Updated Valuations: IDXX, GOOGL, MRK, NVO, and MOH

In early February, some companies covered by Long-Term Pick (updated page) released their quarterly and yearly earnings reports. It's time to update their fair price valuations and review the latest reports. Some explanations regarding screenshots with fair price estimates:

I marked cells that I updated as grey (after the latest earning reports).

Fair-to-Current Price and Current Price/Fair Price: 🟢 undervalued, 🔵 fairly valued (+/- 5% is “fairly”), 🟡 overvalued.

Additionally, I included updated current valuations alongside their 5-year averages for easy comparison. I also added average future price estimates from other analysts to compare with my Base Fair Price Estimates and past quarterly EPS surprises vs. actuals for the latest 10-year period.

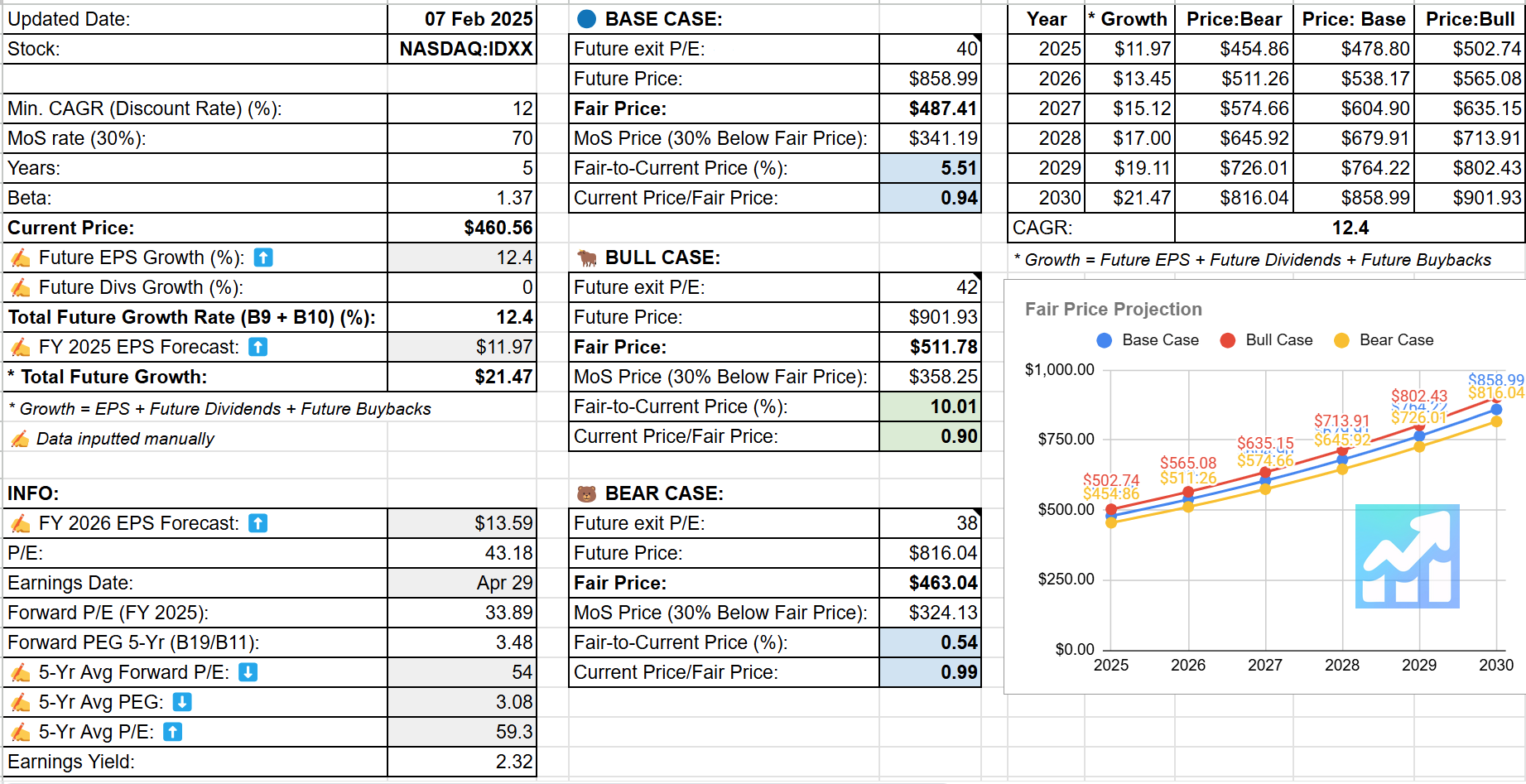

🔵 IDEXX (IDXX)

📝 Analyst Notes

My previous fair price was $401. After changes, the new fair price has become $487 (higher). I’ve increased the 3-year average EPS growth rate.

IDEXX remains optimistic about 2025 with projected revenue growth between $4.055 billion and $4.170 billion, supported by innovations in veterinary diagnostics.

Management highlighted IDEXX Cancer Dx and IDEXX inVue Dx as key drivers of growth, with 4,500 inVue placements planned for 2025 and a 5-year target of 20,000 placements.

🏷️ Updated Valuation

Latest earnings report (Feb 3, 2025):

👍 Positive Points

IDEXX Laboratories reported a 6% organic revenue growth in Q4 2024, with CAG Diagnostic recurring revenues increasing by 7% organically.

The company achieved a full-year EPS of $10.67 per share, marking a 12% increase on a comparable basis.

IDEXX's international CAG Diagnostic recurring revenue growth was strong at 12% in Q4, supported by net price gains and improved volume growth.

The company successfully launched IDEXX inVue Dx, a new cellular analyzer, with nearly 1,600 preorders globally by the end of Q4.

IDEXX's software business saw double-digit growth in cloud-native PIMS placements, enhancing clinic efficiency and fostering deeper connections with practices and pet owners.

👎 Negative Points

US same-store clinical visit levels declined nearly 3% in Q4 and 2% for the full year in 2024, posing a constraint on IDEXX's growth.

Rapid assay revenue was flat on an organic basis in Q4, constrained by pressure on US wellness visits.

Operating expenses increased by 10% as reported in Q4, reflecting higher R&D spending.

Foreign exchange had a negative impact on Q4 EPS, contributing to a $0.03 per share headwind.

The company faces a 2% negative impact on full-year 2025 revenue growth due to foreign exchange rates.

💲Current Valuation

📈 Price Forecast

↗️ Sales and EPS Forecast

⏺️ EPS Actual vs. Estimate

📈 5Y Performance

🟢 Alphabet (GOOGL)

📝 Analyst Notes

My previous fair price was $220. After changes, the new fair price has become $218 (lower). The 3-year average EPS growth has lowered, and I’ve increased future exit P/E for the Base and Bull Cases a bit.

Robust growth in Search, YouTube, and Cloud. $75 billion in planned CapEx for 2025. The company is doubling down on AI and cloud infrastructure, reflecting confidence in sustained demand.

🏷️ Updated Valuation

Latest earnings report (Feb 4, 2025):

👍 Positive Points

Alphabet reported strong revenue growth, with a 12% increase in Q4 2024, driven by robust performance in Google Search and Cloud.

The company achieved a significant milestone with its Cloud and YouTube businesses, reaching a combined annual revenue run rate of $110 billion.

AI advancements, including the launch of Gemini 2.0, have enhanced product capabilities and driven increased consumer and developer engagement.

Google Cloud saw a 30% revenue increase, with strong demand for AI-powered solutions and strategic deals over $1 billion.

YouTube continues to lead in streaming watch time in the US, with significant growth in ad revenue, particularly from election-related content.

👎 Negative Points

Network advertising revenue declined by 4%, impacting overall advertising growth.

The company faces capacity constraints in its Cloud segment, limiting potential revenue growth despite high demand.

Foreign exchange rates and the absence of a leap year are expected to negatively impact Q1 2025 revenue.

Increased capital expenditure, projected at $75 billion for 2025, may pressure profitability due to higher depreciation costs.

Alphabet anticipates challenges in maintaining growth in the financial services vertical, particularly in the insurance segment.

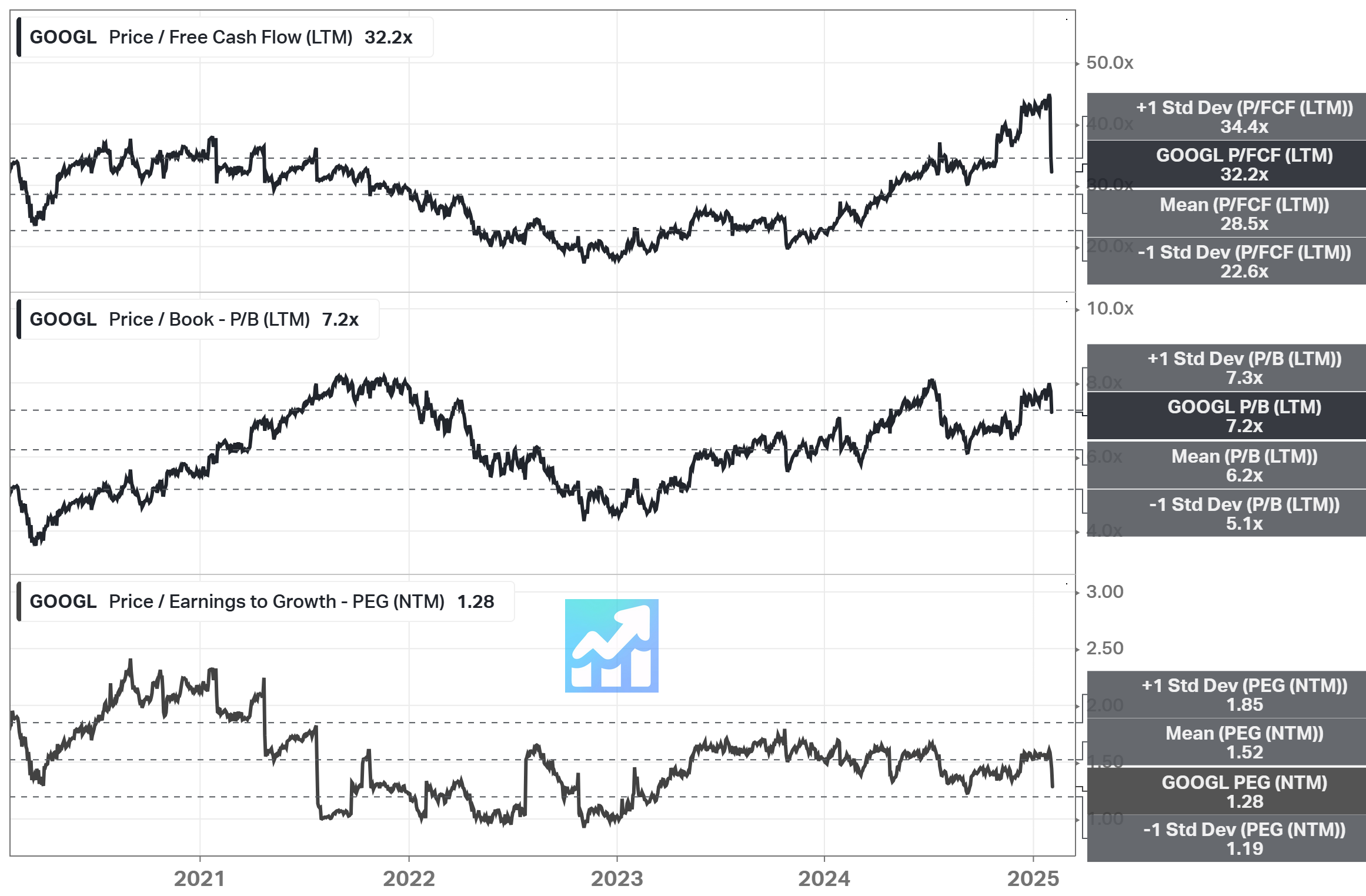

💲Current Valuation

📈 Price Forecast

↗️ Sales and EPS Forecast

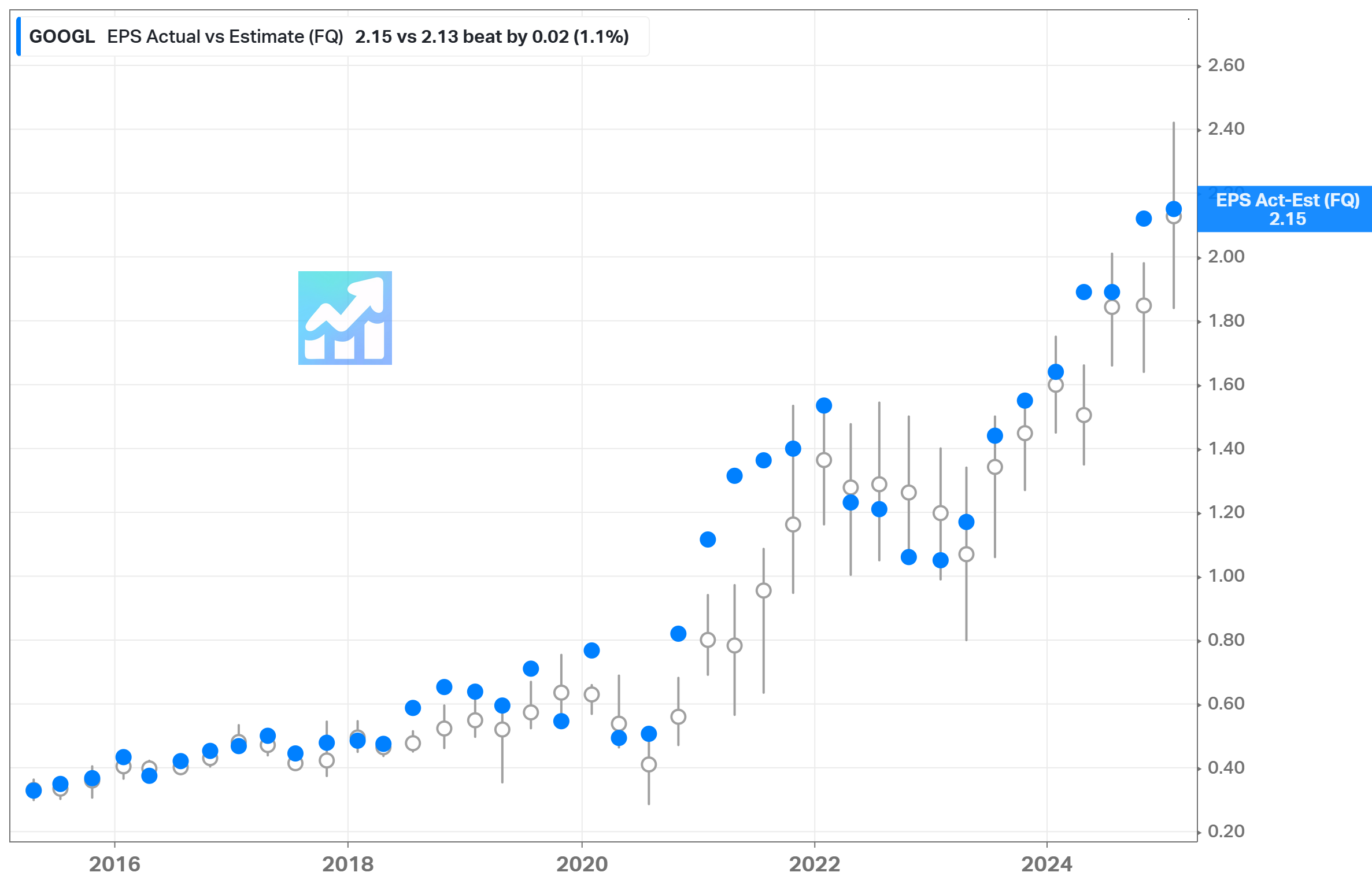

⏺️ EPS Actual vs. Estimate

📈 5Y Performance

🟢 Merck & Co. (MRK)

📝 Analyst Notes

My previous fair price was $148. After changes, the new fair price has become $188 (higher). Yes, the fair price is far above the current price, but the reason is that the 3-year average EPS growth has increased compared to the previous values. I’ve decreased future exit P/E for all cases (Base, Bull, and Bear).

Why is the price down? The company's 2025 guidance fell short of analysts' expectations, with projected revenue between $64.1 billion and $65.6 billion, which is below the anticipated $67.31 billion. Additionally, Merck paused shipments of its HPV vaccine Gardasil to China through mid-2025, impacting its revenue outlook.

🏷️ Updated Valuation

Latest earnings report (Feb 4, 2025):

👍 Positive Points

Merck achieved strong growth in 2024, driven by demand for its innovative portfolio, including KEYTRUDA and the successful launch of WINREVAIR.

The company reached nearly 0.5 billion people with its medicines and vaccines in 2024, showcasing its global impact.

MRK is making significant progress in its pipeline, with 20 potential new growth drivers, many with blockbuster potential.

The Animal Health business delivered strong performance with a 13% sales growth.

Merck has a robust late-phase pipeline with promising developments in oncology, cardiometabolic, and infectious diseases.

👎 Negative Points

GARDASIL sales decreased by 18% due to lower demand in China, leading to elevated inventory levels.

MRK decided to temporarily pause GARDASIL shipments to China, impacting short-term revenue.

The company faces challenges in the Chinese market for GARDASIL due to increased pressure on discretionary consumer spending.

There is uncertainty regarding the timing of economic recovery in China, affecting long-term sales projections for GARDASIL.

The Medicare Part D redesign is expected to negatively impact sales by approximately $400 million, affecting products like WINREVAIR and small molecule oncology products.

💲Current Valuation

📈 Price Forecast

↗️ Sales and EPS Forecast

⏺️ EPS Actual vs. Estimate

📈 5Y Performance

🟢 Novo Nordisk (NVO)

📝 Analyst Notes

My previous fair price was $125. After changes, the new fair price has become $132 (higher). I’ve lowered future exit P/E for all the cases.

Why is the price down? Recently, the company faced a significant drop after disappointing results from its new weight-loss drug, CagriSema. The trial showed less weight loss than expected. Additionally, Novo Nordisk's third-quarter sales were lower than analysts' expectations despite growth in obesity and diabetes treatments. Regarding Q4, see my comments below.

🏷️ Updated Valuation

Latest earnings report (Feb 5, 2025):

👍 Positive Points

Novo Nordisk reported a strong 26% sales growth and 26% operating profit growth for 2024.

The company expanded its patient reach, now serving over 45 million patients with diabetes and obesity treatments.

Obesity care sales increased by 57%, driven by significant growth in both North America and international operations.

NVO maintained its leadership in the GLP-1 market, serving nearly two-thirds of all patients on GLP-1 treatments.

The company completed the acquisition of Catalent sites, enhancing its global fill and finish footprint, which will support future market supply expansion.

👎 Negative Points

Total carbon emissions rose by 23% due to increased production volumes and capital expenditure investments.

R&D costs increased by 48%, reflecting higher clinical trial activity and impairment losses related to intangible assets.

The net financial items showed a net loss of DKK1.1 billion, primarily due to losses on non-hedged currencies.

The effective tax rate increased to 20.6% in 2024, compared to 20.1% in 2023.

Free cash flow was negative at minus DKK14.7 billion, impacted by significant capital expenditures and the Catalent site acquisition.

💲Current Valuation

📈 Price Forecast

↗️ Sales and EPS Forecast

⏺️ EPS Actual vs. Estimate

📈 5Y Performance

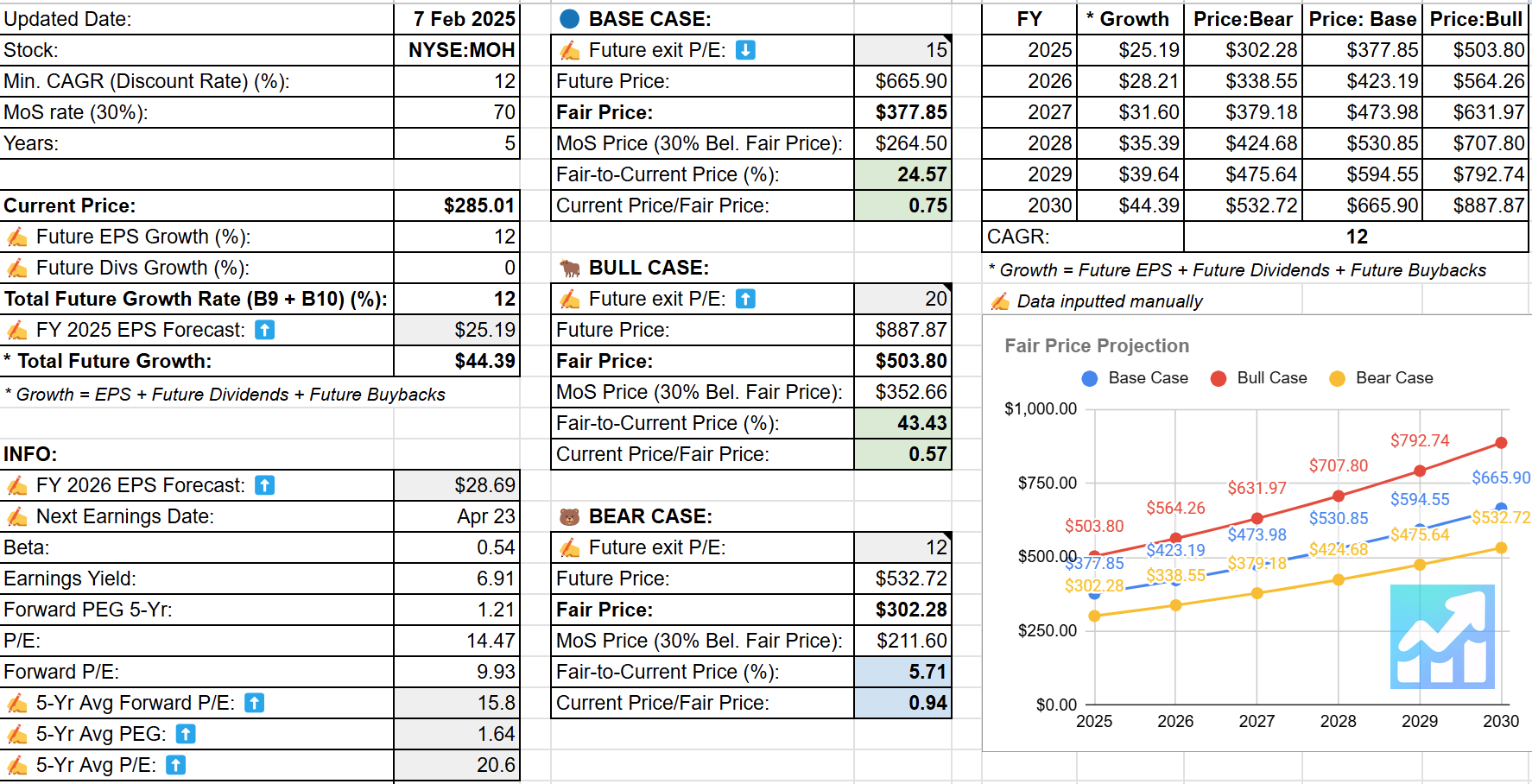

🟢 Molina Healthcare (MOH)

📝 Analyst Notes

My previous fair price was $387. After changes, the new fair price has become $378 (lower). The value is a bit lower since I’ve lowered future exit P/E for the Base Case.

Why is the price down? The company reported mixed fourth-quarter results, beating revenue expectations but missing earnings estimates due to higher medical spending in Medicaid. Additionally, Molina's 2025 earnings guidance was lower than anticipated, partly because of implementation costs from new Medicaid and Medicare contracts. Despite these challenges, the company remains optimistic about future growth potential from these contract wins.

🏷️ Updated Valuation

Latest earnings report (Feb 5, 2025):

👍 Positive Points

Full year 2024 premium revenue increased by 19% year-over-year to $38.6 billion.

GAAP net income per diluted share rose by 9% year-over-year to $20.42.

Adjusted net income per diluted share increased by 8% year-over-year to $22.65.

2025 guidance projects premium revenue of approximately $42 billion, with adjusted earnings of at least $24.50 per diluted share.

Strong operating performance in the Marketplace segment with a Medical Care Ratio (MCR) of 75.4%.

👎 Negative Points

Operating cash flow decreased to $644 million in 2024 from $1,662 million in 2023.

Cash and investments at the parent company dropped to $445 million as of December 31, 2024, from $742 million the previous year.

Medical Care Ratio (MCR) for Medicaid was higher than long-term expectations due to redetermination-related acuity shifts.

💲Current Valuation

📈 Price Forecast

↗️ Sales and EPS Forecast

⏺️ EPS Actual vs. Estimate

📈 5Y Performance

🟣 Uber Technologies (UBER)

The project's patrons will also receive an UBER update. Additionally, the .XLS file containing all updated fair price valuations for easier access.

Please note that some covered companies are available only to patrons.

This is not a financial or investing recommendation. It is solely for educational purposes.