Synopsys: High-Growth Play in Chip Design and Verification

Synopsys (SNPS) is a leading provider of electronic design automation (EDA) software and intellectual property (IP) solutions for semiconductor companies. The company helps engineers design complex chips by offering tools that improve efficiency, automate processes, and reduce errors. Its products are widely used by semiconductor and electronics companies worldwide.

➡️ Additional materials: PDF/PNG quick analysis, future of the EDA industry, SNPS vs CDNS, and valuation comparison with the industry

Content:

💡 Investment Thesis

🧐 Company Overview

🏰 Economic Moat

🚀 Business Strategy

🏛️ Capital Allocation

✅ Advantages

❌ Disadvantages

🥇 Competitors

⏮️ Past

📶 Future

💲Current Valuation

🏷️ Fair Price

☑️ Checklist

✍️ Due Diligence

💡 Investment Thesis

Synopsys is a dominant player in the EDA market, providing essential software and IP solutions for semiconductor companies. Its tools are deeply embedded in chip design workflows, making them critical for AI, high-performance computing, and advanced semiconductor manufacturing. With a strong economic moat built on high switching costs, deep industry partnerships, and continuous innovation, Synopsys is well-positioned for long-term growth.

The company's expansion into AI-driven chip design, system verification, and silicon lifecycle management strengthens its market leadership (together with Cadence - duopoly). Additionally, the pending $35 billion acquisition of Ansys will significantly expand its total addressable market, reinforcing its role in semiconductor and system-level simulation.

Based on my estimate, Synopsys is on track to achieve a revenue CAGR of at least 14% through 2030. The company’s strong financial position, high margins, and recurring revenue model provide stability and long-term profitability.

Currently, Synopsys remains an attractive investment, with its stock trading near fair value.

🧐 Company Overview

Market Cap: ~$70.82 Bil

Sector: Technology

Industry: Software - Infrastructure

Type: Large Core

Total Number of Employees: ~20,000

Website: www.synopsys.com

Next earning report: May 28, 2025 (estimated)

While EDA solutions are not directly involved in the manufacture of chips, they play a critical role in three ways. First, EDA tools are used to design and validate the semiconductor manufacturing process to ensure it delivers the required performance and density. This segment of EDA is called technology computer-aided design, or TCAD.

Second, EDA tools are used to verify that a design will meet all the requirements of the manufacturing process. Deficiencies in this area can cause the resultant chip to either not function or function at reduced capacity. There are also reliability risks. This area of focus is known as design for manufacturability (DFM).

The third area is relatively new. After the chip is manufactured, there is a growing requirement to monitor the performance of the device from post-manufacturing test to deployment in the field. The goal of this monitoring is to ensure the device continues to perform as expected throughout its lifetime and to ensure the device is not tampered with. This third application is referred to as silicon lifecycle management (SLM).

The broad Synopsys IP portfolio includes logic libraries, embedded memories, interface IP, security IP, embedded processors and subsystems. Synopsys’ IP Accelerated initiative provides architecture design expertise, pre-verified and customizable IP subsystems, hardening, and signal/power integrity analysis.

Semiconductor IP, or Semiconductor Intellectual Property, refers to intellectual property blocks or pre-designed and pre-verified components used in the creation of semiconductor chips or integrated circuits (ICs). Crucial building blocks like processor cores, memory controllers, interface protocols, and specialised functions are included in this intellectual property, which semiconductor companies can reuse or licence.

Designers can expedite the process of designing complex semiconductor devices, reduce development costs, and streamline workflows by utilising semiconductor intellectual property — Imagination Technologies.

For instance, in November 2023, Synopsys announced the extension of its ARC Processor IP portfolio to include the new RISC-V ARC-V Processor IP, enabling customers to choose from a broad range of flexible, extensible processor options that deliver optimal power-performance efficiency for their target applications. Synopsys ARC-V Processor IP includes high-performance, mid-range, and ultra-low power options, as well as functional safety versions, to address a broad range of application workloads.

Synopsys was founded in 1986 and has grown into a market leader through innovation and acquisitions. The company is led by CEO Sassine Ghazi, who took over in January 2024. Ghazi has been with Synopsys for over two decades and played a key role in its expansion into AI-driven chip design and simulation technologies. Under his leadership, Synopsys is aggressively expanding its market presence, focusing on AI integration, system-level design solutions, and acquisitions that strengthen its technological portfolio.

Synopsys generates revenue from three main segments: Time-Based Products, Upfront Products, and Maintenance and Services. In fiscal 2024, Time-Based Products accounted for 53% of revenue, Upfront Products contributed 29%, and Maintenance and Services made up the remaining 18%.

The company operates in multiple regions, with North America bringing in almost 45% of revenue, China 16%, Korea with almost 13%, and Europe 10%.

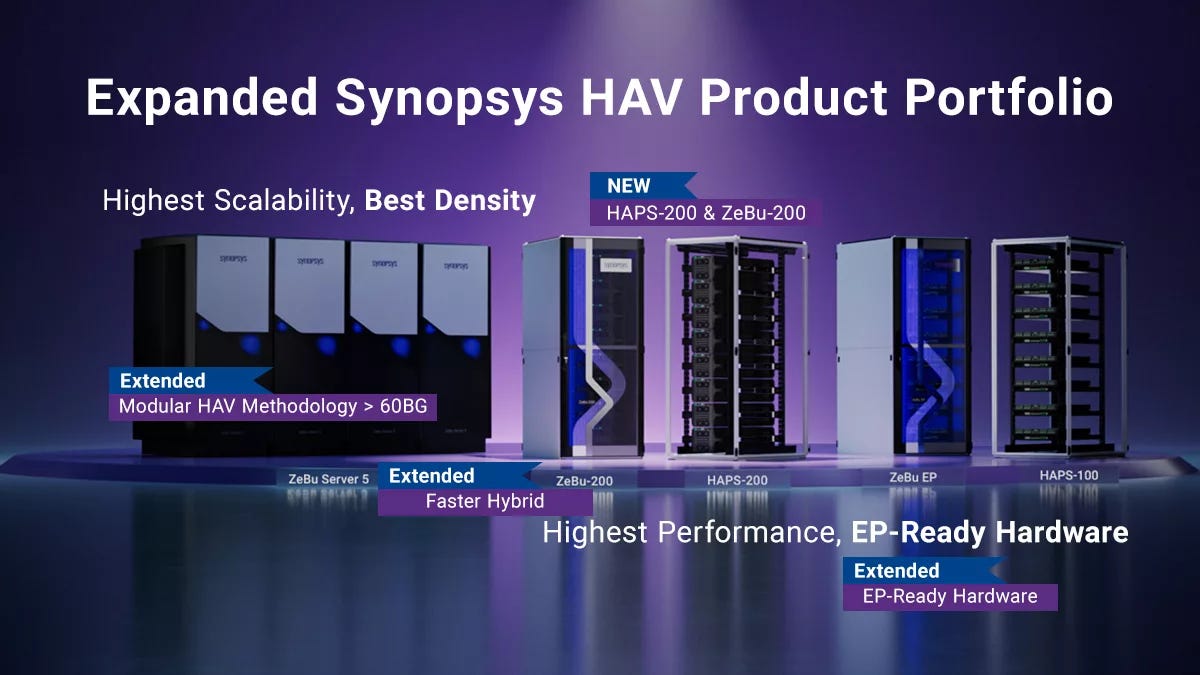

Synopsys HAPS-200 is the industry’s highest performance and most scalable pre-silicon prototyping system. Because of its high performance, HAPS is used in pre-silicon software development, as well as at-speed interface validation in the system environment.

Growing software, silicon, and system complexity requires advanced hardware-assisted verification (HAV) solutions to achieve first pass silicon success. Synopsys ZeBu-200 is the fastest emulation platform, making it the ideal platform to execute complex and long running workloads needed for power, performance analysis and software/hardware validation.

The increasing complexity of semiconductor chips and the rise of AI-driven designs continue to drive demand for Synopsys' products, positioning the company as a crucial player in the semiconductor ecosystem.

Synopsys serves a diverse range of clients, including major semiconductor manufacturers, technology firms, and system integrators. Some of its key customers include AMD, Arm, Intel Foundry, Microsoft, and Tesla. Additionally, Synopsys partners with third-party companies such as Taiwan Semiconductor Manufacturing Company (TSMC) and Samsung Foundry to optimize chip design processes and manufacturing.

To read: Success Stories

To read: AMD and Synopsys collaborate on the development of complex AI chips

🏰 Economic Moat

Synopsys has a wide economic moat due to its strong customer relationships, switching costs, and intangible assets. Its software tools are deeply integrated into client workflows, making it difficult for customers to switch providers without facing high costs and operational risks. The company also holds a dominant market position in EDA, competing primarily with Cadence Design Systems and Siemens EDA.

Synopsys and Cadence together control nearly 75% of the market, giving them significant pricing power and stability.

Expected growth rates further strengthen the company’s market leadership. The EDA segment is projected to grow at a 13% compound annual growth rate (CAGR) through 2030, while the IP segment is anticipated to grow at 14% over the same period.

🚀 Business Strategy

Synopsys’ business strategy focuses on continuous innovation, expanding into new markets, and strategic acquisitions. The company is investing heavily in AI to improve chip design and enhance automation. AI-driven tools are helping customers reduce time-to-market and increase efficiency.

A major development is the planned acquisition of Ansys for $35 billion (first half of 2025). This deal will expand Synopsys’ total addressable market by 50% to $28 billion.

Ansys (ANSS) is an engineering software company that provides simulation capabilities for structural, fluids, semiconductor power, embedded software, optical, and electromagnetic properties. Ansys employs over 4,000 people and serves over 50,000 customers globally.

Business segments:

Silicon Design and Verification: This segment is the backbone of Synopsys, providing a comprehensive portfolio of EDA tools. These tools facilitate the design, simulation, and verification of chips at various stages of development. It covers aspects such as logic synthesis, physical design, verification, and test solutions, which are crucial for creating semiconductor products efficiently and effectively.

IP: Synopsys offers a broad range of pre-designed IP blocks, which semiconductor companies can integrate into their designs. This segment includes IP for various functions such as memory, interfaces, processors, and security protocols. By implementing these pre-built blocks, companies can accelerate time-to-market and reduce design risk.

Software Integrity: This segment focuses on application security and quality. Synopsys provides solutions to ensure that software is secure, high quality, and compliant with industry standards. These include static and dynamic analysis tools, software composition analysis, and security testing services, which help organizations identify and mitigate potential vulnerabilities early in the development cycle.

Read also:

🏛️ Capital Allocation

Synopsys follows a disciplined capital allocation strategy focused on long-term growth, maintaining financial flexibility, and enhancing shareholder value. The company has strong cash reserves and minimal debt, allowing it to reinvest in its core business while pursuing strategic acquisitions.

As of writing this analysis, Synopsys holds $3.81 billion in cash and short-term investments, with only $665 million in total debt. This low leverage provides financial flexibility for investments in R&D, acquisitions, and operational expansion without heavy reliance on external financing.

Synopsys does not currently pay dividends, but it is prioritizing reinvestment in growth initiatives. The company believes that funding innovation, acquisitions, and technology expansion offers higher long-term returns than distributing cash to shareholders. Strengthening its competitive position remains the priority.

Synopsys has a history of share repurchases to enhance shareholder value. Over the past five years, it has spent more than $3 billion on buybacks, reducing outstanding shares and supporting earnings per share growth. However, buybacks were paused in 2024 due to the pending $35 billion Ansys acquisition, which is expected to expand Synopsys' market leadership in semiconductor design and system-level simulation.

R&D investment remains central to Synopsys’ capital strategy. The company allocates a significant portion of revenue to innovation, particularly in AI-driven automation, advanced chip verification, and system-level modeling.

To read: Acquisition History

✅ Advantages

Market Leadership: Synopsys holds a dominant position in the EDA market, with a market share of approximately 38%. The company's software is deeply embedded in semiconductor design workflows, making it indispensable to chip manufacturers.

Recurring Revenue Model: Nearly 80% of sales come from long-term contracts, providing stability and predictability in earnings. Customers rely on Synopsys’ tools for continuous chip development.

Financial Strength: The company has significant cash reserves and minimal debt, allowing it to invest in growth initiatives without financial strain.

Strategic Acquisitions: The planned acquisition of Ansys will strengthen its position in system-level design and simulation, expanding its product offerings and increasing its addressable market.

AI Integration: Synopsys’ AI-driven automation in EDA tools helps reduce design errors, improve productivity, and shorten time-to-market, keeping it ahead of competitors.

❌ Disadvantages

Strong Competition: The company faces intense competition from Cadence Design Systems. This competitor invests heavily in R&D and has strong customer bases.

➡️ Additional materials: SNPS vs CDNS

Customer Concentration Risk: A significant portion of Synopsys' revenue comes from a few large customers. Losing a major client could seriously impact financial performance.

Geopolitical Risks: Due to U.S. trade restrictions.

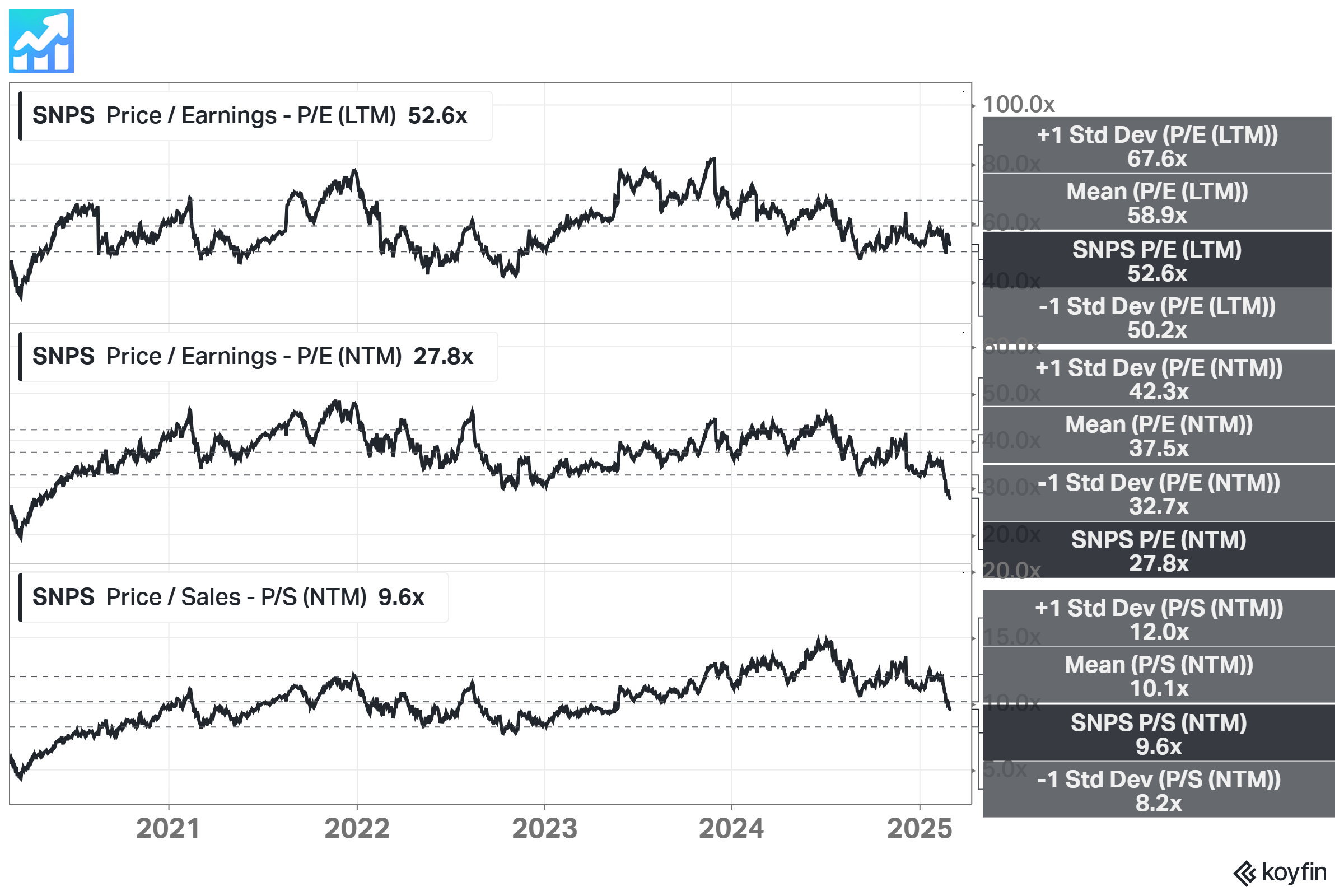

High Valuation: The stock trades at a high P/E ratio of 53.3, making it expensive compared to some peers. Any slowdown in earnings growth could lead to stock price declines.

Dependence on Semiconductor Cycles: If chip companies reduce R&D budgets during downturns, Synopsys' revenue growth could slow.

🥇 Competitors

Cadence Design Systems: Cadence is Synopsys’ closest competitor, with a 36% market share in EDA. Both companies dominate the industry, but Cadence has a stronger focus on system design and verification. While Synopsys has a broader IP portfolio, Cadence excels in analog and mixed-signal design tools.

Siemens EDA: Siemens EDA, formerly Mentor Graphics, is part of Siemens AG and has a more diversified business model. Unlike Synopsys, which focuses solely on EDA and IP, Siemens EDA benefits from integration with Siemens’ broader industrial and manufacturing software. This allows it to provide better services to automotive and industrial customers.

⏮️ Past

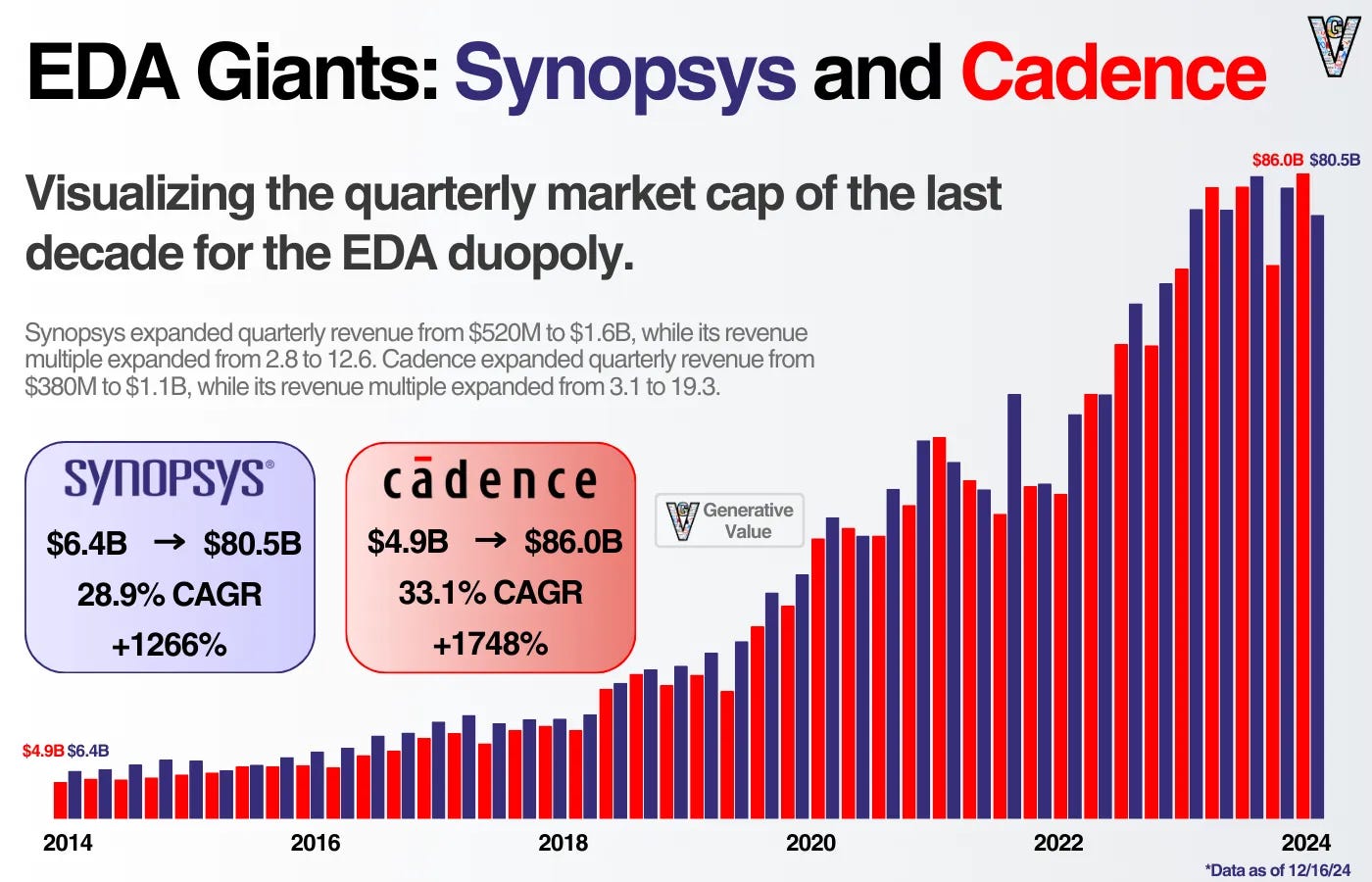

The CAGR rate for the SNPS stock over 5-, 10-, and 15-year time periods is shown above. During long-term periods, the stock significantly outperforms the S&P 500.

In the section Competitors, you can compare SNPS with the S&P 500 on a 10-year interval (the last chart in the section above): +844% vs. almost 230%. The difference is significant.

Below are some significant events from recent years.

Acquisition of Ansys: Synopsys announced a definitive agreement to acquire Ansys, a leading company in simulation and analysis software. This acquisition is expected to create a leader in silicon to systems design solutions, significantly expanding Synopsys' total addressable market.

Leadership Transition: Sassine Ghazi succeeded Aart de Geus as CEO of Synopsys in January 2024. Ghazi, with a 25-year history at the company, was crucial in leading AI-driven chip design at Synopsys.

Introduction of Synopsys.ai Copilot: In November 2023, Synopsys announced Synopsys.ai Copilot, a result of collaboration with Microsoft to integrate Azure OpenAI service for semiconductor design. This tool allows engineers to make natural language requests for chip design, addressing workforce shortages and increasing productivity.

📶 Future

➡️ Additional materials: future of the EDA industry

Below is the 3-year forecast for future sales and EPS growth, which is projected to be around 12.40% and 14.30%, respectively.

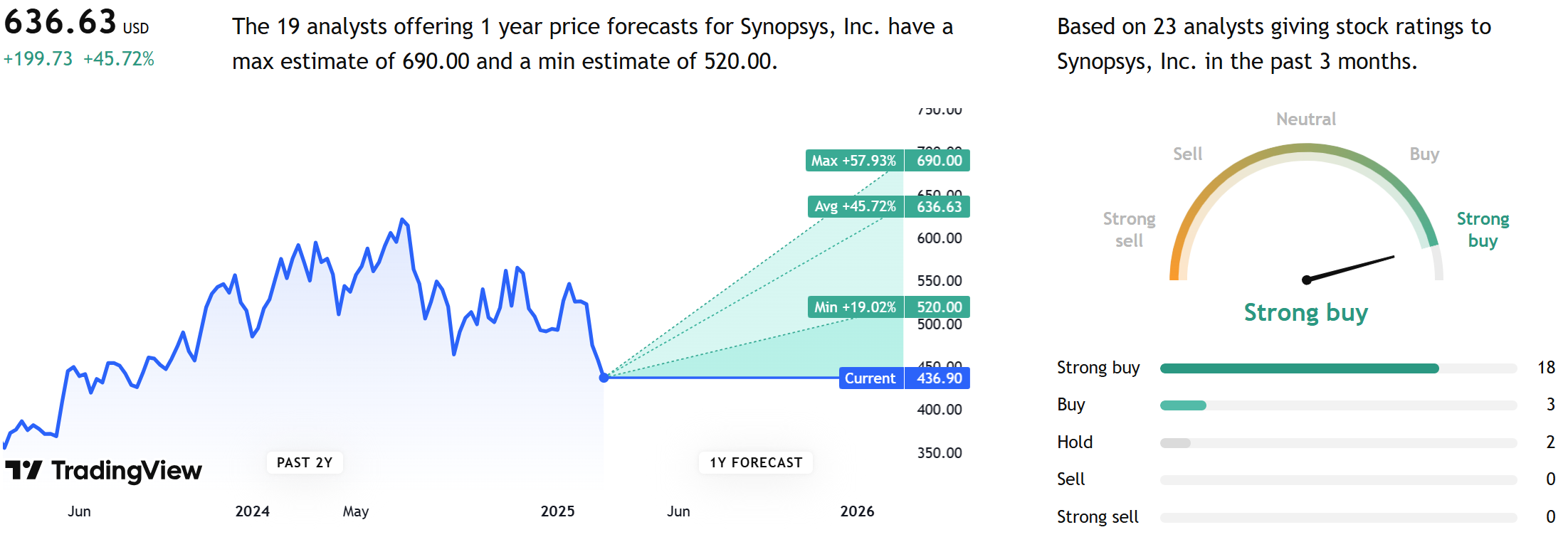

Based on 1-year price targets offered by other analysts, the average price target for SNPS comes to $636. The forecasts range from a low of $520 to a high of $690. The average price target represents an increase of 45.72%.

💲Current Valuation

Here are two charts showing the current valuation of SNPS stock. The company is trading below its 5-year averages, except for the Price/FCF ratio. But the company trades still relatively expensive, though. Also, please note that the PEG ratio remains above 2.

➡️ Additional materials: valuation comparison with the industry

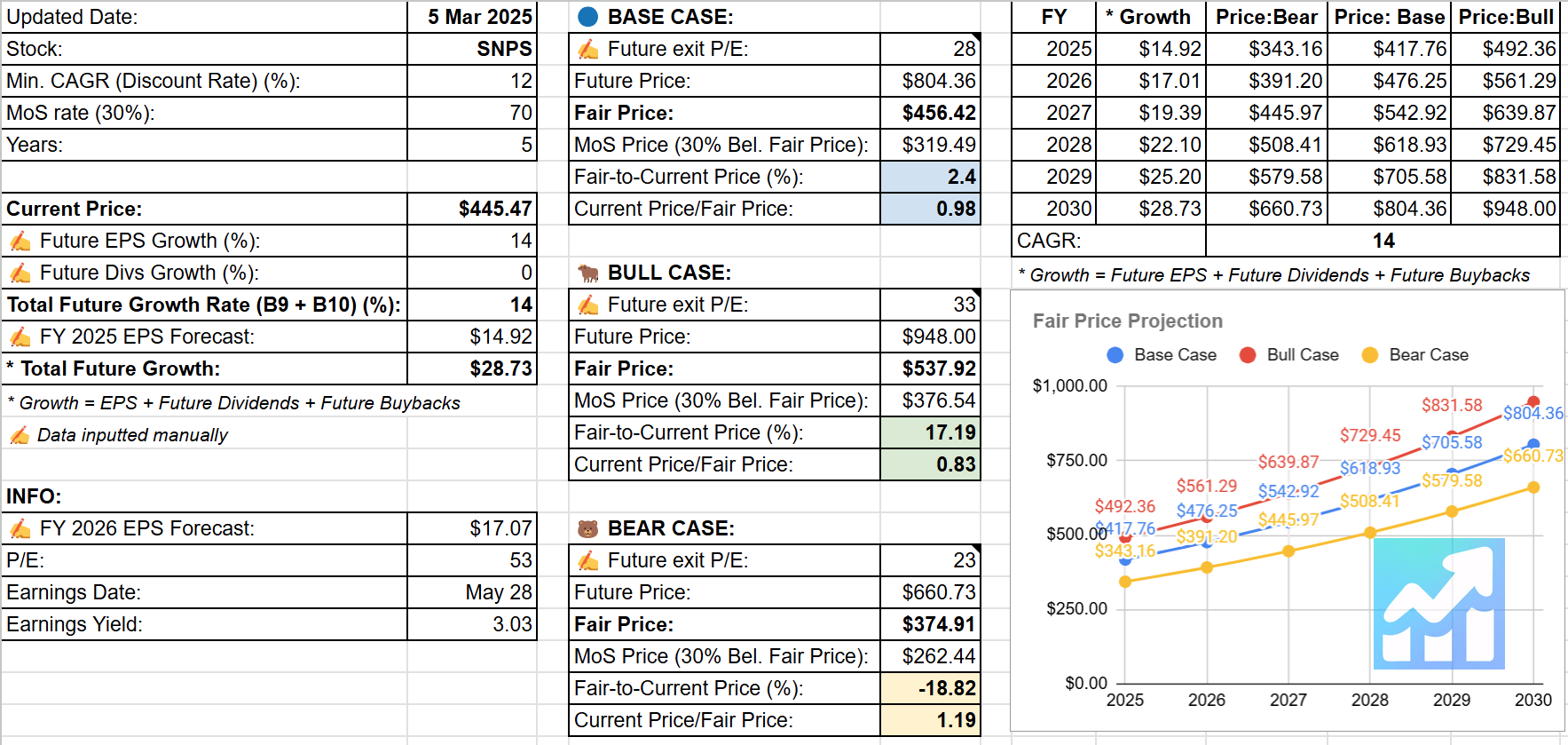

🏷️ Fair Price

Setting the future exit P/E values for SNPS was slightly complicated since the market has always estimated the stock high - take a look at the image below. I decided to use Future Growth Rate x 2 as the value for the Base Case (14 x 2 = 28). For the Bear Case, I subtracted 5 from the Base Case (23), and for the Bull Case, I added 5 to the Base Case (33). Please note that this remains pessimistic, so you may decide to look at the Bull Case, which is still below the average 5-year value (58.9).

The Long-Term Pick's Fair Price (Base Case) for SNPS is $456.42. The current price of $445.47 is lower by 2.4%.

Fair-to-Current Price (%): 2.4%

Current Price/Fair Price: 0.96

I used:

Discount Rate: 12%

Margin of Safety: 30%

Years: 5

Future EPS Growth Rate: 14%

Future Dividend Yield: 0%

Total Future Annual Growth Rate: 14 + 0 = 14%

☑️ Checklist

Profitability:

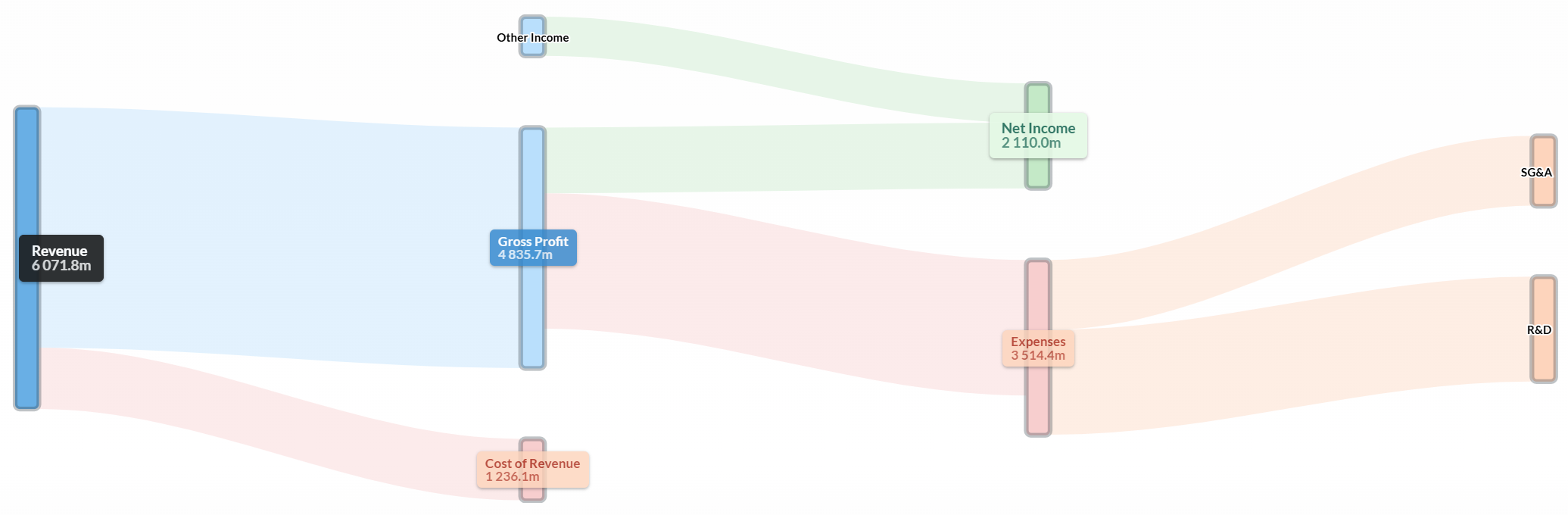

✅ Gross margin at least 40%: 79.6%

✅ Net margin at least 10%: 34.8%

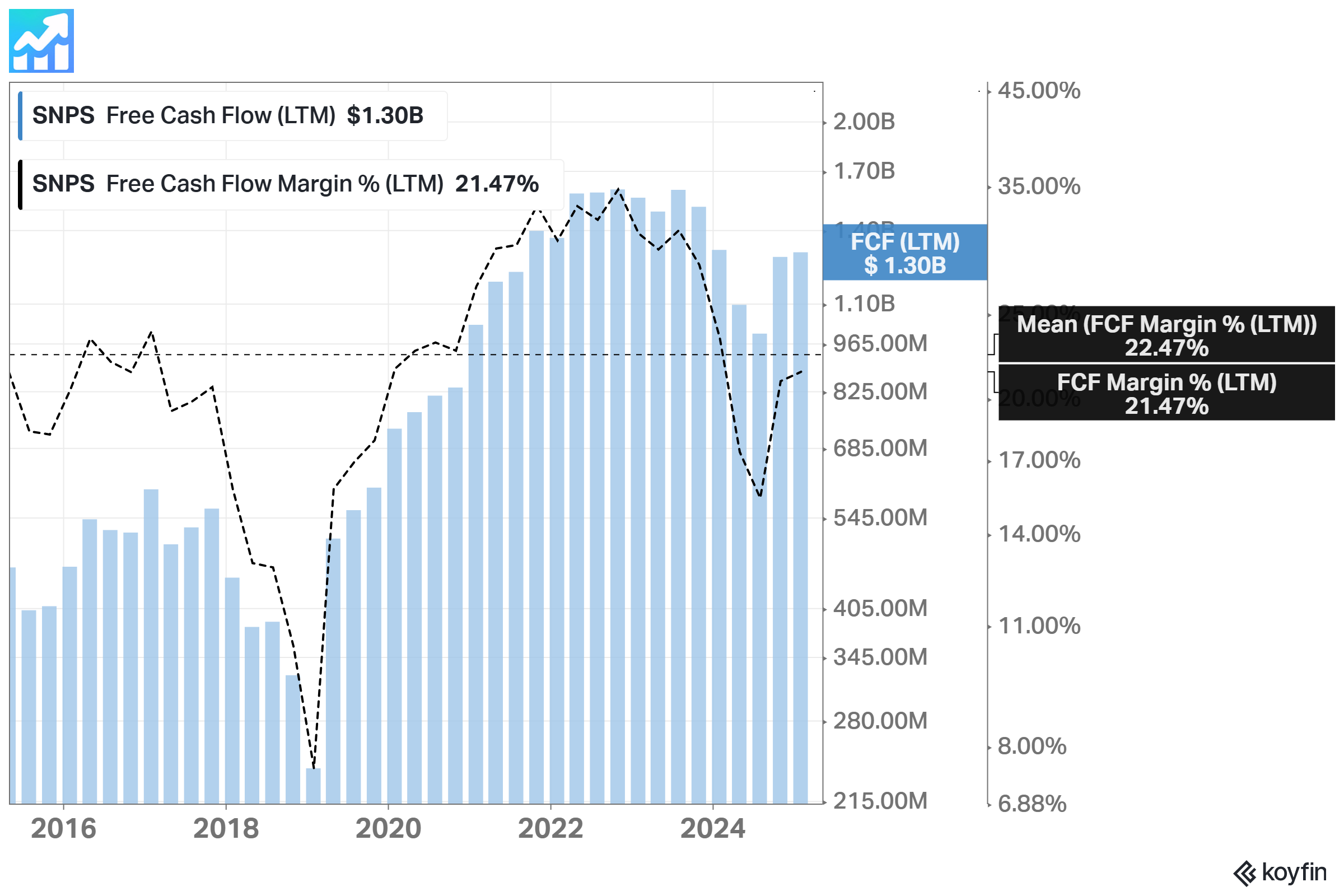

✅ FCF margin at least 10%: 20.0%

✅ Management (ROIC, ROCE, ROE, ROA): Yes (All above 10%)

🟡 Piotroski F-Score: 5 of 9 (Not passed: CFROA > ROA, Less Shares Outstanding yoy, Higher Gross Margin yoy, Higher Asset Turnover yoy)

✅ Revenue surprises in last 7 years: Yes (Based on TradingView's data)

✅ EPS surprises in last 7 years: Yes (Based on TradingView's data)

✅ EPS growth YoY 7 years in a row: Yes (Based on TradingView's data)

Valuation and Advantage:

✅ Valuation below its 5-year averages: Yes

❓ Valuation below the industry: available for patrons only

✅ Does it have a moat: Yes (wide)

✅ Outperformed the S&P 500 10-year CAGR: Yes (25.26% vs 12.65%)

Shares:

❌ Insider ownership at least 5%: No (0.47%)

❌ Less shares outstanding YoY: No

❌ Insider buys last six months: No

Price:

✅ 1-year stock price forecast is above 10%: +45.72%

✅ Next 5-year EPS growth estimates (CAGR) is above 10%: Yes (14.30%)

❌ DCF Value: $333.71; Overvalued by 24% (5 years, discount rate: 10%, terminal growth: 3%, equity model: FCFE)

✅ Short Interest below 5%: Yes (2.30%)

✍️ Due Diligence

Profitability (7 of 10):

✅ Positive Gross Profit: 4.88 USD (for the last twelve months)

✅ Positive Operating Income: 1.3B USD (for the last twelve months)

✅ Positive Net Income: 2.1B USD (for the last twelve months)

✅ Positive Free Cash Flow: 1.2B USD (for the last twelve months)

🟡 Positive 1-Year Revenue Growth: 1% (over the past 12 months)

🟡 Positive 3-Years Revenue Growth: 10% (per year for the last 3 years)

🟡 Positive Revenue Growth Forecast: 13% (per year over the next 3 years)

✅ Exceptional ROE: 26% (for the past 12 months)

✅ 3-Year Average ROE: 21% (three-year average)

✅ ROE is Increasing: 18% → 26% (in the last 3 years)

🟡 Positive ROIC: 13.5% (for the past 12 months)

🟡 3-Year Average ROIC: 14% (three-year average)

🟡 ROIC is Decreasing: 14% → 13.5% (in the last 3 years)

Solvency (8.5 of 10):

✅ Short-Term Solvency: short-term assets (6B USD) exceed its short-term liabilities (2B USD)

✅ Long-Term Solvency: long-term assets (13B USD) exceed its long-term liabilities (4B USD)

✅ Negative Net Debt: -3.8B USD (the company has more cash and short-term investments (4B USD) than debt (14m USD))

✅ Low Debt-to-Equity Ratio: 0

✅ High Altman Z-Score: 14.84 (whether a company is headed for bankruptcy - takes into account profitability, leverage, liquidity, solvency, and activity ratios)

This is not a financial or investing recommendation. It is solely for educational purposes.

If you like the content, please hit the like icon, leave a comment, and share the publication with your friends and colleagues - this will motivate the author. If you're ready to support the project and get access to additional materials, visit this page.

Dan, thanks. As always, a detailed overview!