Quiet Energy Revolution

The market is still pricing energy on yesterday's costs. That gap is the opportunity.

Content:

Solar

Storage

Demand

The Grid

Materials

Transport

Geopolitics

Risks

The Evidence

Conclusion

Every few decades, the price of something essential collapses and quietly rewrites the market’s winners and losers. It happened with railways, with oil, with semiconductors. It is happening now with energy, and I don’t think most portfolios are positioned for it.

Solar power, batteries, and electric transport have crossed the line from expensive to simply the cheapest choice available. And when the cheapest option is also the fastest-growing, capital has only one direction to flow.

Below is the first part of my analysis. In the following part, I will provide an overview of potential companies and funds to keep on your watch list or even start forming positions.

Solar

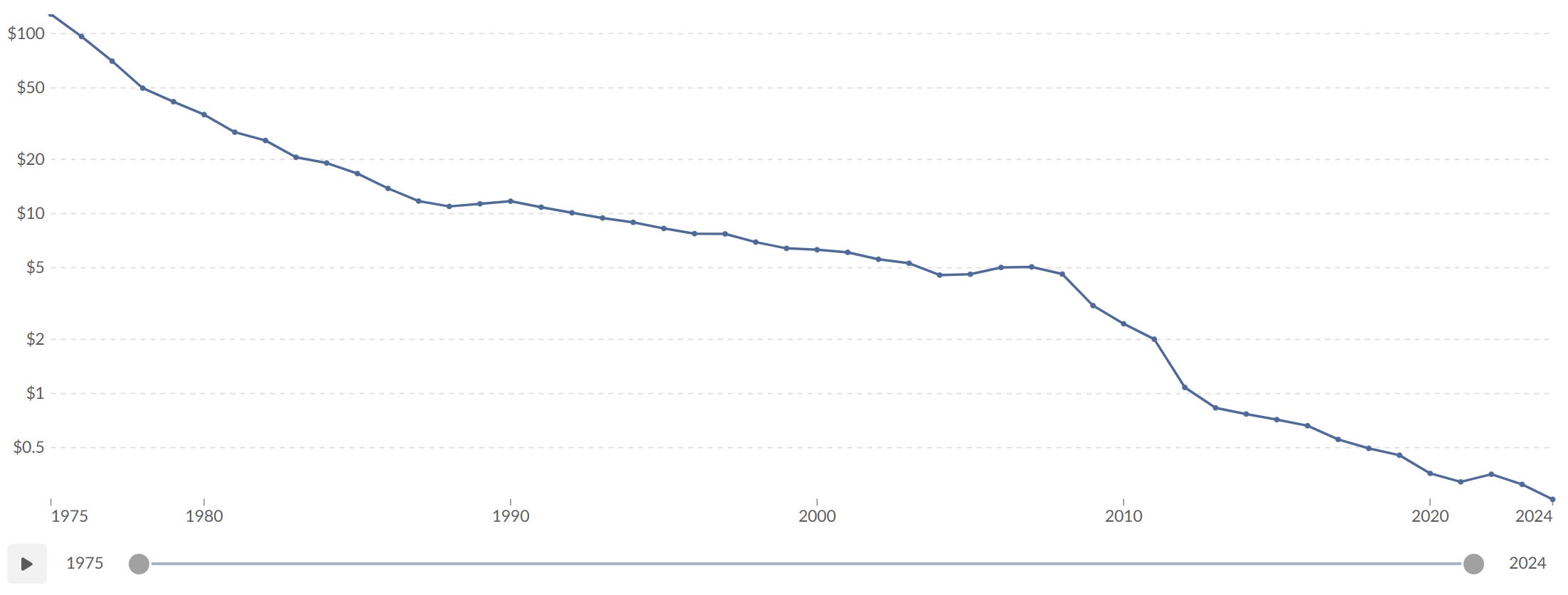

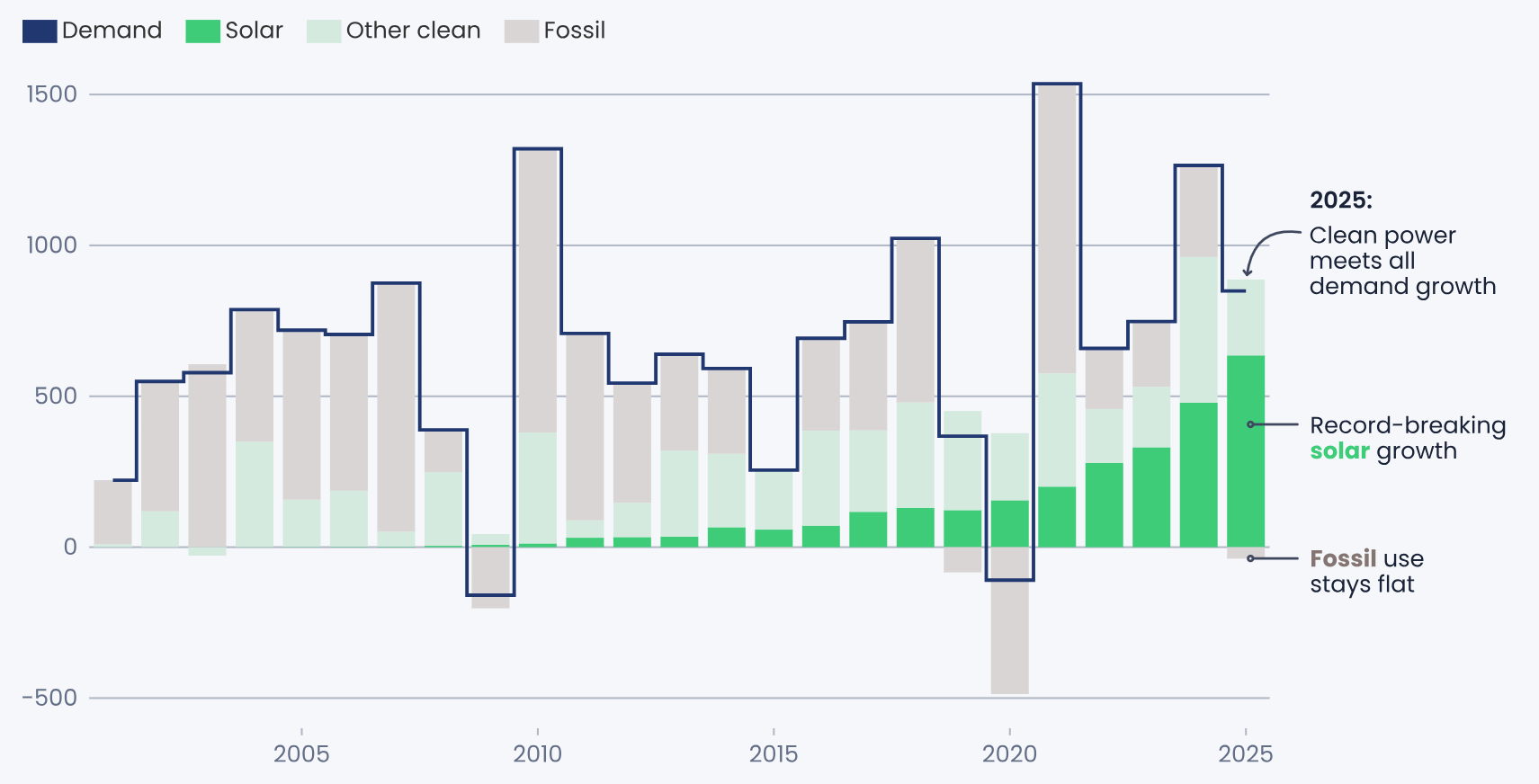

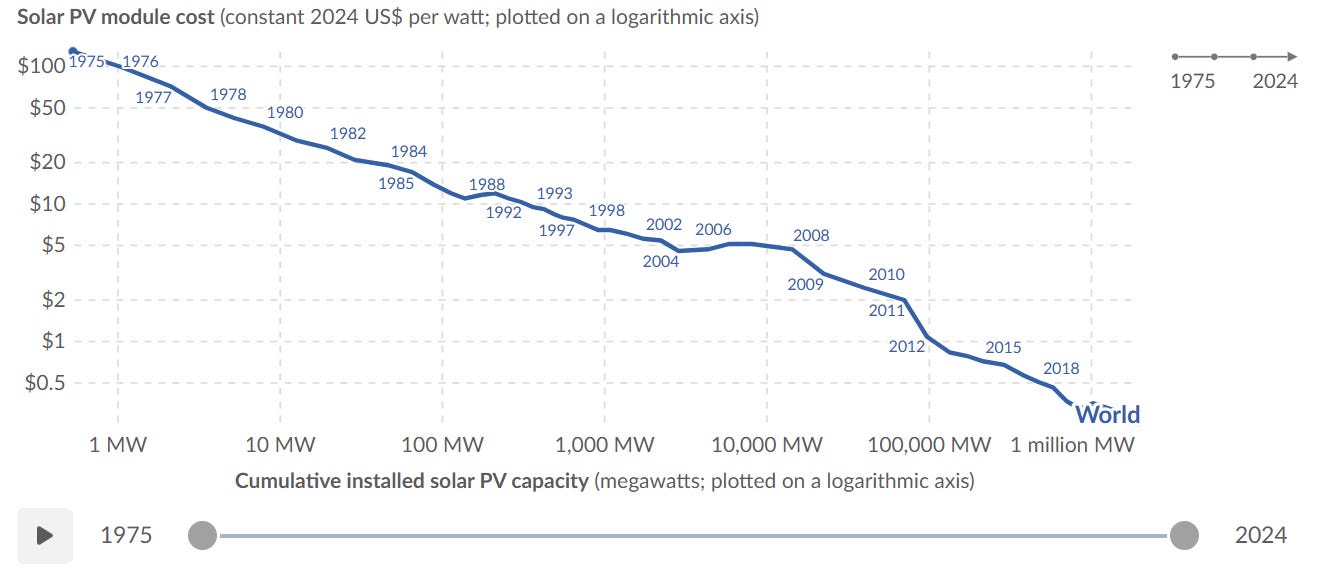

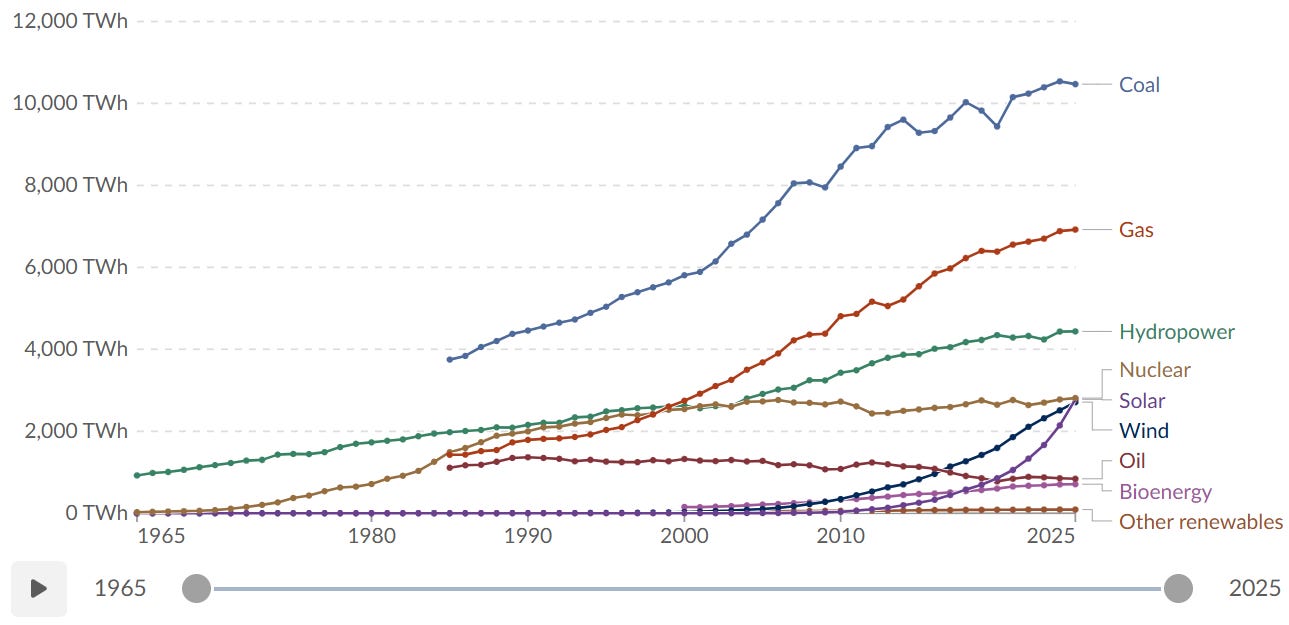

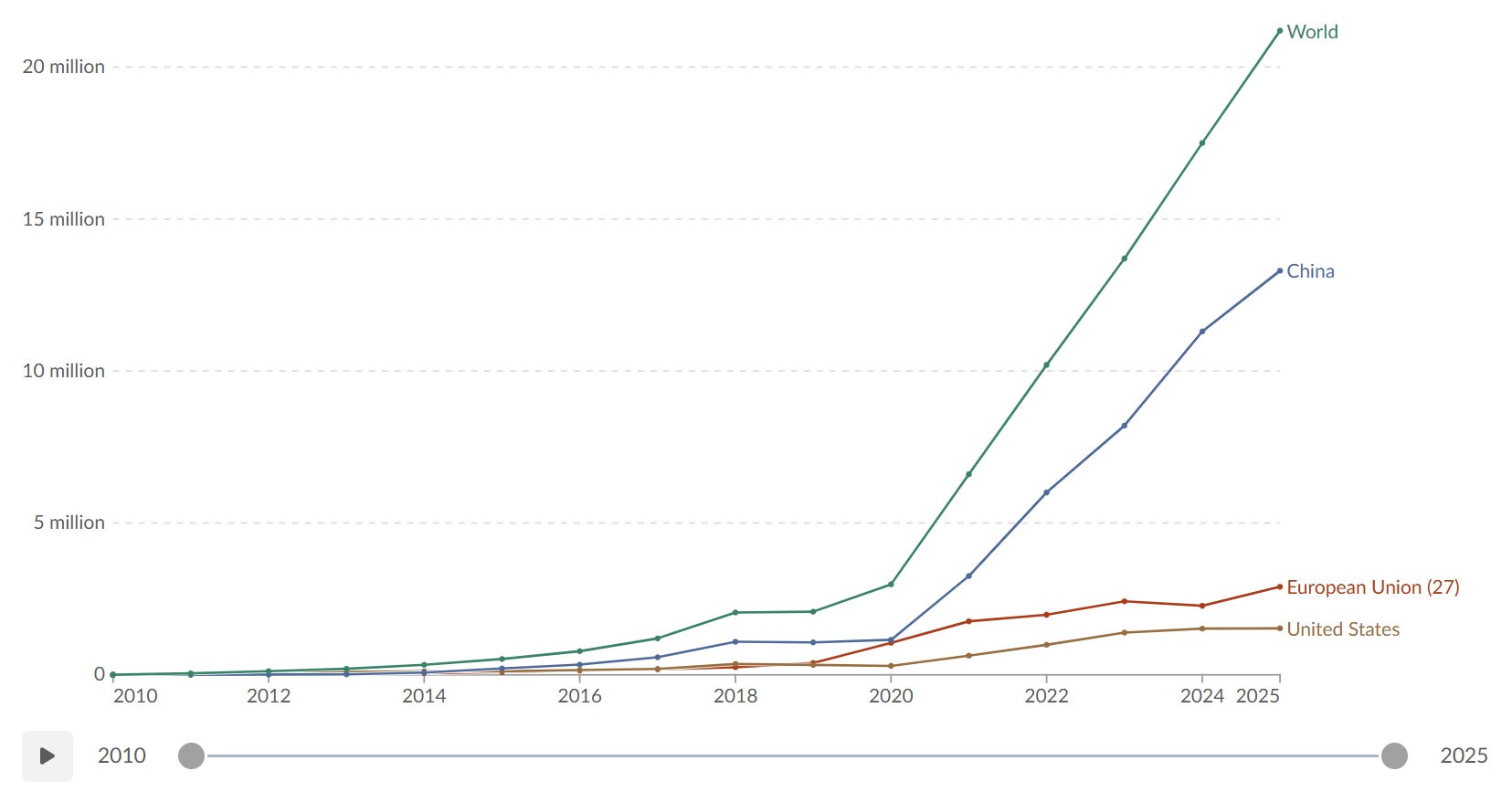

The starting point is the price of solar panels. Module prices fell by about 90% between 2010 and 2024, from about $2.44 to $0.26 per watt, according to Our World in Data. Lower prices encouraged greater production, and the effect became clear in 2025, when solar met about 75% of the growth in global electricity demand. In the same year, renewables reached 33.8% of global power generation, and overtook coal (33%) for the first time in a century. China accounted for more than half of the new solar capacity.

A technology expanding at this rate is no longer a small segment of the market; it is becoming a central one.

Further gains are already in development. Mainstream silicon panels convert about 22–23% of sunlight into electricity today, while tandem perovskite-silicon cells reached a certified 34.85% in 2025, against a theoretical limit in the mid-40s. As these tandem cells move toward mass production, the same installation will generate more power, and costs will decline again.

To read: Global Electricity Review 2026 (PDF)

Storage

The main limitation of solar power is that it does not generate electricity at night. Battery storage addresses this by storing electricity during the day and releasing it later.

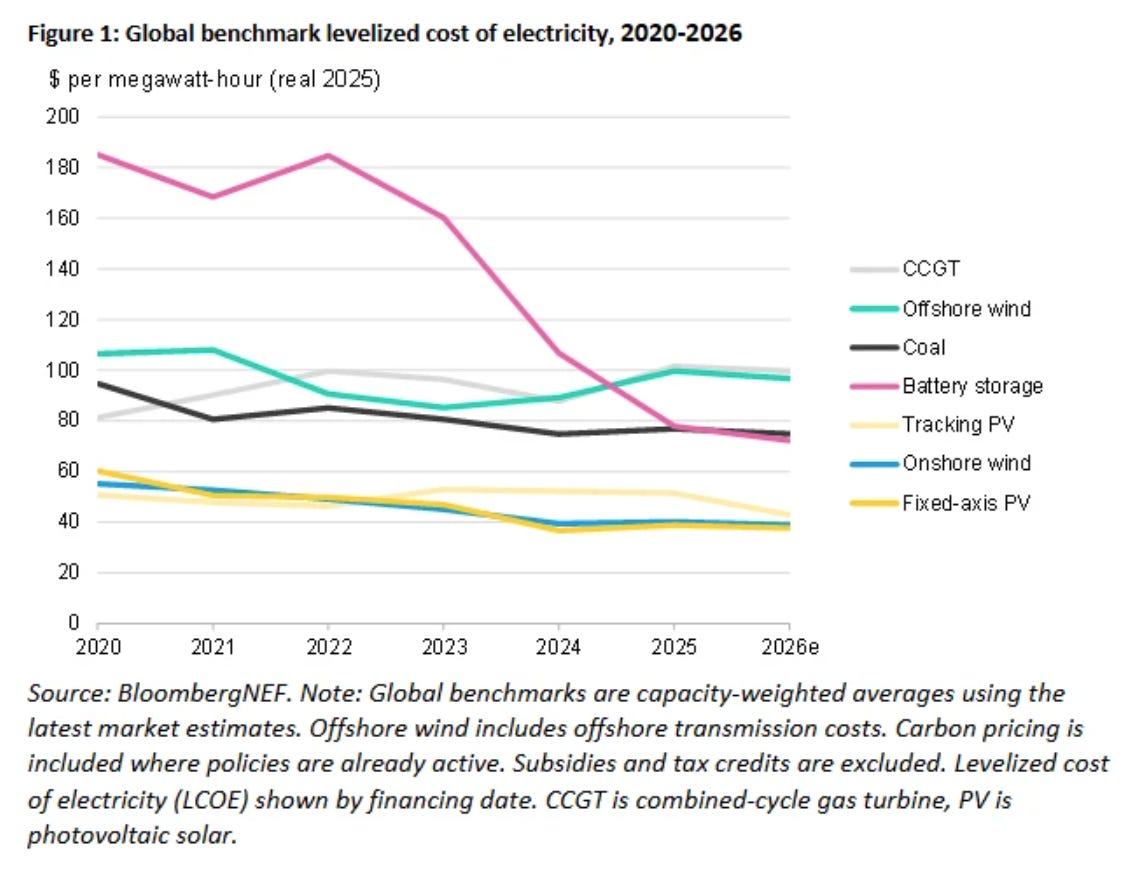

The economics changed in 2025. According to BloombergNEF, the cost of a four-hour battery fell 27% to $78 per megawatt-hour (MWh), the lowest level since 2009, while the cost of a new gas plant rose 16% to a record $102 per MWh. A combined solar-and-storage system reached about $57.

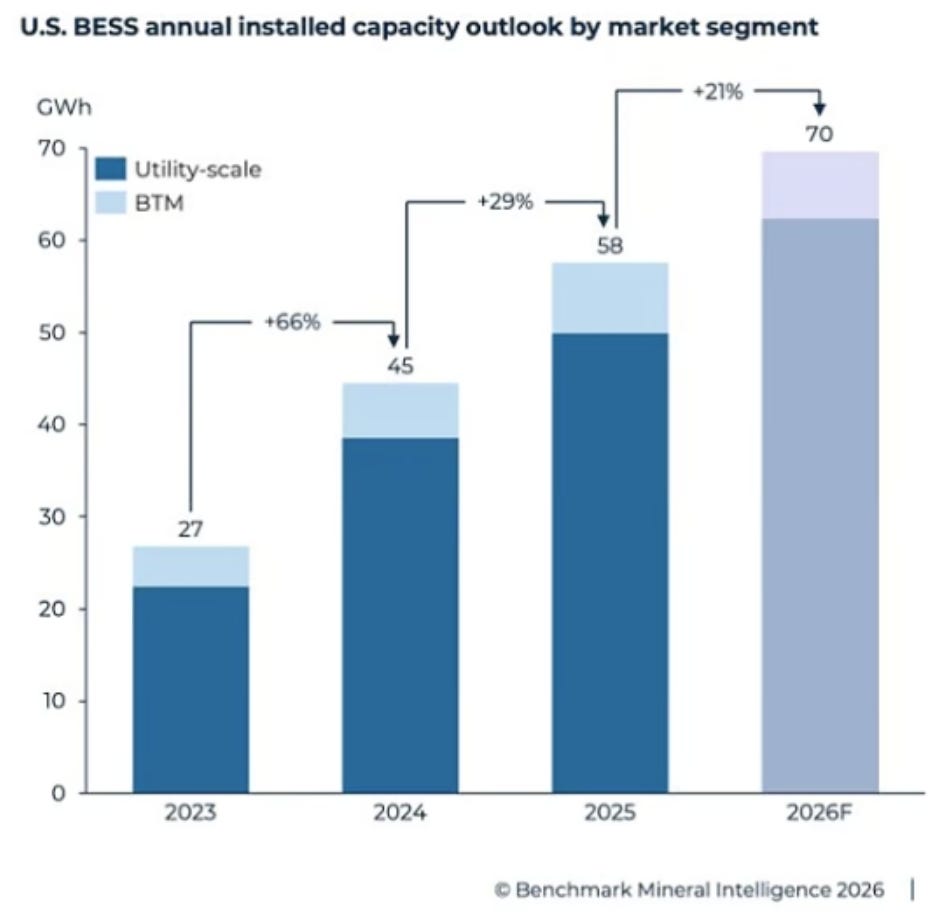

These figures are supported by falling input costs: battery costs declined 20% in 2024, and a further 45% in 2025, and electric-vehicle battery packs reached a record low of about $108 per kilowatt-hour (kWh). New solar farms are now priced near $39 per MWh and onshore wind near $40, both below the cost of a new gas plant. As a result, new gas plants are increasingly difficult to justify on cost. The scale of the change is significant: the United States added a record 28 gigawatts (GW), or 57 gigawatt-hours (GWh), of storage in 2025.

To read: Meta, Amazon, Google, and Microsoft Dominate Clean Energy Deals as Global Buying Slips in 2025

The implication is clear. The lowest-cost method of adding reliable, on-demand power is no longer a gas turbine but solar combined with a battery. This favours large-scale developers and independent power companies with storage projects, battery system suppliers, and the core equipment of the grid, including cells, inverters, and cabling.

A further consideration is battery chemistry. Lithium iron phosphate (LFP) has become the standard cell for grid storage because it is low-cost, safe, and durable. Sodium-ion technology is now emerging: it holds less than 1% of the market, but it is scaling quickly. CATL, the largest battery manufacturer, has signed the largest sodium order to date, at 60 GWh. Sodium requires no lithium, cobalt, or nickel, may prove a third or more cheaper than LFP, and performs well in cold conditions. If it succeeds, it reduces the most significant supply risk in the sector.

Demand

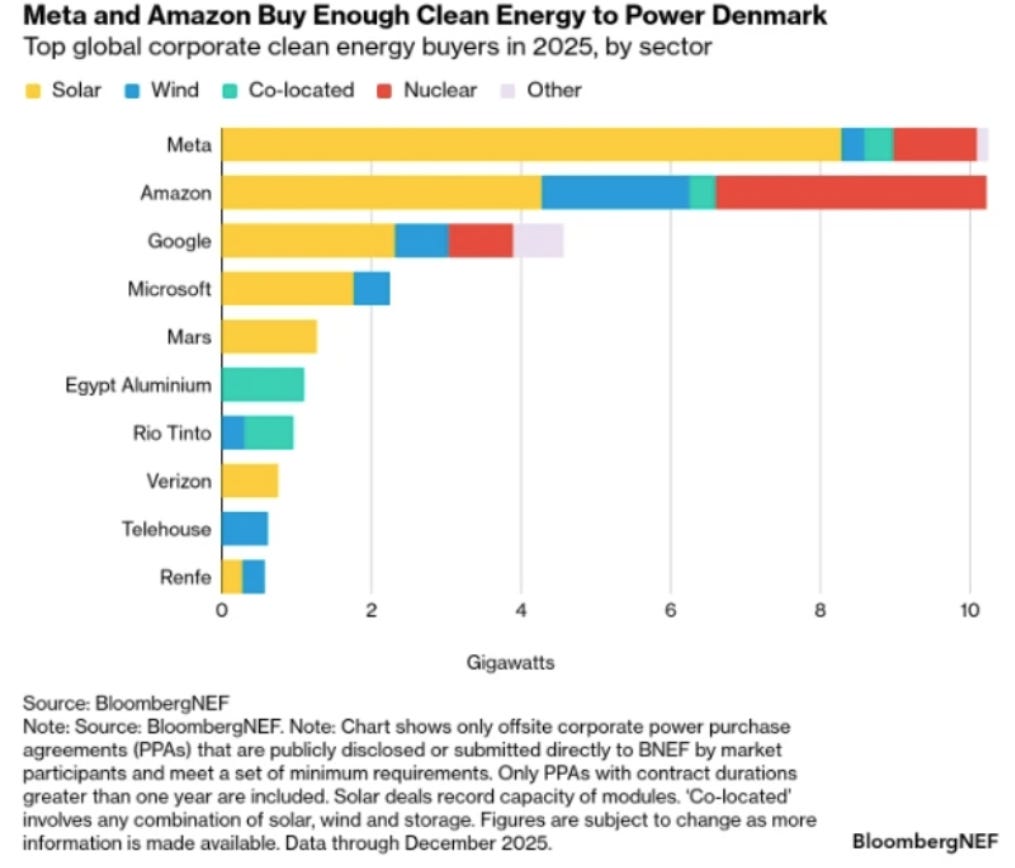

Electricity demand is rising sharply because of artificial intelligence, and the buyers are among the largest companies in the world. In 2025, four firms - Amazon, Microsoft, Google, and Meta - signed about half of all clean-power agreements globally, and total corporate purchasing reached about 55.9 GW.

These companies commit to twenty-year power purchase agreements (PPAs) because clean power is the lowest-cost reliable supply they can secure at large scale. A long-term, twenty-year contract will guarantee a fixed electricity price and allow you to cover a part of your consumption with renewably sourced power.

Demand for new data centre capacity is substantial, and each facility requires steady, low-carbon power. This demand flows into grid equipment, high-voltage components, and, for continuous baseload supply, renewed investment in nuclear power and uranium. This area offers some of the least crowded exposure in the sector.

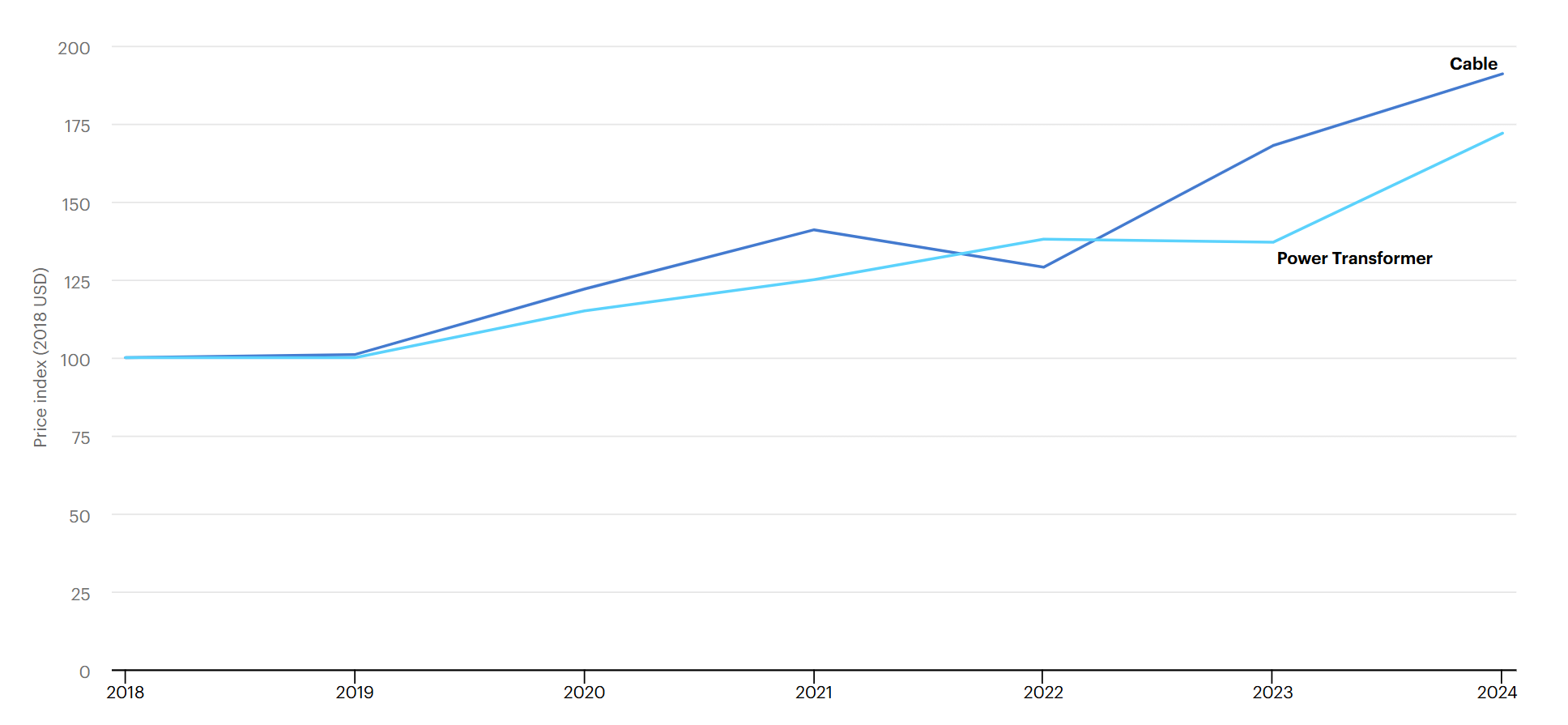

The Grid

The most significant constraint on this transition is the transmission network. A solar farm can be built in months, but the transmission required to connect it takes years. The International Energy Agency (IEA) reported about 1,650 GW of solar and wind capacity waiting in connection queues in 2024. Over the past decade, only about 1.5 million kilometres of new transmission lines were built, well below what is required.

This constraint represents an opportunity. Transmission builders, transformer and high-voltage equipment manufacturers, cable suppliers, and grid-upgrading technology all supply a market that will remain short of capacity for years, which supports strong pricing power.

Materials

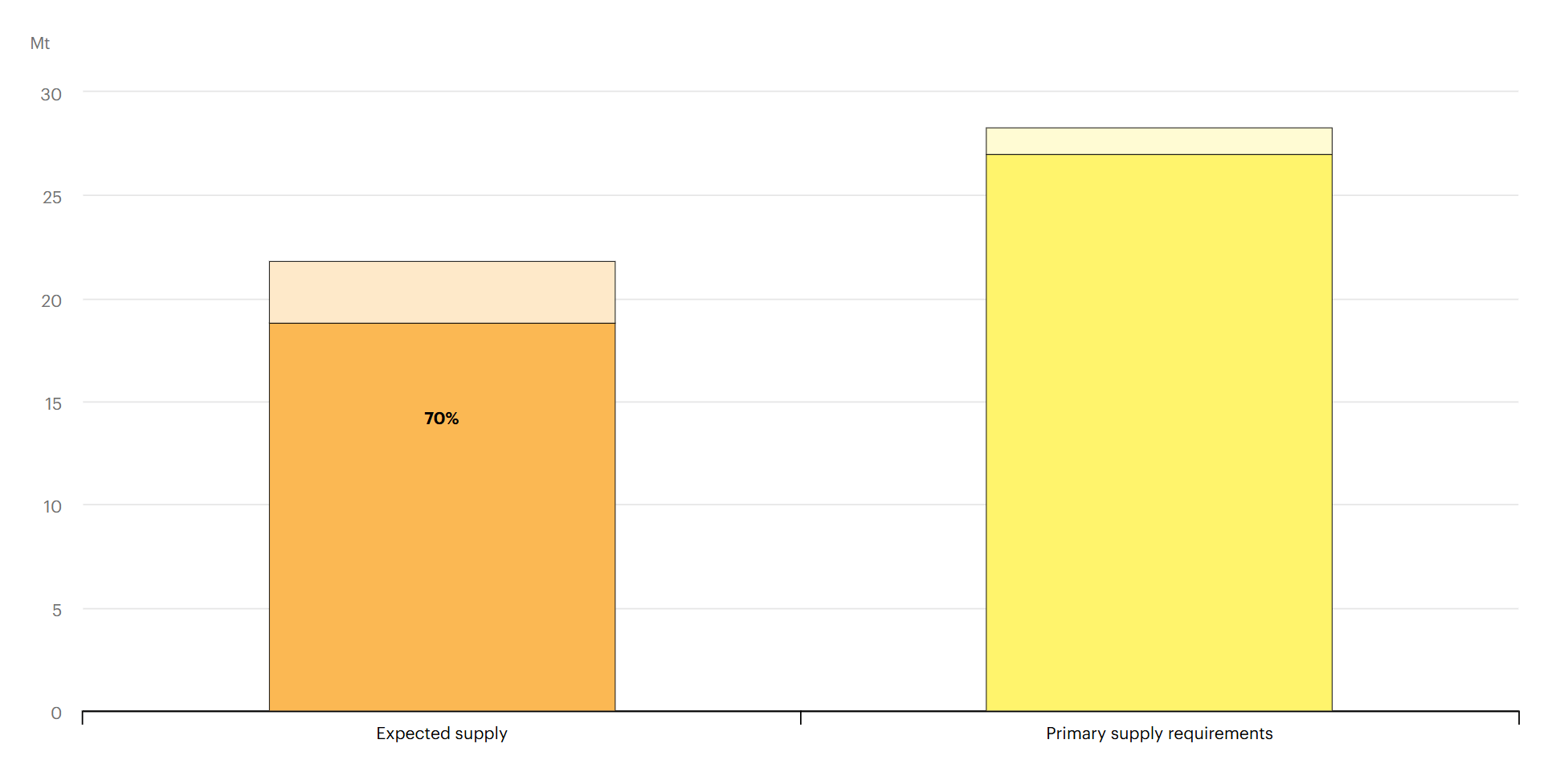

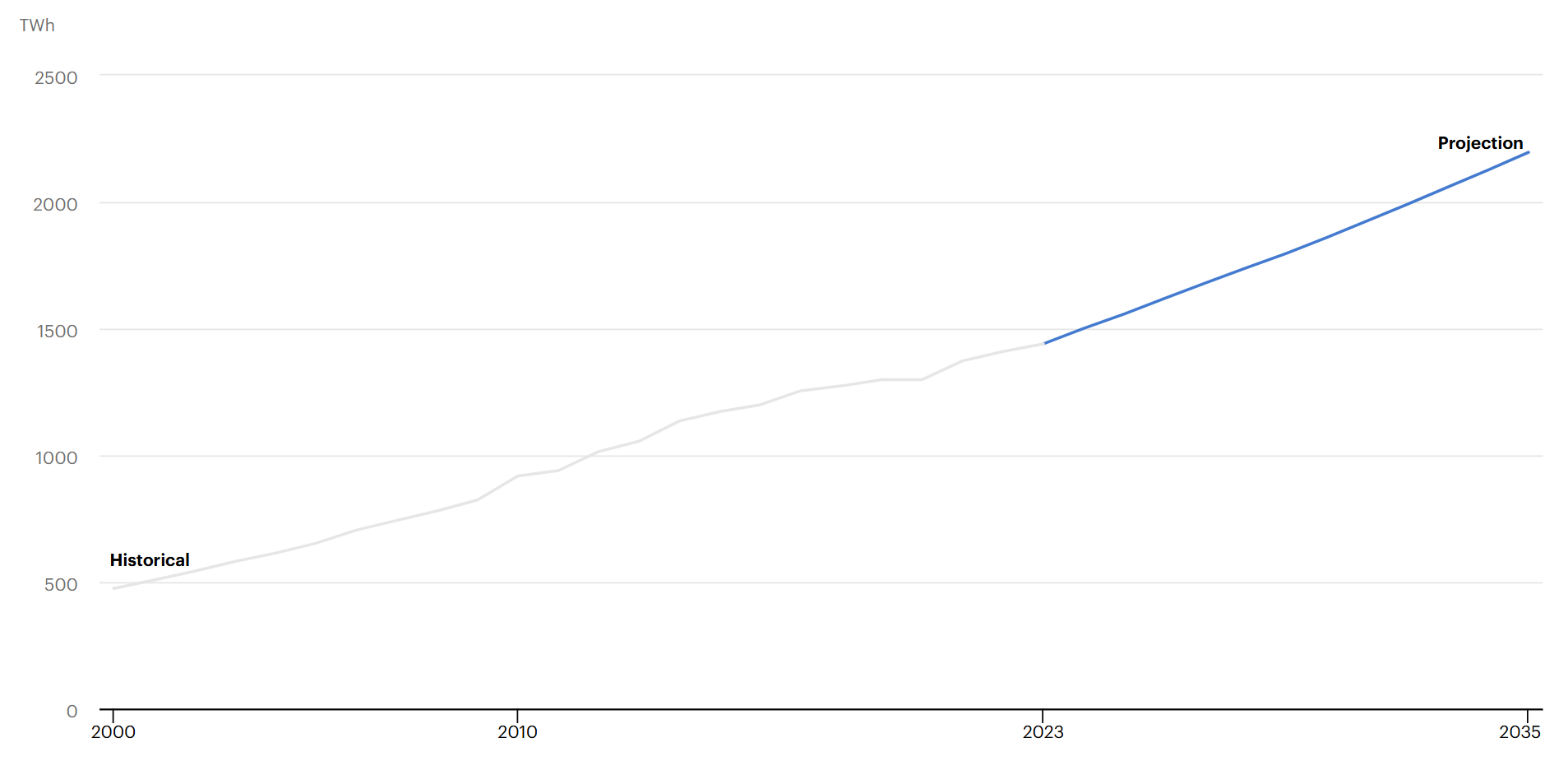

The same demand extends to raw materials. Copper, which is used in wiring, motors, and transformers, had demand of about 27 million tonnes in 2024, projected to reach roughly 33 million by 2035.

The IEA warns that announced projects will cover only about four-fifths of copper requirements by 2030, with a shortfall approaching a third by 2035.

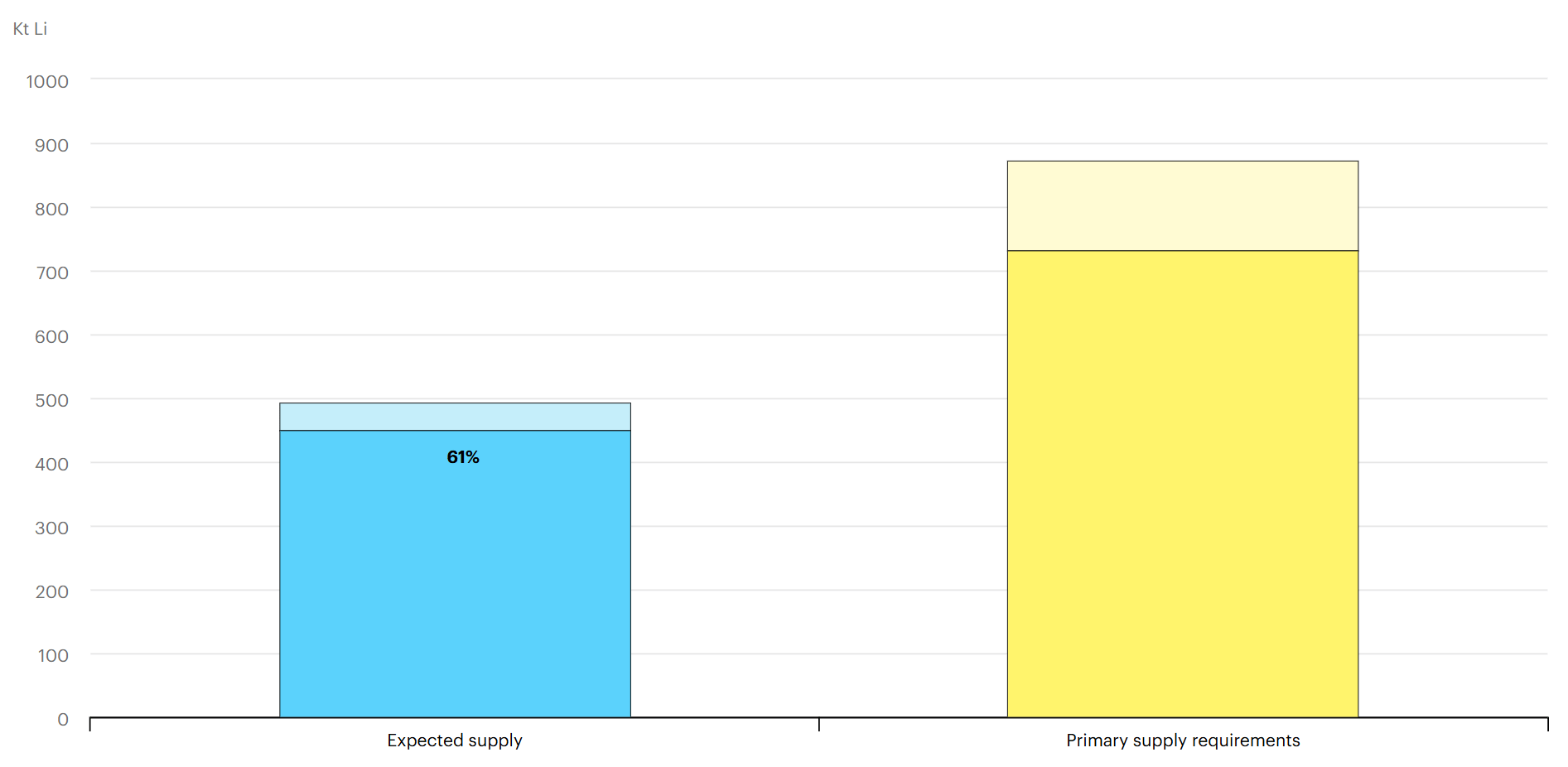

Lithium demand could increase four to six times by 2030.

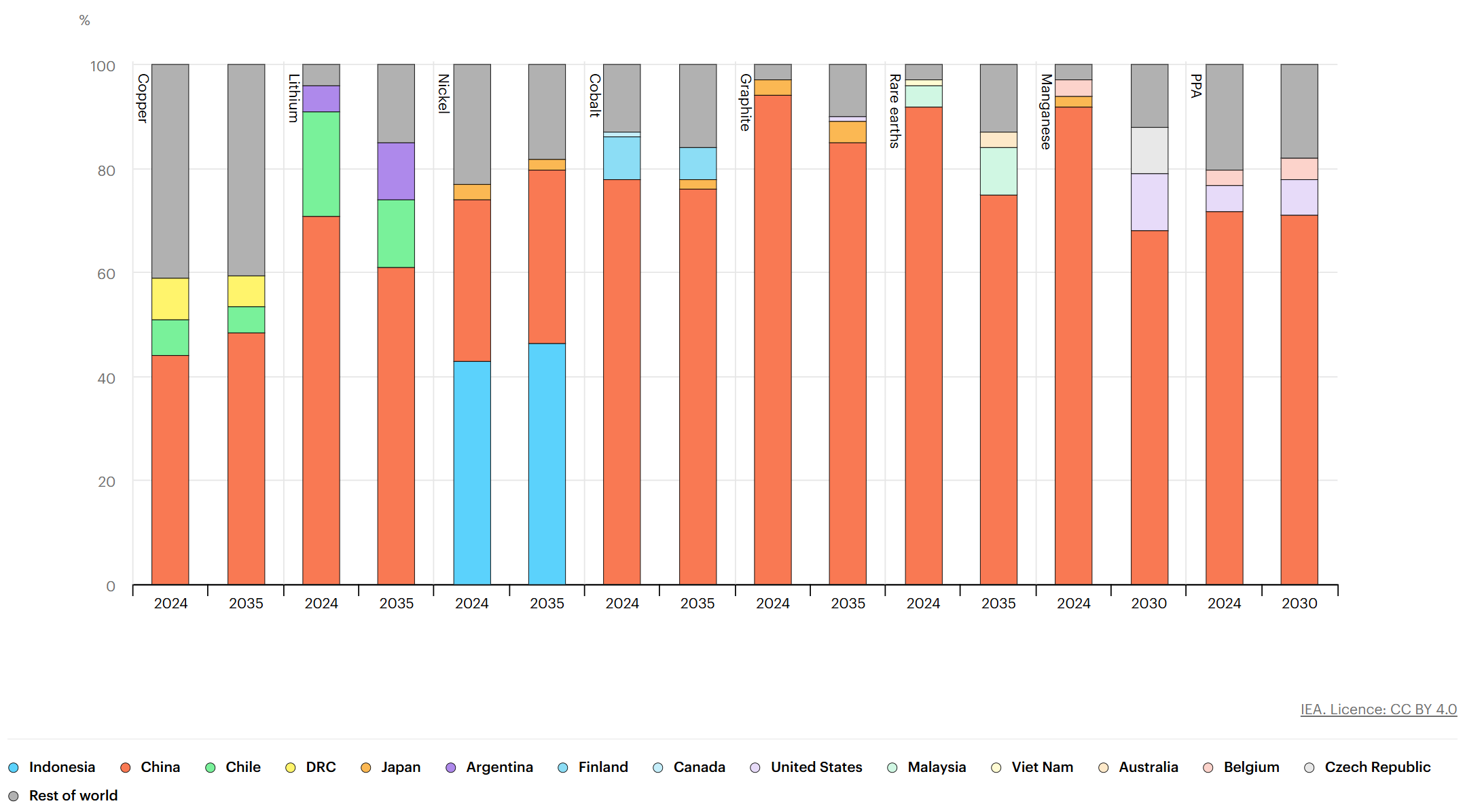

Processing is also highly concentrated: China refines between half and nearly all of the world’s key battery metals, depending on the material.

Recycling, sometimes called urban mining, provides some relief; the IEA estimates it could reduce primary supply requirements by about a tenth by 2040, as the first large group of used batteries reaches the end of its life. The relevant investments here include miners, refiners, and battery recyclers.

Transport

Electric car sales exceeded 20 million in 2025, and one in four new cars sold worldwide is now electric. In Norway, the figure is 97%. Global sales of combustion-engine cars, by contrast, already peaked in 2017. This represents a gradual decline in oil demand.

The world consumes more than 100 million barrels of oil a day. Electric vehicles (EVs) reduced this by about 1.2 million barrels a day in 2025, and the IEA expects the figure to reach 5.4 million by 2030, with total oil demand stabilization toward the end of the decade.

Geopolitics

The actions of oil producers are more informative than their statements. Across the Middle East and North Africa, governments are building solar and nuclear capacity at home so they can export more of their oil and gas and stabilise their budgets.

To watch: The Middle East has built the largest solar farm in the world. Here's why. (YouTube)

The IEA projects that oil’s share of the region’s own electricity will fall to about 5% by 2035, while regional nuclear capacity triples to 19 GW. When the lowest-cost producers reduce their own use of oil, the implications for oil-dependent economies are difficult to ignore.

Risks

The first is seasonality: solar output falls in winter, and a four-hour battery cannot cover an extended period of low sunlight, so wind and nuclear remain necessary.

The second is concentration: China produces most of the world’s panels and more than 70% of its EVs, which means tariffs and political decisions can disrupt the supply chain.

The third is timing: forecasters disagree on the peak in oil demand. ExxonMobil and BP place it near 2030, while S&P Global places it closer to 2034.

A cost trend does not fix a precise date, so investors should position for the direction rather than for exact timing.

The Evidence

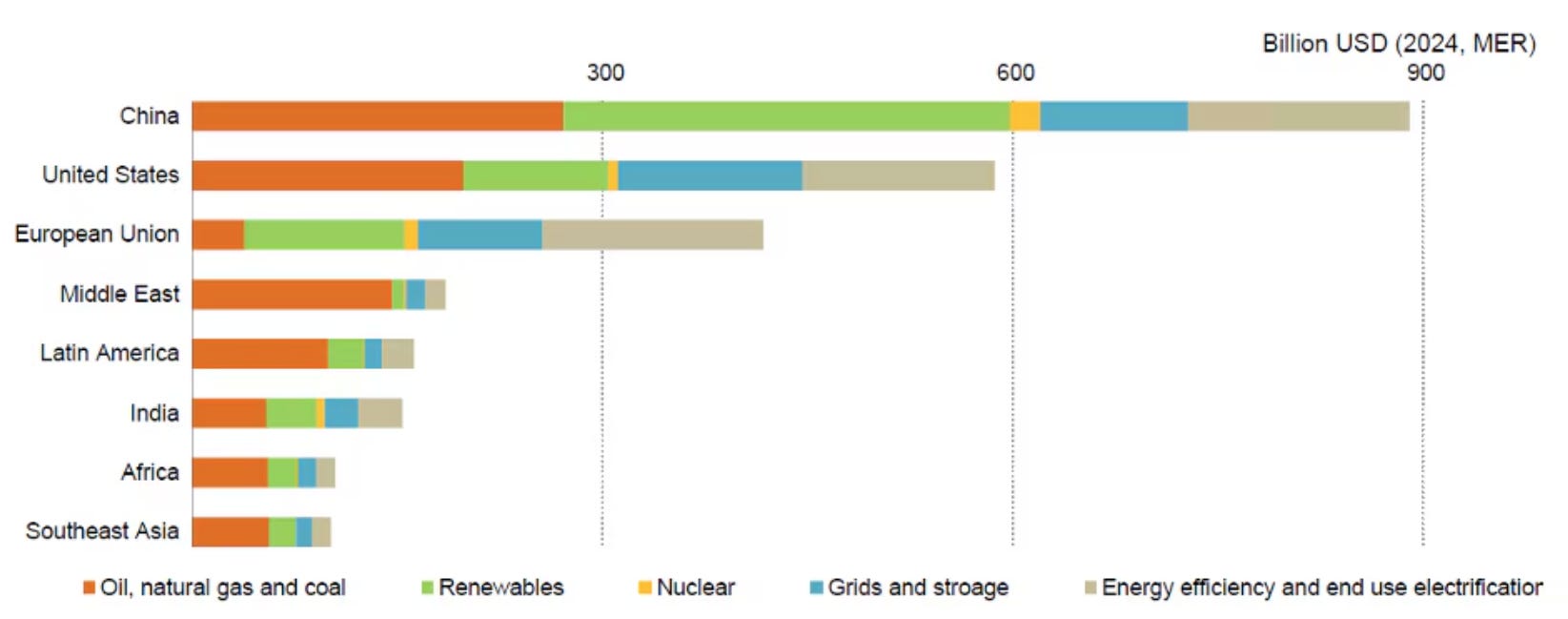

The pattern is confirmed by capital allocation. Global energy investment reached about $3.3 trillion in 2025. Of this, about $2.2 trillion went to clean energy, compared with $1.1 trillion for oil, gas, and coal - a ratio of two to one.

Solar alone attracted about $450 billion, the largest single item in the energy system, while grid-scale batteries received about $66 billion, and nuclear spending rose by half over five years.

The largest investors have already committed to this direction.

Conclusion

The evidence already points in one direction.

In 2025, solar supplied about three-quarters of the growth in world electricity demand; battery storage undercut a new gas plant for the first time, at $78 against $102 per MWh; and investors worldwide committed roughly two dollars to clean energy for every one to oil, gas, and coal. The trend has further to run, with BloombergNEF expecting battery costs to fall another 25% and solar another 30% by 2035.

The lowest-cost energy is now also the fastest-growing, yet market prices have not fully adjusted to that fact. That gap is the opportunity. Build exposure to the companies driving and supplying this change: developers, storage, the grid, nuclear, and the metals beneath it; and reduce exposure to the assets still priced for rising oil and gas demand.

You have read only the first part of the analysis. In the next post, I will write an overview of the publicly traded companies and funds worth keeping on your watch list.

This is not a financial or investing recommendation. It is solely for educational purposes.