GOOGL: Currently Undervalued by 50%

A comprehensive analysis of Alphabet Inc. (GOOGL), a global technology conglomerate best known as Google's parent company, shows significant long-term growth potential.

Changelog:

Feb 8, 2025: Updated fair price valuation: $218.

Jan 27, 2025: Overview: Renovation of AI portfolio, Record performance in Google Cloud, Failed acquisitions of Wiz and HubSpot, Major data center investments, Ongoing antitrust challenges, YouTube monetization updates, and Focus on sustainability.

Nov 01, 2024: Updated fair price valuation: $242.

A dominant search engine market share of over 80% globally, rising to 90% on mobile devices, and a rapidly growing cloud computing division. The company's diverse portfolio, including YouTube with over 2 billion monthly users and Android powering two-thirds of the world's smartphones, shows its expansive reach. Expecting a robust double-digit increase in revenue and placing significant emphasis on AI-powered innovations.

Previous analysis:

Content:

💡 Investment Thesis

🧐 Company Overview

🏰 Economic Moat

🚀 Business Strategy

✅ Advantages

❌ Disadvantages

🏛️ Capital Allocation

🥇 Competitors

📣 Recent News

⏮️ Past

📶 Future

💲Current Valuation

🏷️ Fair Price

☑️ Checklist

💡 Investment Thesis

Alphabet presents a compelling investment opportunity due to its dominant market position in digital advertising and strong growth in cloud computing. The company's core businesses, Google Search and YouTube, continue to show robust growth, while Google Cloud's rapid expansion demonstrates successful diversification. Heavy investments in AI across its product collection position it well for future growth.

While regulatory challenges present risks, Alphabet's wide economic moat and strong financial position provide significant advantages. The company's current valuation, trading below 5-year averages, suggests an attractive entry point. With projected double-digit revenue and earnings growth over the next three years and strategic investments in emerging technologies, Alphabet offers strong potential for long-term value creation. I believe the company is unlikely to be forced to split up to comply with antitrust laws.

🧐 Company Overview

Incorporated: 2007; IPO: 2008

Sector: Communication Services

Industry: Internet Content & Information

Stock Style: Large Core

Market Cap: $1.86 Tril.

Earnings Date: Oct 22 - Oct 28, 2024Alphabet Inc., a global technology conglomerate best known as Google's parent company, has built a strong portfolio of businesses ranging from online advertising to cloud computing and artificial intelligence (AI). Alphabet operates through three primary segments: Google Services, Google Cloud, and "Other Bets." Google Services, including Search, YouTube, and Google Play, form the core of its revenue, while Google Cloud and "Other Bets" represent areas of future growth and technological innovation.

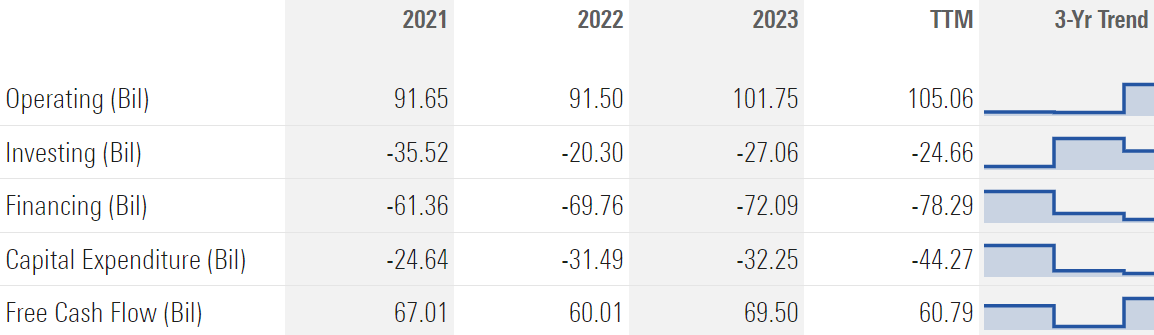

The company is recognized for generating tens of billions in free cash flow annually, strengthening its position as one of the most valuable companies globally.

Sundar Pichai is the current CEO of both Google and its parent company Alphabet. He joined Google in 2004 and became Google's CEO in 2015, later assuming the role of Alphabet CEO in December 2019 when co-founders Larry Page and Sergey Brin stepped down. Pichai previously executed as Google's product chief. Under his leadership, Google has increased its focus on artificial intelligence, cloud computing, and other emerging technologies. While Pichai leads operations, Page and Brin still hold over 50% of the voting power through Class B supervoting shares, maintaining significant influence over strategic decisions.

🏰 Economic Moat

Alphabet has a wide economic moat, supported by its dominance in search, advertising, and cloud services. Google Search, the company’s flagship product, holds over 80% of the global market share, rising to over 90% on mobile devices. Its brand recognition and network effects are central to this dominance, attracting both users and advertisers in a self-reinforcing cycle. The ability to collect data from billions of search queries each day allows Alphabet to offer highly targeted advertising solutions, ensuring advertisers see strong returns on their ad spend.

Outside search, Alphabet’s other platforms, such as YouTube and Google Cloud, also contribute to its moat. YouTube, with its large user base and diverse content, continues to attract advertisers and content creators. Meanwhile, Google Cloud, though smaller than competitors like AWS and Microsoft Azure, is growing rapidly and offers significant potential due to its cost advantages and AI-driven innovations.

🚀 Business Strategy

Alphabet's business strategy concentrated on maintaining its dominance in the advertising industry while expanding into high-growth areas such as cloud computing, AI, and new technologies. Alphabet is heavily invested in each of its key products and services to ensure it continues to lead in the digital ecosystem. Here's a closer look at its core products:

Google Search

Google Search is the backbone of Alphabet’s operations, driving a significant portion of its ad revenue. In Q2 2024, Google Search generated $48.5 billion in advertising revenue, growing by 14% YoY. Search remains Alphabet’s largest revenue contributor, with retailers, particularly those in Asia, fueling much of this growth. Alphabet’s ongoing investment in AI is designed to improve the search experience further. For instance, AI-powered features, such as search overviews, are being introduced to offer users faster and more relevant search results. These advancements also enhance the ability to deliver more personalized and targeted ads, increasing the overall effectiveness of Google’s advertising platform.

YouTube

YouTube continues to be a vital asset in Alphabet’s portfolio. It is one of the largest video-sharing platforms globally, with over 2 billion monthly users. While YouTube’s advertising growth slowed to 13% in Q2 2024, compared to 21% in the previous quarter, it remains a major contributor to Alphabet’s overall revenue. The platform generates income through ads, subscription services like YouTube Premium, and YouTube TV. With more than 8 million YouTube TV subscribers, the company is steadily building its subscription revenue alongside its traditional ad-supported model. YouTube’s ability to reach users across multiple devices—mobile, desktop, and TV—makes it a powerful tool for advertisers, ensuring its relevance in Alphabet’s broader advertising strategy.

Google Cloud

Google Cloud is one of Alphabet’s fastest-growing segments. In Q2 2024, it posted a revenue growth of 28%, marking the highest growth rate in the last 18 months. Google Cloud offers a suite of services, including Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS), competing directly with Amazon Web Services (AWS) and Microsoft Azure. As more businesses migrate to cloud-based services and AI-powered applications, Google Cloud is well-positioned to capture a growing share of this market. Alphabet has heavily invested in AI tools and infrastructure for Google Cloud, such as its proprietary Tensor Processing Units (TPUs), which give it a competitive edge in AI-driven workloads.

Alphabet’s strategy for Google Cloud is to continue scaling the platform while improving profitability. With AI becoming a critical part of enterprise solutions, Google Cloud’s offerings, including Google Workspace (a suite of productivity tools), are expected to play an increasingly important role in Alphabet’s overall business, contributing more than 20% of the company’s total revenue within the next five years.

Android and Google Play

Android, Alphabet’s mobile operating system, powers over two-thirds of the world’s smartphones. Google Play, the app marketplace associated with Android, is a key revenue generator, with income derived from app sales, in-app purchases, and advertising. By offering developers access to billions of users, Google Play attracts a vast range of applications and services, further cementing Android’s dominance in the mobile market.

Google has structured its Android ecosystem to promote its own services, such as Google Search and YouTube, through default preinstallations on devices. While regulatory scrutiny has targeted some of these practices, Alphabet’s ability to maintain control over the Android ecosystem ensures it continues to generate significant revenues from this segment.

Devices

While hardware products are not a major contributor to Alphabet’s overall revenue, the company has made significant strides in expanding its device offerings. The Pixel line of smartphones, Nest smart home products, and Fitbit wearables are some of the notable hardware initiatives. These devices are designed to integrate seamlessly with Google’s software and services, enhancing the user experience and encouraging further engagement within the Google ecosystem.

The Pixel smartphone has gained traction in specific markets, including Japan, where it holds around 10% market share. Meanwhile, Nest products, including smart thermostats and home security systems, position Alphabet as a player in the growing smart home market. Though hardware is not a core revenue stream, these devices help Alphabet keep users within its ecosystem, increasing usage of services like Google Assistant and YouTube.

Other Bets

Alphabet’s "Other Bets" include a range of forward-looking projects and moonshots, many of which are still in the developmental stages. Waymo, Alphabet’s autonomous vehicle project, is a standout in this category. Waymo is one of the leaders in self-driving technology and has been expanding its autonomous ride-hailing services in several U.S. cities. Verily, another notable "Other Bet," focuses on health and life sciences, to leverage technology to improve human health.

Although these projects are not yet profitable and have been a drag on Alphabet’s overall cash flow, the company continues to invest heavily in them. Alphabet’s strategy with "Other Bets" is to stay at the forefront of technological innovation, hoping that some of these ventures will become major revenue contributors in the future. Despite the risks, Alphabet’s financial strength — proven by more than $110 billion in cash reserves — allows it to sustain these investments without threatening its core business.

Alphabet’s "Other Bets" segment also includes Calico, a research and development company focused on longevity and health improvement. Calico is investigating ways to battle against ageing and improve human health through medical advancements, though it remains a long-term investment with no immediate commercial success.

Another key initiative is GV (formerly Google Ventures), Alphabet’s venture capital branch. GV invests in startups across a variety of industries, including healthcare, AI, and technology. This venture capital strategy helps Alphabet stay connected to emerging technologies and innovations that may support its future growth.

✅ Advantages

A diversified business model and strong dominance in key sectors like digital advertising, search, and cloud computing. The company’s vast ecosystem allows it to generate significant revenue from various sources, ensuring resilience even in challenging economic times. One of its core strengths is the ability to leverage its AI capabilities across all its products and services. With continuous investments in AI, Alphabet is not only improving user experience but also enhancing its advertising business, ensuring that ads are more targeted and relevant to users. This increases returns on ad spending for advertisers, making Google the go-to platform for digital advertising.

Google Cloud is also emerging as a significant advantage for Alphabet, with its revenue growing 28% in Q2 2024. As more businesses adopt cloud solutions and AI-driven tools, Google Cloud’s infrastructure and AI capabilities put it in a strong position to compete with giants like Amazon Web Services (AWS) and Microsoft Azure. Its own AI tools, like Tensor Processing Units (TPUs), give Alphabet a technological edge in handling AI workloads, making it a preferred choice for enterprises looking to integrate AI into their operations.

Alphabet’s financial strength is another key advantage. The company has over $110 billion in cash reserves and generates billions in free cash flow annually. This financial health allows Alphabet to invest in growth areas, such as AI, cloud computing, and "moonshot" projects, without sacrificing its core operations. Alphabet’s robust capital allocation strategy also includes aggressive share buybacks, which have reduced outstanding shares by 11% over the last five years, and a newly introduced dividend in 2024, further enhancing shareholder returns.

Additionally, the dominant position in the mobile ecosystem with Android is a major advantage. As the world’s most popular mobile operating system, Android serves more than two-thirds of global smartphones. The Google Play store, associated with Android, generates significant revenue through app sales and in-app purchases, benefiting from its vast user base.

YouTube, with over 2 billion monthly users, is another success. While advertising growth has slowed to 13% in Q2 2024, YouTube continues to make substantial revenue through ads and subscription services like YouTube Premium and YouTube TV. Its reach across mobile, desktop, and TV devices makes it a powerful platform for advertisers, ensuring Alphabet remains a leader in digital advertising.

Finally, the flexibility to stay ahead of the competition. Projects like Waymo (autonomous vehicles) and Verily (health sciences) hold long-term potential, allowing Alphabet to explore new markets and technologies that could become significant revenue streams in the future.

❌ Disadvantages

Regulatory scrutiny. Governments around the world are increasingly targeting Alphabet for its dominance in search and digital advertising, raising concerns about monopolistic practices. Antitrust cases, particularly in the U.S. and Europe, could lead to major operational changes if Alphabet is forced to change its business practices or divest certain assets. Privacy regulations, such as the General Data Protection Regulation (GDPR) in Europe, impose strict rules on how companies like Alphabet collect and use user data. With user privacy becoming a growing concern globally, more regulations could affect Alphabet’s ability to gather data for targeted advertising, which is a core part of its business.

The conglomerate also faces increasing competition from both established players and new entrants. Microsoft, through its investments in AI and the growth of Bing, poses a credible threat to Google Search. Amazon continues to be a tremendous competitor in cloud services, and emerging startups are challenging Alphabet in areas like AI and digital services. This competitive landscape creates pressure on Alphabet to continuously innovate and execute successfully, which requires substantial investment. The company must also navigate technological risks associated with AI, such as ethical concerns and regulatory compliance.

Emerging AI technologies, particularly advanced chatbots like ChatGPT or Claude, present a potential threat to Alphabet's core search business. These AI-powered conversational interfaces could change how users access information, potentially bypassing traditional search engines. If users increasingly turn to these chatbots for information retrieval and task completion, it could diminish Google's dominance in the search market and impact its primary revenue source from search advertising. While Alphabet is investing heavily in its own AI capabilities, including conversational AI, the rapid advancement and adoption of competing AI technologies represent a significant challenge to its established business model.

Dependence on ad revenue. The majority of Alphabet’s revenue comes from digital advertising, particularly from Google Search and YouTube. This makes the company vulnerable to shifts in global economic conditions. A downturn in the economy could lead to reduced advertising budgets, directly impacting Alphabet’s bottom line. Moreover, the increasing use of ad-blocking technologies and changes in user privacy expectations (such as Apple’s privacy features that limit tracking) could reduce the effectiveness of targeted ads, potentially affecting ad revenue. Changes in user behavior, such as the growing demand for privacy or reduced tolerance for intrusive ads, may also challenge the advertising model.

Many of these projects, including Waymo and Verily, have yet to generate meaningful profits and remain a drain on the company’s overall cash flow. Alphabet’s strategy of investing in long-term, high-risk ventures is ambitious, but there is no guarantee that these initiatives will succeed. As a result, the continued funding of these moonshot projects could distract resources from other profitable segments of the business.

Technological risks are also a concern. As Alphabet increases its focus on cloud services through Google Cloud, it must continuously strengthen its cybersecurity measures to protect against data violations and cyberattacks.

Global economic factors like inflation, supply chain disruptions, and potential recessions pose risks to Alphabet's hardware businesses, such as Pixel phones and Nest devices. Rising operational costs could impact the profitability of these products, especially in the face of supply chain challenges.

Public perception and brand risks are an ongoing concern. Issues like content moderation on YouTube, the spread of misinformation, and perceived monopolistic practices could lead to public backlash, eroding trust in the company. Managing employee satisfaction is also crucial for maintaining corporate culture and retaining top talent. Discontent within Alphabet’s workforce, including issues related to diversity or working conditions, could lead to unrest and talent attrition, harming the company’s innovative capabilities.

Alphabet must also contend with geopolitical issues that could affect its global operations. For example, the company’s inability to fully access the Chinese market due to government restrictions limits its growth opportunities in one of the world’s largest economies. Furthermore, increasing political tensions between countries could lead to sanctions or restrictions, potentially impacting Alphabet’s operations in key regions.

🏛️ Capital Allocation

Alphabet's approach to capital allocation is exemplary for its balanced focus on growth and delivering value to shareholders. Over the years, Alphabet has made several key acquisitions, such as YouTube, Android, and, more recently, cybersecurity firm Mandiant. These acquisitions have strengthened Alphabet’s core businesses while positioning it for future growth in cybersecurity and mobile software.

The company continues to invest heavily in research and development, with R&D spending consistently representing 14-16% of total sales over the past seven years. This trend is expected to continue as Alphabet invests in emerging technologies like generative AI.

The company also has an aggressive share buyback program, reducing its shares outstanding by 11% in the last five years. In Q2 2024, Alphabet authorized an additional $70 billion in buybacks, showing its commitment to returning value to shareholders. Additionally, Alphabet introduced a quarterly dividend in 2024, paying $0.20. I expect the company will leverage both its dividend and share repurchases as a way of shareholder distributions in the future.

🥇 Competitors

Alphabet faces competition from several major technology companies. In the cloud computing space, Google Cloud Platform competes with Amazon's AWS and Microsoft's Azure. These companies are also investing heavily in AI technologies, creating a competitive landscape in this emerging field.

In the advertising market, Alphabet competes with companies like Meta (Facebook) and Amazon, which have their own large user bases and advertising platforms. However, Google's search advertising is often seen as additional to these other platforms rather than directly replaceable.

Microsoft's Bing search engine is a direct competitor to Google Search, although it has struggled to gain significant market share. The potential emergence of AI-powered search engines presents a new competitive threat, although Google is also investing heavily in this area to maintain its leadership position.

Apple is a significant competitor, particularly in the mobile space. While Apple's iOS and iPhone don't directly compete with Google's core search business, they present a challenge to Google's Android ecosystem and Pixel smartphone line. The competition between iPhone and Pixel represents Alphabet's efforts to secure a base in the premium smartphone market. Additionally, Apple's focus on privacy and potential development of its own search engine could pose future threats to Google's dominance in mobile search and advertising.

📣 Recent News

On Sep 07, 2024, The U.S. Department of Justice planned to issue an outline by December on what Alphabet's Google must do to restore competition after a judge earlier found the company illegally monopolized the market for online search.

On Aug 28, 2024, Yelp complained for more than a decade that Google tilted the search market in its favor. After its rival’s landmark legal loss, it finally decided to sue.

On Aug 20, 2024, Alphabet extended its partnership with Shopify to allow all the eligible U.S. Shopify Plus and Advanced merchants to sign up for YouTube Shopping’s affiliate program through the Google & YouTube app on Shopify.

On Jun 6, 2024, Alphabet rolled out its AI-powered note-taking app, NotebookLM, in Australia, Brazil, Canada, India, the U.K., and 208 more countries and territories.

On Mar 13, 2024, Alphabet's Waymo made its fully autonomous ride-hailing service called Waymo One available for select members in Los Angeles, CA.

On Mar 4, 2024, Alphabet's Google Cloud announced the general availability of Anthropic’s new family of state-of-the-art models named Claude 3 on Vertex AI Model Garden.

⏮️ Past

During the second quarter, Alphabet's total revenues increased by 14% to reach $84.7 billion. Google Search and Cloud made significant contributions to this growth. The operating income grew by 26% to $27.4 billion, resulting in a 32% operating margin. Google Cloud generated over $10 billion in revenues and achieved a $1 billion operating profit for the first time. Alphabet expects further revenue growth, particularly in AI solutions, and anticipates an increase in operating margin for the full year 2024. Additionally, the company announced a new $5 billion investment in Waymo to advance its autonomous driving technology.

GOOGL has demonstrated strong long-term performance, outperforming both its industry and the broader market index over 10-year and 15-year periods with CAGR returns of 18.84% and 15.16% respectively. The company's 5-year CAGR return of 22.41% also exceeds industry and index performance. However, GOOGL has lagged in recent timeframes.

📶 Future

Alphabet expects continued revenue expansion, particularly in AI-driven solutions, for the upcoming periods. They caution that third-quarter operating margins will be impacted by increased depreciation and expenses associated with higher investments in technical infrastructure. Alphabet remains committed to aggressive investments in AI and cloud infrastructure, which they view as essential for long-term growth. The company expects to maintain its double-digit revenue growth trajectory, especially in areas like Google Search, YouTube, and Google Cloud, with AI applications playing an increasingly significant role in driving this growth. Additionally, Alphabet announced a new $5 billion investment in Waymo to further enhance its autonomous driving technology, signalling continued focus on innovation in emerging technologies.

Alphabet is projected to maintain strong growth over the next three fiscal years. Sales are expected to grow from $347.35B in FY2024 to $428.34B in FY2026, with annual growth rates gradually decreasing from 13.00% to 10.78%. EPS is forecasted to rise from $7.63 in FY2024 to $9.97 in FY2026, with growth rates ranging from 31.47% to 13.99%. Overall, the company is expected to deliver solid double-digit growth in both revenue and earnings, with EPS growth outpacing revenue growth.

Based on short-term price targets offered by 41 analysts, the average price target for Alphabet comes to $204.34. The forecasts range from a low of $170.00 to a high of $225.00.

An average brokerage recommendation (ABR) of 1.39 on a scale of 1 to 5 (Strong Buy to Strong Sell), was calculated based on the actual recommendations (Buy, Hold, Sell etc.) made by 44 brokerage firms.

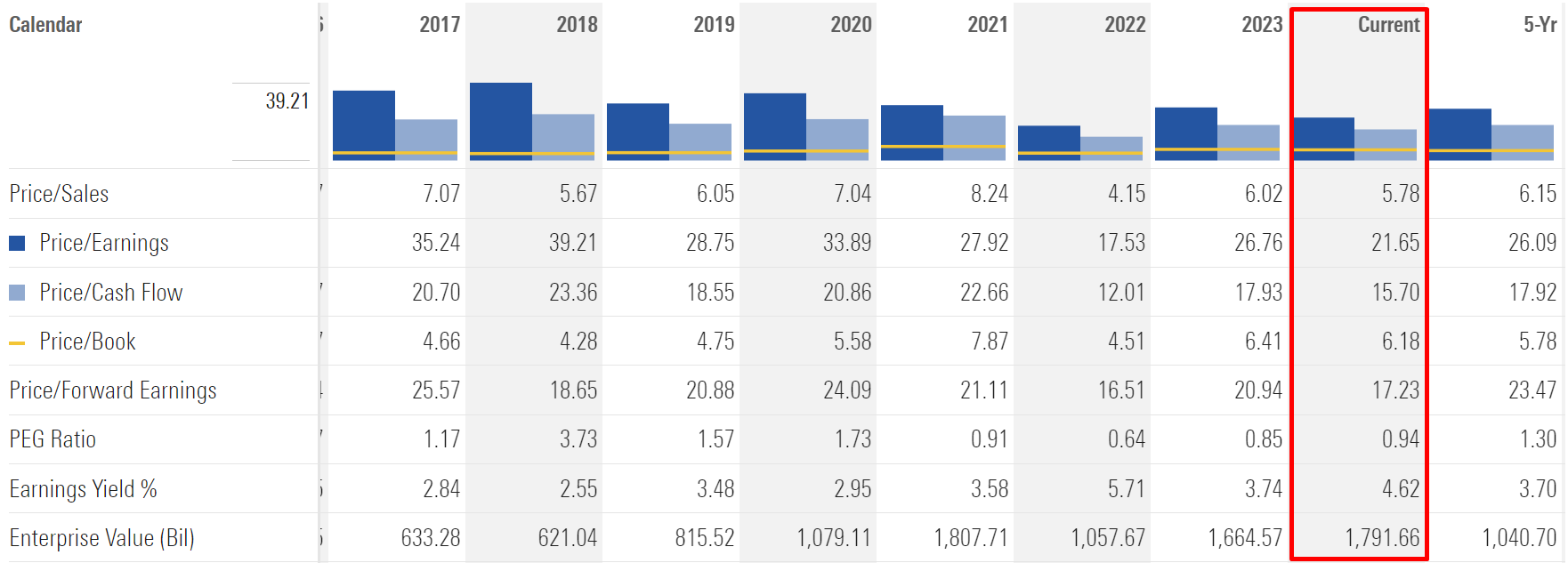

💲Current Valuation

GOOGL is currently trading at lower multiples compared to its 5-year averages across most metrics. The P/E ratio (21.65 vs 26.09), P/S ratio (5.78 vs 6.15), P/CF ratio (15.70 vs 17.92), and P/Forward Earnings (17.23 vs 23.47) are all below their 5-year averages. The PEG ratio (0.94 vs 1.30) suggests better value relative to growth, while the higher Earnings Yield (4.62% vs 3.70%) indicates improved earnings relative to price. Overall, these metrics suggest the stock may be more attractively valued now than its 5-year historical average.

The current PEG ratio is almost at the lowest value for the last ten years:

🏷️ Fair Price

➡️ Updated fair price valuation: https://longtermpick.com/p/updated-valuations-nov-24

The Long-Term Pick's Fair Price (Base Case) for GOOGL is $293. The current price of $150 is lower by 48.53%. Yes, it's an insane estimation but let me explain everything below.

Fair-to-Current Price (%): 48.53%

Current Price/Fair Price: 0.51

I used:

Discount Rate: 12% (S&P 500 Next 5-Yr Growth Estimates is 11.90%)

Margin of Safety: 30%

Years: 10

Future EPS Growth Rate: 17.5%

Future Dividend and Buyback Yield: 2%

Total Future Annual Growth Rate: 17.5 + 2 = 19.5%

For the Base Case, the Future Expit P/E is 20. 5-Yr average P/E ratio is 26, the lowest P/E during the last ten years was 17. Honestly, I expect a potential economic drawdown in the next 1-2 years, but in the long term, I expect GOOGL to rise at high levels. So, for the Base Case, I decided to take my estimated total future annual growth rate which is 19.5% (rounded to 20) -- it's lower than the 5-year average P/E ratio of 26.

3-Year Average Share Buyback Ratio: 2.6. It's even less than my 2%. Also, it's worth noting that GOOGL has started paying dividends recently.

So, as you can see, as much as I didn't try to minimise the figures, in the Base Case scenario the stock still looks very undervalued. To confirm my assumptions, I did a DCF valuation and the Bull Case showed $237.

☑️ Checklist

Profitability:

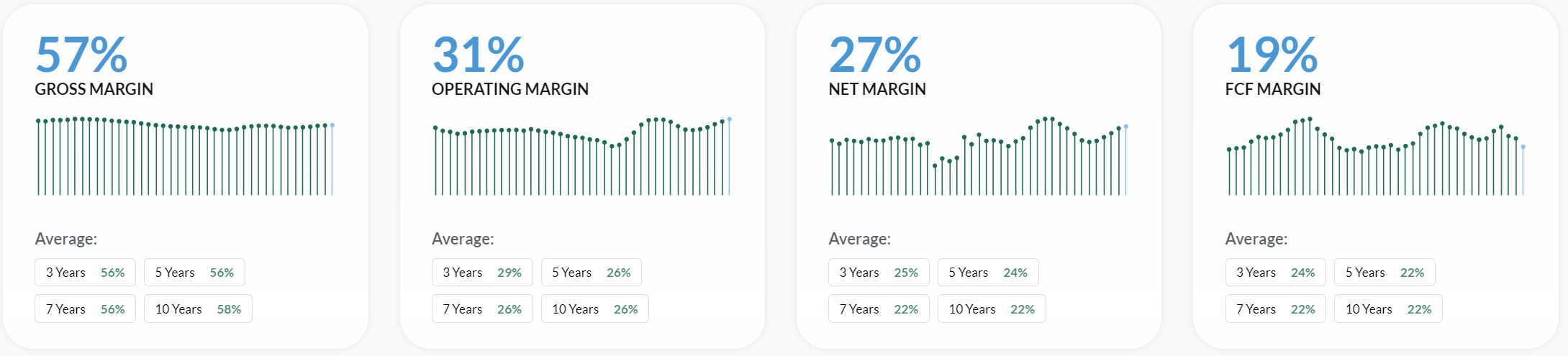

✅ Gross margin at least 40%: 57%

✅ Net margin at least 10%: 27%

✅ Management (ROIC, ROCE, ROE, ROA): Yes (All above 20%)

✅ Piotroski F-Score: 8 of 9 (Not passed: Higher Current Ratio YoY)

❌ Revenue surprises last 10 years: No (Missed: 2019 -- Based on TradingView's data)

❌ EPS surprises last 10 years: No (Missed: 2022 -- Based on TradingView's data)

❌ EPS growth YoY 10 years: No (Missed: 2017, 2022)

Valuation and Advantage:

✅ Valuation below its 5-Yr average: Yes

✅ Does it have a moat: Yes (wide)

Shares:

✅ Insider ownership at least 5%: Yes (10.38%)

✅ Less shares outstanding YoY: Yes

❌ Insider buys last six months: No (Worth noting that Sundar Pichai sold shares actively during August and September)

Price:

✅ 1-year stock price forecast: +30%

✅ Next 5-Yr CAGR is above S&P 500: Yes (20.50% vs 11.90%)

✅ DCF Value: $166.73 (Undervalued by 9%; 10 years, discount rate: 10%, terminal growth: 3%, equity model: FCFE)

✅ Short Interest below 5%: Yes (1.18%)

This is not a financial or investing recommendation. It is solely for educational purposes.