Novo Nordisk: Diabetes Care Leader Below Fair Price

Novo Nordisk remains a dominant player in the global healthcare market driven by its innovative therapies and strategic focus on diabetes and obesity care.

Changelog:

Feb 8, 2025: Updated fair price valuation: $132.

Jan 24, 2025: Overview: FDA Price Negotiations for GLP-1 Drugs, Semaglutide 7.2 mg Trial Success, Collaboration with Valo Health, Acquisition of Manufacturing Sites, Share Repurchase Program, Disappointing CagriSema Trial Results, UBS Stock Upgrade, and Market Leadership in Weight-Loss Drugs.

Novo Nordisk (NVO) is a well-known company in the global healthcare field, focusing mainly on diabetes care, obesity treatment, and rare diseases. With a strong emphasis on new and effective therapies, Novo Nordisk has established a unique position that helps it succeed despite strong competition from other pharmaceutical companies. Under the leadership of CEO Lars Fruergaard Jørgensen, the company has made important changes, expanded its product range, and improved its operations, setting the stage for continued growth in a vital part of the healthcare industry.

Content:

💡 Investment Thesis

🤔 Why is Novo Nordisk down this year?

🧐 Company Overview

🏰 Economic Moat

🚀 Business Strategy

🏛️ Capital Allocation

✅ Advantages

❌ Disadvantages

🥇 Competitors

⏮️ Past

📶 Future

💲Current Valuation

🏷️ Fair Price

☑️ Checklist

✍️ Due Diligence

💡 Investment Thesis

Novo Nordisk is well-positioned in the market, driven by innovative products like Ozempic and Wegovy, which have transformed treatment options for diabetes and obesity. Under CEO Lars Fruergaard Jørgensen, the company has focused on expanding its product offerings and improving operational efficiencies, where I see a way for continued growth.

NVO has shown consistent revenue growth, reporting DKK 204.7 billion in revenue for the first nine months of 2024, a 23% increase YoY. This growth is supported by a strong pipeline of new therapies and a commitment to R&D. Novo Nordisk leads the GLP-1 market with a 34% global market share in diabetes care, further strengthened by the recent launch of Wegovy for obesity management.

Financial health is strong - impressive profit margins and a disciplined capital allocation strategy that prioritizes shareholder returns through dividends and share buybacks. With low debt and a solid balance sheet, the company is poised to handle competitive challenges effectively. Strong earnings growth potential and a solid market position.

The stock is currently trading at attractive valuations compared to historical averages, making it an appealing option for investors seeking stable growth in the healthcare sector. The current PEG ratio is the lowest for the last 10 years.

➡️ Novo Nordisk: Quick Analysis, Market Overview, and Comparison With Competitors (Free)

🤔 Why is Novo Nordisk down this year?

In my view, Novo Nordisk's stock has gone down this year for several reasons. One major issue is that the company’s new obesity drug, monlunabant, did not perform well in clinical trials, showing less weight loss than expected. This news disappointed investors and caused the stock price to drop.

Additionally, while Novo Nordisk's sales increased by 21% compared to last year, they were still lower than what analysts predicted. There is also growing criticism about high drug prices from U.S. lawmakers, which adds to the negative sentiment around the company. With more competition in the obesity treatment market, investors are concerned about Novo Nordisk's future growth.

🧐 Company Overview

Incorporated: 1923

Sector: Healthcare

Industry: Drug Manufacturers

Stock Style: Large Growth

Market Cap: $444.27 Bil

Total Number of Employees: 72,000

Website: https://www.novonordisk.com/

Earnings Date: Feb 5, 2025Novo Nordisk is a leading Danish healthcare company that specializes in diabetes care, obesity treatment, and rare disease management. Based in Bagsværd, Denmark. The company has built a strong reputation over many years for its expertise in insulin and glucagon-like peptide-1 (GLP-1) receptor agonists. Novo Nordisk operates through two main segments: Diabetes and Obesity Care, and Rare Diseases. This focus has made it a leader in the diabetes care market, holding a 34% share of the global market. Its best-known products include Ozempic, Wegovy, and Rybelsus, along with essential insulin therapies like Levemir and Tresiba.

The company has shown impressive growth, with revenues reaching DKK 204.7 billion in the first nine months of 2024. This represents a 23% increase compared to the previous year.

Under CEO Lars Fruergaard Jørgensen (LinkedIn), who has led the company since January 2017, Novo Nordisk has continued to grow. Jørgensen has worked at Novo Nordisk since 1991, giving him deep knowledge of the healthcare industry and the company's strengths. His focus on innovation and patient-centered solutions has been key to advancing Novo Nordisk’s mission to improve lives through effective diabetes care.

Recently, Jørgensen received a 13% raise for his performance in 2023, bringing his total compensation to about 68.2 million DKK (around $9.9 million). This increase reflects his successful leadership during a time of high demand for Novo's GLP-1 treatments.

🏰 Economic Moat

Novo Nordisk has a strong wide economic moat due to its innovative products and broad global reach. The company leads in the GLP-1 market with a 54% share in diabetes-related therapies as of 2023. Its ongoing R&D efforts help ensure that it continues to create new products while extending patent protections for existing ones. Efficient manufacturing processes also support its profitability. Although there is significant pricing pressure in key markets like the U.S. and China, Novo Nordisk benefits from its size and expertise in producing biologics.

The company's commitment to research is evident in its significant investments aimed at developing new therapies for chronic conditions beyond diabetes, including obesity and heart diseases. Recent clinical trials have shown promising results for semaglutide treatments, strengthening Novo Nordisk's position as an industry leader. This focus on innovation not only enhances its product offerings but also creates high barriers for potential competitors trying to enter the market.

Read Also:

🚀 Business Strategy

Novo Nordisk’s business strategy is based on innovation in diabetes and obesity care. The company has successfully shifted its revenue from traditional insulin therapies to GLP-1 products, which now make up about 70% of its sales. Recent launches like Wegovy for obesity management and Rybelsus for oral diabetes treatment show its dedication to addressing chronic diseases with advanced therapies that meet patient needs.

Additionally, Novo Nordisk is expanding GLP-1 applications beyond diabetes into areas such as obesity, heart disease, metabolic-associated fatty liver disease (MASH), and even Alzheimer’s disease. Strategic acquisitions are also important; recent purchases like Inversago Pharma aim to strengthen its cardiometabolic pipeline while supporting internal innovations. This diverse approach not only broadens its product range but also positions the company well against emerging competitors.

Moreover, Jørgensen emphasizes working with various stakeholders to improve patient access to medications while addressing pricing concerns raised during discussions with U.S. lawmakers. This proactive engagement shows Novo Nordisk's commitment to balancing profit with social responsibility.

Core business segments:

Diabetes Care: This segment is the largest and most well-known. The company offers a range of products for diabetes management, including insulin (both long-acting and rapid-acting), GLP-1 receptor agonists, and other diabetes-related devices. Novo Nordisk is a leader in developing innovative treatments that improve glucose control and patient outcomes.

Obesity Care: In recent years, Novo Nordisk has expanded its focus to include obesity care, reflecting the growing importance of managing obesity as a chronic disease. The company has developed medications such as semaglutide for the treatment of obesity, capitalizing on its expertise in GLP-1 receptor agonists.

Hemophilia Care: The company also has a dedicated segment for the treatment of haemophilia and other bleeding disorders. This includes a variety of factor replacement therapies that help manage the condition and improve patients' quality of life.

Growth Hormone Therapy: This segment focuses on products for managing growth hormone deficiencies in children and adults. Novo Nordisk has a range of growth hormone therapies that are essential for patients with these deficiencies.

Hormone Replacement Therapy: This involves products designed for patients with hormonal deficiencies, including treatments for conditions like menopause. While smaller than its other segments, it adds diversity to Novo Nordisk's product offerings.

Other Serious Chronic Conditions: The company invests in R&D for other serious chronic conditions that include areas like cardiovascular diseases, chronic kidney disease, and autoimmune disorders.

🏛️ Capital Allocation

I see NVO’s capital allocation strategy as strong. The company prioritizes returning money to shareholders through dividends and share buybacks totalling DKK 61 billion in 2023 - demonstrating its financial strength amid rising demand for its products. It also invests heavily in internal research initiatives aimed at advancing innovation within its therapeutic areas.

Recent acquisitions such as Inversago Pharma and Dicerna Pharmaceuticals are strategically focused on enhancing its obesity and cardiometabolic pipelines while improving overall growth prospects. Furthermore, Novo Nordisk’s careful approach to managing debt ensures financial flexibility; as of late 2024, it maintains low levels of net debt.

Investments in production capacity are particularly noteworthy - these efforts reflect the company's commitment to meet rising global demand for GLP-1 therapies while addressing supply constraints that have previously affected growth. By effectively allocating capital toward both innovation and shareholder returns, NVO positions itself for long-term success.

Read Also:

✅ Advantages

Leadership in Diabetes Care: Novo Nordisk’s main advantage is its leadership position within diabetes and obesity care. Products like Ozempic and Wegovy have shown great effectiveness, leading to significant market adoption among patients.

Strong Research Pipeline: The company’s solid research capabilities ensure a pipeline filled with promising candidates that support ongoing innovation aimed at meeting unmet medical needs.

Strong Financial Position: With substantial free cash flow generation, NVO is well-positioned to invest strategically in innovation and capacity expansion.

Global Market Share: Holding a 34% global market share in diabetes care gives Novo Nordisk a competitive edge over competitors while building loyalty among healthcare providers.

Focus on Patient-Centric Solutions: The company's dedication to developing treatments that address rising global health challenges positions it favorably for long-term growth while improving patient outcomes.

❌ Disadvantages

Intense Competition: Despite its strengths, Novo Nordisk faces significant competition from other companies like Eli Lilly's Mounjaro and Zepbound that threaten its market share amid growing demand for obesity treatments.

Supply Constraints: Supply issues for key products like Wegovy have occasionally limited growth potential. Jørgensen acknowledged that demand may exceed production capabilities for some time.

Pricing Pressure: Ongoing pricing pressure from U.S. lawmakers creates uncertainty regarding revenue forecasts. Recent discussions highlighted concerns over affordability for patients relying on these medications.

Patent Expirations: Patent expirations for older products such as NovoLog and Levemir pose risks to revenue stability as generic alternatives become available on the market.

Regulatory Hurdles: Delays in regulatory approvals for new products add complexity to operations; these challenges can affect timelines for bringing innovative therapies to market.

🥇 Competitors

Novo Nordisk's main competitors include Eli Lilly, AstraZeneca, and Sanofi. Eli Lilly presents the biggest challenge with its innovative GLP-1 therapies such as Mounjaro and Zepbound that compete directly with Novo's products. These have gained popularity due to their effectiveness in weight management.

To Read: Mounjaro, Ozempic, Wegovy, Zepbound: What’s the Difference?

AstraZeneca has recently entered the obesity market with competitive offerings that could disrupt Novo's dominance. Their strategic initiatives aim at capturing more market share within this profitable segment. Meanwhile, Sanofi maintains an established presence in diabetes care that continues to challenge Novo's fortress in this important market.

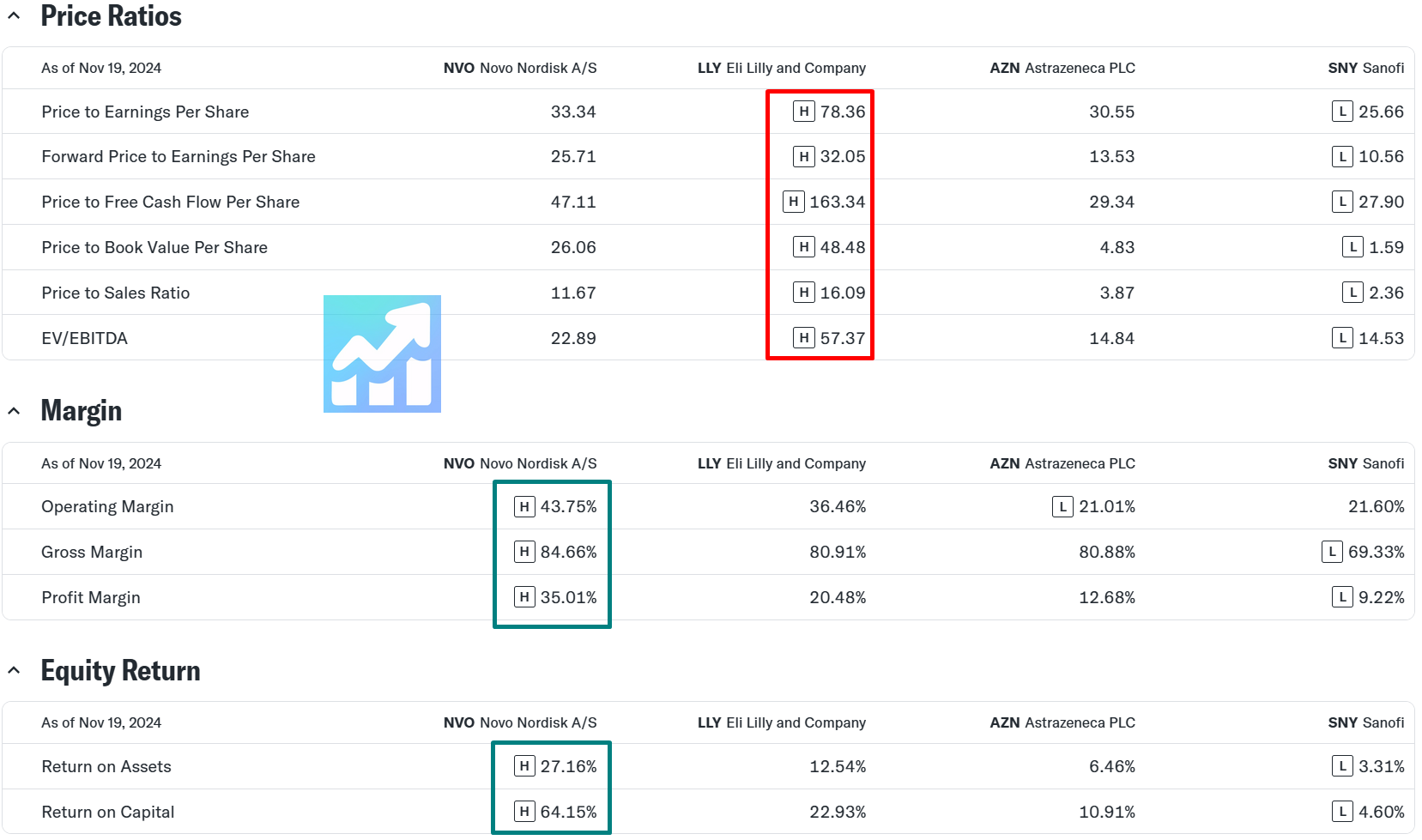

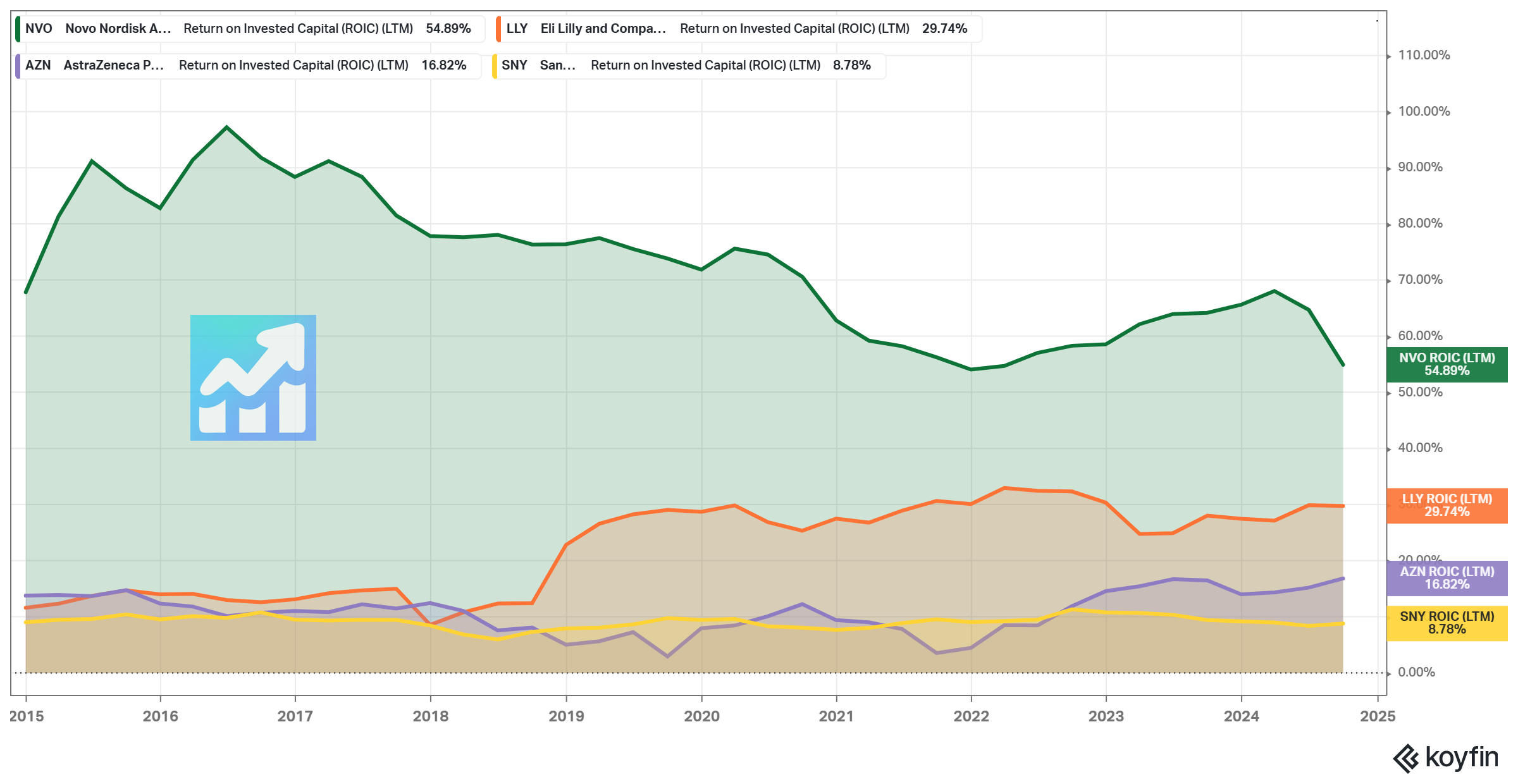

Pay attention that NVO has the highest margins and equity returns among its competitors (see my screenshots above). LLY is trading the most expensive at the moment.

⏮️ Past

NVO achieved an impressive 24% sales growth in the first nine months of 2024, driven by strong demand for GLP-1 diabetes and obesity treatments. The company now serves around 43 million patients, nearly 3 million more than last year. North America led with a 31% growth, while obesity care surged by 44%. Operating profit rose 22%, and guidance for 2024 has been narrowed to 23-27% sales growth and 21-27% operating profit growth. Free cash flow is expected between DKK 57-65 billion. Investments are set at DKK 45 billion, indicating robust expansion plans for the future.

Compound annual growth rate (CAGR) for the Novo Nordisk stock over 5-year, 10-year, and 15-year time periods. The 5-year CAGR is 29.73%, the 10-year CAGR is 17.94%, and the 15-year CAGR is 21.53%. All periods are outperforming the S&P 500.

Above is a comparison of total returns with the S&P 500 (VOO).

Latest important news:

FDA Confirms Availability of Wegovy Doses (October 2024). The FDA confirmed that all doses of Wegovy are now available, indicating improvements in production capacity. This announcement is crucial as Novo Nordisk continues to face high demand for its GLP-1 products and aims to mitigate ongoing supply constraints affecting both Wegovy and Ozempic.

Research Highlights Potential Benefits of Ozempic (October 2024). Recent studies suggested that Ozempic may lower the risk of Alzheimer's disease, highlighting its potential benefits beyond diabetes management. This finding could enhance market interest in the drug and align with Novo's strategy to expand the therapeutic applications of its products.

Novo Nordisk Expands Manufacturing Capacity (April 2024). To meet rising demand for its GLP-1 treatments, Novo Nordisk announced plans to expand its manufacturing capabilities both domestically and internationally. The company is collaborating with Catalent to enhance production and is focusing on addressing supply issues that have impacted the availability of its diabetes medications.

📶 Future

According to the Global Market Insights report, the global diabetes care devices market size was valued at around USD 45.1 billion in 2023 and is estimated to grow at 11.4% CAGR from 2024 to 2032. Diabetes care devices refer to a range of medical tools designed to monitor, manage, and treat diabetes. These devices include blood glucose meters, continuous glucose monitors (CGMs), insulin pumps, smart insulin pens, syringes, and lancets.

Based on short-term price targets (1-year period), the average price target for Novo Nordisk comes to $146.00. The forecasts range from a low of $85.50 to a high of $160.00. The average price target represents an increase of 46.28%.

Currently, 11 brokerage firms have made an average brokerage recommendation (ABR), with nine classified as Strong Buy, accounting for 81.82% of all recommendations. A month ago, Strong Buy also represented 81.82%.

Sales are projected to grow steadily, from $40.59 billion in FY 2024 to $57.17 billion in FY 2026, a CAGR of around 17-20%. EPS is also expected to grow strongly, from $3.23 in FY 2024 to $4.84 in FY 2026, a CAGR of 17-24%.

💲Current Valuation

The current Price/Earnings (LTM) ratio is 34.2x, which is a bit below the 5-year average of 35.0x. The current Price/Forward Earnings (NTM) ratio is 27.4x, also below the 5-year average of 29.9x.

What I like the most is that the current PEG ratio is the lowest for the last 10-year period (1.35).

The company is currently trading at almost the 5-year average Price/Sales ratio. In terms of the Price/FCF ratio, it is trading at a premium.

Additionally, I would like to note that the current Earnings Yield is 3.09%, which is higher than the 5-year average value of 2.87%; the US 10-year Treasury Bond Note Yield is 4.38%.

🏷️ Fair Price

The Long-Term Pick's Fair Price (Base Case) for NVO is $124.92. The current price of $104.09 is lower by 16.68%.

Fair-to-Current Price (%): 16.68%

Current Price/Fair Price: 0.83

I used:

Discount Rate: 12% (S&P 500 Next 5-Yr Growth Estimates is 11.05%)

Margin of Safety: 30%

Years: 5

Future EPS Growth Rate: 17% (See my comments below)

Future Dividend and Buyback Yield: 2.4% (Buybacks and dividends; I took 5-year average value)

Total Future Annual Growth Rate: 17 + 2.4 = 19.4%

Despite the fact that Koyfin projects a 5-year EPS growth rate of 20.35% annually, I decided to lower the value to 17%, but the higher value is doable - see the Future section.

I expect a 19.4% future annual growth rate achievable since past NVO performance shows that the company is able to produce such high annual returns - see the Past section.

☑️ Checklist

Profitability:

✅ Gross margin at least 40%: 85%

✅ Net margin at least 10%: 35%

✅ Management (ROIC, ROCE, ROE, ROA): Yes (All above 10%)

✅ Piotroski F-Score: 8 of 9 (Not passed: Lower Leverage YoY)

❌ Revenue surprises in last 7 years: No (2020; Based on TradingView's data)

❌ EPS surprises in last 7 years: No (2018, 2019, and 2020; Based on TradingView's data)

❌ EPS growth YoY 7 years in a row: No (2018, 2019; Based on TradingView's data)

Valuation and Advantage:

✅🟨 Valuation below its 5-yr average: Yes (Except P/FCF)

✅ Does it have a moat: Yes (wide)

Shares:

❌ Insider ownership at least 5%: No (0%)

✅ Less shares outstanding YoY: Yes

❌ Insider buys last six months: No

Price:

✅ 1-year stock price forecast is above 10%: +46.28%

✅ Next 5-Yr Growth Estimates (CAGR) is above S&P 500: Yes (20.35% vs 11.05%; Based on Koyfin)

✅ DCF Value: Fairly valued (10 years, discount rate: 10%, terminal growth: 3%, equity model: FCFE)

✅ Short Interest below 5%: Yes

✍️ Due Diligence

Profitability (8.5 of 10):

✅ Positive Gross Profit: 229.1B DKK (for the last twelve months)

✅ Positive Operating Income: 118.4B DKK (for the last twelve months)

✅ Positive Net Income: 94.7B DKK (for the last twelve months)

✅ Positive Free Cash Flow: 67B DKK (for the last twelve months)

✅ Exceptional 1-Year Revenue Growth: 26% (over the past 12 months)

✅ Exceptional 3-Year Revenue Growth: 26% (for the last 3 years)

✅ Exceptional Revenue Growth Forecast: 21% (over the next 3 years)

✅ Exceptional ROE: 89% (for the past 12 months)

✅ Exceptional 3-Year Average ROE: 82%

✅ ROE is Increasing: 73% → 89% (in the last 3 years)

✅ Exceptional ROIC: 35% (for the past 12 months)

✅ Exceptional 3-Year Average ROIC: 35%

❌ Declining ROIC: 38% → 35% (in the last 3 years)

Solvency (8 of 10):

✅ High Interest Coverage: 237.21 (earns more than enough operating income (118B DKK) to safely cover interest payments on its debt (499m DKK))

❌ Short-Term Solvency (short-term liabilties (208B DKK) exceed its short-term assets (195B DKK))

✅ Long-Term Solvency (long-term assets (397B DKK) exceed its long-term liabilties (277B DKK))

✅ Negative Net Debt: -23.4B DKK (has negative Net Debt - this means that the company has more cash and short-term investments (75B DKK) than debt (51B DKK))

✅ Low D/E: 0.43

✅ High Altman Z-Score: 9.35

This is not a financial or investing recommendation. It is solely for educational purposes.

Thank you for being a reader of Long-Term Pick! Your valuable feedback is welcome, so feel free to share your thoughts.

Appreciate the meticulous analysis Dan, thank you.

Thanks so much for this. Amazingly thorough breakdown.