Molina Healthcare: Focus On Low-Income Populations

Molina Healthcare has a strong position in government-sponsored healthcare with a focus on Medicaid and Medicare.

Changelog:

Feb 8, 2025: Updated fair price valuation: $378.

Jan 24, 2024: Overview: New Florida Medicaid Contract, Wisconsin Contract Award, Expansion into Dual-Eligible Market, Quality Improvement Initiative, and Senior Notes Offering.

Molina Healthcare (MOH) stands out as a specialized player in the managed healthcare space, focused primarily on underserved, low-income populations through government-sponsored programs. With a clear focus on Medicaid and Medicare, Molina has established a unique position that protects it from the intense competition from more generalized healthcare providers. Under the leadership of CEO Joseph Zubretsky, Molina has pursued strategic acquisitions, streamlined operations, and improved financial efficiency, setting the stage for steady growth in a critical and stable sector of the healthcare industry.

Previous publication:

Content:

💡 Investment Thesis

🧐 Company Overview

🏰 Economic Moat

🚀 Business Strategy

✅ Advantages

❌ Disadvantages

🏛️ Capital Allocation

🥇 Competitors

⏮️ Past

📶 Future

💲Current Valuation

🏷️ Fair Price

☑️ Checklist

✍️ Due Diligence

💡 Investment Thesis

Molina stands out as a specialized player in the managed healthcare space, focused primarily on underserved, low-income populations through government-sponsored programs. With a clear focus on Medicaid and Medicare, Molina has established a unique position that shields it from the intense competition from more generalized healthcare providers. Under the leadership of CEO Joseph Zubretsky, Molina has pursued strategic acquisitions, streamlined operations, and improved financial efficiency, setting the stage for steady growth in a critical and stable sector of the healthcare industry.

The company’s strong revenue growth, strong balance sheet, and ability to manage costs effectively make it attractive in a highly regulated sector. As government healthcare programs continue to expand, especially for low-income groups, Molina is well-positioned to benefit from this ongoing trend, despite facing pressures from competitors and policy changes. Molina is an attractive option for investors seeking exposure to the healthcare sector with a more focused and socially impactful perspective.

⬇️ Download Quick Analysis in PDF/PNG + Market Trends (Recommended)

🧐 Company Overview

Incorporated: 1980

Sector: Healthcare

Industry: Healthcare Plans

Stock Style: Mid Core

Market Cap: $19.79 Bil

Total Number of Employees: 18,000

Website: https://www.molinahealthcare.com/

Earnings Date: Feb 5, 2025 - Feb 10, 2025Molina Healthcare was founded in 1980 and is headquartered in Long Beach, California. The company primarily focuses on providing healthcare plans for low-income families and individuals through government-sponsored programs like Medicaid, Medicare, and the Marketplace. By specializing in these public programs, Molina serves people who might not have access to traditional private insurance, helping to bridge gaps in healthcare coverage for millions of Americans. Over the years, Molina has become a major player in the managed care industry and is now one of the FORTUNE 500 companies.

Molina’s business is split into three main segments. Medicaid is its largest segment, bringing in around 80.9% of its total revenue. This program supports low-income people by offering affordable healthcare options. Medicare serves seniors and people with disabilities, making up 12.8% of Molina's revenue. The Marketplace segment offers individual health insurance plans, providing around 6.3% of its revenue. Altogether, these segments support Molina’s mission of making healthcare accessible to underserved populations.

As of 2023, Molina Healthcare served about 5 million members, but the company has faced challenges in maintaining steady membership, with a slight 5% decrease compared to the previous year. Despite this, Molina has continued to expand its market presence, achieving steady revenue growth over the past several years. The company's third-quarter results in 2024 show ongoing improvement, with revenue growing due to increased premiums and recent acquisitions. Molina’s ability to adapt to changes in the healthcare industry and expand its membership base has kept it competitive in the managed care market.

Under the leadership of CEO Joseph Zubretsky, who joined Molina in 2017, the company has pursued a strategy focused on growth, efficiency, and cost control. Zubretsky has a strong background in the healthcare sector. His leadership has led to better financial performance, driven by strategic acquisitions and effective cost management. Under Zubretsky’s direction, Molina has successfully reduced its general and administrative expenses, helping the company remain financially healthy and competitive.

🏰 Economic Moat

The company has a narrow economic moat. It mostly comes from its longstanding relationships with government health programs and its focus on Medicaid and Medicare. By specializing in these programs, Molina has built a reputation for serving low-income populations, which creates a unique position in the healthcare market.

One of the key strengths of Molina's moat is its established contracts with state and federal governments. These contracts are crucial for Molina’s business, as they allow it to operate Medicaid and Medicare services in multiple states. Unlike private insurance providers that depend on a mix of government and private clients, Molina focuses primarily on government contracts. This focus can be an advantage, as these contracts often have long-term commitments, which bring a level of stability to Molina’s revenue. However, this dependence also means Molina’s revenue is vulnerable to government policy changes, such as adjustments in Medicaid funding or shifting eligibility requirements.

By focusing on low-income populations, Molina has positioned itself in a less competitive market niche, where fewer healthcare companies are active. Many larger competitors, like UnitedHealth Group and CVS Health, focus on a wider range of insurance and healthcare services. Molina, on the other hand, benefits from being a specialist in government-sponsored programs, which helps to differentiate it from larger, more diversified companies.

You’re reading this analysis for free. Consider supporting the project and gaining access to exclusive investment ideas that are not publicly available. On 30 October, I wrote a publication titled “Small-Cap Fintech Hidden Gem“—that was Dave (NASDAQ: DAVE). After the latest earnings report, the stock rose by 38.71%.

🚀 Business Strategy

Their strategy is to grow by expanding its coverage and improving operational efficiency. The company achieves this by acquiring other healthcare providers and winning new contracts. Recent acquisitions include My Choice Wisconsin and Bright Healthcare’s California Medicare business. By expanding its services, Molina can increase its membership and geographical reach.

Additionally, Molina focuses on cutting costs through an ongoing restructuring plan. This plan has helped Molina lower its general and administrative (G&A) costs, contributing to better financial performance. The company aims to balance growth and cost control, helping it compete with larger companies without overspending.

Core business segments:

Medicaid: This is the largest segment, where the company provides health plans to low-income individuals and families who qualify for Medicaid. Molina operates in various states, managing the administrative aspects of the program while ensuring that members receive access to necessary healthcare services.

Medicare: Molina also offers Medicare Advantage plans to eligible seniors. This segment focuses on providing health insurance to individuals aged 65 and older, including various health services that may not be covered under traditional Medicare.

To Read: Healthcare 2030

Marketplace Plans: This segment includes plans that are offered through Health Insurance Marketplaces established under the Affordable Care Act (ACA). Molina provides health insurance options to individuals and families who do not qualify for Medicaid or Medicare but still need affordable healthcare solutions.

Long-Term Care and Specialty Services: The company offers additional services aimed at individuals with special needs or chronic conditions. This can include care coordination, behavioral health services, and other specialized programs designed to support members with complex health requirements.

✅ Advantages

Strong Revenue Growth: Molina has shown consistent revenue growth, largely due to rising premiums and new Medicaid contracts. For example, in the first nine months of 2024, revenue grew by 20.5% compared to the same period last year, driven by new contracts and acquisitions.

Solid Financial Position: Molina has a strong balance sheet, with $4.7 billion in cash compared to $2.3 billion in long-term debt as of September 2024. This financial flexibility allows Molina to pursue acquisitions and handle unexpected expenses without relying heavily on borrowing.

High Return on Equity: Molina’s ROE is 27.9%, higher than the industry average of 23.9%. This means the company effectively uses its shareholders’ money to generate profits.

❌ Disadvantages

High Medical Care Costs: Their medical care ratio (MCR), the percentage of premium revenue spent on medical care, is high. The MCR is projected to be 88.4% for 2024, up from 88.1% in 2023. This increase means that Molina has less premium revenue left after paying medical claims, impacting profitability.

Dependence on Government Programs: The company relies heavily on Medicaid and Medicare, both of which are funded by government programs. This dependency makes the company vulnerable to changes in government policy, especially if pandemic-related subsidies decrease over time.

🏛️ Capital Allocation

Molina actively invests in growth through acquisitions to expand its reach and increase membership. In addition to my previously mentioned acquisitions, the company recently acquired ConnectiCare for $350 million, which strengthens Molina’s presence in Connecticut. Through acquisitions, Molina diversifies its revenue and extends its coverage area, allowing it to grow its customer base.

Their capital allocation focuses on reinvestment into the business rather than shareholder dividends or buybacks (but it does buybacks). With strong cash flow, Molina has the flexibility to make acquisitions without accumulating too much debt.

🥇 Competitors

Molina Healthcare competes directly with several large healthcare providers in the managed care industry.

UnitedHealth Group (UNH): UnitedHealth Group is the largest player in the managed care industry. It has a broad network and a well-diversified business model that includes both healthcare services and insurance. Compared to Molina, UnitedHealth’s size and resources allow it to offer a wider range of services and better withstand industry changes. Molina’s focus on government programs makes it more specialized, but also more limited.

CVS Health (CVS): CVS Health operates in both retail and healthcare services. Its acquisition of Aetna expanded its healthcare services, giving CVS a strong presence in insurance. Molina’s narrower focus on Medicaid and Medicare gives it an edge in specific low-income markets but limits its reach compared to CVS, which can offer a variety of services and products across a larger population.

Centene Corporation (CNC): One of Molina’s closest competitors in the Medicaid and government health insurance markets. Both companies focus on low-income members through Medicaid and Medicare, but Centene has a larger network and operates in more states. Centene’s scale and resources make it a strong competitor, but Molina’s focus on cost efficiency and targeted acquisitions helps it compete effectively within its chosen markets.

⏮️ Past

The company reported third-quarter adjusted earnings per share of $6.01 and reaffirmed 2024 premium revenue guidance at $38 billion, with EPS projected to reach at least $23.50. Their MCR rose to 90.5%, primarily due to higher medical costs, but is expected to improve to 89% in the fourth quarter. Additionally, favorable rate updates are anticipated to offset costs, contributing to a full-year MCR projection of 90%. The company’s embedded earnings per share are now noted at $5.75, underpinning a stable path for long-term growth.

Worth noting that during the 5-, 10, and 15-year periods (CAGR), MOH overperformed the industry (Healthcare Plans) and the S&P 500.

📶 Future

Based on the Grand View Research report, the U.S. individual health insurance market size is expected to expand at a CAGR of 6.08% by 2030. An increase in insurer participation and new product offerings are among the major factors leading to the rising demand for individual health insurance in the U.S.

Based on short-term price targets offered by 15 analysts, the average price target for Molina comes to $370.27. The average price target represents an increase of 9.65%.

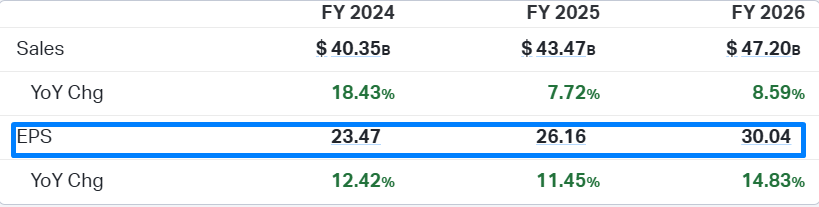

The company's sales are expected to increase each year, rising from $40.37 billion in FY 2024 to $47.18 billion in FY 2026. Similarly, the company's EPS is forecast to grow from $23.47 in FY 2024 to $30.10 in FY 2026, with the YoY growth rate in EPS expected to be 12.42% in FY 2024, 11.59% in FY 2025, and 14.93% in FY 2026, indicating a steady increase in the company's sales and earnings over the next 3 fiscal years.

💲Current Valuation

The current valuation indicates that the company’s stock price is lower than its 5-year average. However, it's important to note that the PEG ratio is high compared to previous years. The Earnings Yield ratio is high, which I find particularly appealing since the US 10-year Treasury Bond Note Yield is 4.3%.

🏷️ Fair Price

The Long-Term Pick's Fair Price (Base Case) for MOH is $386.90. The current price of $329.65 is lower by 14.80%.

Fair-to-Current Price (%): 14.80%

Current Price/Fair Price: 0.85

I used:

Discount Rate: 12% (S&P 500 Next 5-Yr Growth Estimates is 11.05%)

Margin of Safety: 30%

Years: 5

Future EPS Growth Rate: 12% (Based on Yahoo Finance and Koyfin)

Future Dividend and Buyback Yield: 1% (Buybacks only)

Total Future Annual Growth Rate: 12 + 1 = 13%

I want to add a couple of moments to my estimate. First, MOH's past performance (CAGR) for 5, 10, and 15-year periods is higher than my "modest" 13% growth rate (see the Past section) - I expect even higher returns in the next 5 years. Second, if you look at my projected growth ($23.13, $26.14, ..., $42.16), you will see that the values are very similar to other analysts estimates:

☑️ Checklist

Profitability:

❌ Gross margin at least 40%: 16% (But it’s OK for the industry)

❌ Net margin at least 10%: 3% (But it’s OK for the industry)

✅ Management (ROIC, ROCE, ROE, ROA): Yes (All above 10%, except ROA)

✅ Piotroski F-Score: 7 of 9 (Not passed: CFROA > ROA, Higher Gross Margin YoY)

❌ Revenue surprises in last 7 years: No (2019 and 2020; Based on TradingView's data)

❌ EPS surprises in last 7 years: No (2017, 2019, and 2020; Based on TradingView's data)

❌ EPS growth YoY 7 years in a row: No (2020; Based on TradingView's data)

Valuation and Advantage:

✅ Valuation below its 5-yr average: Yes

✅ Does it have a moat: Yes (narrow)

Shares:

❌ Insider ownership at least 5%: No (1.13%)

✅ Less shares outstanding YoY: Yes

❌ Insider buys last six months: No

Price:

❌ 1-year stock price forecast is above 10%: +9.65%

✅ Next 5-Yr Growth Estimates (CAGR) is above S&P 500: Yes (12.15% vs 11.05%; Based on Yahoo Finance)

✅ DCF Value: $432.12 (Undervalued by 22%; 10 years, discount rate: 10%, terminal growth: 3%, equity model: FCFE)

✅ Short Interest below 5%: Yes (2.05%)

✍️ Due Diligence

Profitability (8 of 10):

✅ Positive Gross Profit: 6.3B USD

✅ Positive Operating Income: 1.6B USD

✅ Positive Net Income: 1.1B USD

✅ Positive Free Cash Flow: 94m USD

✅ Positive 1-Year Revenue Growth: 18%

✅ Positive 3-Year Revenue Growth: 15%

✅ Positive Revenue Growth Forecast: 12%

✅ Exceptional ROE: 26%

✅ Exceptional 3-Year Average ROE: 28%

✅ ROE is Increasing: 25% > 26%

✅ Exceptional ROIC: 26%

✅ Exceptional 3-Year Average ROIC: 27%

❌ Declining ROIC: 27% > 26%

Solvency (8.5 of 10):

✅ Short-Term Solvency (short-term assets (13B USD) exceed its short-term liabilties (8B USD))

✅ Long-Term Solvency (long-term assets (16B USD) exceed its long-term liabilties (11B USD))

✅ Negative Net Debt: -6.7B USD (has more cash and short-term investments (9B USD) than debt (3B USD))

✅ Low D/E: 0.53

✅ High Altman Z-Score: 3.93

This is not a financial or investing recommendation. It is solely for educational purposes.

❤️ Thanks for being Long-Term Pick’s reader!

🤝 Feel free to provide your feedback.

Thanks for the analysis!