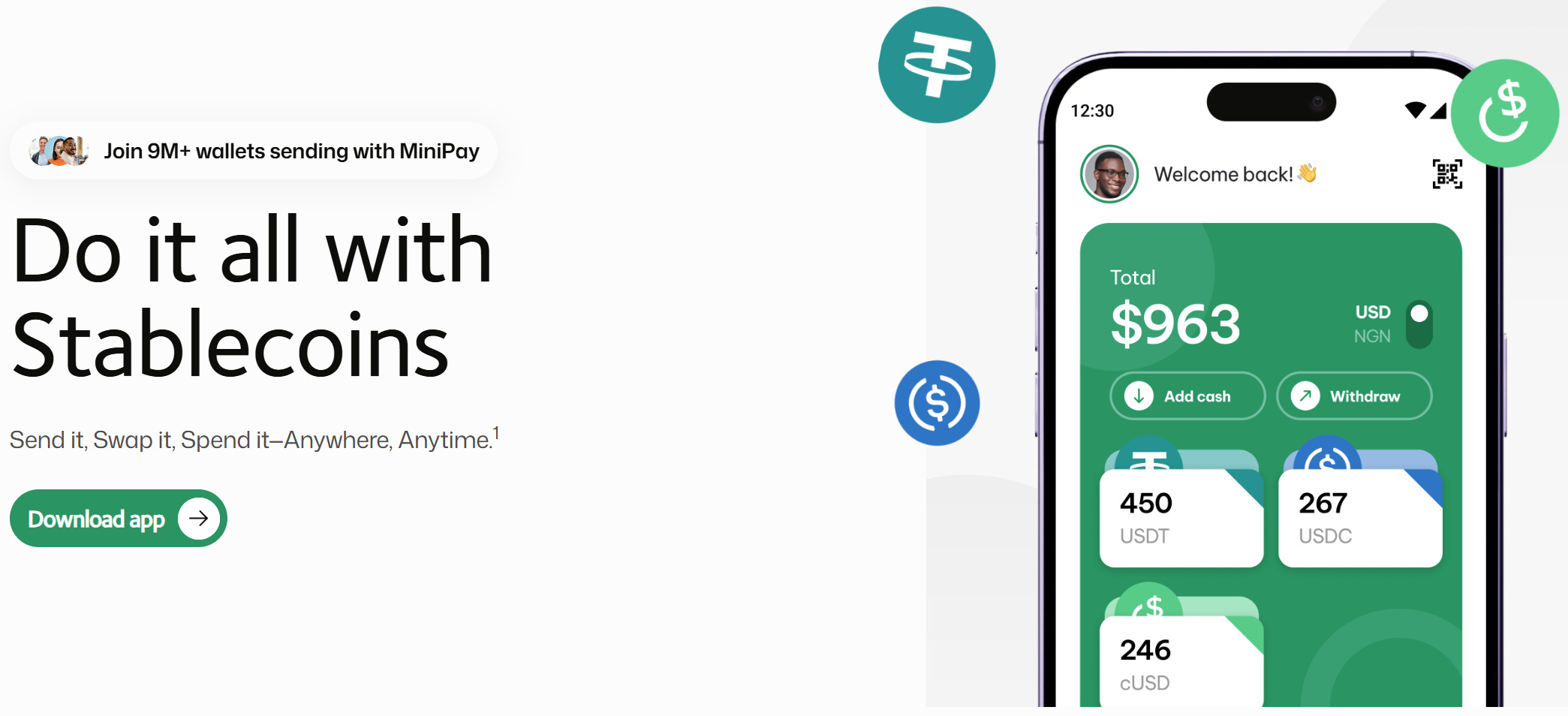

Opera is also expanding into new services. MiniPay, its non-custodial stablecoin wallet, became one of the fastest-growing digital wallets globally. It surpassed 9 million activated wallets and processed more than 250 million transactions, with a 255% activation surge in Q2 2025. Opera is also strengthening premium services. In 2025, VPN Pro was upgraded with faster speeds, better security, and more global locations. These moves show Opera’s ambition to move beyond browsing into financial services and security products.

Capital Allocation

Opera has consistently returned capital to shareholders while maintaining a strong balance sheet.

Since 2020, the company has returned about $477 million to investors. This includes $228 million spent to repurchase 35.5 million ADS shares, equal to 30% of shares outstanding at the start of 2020.

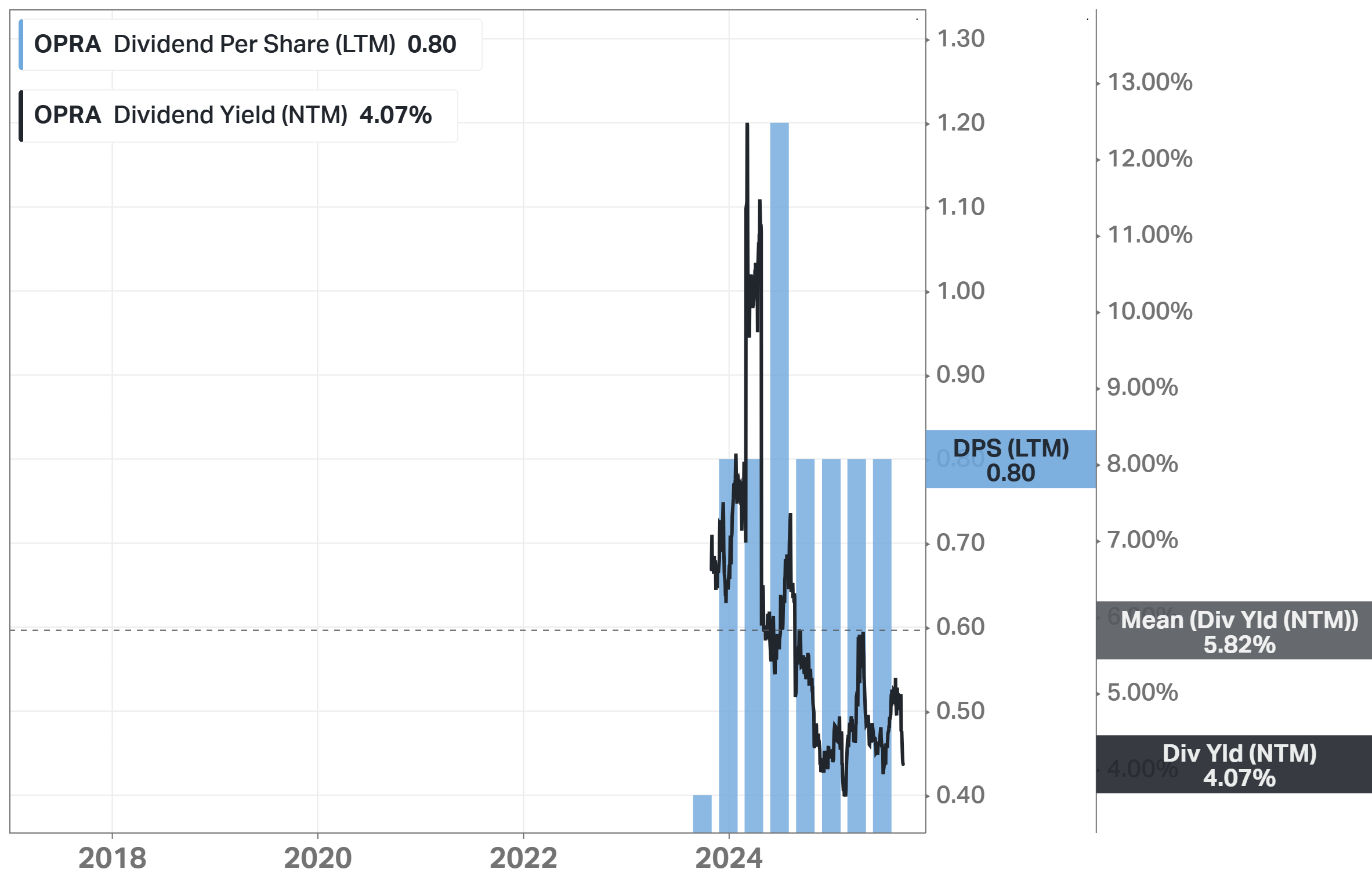

The company has also paid dividends. In January 2023, Opera distributed a special dividend of $0.80 per ADS, equal to $71 million. Later that year, it started a recurring dividend program of $0.80 per ADS per year, paid semi-annually. By mid-2025, this program had distributed $178 million.

Opera maintains liquidity to continue these shareholder returns. At the end of June 2025, Opera held $392 million in cash and investments. This included $133.8 million in cash and a 9.4% stake in OPay valued at $258.3 million. Such capital strength allows Opera to balance dividends, buybacks, and investments in new products.

Advantages

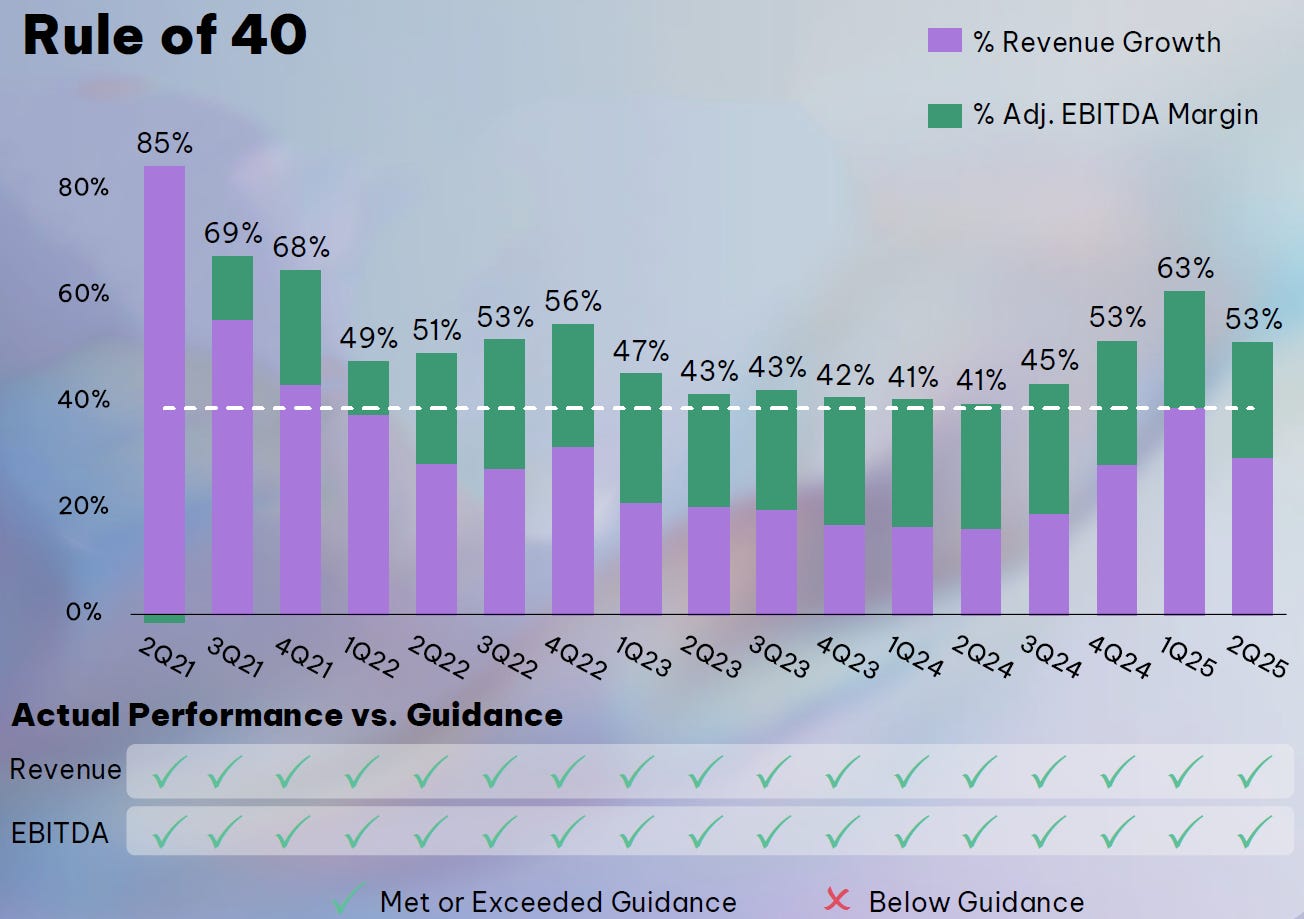

Consistency in growth metrics. Opera has delivered 17 consecutive quarters above the “Rule of 40.” In Q2 2025, the combination of revenue growth and EBITDA margin was 53%. This consistency shows Opera can scale while staying profitable.

The Rule of 40 is a benchmark for Software-as-a-Service (SaaS) companies, stating that a company's combined revenue growth rate and profit margin should be 40% or higher to indicate strong financial health and long-term sustainability.

Revenue expansion. Revenue increased 30% year-over-year in Q2 2025. The strong rise was driven by advertising growth of 44%, which outpaced most industry averages. This performance supports Opera’s raised full-year guidance.

Focus on high-value users. Opera’s ARPU reached $1.97 in Q2 2025, reflecting a 35% year-over-year rise. By targeting Western markets, which reached 58 million MAUs, Opera maximizes revenue efficiency rather than relying only on scale.

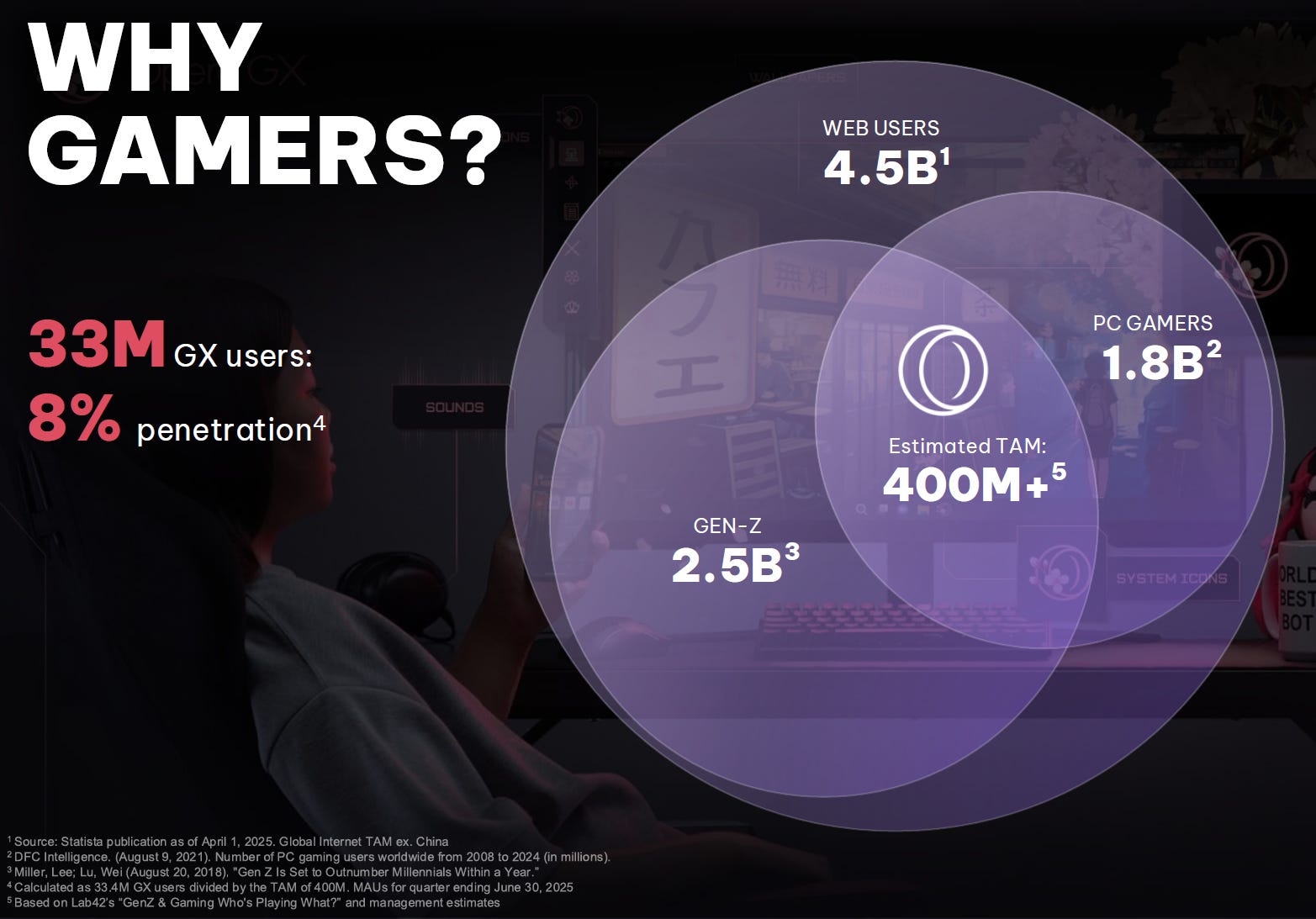

Leadership in niche segments. Opera GX serves 33 million gamers, around 8% penetration of its addressable market. This focus builds loyalty in a valuable segment that larger competitors do not prioritize.

Innovative ecosystem. Opera invests in features like MiniPay and VPN Pro. MiniPay surged 255% in activations during Q2 2025, making it one of the fastest-growing wallets worldwide. VPN Pro improvements show Opera’s push to monetize security-conscious users.

Disadvantages

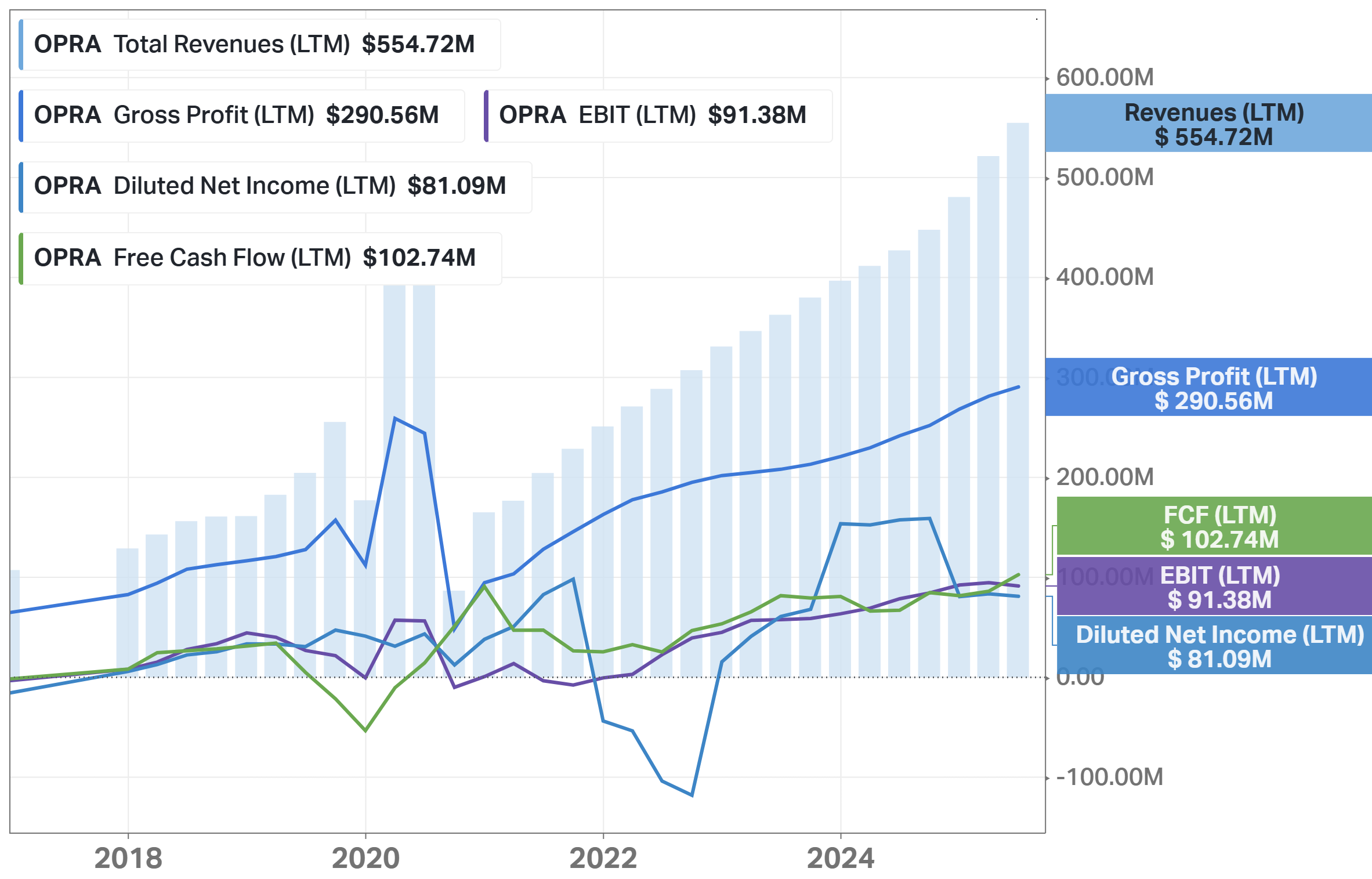

Decline in net income. Net income fell to $15.7 million in Q2 2025 from $19.3 million a year earlier. This shows that even with strong revenue growth, profitability at the bottom line has weakened.

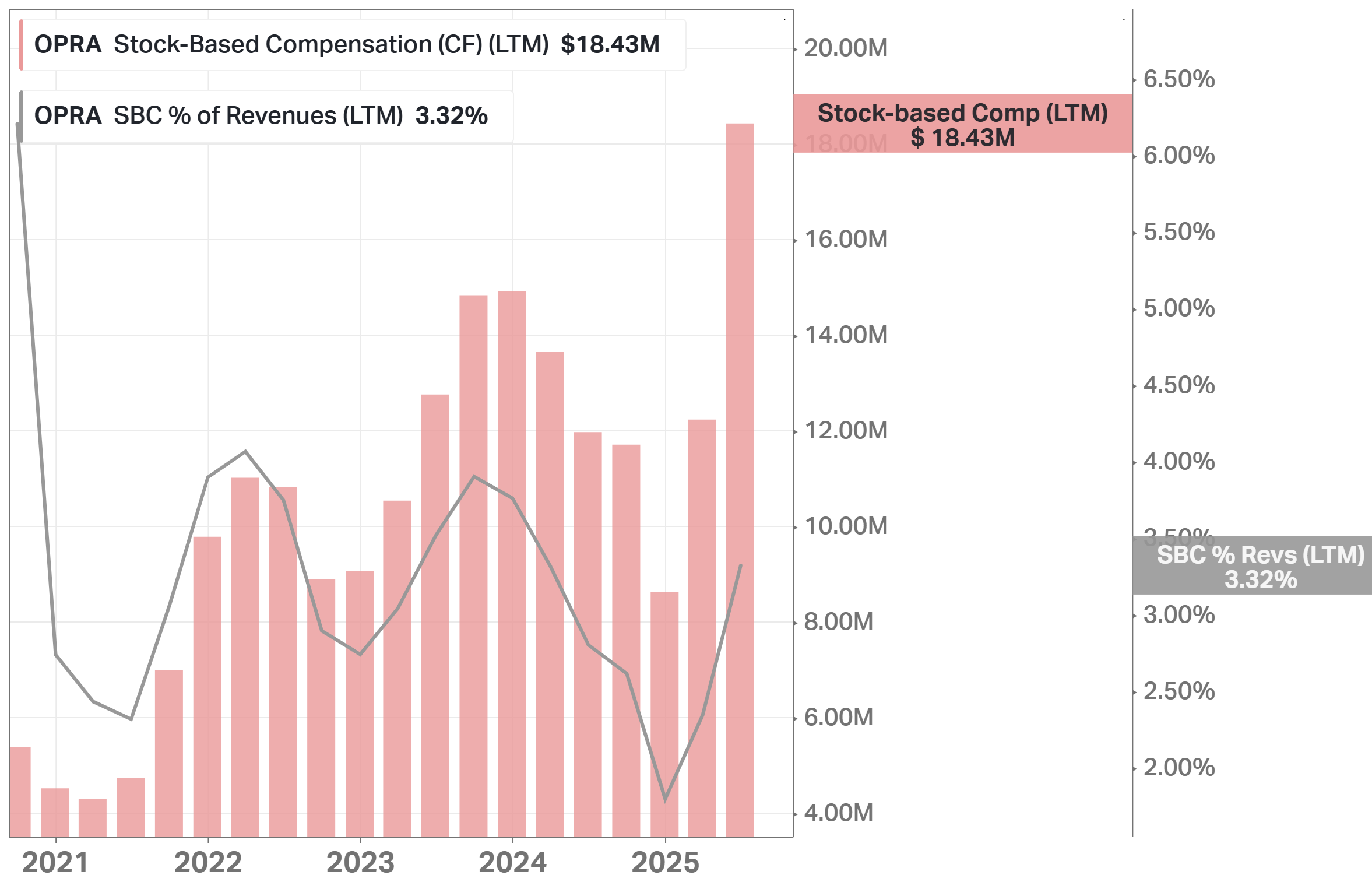

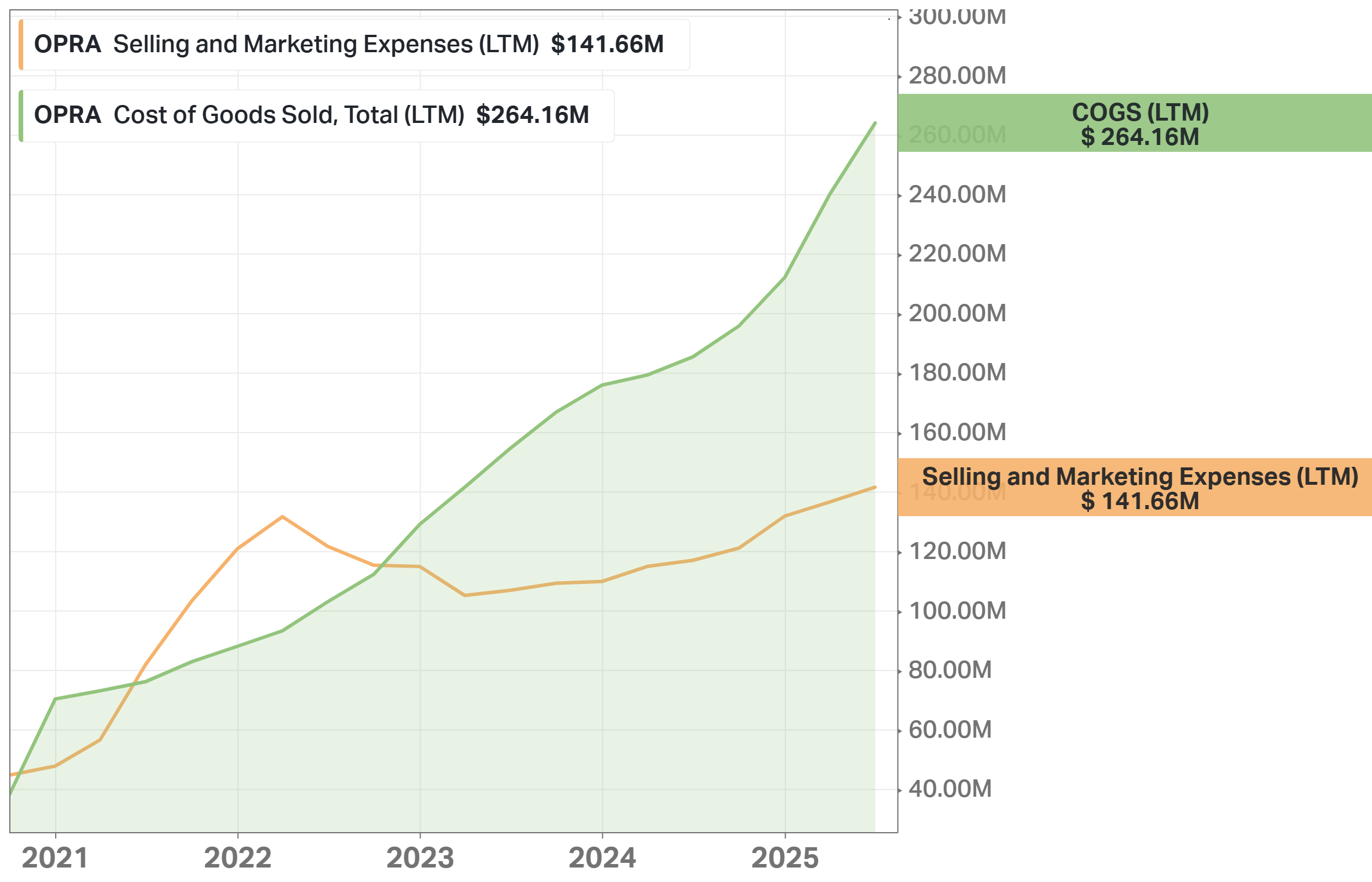

Higher operating expenses. Operating costs rose by 40% year-over-year, reaching $124.9 million. The faster rise in expenses compared to revenue pressures Opera’s margins.

Rising share-based compensation. Compensation costs have significantly increased in recent years.

Increased marketing spend. Marketing and selling expenses rose. While necessary to grow user numbers, these costs reduce operating efficiency if growth slows.

Lower operating margin. Operating profit dropped to $18.1 million with a margin of 13%, down from 20% in Q2 2024. This decline reflects that Opera is spending heavily to maintain growth momentum.

Competitors

Google Chrome. Chrome dominates the global market share with pre-installation on Android devices and integration with Google services. Opera, with its 7% global user share outside China, competes by offering built-in VPN, ad blocker, and AI assistants, features not present in Chrome.

Apple Safari. Safari benefits from being the default browser on iPhones and Macs. Opera does not have that advantage, but it is available across all devices, including Android. Unlike Safari, Opera invests in gamer-specific and AI-driven features, giving it unique differentiation.

Microsoft Edge. Edge is the default on Windows and ties directly into Microsoft’s ecosystem. Opera builds loyalty instead through product design and integrated AI. Features like Aria, MiniPay, and Opera Neon provide differentiation that Edge does not emphasize.

Mozilla Firefox. Firefox attracts users who value privacy and open-source development. Opera also emphasizes privacy with VPN and ad-blocking, but combines it with mainstream AI features. This allows Opera to appeal to both privacy-conscious and innovation-seeking users.

Past

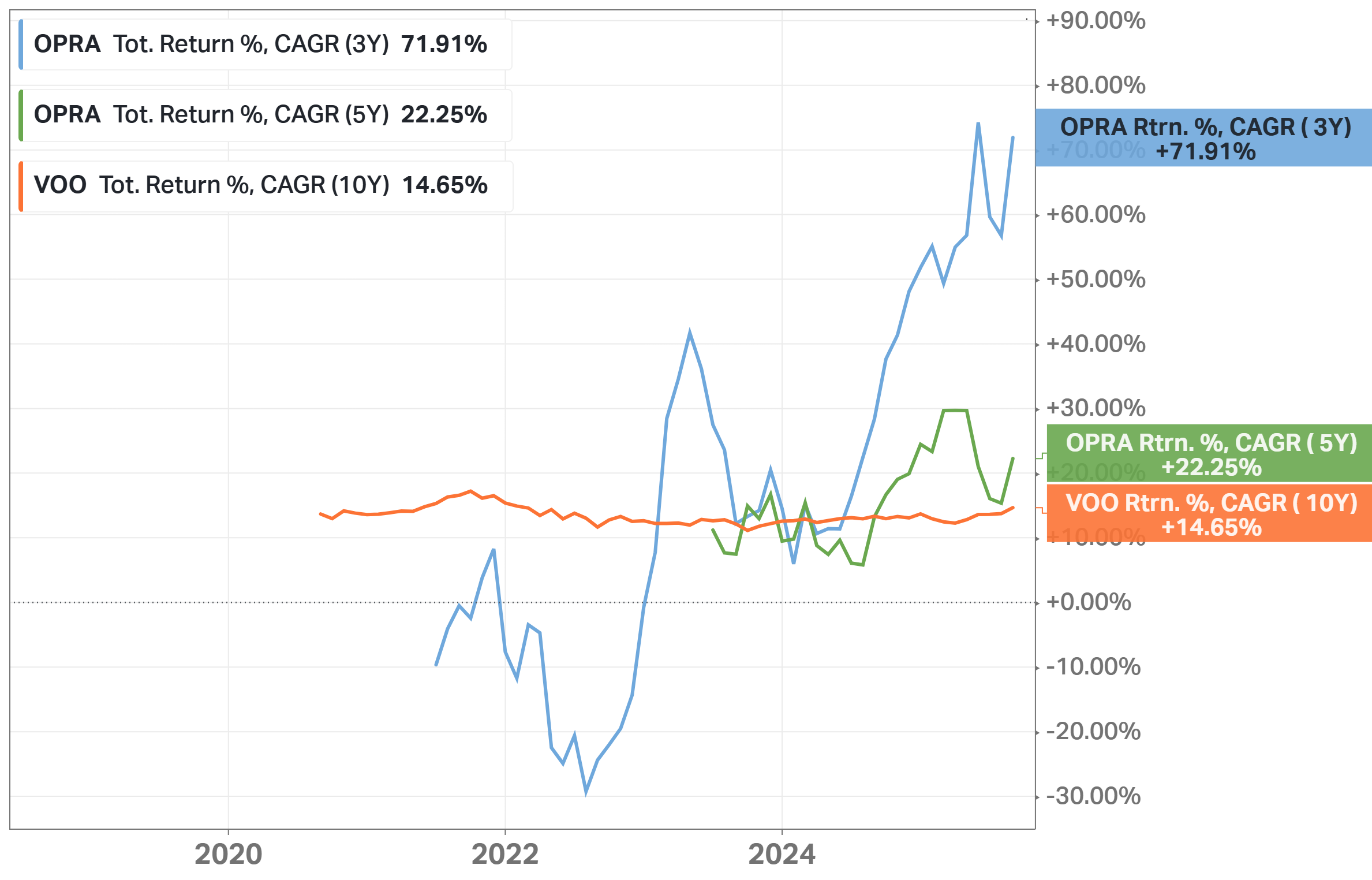

The CAGR rate for the stock over 3 and 5-year time periods is shown above. The stock overperforms the S&P 500. But please note that the company went public “only” in 2018.

Below are some significant recent events.

Opera Neon Browser Announced: In May 2025, Opera introduced Opera Neon, a new agentic browser with a fully integrated AI agent. It combines advanced reasoning and summarization with user context, aiming to redefine productivity and browsing experience.

MiniPay Wallet Surge: MiniPay, Opera’s non-custodial stablecoin wallet, surpassed 9 million activated wallets and processed over 250 million transactions. It recorded a 255% surge in activations in Q2 2025, making it one of the fastest-growing wallets globally.

VPN Pro Upgrade: In 2025, Opera revamped VPN Pro, offering faster connection speeds, stronger privacy features, and expanded coverage with more global server locations.

Strong Advertising Momentum: Advertising revenue grew 44% year-over-year in Q2 2025, reaching $92.9 million. E-commerce partners remained the fastest-growing vertical.

Dividend Distribution: In June 2025, Opera announced and later paid a recurring semi-annual dividend of $0.40 per share in July, continuing its shareholder return program.

User Growth: Opera reached 289 million average monthly active users in Q2 2025. Opera GX, the gaming-focused browser, reached 33 million users, up 11% year-over-year.

Capital Strength: At the end of Q2 2025, Opera held a 9.4% stake in OPay valued at $258.3 million.

Future

Below is the 3-year forecast for future sales and EPS growth, which is projected to be around 17.58% and more than 26.30%, respectively.

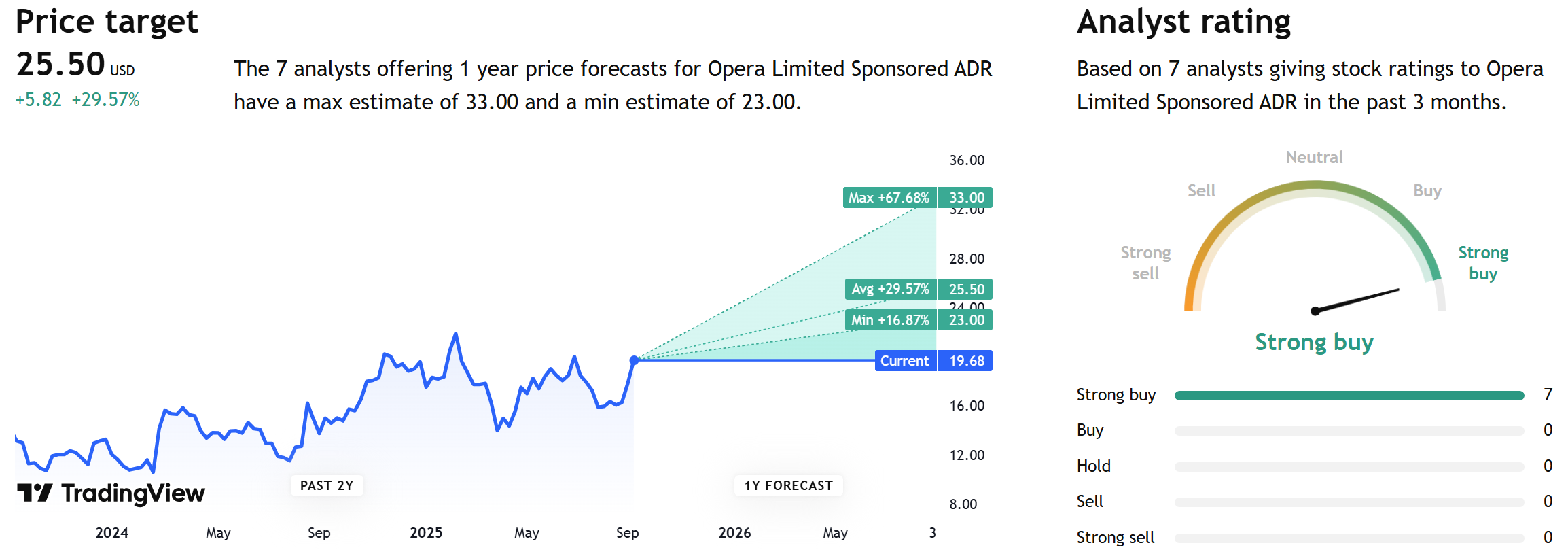

Based on 1-year price targets offered by other analysts, the average price target for Opera comes to $25.50. The average price target represents an increase of more than 29%.

Current Valuation

Opera’s valuation ratios indicate that the stock is trading at reasonable levels compared with its 5-year history. Overall, the company is valued modestly relative to both its earnings growth and historical averages, suggesting that the stock offers investors a balanced entry point.

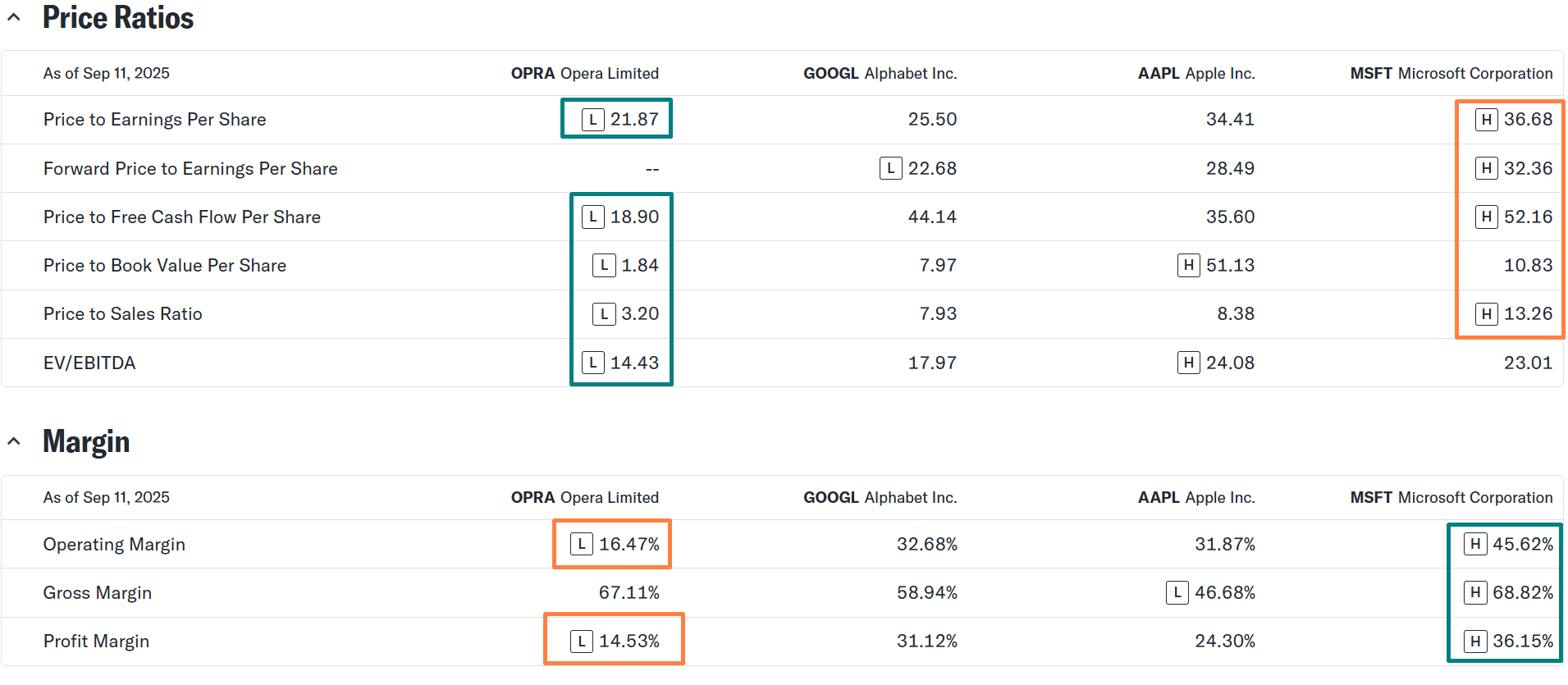

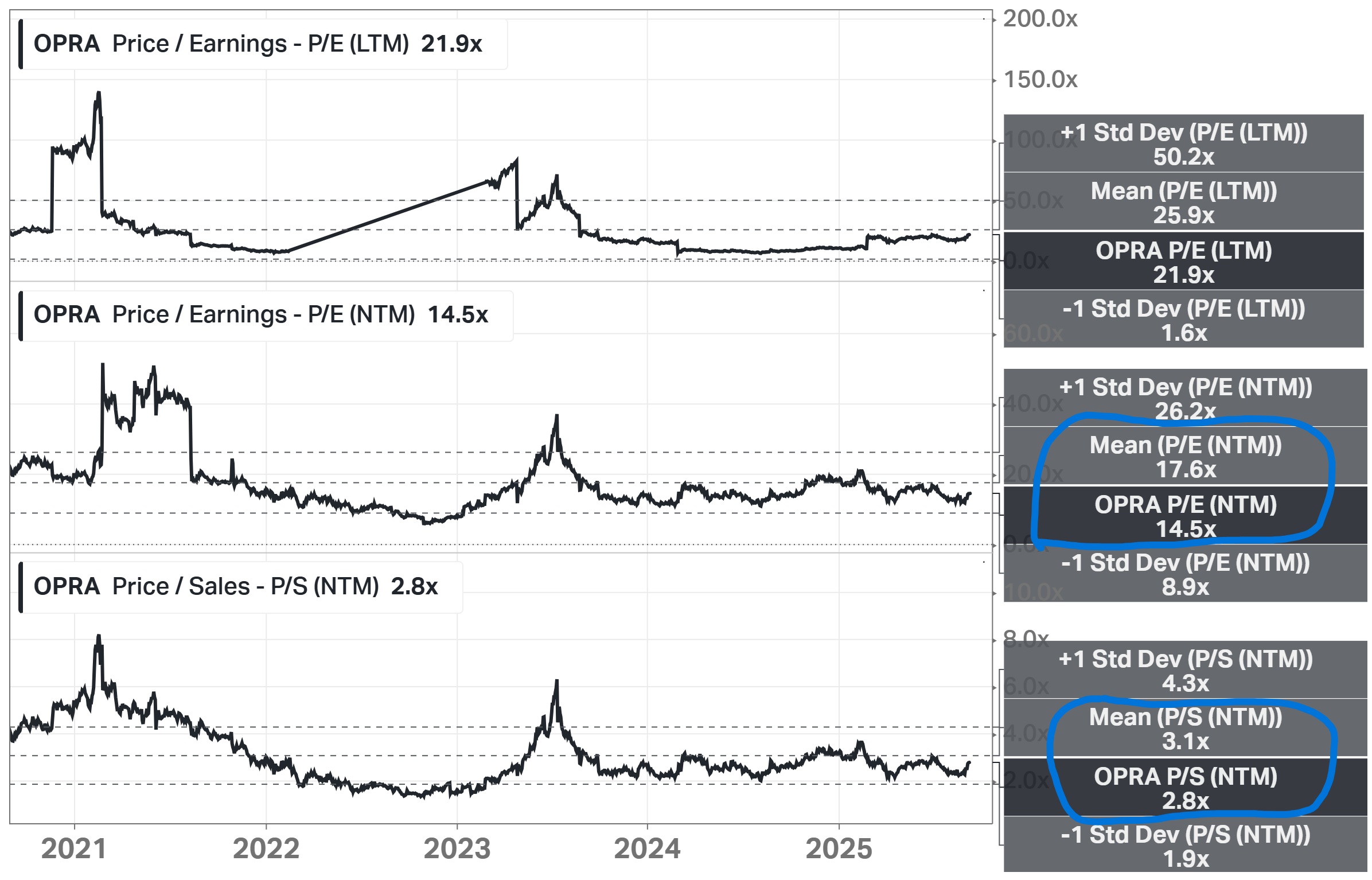

The company’s price-to-earnings ratio on a trailing basis is 21.9, which is below the 5-year average of 25.9. On a forward basis, the P/E ratio is 14.5, also below its historical mean of 17.6. The price-to-sales ratio is 2.8, below its mean of 3.1.

Looking at cash generation, Opera trades at 17.1 times free cash flow, which is under its 5-year mean of 22.0. The price-to-book ratio is 1.8, slightly above its historical mean of 1.2.

Finally, the PEG ratio stands at 0.93, a level under 1.0, which implies that Opera’s expected growth is not yet fully reflected in the share price.

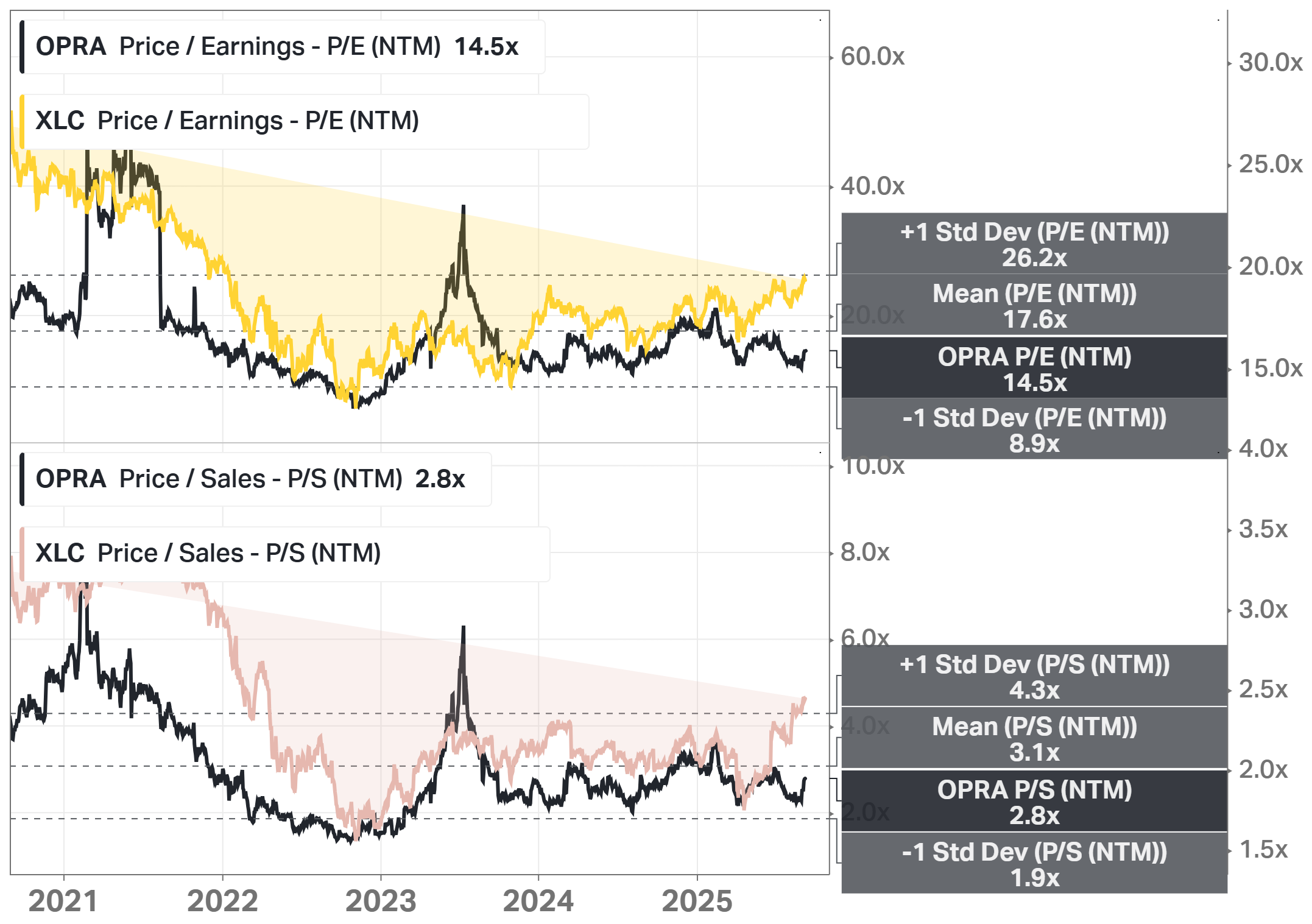

Below is a comparison with the communication services sector (XLC) in a 5-year timeframe. OPRA trades below the sector averages in terms of all the ratios.

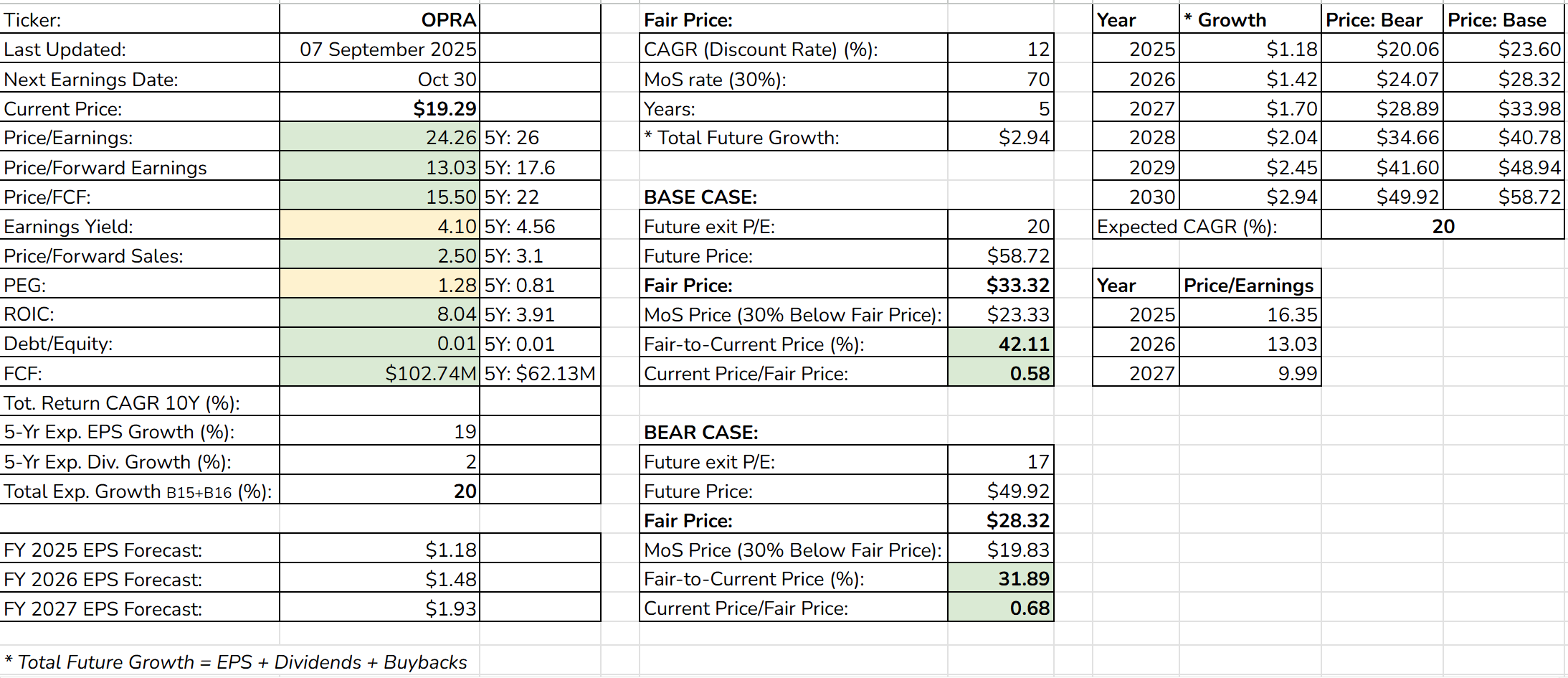

Fair Price

The Long-Term Pick's Fair Price (Base Case) for OPRA is $33.32. The current price of $19.29 is lower by 42%.

Fair-to-Current Price (%): 42%

Current Price/Fair Price: 0.58

I used:

Discount Rate: 12%

Margin of Safety: 30%

Years: 5

Future EPS Growth Rate: 19%

Future Dividend Yield: 2%

Total Future Annual Growth Rate: 19 + 2 = 21% (but my maximum is 20%)

As the exit Price/Earnings ratio for the Base Case, I used 20, which is still lower than the 5-year mean value (25.9). For the Bear Case, I subtracted 3 from the Base Case.

Checklist

Profitability:

✅ Gross margin at least 40%: 67.2%

✅ Net margin at least 10%: 14.5%

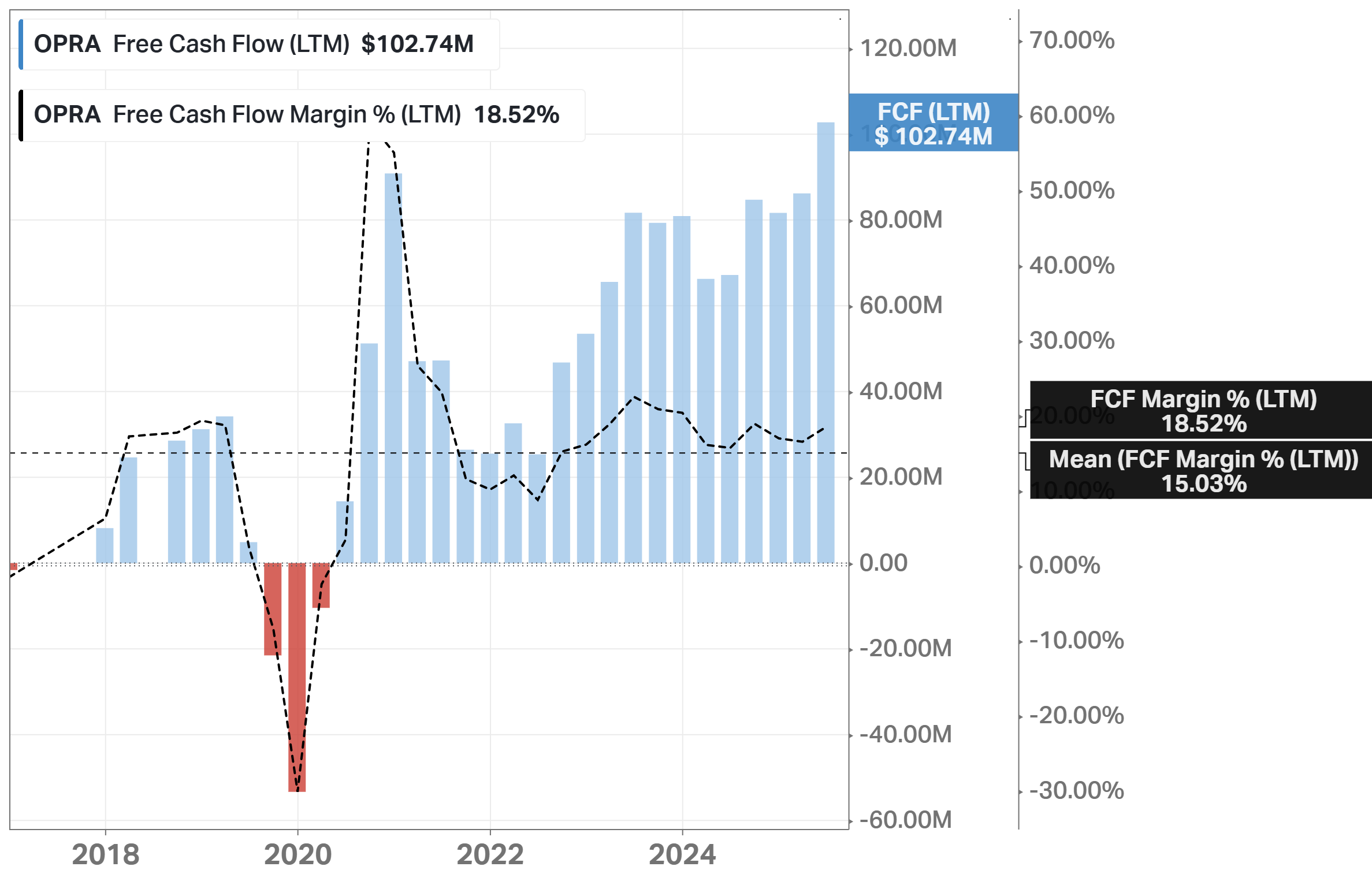

✅ FCF margin at least 10%: 18.5%

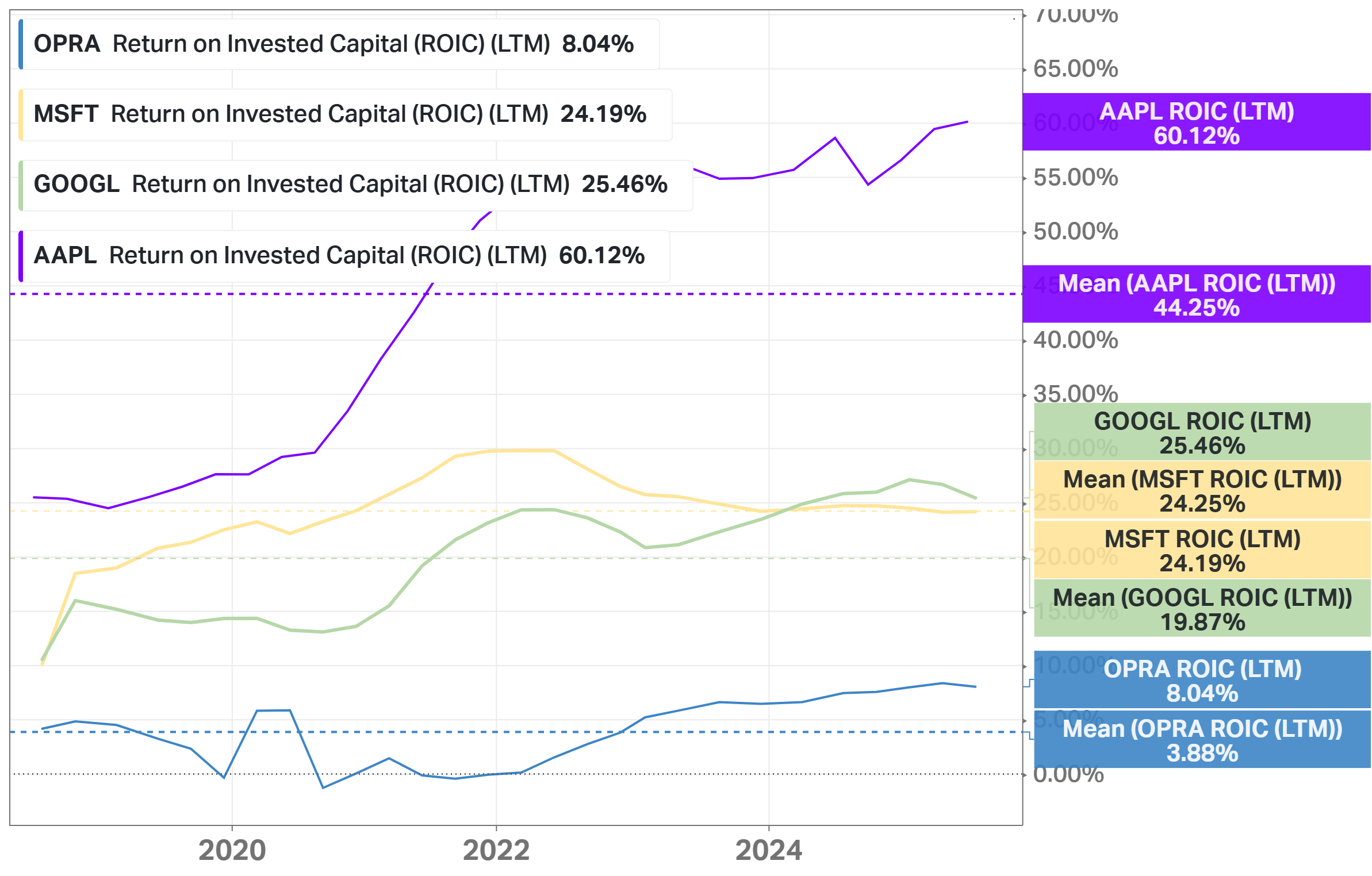

❌ Management (ROIC, ROCE, ROE, ROA): No (All below 10%)

🟨 Piotroski F-Score: 5 of 9 (Not passed: Higher ROA yoy, Higher Current Ratio yoy, Less Shares Outstanding yoy, and Higher Gross Margin yoy)

❌ EPS surprises in last 5 years: No (Based on TradingView's data)

❌ EPS growth YoY 5 years in a row: No (Based on TradingView's data)

Valuation and Advantage:

✅ Valuation below its 5-year averages: Yes

✅ Valuation below the sector: Yes

✅ Does it have a moat: Yes (narrow)

✅ Outperformed the S&P 500 CAGR: Yes (3 and 5-year CAGR)

Shares:

✅ Insider ownership at least 5%: Yes (7.52%)

❌ Less shares outstanding YoY: No

❌ Insider buys last six months: No

Price:

✅ 1-year stock price forecast is above 10%: +32.50%

✅ Next 3-year EPS growth estimates (CAGR) is above 10%: Yes (26.30%)

✅ DCF Value: $26.60; Undervalued by 28% (5 years, discount rate: 10%, terminal growth: 3%, model: Net Income)

Due Diligence

Profitability (6 of 10):

✅ Exceptional Gross Margin: 67%

✅ Strong 3-Year Average Gross Margin: 78%

❌ Declining Gross Margin: 90% → 67% (in the last 3 years)

🟨 Healthy Operating Margin: 16%

🟨 Sustainable 3-Year Average Operating Margin: 16%

✅ Operating Margin is Increasing: 8% → 16% (in the last 3 years)

🟨 Sustainable 3-Year Average Net Margin: 13%

🟨 Healthy Net Margin: 15%

✅ Net Margin is Increasing: -36% → 15% (in the last 3 years)

❌ Low ROE: 9%

❌ Low 3-Year Average ROE: 7%

✅ ROE is Increasing: -10% → 9% (in the last 3 years)

❌ Low ROIC: 9%

❌ Low 3-Year Average ROIC: 7%

✅ ROIC is Increasing: 3% → 9% (in the last 3 years)

Solvency (9.5 of 10):

✅ High Interest Coverage: 161.16 (earns far more than enough operating income to cover its interest payments)

✅ Short-Term Solvency: strong liquidity position with current assets exceeding current liabilities

✅ Long-Term Solvency: long-term assets are greater than long-term liabilities, supporting financial stability

✅ Negative Net Debt: –$128.6M (holds more cash and equivalents than total debt)

✅ Low Debt-to-Equity Ratio: 0.01 (very limited reliance on debt financing)

✅ High Altman Z-Score: 10.38 (well above the distress threshold, indicating very low bankruptcy risk)

Investment Thesis

OPRA trades below its five-year averages, below the sector benchmark (XLC), and under my fair value estimate of $33.32. With high EPS and revenue growth projections, the company offers upside potential at a discounted valuation.

Opera is diversified across multiple segments, including desktop and mobile browsers, the world’s first gaming browser, fintech with MiniPay, advertising, and crypto-related services. Its long-standing cooperation with Google provides stable search revenue, while growing ARPU and brand awareness strengthen its positioning. A recurring dividend program and disciplined capital allocation further support shareholder returns.

The company’s balance sheet is very strong, with solvency of 9.5 out of 10 and negative net debt. However, Opera faces challenges from a decline in gross margin, rising share-based compensation, and intense competition in a market where it holds only a small share.

Despite these risks, Opera’s combination of solvency, growth, diversification, and undervaluation creates a compelling case for investors seeking exposure to a profitable and innovative mid-cap stock.

This is not a financial or investing recommendation. It is solely for educational purposes.

If you like the content, please hit the like icon, leave a comment, and share the publication with your friends and colleagues - this will support the project. If you're ready to become a patron of the project, visit this page.