Merck: Large Value Company Currently Undervalued

Merck & Co. (MRK) is a major pharmaceutical company, known for its important cancer therapies and vaccines. The company continues to play a key role in healthcare worldwide.

Changelog:

Feb 8, 2025: Updated fair price valuation: $188.

Jan 24, 2024: Overview: FDA Acceptance for Clesrovimab, Strategic Focus on Oncology, Pipeline Developments, and Focus on Global Markets.

Merck & Co. is a major American pharmaceutical company known for its vital role in healthcare worldwide. Specializing in innovative drugs and vaccines, the company develops treatments for major health challenges, including cancer, cardiovascular disease, and infectious diseases. The company’s top products, like Keytruda for cancer and Gardasil for HPV, have transformed patient care and improved Merck's position in the industry. Additionally, Merck is presented in animal health. The company focuses on advanced research and new treatment areas.

Previous publication:

Content:

💡 Investment Thesis

🧐 Company Overview

🏰 Economic Moat

🚀 Business Strategy

✅ Advantages

❌ Disadvantages

🏛️ Capital Allocation

🥇 Competitors

⏮️ Past

📶 Future

💲Current Valuation

🏷️ Fair Price

☑️ Checklist

✍️ Due Diligence

💡 Investment Thesis

A strong lineup of important drugs and vaccines, including Keytruda for cancer and Gardasil for HPV prevention. Merck’s strengths come from its solid patents, high spending on research, and valuable partnerships. Reliable income, supported by demand in both human and animal health, gives it a steady cash flow, which is used to grow and reward shareholders.

The company is focused on leading areas like cancer and immunotherapy, which keeps it aligned with current trends in healthcare. Keytruda, its top drug, is now approved for over 40 types of cancer in the U.S., showing its strong position in this market. The company’s future looks promising, with new drugs in late-stage trials and partnerships with firms like Moderna and Daiichi Sankyo to develop new treatments. Although challenges like pricing rules and patent losses are expected, Merck’s focus on early-stage treatments and personalized medicine shows it is planning for long-term steady growth.

The stock is trading at just 10.70 times its forward earnings and mostly below its 5-year averages. High Earnings Yield. Based on my Fair Price estimate, is undervalued by more than 30%. Other analysts are also positive-looking. If you are looking for a stable healthcare investment with steady growth potential, worth noting.

⬇️ Download Quick Analysis in PDF/PNG + Market Trends (Recommended)

🧐 Company Overview

Incorporated: 1891

Sector: Healthcare

Industry: Drug Manufacturers

Stock Style: Large Value

Market Cap: $258.25 Bil

Total Number of Employees: 72,000

Website: https://www.merck.com/

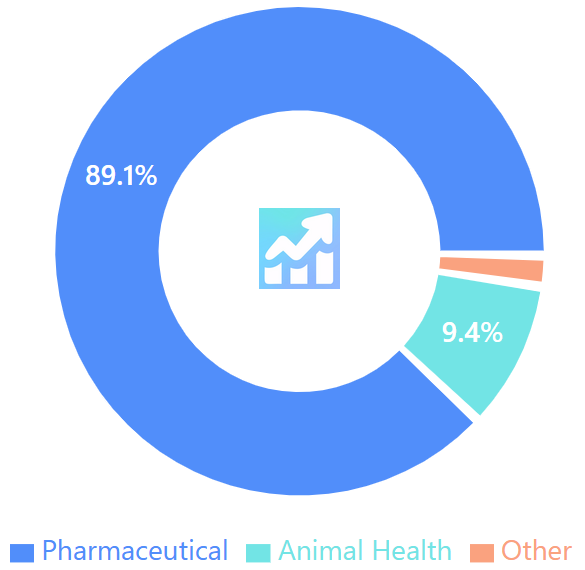

Earnings Date: February 6, 2025Merck & Co. (MRK) has been a major player in healthcare for over a century. The company is known for developing and delivering medicines, vaccines, and animal health products that address serious health challenges. With a diverse product lineup, Merck generated $60.1 billion in revenue in 2023. Pharmaceuticals made up 89.1% of total sales, with the remaining 10.9% coming from its Animal Health segment. Keytruda, its flagship oncology drug, contributes around 50% of Merck’s pharmaceutical revenue, earning $7.27 billion in Q3 alone—up 21% year-over-year due to demand in early-stage lung cancer and other new indications. Gardasil, Merck’s HPV vaccine, also saw an impressive 4% increase in Q3 sales to $2.48 billion, showing solid growth in the U.S. despite a dip in China.

To Read: Merck’s History

Rob Davis has been Merck’s CEO since early 2021, following years of financial and operational leadership within the company. Davis was initially Merck’s CFO and held senior roles at Baxter and Eli Lilly before joining Merck. He is continuing the legacy of former CEO Ken Frazier, who led Merck through major growth phases and innovations. Davis's approach reflects Merck’s long-term commitment to innovation and value for shareholders.

🏰 Economic Moat

Merck has a wide economic moat supported by strong patents, effective production capabilities, and a high-quality research and development base. Patents protect Merck's major drugs from competitors, ensuring steady revenue from these products. With an extensive sales network and effective marketing, Merck reaches global markets efficiently, helping it stand out in a competitive industry.

Vast R&D resources also provide an advantage in discovering new drugs, supporting its ability to stay relevant with new therapies over time. Additionally, Merck's established presence in immuno-oncology and vaccines offers long-term growth potential, despite price pressure from governments worldwide.

Key Components:

Intangible Assets: Valuable patents, established brand, and critical regulatory approvals.

Switching Costs: Once healthcare providers integrate Merck’s therapies, especially in complex treatment areas like immuno-oncology, switching to a competitor’s drugs can be challenging and costly due to specific treatment protocols.

Network Effects: As more oncologists adopt Keytruda as a first-line treatment, its credibility and effectiveness become even more recognized.

Cost Advantages: Operational efficiency and economies of scale, which allow it to allocate significant resources to R&D while maintaining high profit margins. A ten-year average operating margin of around 24% reflects strong pricing power and effective cost management.

Recurring Revenue Model: Their revenue stream is heavily supported by ongoing drug sales and repeat orders for vaccines. This recurring revenue model provides stability and predictability.

🚀 Business Strategy

Merck’s business strategy focuses on expanding its core strengths in oncology and vaccines while diversifying into other areas to reduce dependence on Keytruda. In oncology, the company is committed to growing Keytruda’s reach in new cancer indications, especially in early-stage treatment. Merck is also developing a personalized mRNA cancer vaccine with Moderna, further strengthening its cancer treatment portfolio.

The company aims to diversify through targeted acquisitions, with recent deals like Prometheus Biosciences in 2023 adding immune-mediated disease treatments to its lineup. These efforts reflect Merck’s goal to address unfulfilled medical needs while securing its future growth through a broader pipeline.

Related analysis:

Core business segments:

Pharmaceuticals: This is the largest segment and includes a wide range of medications covering various therapeutic areas. Key products in this segment include:

Oncology: Notable for Keytruda (pembrolizumab), a leading cancer immunotherapy.

Vaccines: This includes products such as Gardasil (for HPV) and Vaxneuvance (pneumococcal vaccine).

Infectious Diseases: Medications for HIV and hepatitis C, including the Dovato and Isentress lines.

Revenue by Source, 2023 FY (Author’s Chart)

Animal Health: Merck is a significant player in the animal health industry, providing vaccines and medications for both livestock and companion animals. This segment includes products that prevent and treat infectious diseases and control parasites.

Consumer Health: Although a smaller segment compared to Pharmaceuticals and Animal Health, Merck offers over-the-counter products targeting wellness and disease prevention, including products in allergy relief, pain management, and digestive health.

Revenue by Country, 2023 FY (Author’s Chart) Research and Development (R&D): While not a business segment, I see R&D as crucial to Merck’s strategy, focusing on the discovery and development of new medications and vaccines. This segment can impact the Pharmaceuticals segment significantly, as it can lead to new products that drive growth.

✅ Advantages

Their leading position in oncology, with Keytruda as a major player. Approved for over 40 cancer indications in the U.S., Keytruda is expected to continue its growth trajectory, especially with recent approvals for early-stage cancers.

A diverse portfolio includes successful vaccines and treatments in cardiovascular, infectious diseases, and animal health, reducing its reliance on any single product or market. For example, Gardasil has been a key contributor, bringing in over $2.4 billion in Q3 2024 alone.

Merck’s R&D capability allows them to develop and launch new products regularly. Currently, Merck’s R&D investment is close to 36% of its revenue.

Their commitment to shareholder returns is evident in their steady dividends and share buybacks. In recent years, Merck has repurchased shares when prices were favorable.

Firsts in Vaccines: Maurice Hilleman, a scientist at Merck, developed several groundbreaking vaccines including the first rubella vaccine and the first MMR (measles, mumps, rubella) vaccine.

Financial stability. With $11.35 billion in cash as of June 2024 and a reasonable debt load, Merck is in a strong position to have new acquisitions.

❌ Disadvantages

Merck’s heavy reliance on Keytruda accounts for around half of its pharmaceutical revenue. With its U.S. patent set to expire in 2028, this dependency creates future uncertainty.

The diabetes franchise, including Januvia and Janumet, faces growing competition, particularly from generics outside the U.S., and sales have been declining. In Q3 2024, diabetes franchise sales dropped by 23%.

Merck faces challenges from new price regulations, like the Inflation Reduction Act in the U.S., which aims to lower drug prices under Medicare. These regulations could impact Merck’s profit margins.

The company has experienced setbacks in its pipeline, with clinical holds and some studies failing to meet their goals, like the recent failure of a Keytruda combination study in colorectal cancer.

🏛️ Capital Allocation

From my point of view, Merck’s capital allocation strategy is a balance between shareholder rewards and reinvestment. The company distributes about 50% of earnings as dividends, aiming to provide a stable income for shareholders. The company also conducts share buybacks, particularly when stock prices are favorable, reinforcing long-term value.

In acquisitions, Merck has been strategic, targeting companies that strengthen its core areas, such as EyeBio for ophthalmology and Prometheus Biosciences for immune-mediated diseases. The company’s debt-to-capital ratio, around 44% as of mid-2024, indicates healthy debt management, leaving room for further acquisitions and investments.

Overall, Merck’s capital allocation reflects a commitment to growth and shareholder value.

🥇 Competitors

Merck faces competition from several major pharmaceutical companies, including Bristol-Myers Squibb, Eli Lilly, and Pfizer. Bristol-Myers Squibb, known for its immunotherapy Opdivo, is a strong competitor in oncology, especially in lung cancer, but Merck's Keytruda leads in approved cancer indications. This gives Merck an edge in certain markets.

Merck has over 80 programs in phase 2, more than 30 in phase 3, and over 10 under regulatory review, focusing on various therapeutic areas including oncology, cardiovascular diseases, infectious diseases, and vaccines.

Eli Lilly, with its strong presence in diabetes care and a growing oncology pipeline, is a tough competitor. However, Merck’s broader portfolio in vaccines and animal health sets it apart. Merck’s offerings are more diversified, which provides stability beyond oncology and diabetes.

Pfizer is another significant rival, especially in vaccines and hospital acute care. While Pfizer has a strong vaccine lineup, Merck’s Gardasil has a solid base in the HPV vaccine market, showing Merck's leadership in this area. Additionally, Merck’s focus on expanding its immuno-oncology range keeps it competitive against Pfizer's varied portfolio.

⏮️ Past

In Q3, Merck reported $16.7 billion in revenues, up 4%, driven by a 21% increase in Keytruda sales to $7.4 billion. While Gardasil sales fell 10% to $2.3 billion due to a slow recovery in China, strong demand in other regions provides optimism.

Worth noting that during the 5-, and 10-year period, MRK underperformed the industry and the S&P 500 (CAGR).

📶 Future

Based on the Evaluate report (the leading provider of market insights for the pharmaceutical industry), the global pharmaceutical market is projected to reach $1.7 trillion by 2030, with a CAGR of 7.7% from 2024 onwards. This growth is largely attributed to the development of "big drugs for big diseases," particularly in the obesity treatment sector.

The company expects annual revenue growth of 6-7% for 2024, targeting $63.6-$64.1 billion. The anticipated launch of new products like Winrevair and Capvaxive, along with a growing pipeline, provides a strong long-term growth outlook, with an EPS guidance of $7.72-$7.77.

Based on short-term price targets offered by 24 analysts, the average price target for Merck is $138.88. The forecasts range from a low of $115.00 to a high of $168.00; the average price target represents an increase of 35.73%.

Merck currently has an average brokerage recommendation (ABR) of 1.30 on a scale of 1 to 5 (Strong Buy to Strong Sell), calculated based on the actual recommendations (Buy, Hold, Sell etc.) made by 27 brokerage firms. The current ABR compares to an ABR of 1.23 a month ago based on 26 recommendations. Of the 27 recommendations deriving the current ABR, 23 are Strong Buy, representing 85.19% of all recommendations. A month ago, Strong Buy represented 88.46%.

💲Current Valuation

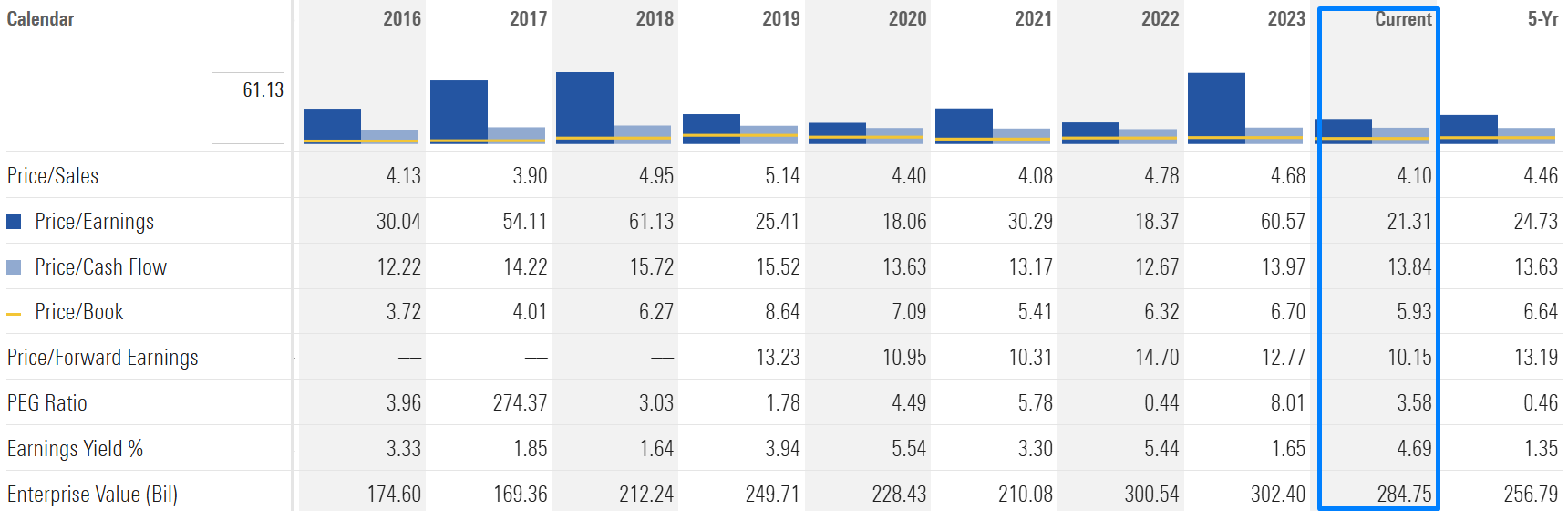

The current valuation shows that the company is trading at a lower price compared to its 5-year average. The current Price/Forward Earnings ratio is only 10, but pay attention to the high PEG ratio. The Earnings Yield ratio is high, that I like the most.

In addition, I would like to add improved operating performance (management does its work well):

🏷️ Fair Price

The Long-Term Pick's Fair Price (Base Case) for MRK is $148.54. The current price of $102 is lower by 31.32%.

Fair-to-Current Price (%): 31.32%

Current Price/Fair Price: 0.69

I used:

Discount Rate: 12% (S&P 500 Next 5-Yr Growth Estimates is 11.04%)

Margin of Safety: 30%

Years: 5

Future EPS Growth Rate: 7% (I will explain below)

Future Dividend and Buyback Yield: 3% (I will explain below)

Total Future Annual Growth Rate: 7 + 3 = 10%

The expected YoY EPS growth for FY 2024 is projected to be significantly higher (see the image below) compared to FY 2023, but it is anticipated to stabilize in the following years. As mentioned in the Future section, the global pharmaceutical market is projected to have a compound annual growth rate (CAGR) of 7.7% through 2030. Initially, I set this figure at 8%, but I revised it to 7% due to Merck being a large value stock with potential future challenges, which we discussed in the Disadvantages section. Therefore, I believe 7% is a reasonable estimate for our analysis.

The average buyback and dividend yield is 3.46%, but for Merck, I decided to lower this figure to 3%. The reason is similar: Merck is a large-cap stock that may face potential issues in the future and increased competition. Consequently, I aimed for a final total future growth rate of 10% 😉

For the Bull Case, I used a future exit P/E of 24, which is based on the company's five-year average. In the Bear Case, I selected the lowest P/E ratio from the last few years, which was 18. For the Base Case, I took the midpoint between the Bull and Bear Cases, resulting in a value of 21. Notably, 21 is also their current P/E ratio.

I would like to compare my valuation with the opinions of other analysts to see what they think. In fact, I already did it in the Future section, but from a different perspective and a different resource.

☑️ Checklist

Profitability:

✅ Gross margin at least 40%: 78%

✅ Net margin at least 10%: 19%

✅ Management (ROIC, ROCE, ROE, ROA): Yes (All above 10%)

✅ Piotroski F-Score: 7 of 9 (Not passed: Lower Leverage YoY, Less Shares Outstanding YoY)

❌ Revenue surprises in last 7 years: No (2017, 2019, and 2020; Based on TradingView's data)

❌ EPS surprises in last 7 years: No (2020; Based on TradingView's data)

❌ EPS growth YoY 7 years in a row: No (2023)

Valuation and Advantage:

✅ Valuation below its 5-yr average: Yes

✅ Does it have a moat: Yes (wide)

Shares:

❌ Insider ownership at least 5%: No (0.06%)

❌ Less shares outstanding YoY: No

❌ Insider buys last six months: No

Price:

✅ 1-year stock price forecast is above 10%: +36%

✅ Next 5-Yr Growth Estimates (CAGR) is above S&P 500: No (over 20% due to low EPS in 2023 vs 11.04%; Based on Yahoo Finance)

✅ DCF Value: $126.61 (Undervalued by 20%; 10 years, discount rate: 10%, terminal growth: 3%, equity model: FCFE)

✅ Short Interest below 5%: Yes (1.03%)

✍️ Due Diligence

Profitability (7 of 10):

✅ Positive Gross Profit: 49B USD

✅ Positive Operating Income: 16.9B USD

✅ Positive Net Income: 12.1B USD

✅ Positive Free Cash Flow: 13.1B USD

✅🟨 Positive 1-Year Revenue Growth: 7%

✅🟨 Positive 3-Year Revenue Growth: 11%

✅🟨 Positive Revenue Growth Forecast: 7%

✅ Exceptional ROE: 29%

✅ Exceptional 3-Year Average ROE: 26%

✅ ROE is Increasing: 22% > 29%

✅ Positive ROIC: 16%

✅ Positive 3-Year Average ROIC: 13%

✅ ROIC is Increasing: 13% > 16%

Solvency (7 of 10):

✅ High Interest Coverage: 13.71 (earns more than enough operating income (17B USD) to safely cover interest payments on its debt (1B USD))

✅ High Altman Z-Score: 4.31

✅ Short-Term Solvency (short-term assets (38B USD) exceed its short-term liabilties (26B USD))

✅ Long-Term Solvency (long-term assets (113B USD) exceed its long-term liabilties (69B USD))

❌ Positive Net Debt: 23.4B USD (has more debt (35B USD) than cash and short-term investments (11B USD))

✅ Low D/E: 0.8

This is not a financial or investing recommendation. It is solely for educational purposes.

I have been looking this company as well, it's at interesting value. Thank for your review and sharing.

Seems to be a good entry point. Thanks for your work.