Medpace: Well-Diversified CRO Service Provider Undervalued By 13%

A contract research organization (CRO) that focuses on late-stage drug development. Provides services to small and midsize biotech companies, and operates in 40 countries.

Changelog:

Feb 12, 2025: Updated fair price valuation: $370.

Jan 27, 2025: Overview: Investigation into financial performance.

Nov 01, 2024: Updated fair price valuation: $380.92.

Medpace (MEDP) is a contract research organization (CRO) that focuses on late-stage drug development. It offers full clinical trial services to small and midsize biotech, pharmaceutical, and medical device companies. The company also provides extra services, like bioanalytical lab work and imaging capabilities. Medpace started over 30 years ago and now has more than 5,400 employees in 40 countries. The company mainly operates in the U.S., but it also has locations in Europe, Asia, South America, Africa, and Australia.

Previous publication:

Content:

💡 Investment Thesis

🧐 Company Overview

🏰 Economic Moat

🚀 Business Strategy

✅ Advantages

❌ Disadvantages

🏛️ Capital Allocation

🥇 Competitors

⏮️ Past

📶 Future

💲Current Valuation

🏷️ Fair Price

☑️ Checklist

✍️ Due Diligence

💡 Investment Thesis

MEDP is a well-established contract research organization (CRO) that focuses on late-stage drug development, primarily serving small and midsize biotech firms. The company’s deep expertise in managing complex, multinational trials and its high customer switching costs create a substantial economic moat. Medpace’s global regulatory knowledge and ability to shorten clinical trial times give it a significant advantage, supporting long-term client relationships.

Financially, Medpace shows strong growth and has a $2.9 billion backlog. The company has a healthy balance sheet, low debt, and focuses on organic growth. However, recent project cancellations and the need to stay innovative present challenges. With a fair price estimate of $394.83, Medpace appears undervalued by about 13%, offering upside potential for long-term investors. At least, a very good choice for a watchlist and regular checks.

⬇️ Download Quick Analysis in PDF (3 pages, 800 KB)

🧐 Company Overview

Incorporated: 1992

Sector: Healthcare

Industry: Diagnostics & Research

Stock Style: Small Growth

Market Cap: $10.62 Bil

Earnings Date: Oct 21, 2024Medpace Holdings is a global late-stage contract research organization (CRO) that provides comprehensive drug development and clinical trial services primarily to small and midsize biotechnology, pharmaceutical, and medical device companies. Founded over 30 years ago in Cincinnati, the company operates across 40 countries with a workforce exceeding 5,400 employees.

Medpace's evolution includes significant milestones, such as CCMP Capital's acquisition of an 80% stake for $285 million in 2011, followed by Cinven's purchase of this stake for $915 million in 2014. Under Cinven's ownership, Medpace expanded its international presence and workforce by more than 55%, eventually going public in 2016.

To Read: Company Overview

The company has demonstrated impressive growth, with its quarterly results showing an 18% year-over-year revenue increase to $511 million in the first quarter of 2024. In the second quarter of 2024, revenue grew by 14.6% year-over-year to $528.1 million.

To Read: What Is a CRO?

The stated mission of the company:

Our unique global partnering philosophy emphasizes an uncompromising commitment to clinical research and to the highest level of ethical standards and performance in our jobs. We are selective about the projects we engage in because we are devoted to quality and providing our partners with best-in-class service.

Medpace’s dedicated teams serve as an extension of your team – we engage quickly and provide strategic thinking – ensuring start-up times are met, superior quality, and the most efficient delivery of every phase of your clinical trial. Our therapeutic and regulatory experts are committed to streamlining your path to approval so every partnership is designed to create research solutions focused on your critical needs.

August J. Troendle, M.D. has been the CEO and Chairman of the Board of Medpace since he founded the company in July 1992, and also was the President through July 31, 2021. Before founding Medpace, Mr. Troendle served as Assistant Director, Associate Director and Senior Associate Director from 1987 to 1992 at Sandoz (Novartis), where he was responsible for the clinical development of lipid-altering agents.

🏰 Economic Moat

Medpace has an economic moat primarily supported by high customer switching costs and valuable intangible assets. The company's expertise in late-stage clinical trials is crucial, as these are larger in scope, more complex, and often multinational, making it difficult for clients to change providers mid-trial.

The drug development process typically spans 10-15 years from discovery to FDA registration, with clinical trials consuming 7.5 years on average. CROs like Medpace complete trials up to 30% faster than in-house pharma company teams, providing significant value by extending the patent-protected market time for successful drugs. The company has submitted drugs for regulatory approval in 60 countries, demonstrating its global regulatory expertise. Additionally, Medpace offers decentralized clinical trial capabilities, positioning it well for next-generation trials that have seen increased adoption since the COVID-19 pandemic.

🚀 Business Strategy

Medpace serves small to midsize biotech companies, which account for 90% of clients and approximately 96% of revenue. Unlike large pharmaceutical companies that might outsource specific tasks, these smaller clients typically need full-service solutions for their clinical trials.

The company provides a comprehensive collection of services (see the list below). This full-service model aligns with the needs of smaller biotech firms that lack in-house clinical trial capabilities and prefer to work with a single, trusted CRO throughout their drug development process.

MEDP's core business segments:

Clinical Development Services: This is the primary segment of Medpace, with a wide range of services to support clinical trial operations. This includes study design, site selection, patient recruitment, data collection, and regulatory compliance. Medpace works with both drug and medical device developers in various phases of clinical trials, from preclinical to post-marketing studies.

Laboratory Services: MEDP offers lab services that support clinical trials by providing testing and analysis of biological samples. This segment ensures accurate data collection and compliance with regulatory standards, which is crucial for the integrity of clinical studies.

Regulatory Affairs and Consulting: Medpace provides guidance and services to its clients for regulatory submissions and compliance, helping them navigate the complexities of requirements from health authorities like the FDA and EMA. Their expertise simplifies the process of bringing new drugs and devices to market.

Post-Marketing Services: After a product is launched, the company continues to support clients with services related to post-marketing supervision, including Phase IV clinical trials and observational studies to monitor the effectiveness and safety of products in the general population.

Therapeutic Expertise: Medpace has specialized capabilities across various therapeutic areas, including oncology, cardiology, neuroscience, and infectious diseases. This segment highlights the company’s ability to handle trials that require specific knowledge of particular medical conditions and treatments.

✅ Advantages

Medpace maintains a strong market position with a healthy backlog of $2.8 billion as of year-end 2023, representing a 20% increase from the previous year.

The company stands out due to its deep expertise in specific therapeutic areas, making it highly efficient in managing complex clinical trials. Also, Medpace offers a full range of services.

MEDP builds dedicated project teams for each client, allowing for better communication, faster decision-making, and a more personalized approach. With a global presence and strong local regulatory knowledge, Medpace is well-equipped to handle international clinical trials.

The company enhances trial management through real-time data collection and analytics.

❌ Disadvantages

The company experienced increased cancellations in recent quarters, exceeding its normal range of below 4.5%. While management attributes these cancellations to product performance and failed compounds rather than funding issues, this trend could negatively impact revenue if it persists.

Medpace must continually invest in innovative technology and next-generation clinical trial processes to avoid losing market share to more innovative competitors.

The company is exposed to product governance risks, as it must ensure trials meet strict quality and safety standards from various regulatory entities.

Recruitment and retention of skilled professionals are crucial, as staffing issues could impact trial execution.

🏛️ Capital Allocation

In my view, MEDP remains a conservative capital allocation approach. The company has minimal debt and focuses on organic growth rather than acquisitions. While Medpace does not currently pay a dividend, this aligns with its growth-oriented strategy of reinvesting in the business.

As we can see, the company has been reducing its shares outstanding for the last seven years.

🥇 Competitors

The company's key competitors include Icon PLC (ICLR), IQVIA Holdings Inc (IQV), and Fortrea Holdings Inc (FTRE). Icon PLC is a global provider of outsourced development and commercialization services to pharmaceutical, biotechnology, medical device, and government organizations. IQVIA Holdings combines advanced analytics, technology solutions, and contract research services for the life sciences industry. Fortrea Holdings offers clinical development and patient access solutions to the biopharmaceutical and medical device industry.

Medpace's focus on small and midsize biotech clients differentiates it from these competitors who target different market segments. Despite operating in the same industry, Medpace has maintained its competitive edge through its full-service model and expertise in complex, multinational clinical trials.

⏮️ Past

In the second quarter of 2024, revenue grew by 14.6% year-over-year to $528.1 million, while EBITDA increased by 34.2% to $112.3 million. Despite higher-than-usual cancellations, the company's ending backlog was up 13.7%, totaling $2.9 billion. Medpace has raised its full-year revenue guidance to between $2.125 billion and $2.175 billion, representing 12.7% to 15.3% growth. EBITDA is expected to range from $430 million to $460 million, reflecting 18.6% to 26.9% growth. Although project cancellations impacted net new business awards, the company remains optimistic about maintaining industry-leading organic revenue growth and profitability.

As we see, MEDP has demonstrated strong long-term performance. The company has outperformed both its industry peers and the broader index over extended periods. Notably, MEDP kept a strong 5-year performance with a 31.77% CAGR.

To get more premium insightful content and see my portfolio, join my Patreon 👍 Your support is important.

📶 Future

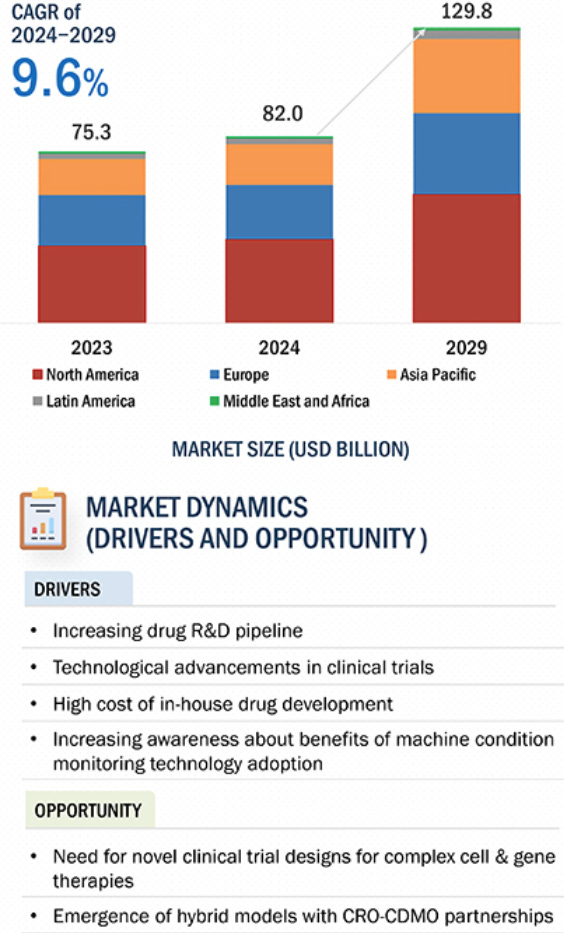

According to Markets&Markets, the CRO services market is projected to reach USD 129.8 billion by 2029 from an estimated USD 82.0 billion in 2024, at a CAGR of 9.6% during the forecast period.

Let’s take a look at future sales and EPS projections.

MEDP's financial outlook appears strong, with projections showing consistent revenue growth in the low teens and healthy earnings expansion over the next three years. The company is expected to maintain steady progress, growing from $2.14B to $2.75B in sales while boosting EPS from $11.81 to $15.01. Although EPS growth moderates from an exceptional 32.38% to align more closely with revenue growth, the overall trajectory indicates sustained, profitable expansion through FY2026.

Price targets suggest significant upside potential, with an average target of $395.00 representing nearly 17% upside from the last close of $337.75. The range spans from a low of $336.00 (-0.52% downside) to an optimistic high of $435.00, implying a potential upside of almost 29%.

The broker rating breakdown shows consistent support over the past three months, with 9 total ratings currently split between Strong Buy and Hold recommendations.

💲Current Valuation

MEDP's current valuation presents a nuanced picture against 5-year averages. While Price/Book has increased significantly to 13.33 from 8.24, key metrics like P/E (32.24 vs 34.12) and P/Forward Earnings (24.27 vs 30.67) are below historical averages. With a PEG ratio of 0.92, though higher than the 0.46 average, the stock appears reasonably valued given its growth prospects despite some elevated multiples.

🏷️ Fair Price

➡️ Updated fair price valuation: https://longtermpick.com/p/updated-valuations-nov-24

As I wrote on my Patreon, I decided to use a 5-year period for my fair price estimation instead of a 10-year period, since I look at the next 3-5-year earnings estimates and take into account 5-year averages. In addition, it's harder to predict a 10-year fair price than a 5-year.

The Long-Term Pick's Fair Price (Base Case) for MEDP is $394.83. The current price of $343.05 is lower by 13.11%.

Fair-to-Current Price (%): 13.11%

Current Price/Fair Price: 0.87

I used:

Discount Rate: 12% (S&P 500 Next 5-Yr Growth Estimates is 11.91%)

Margin of Safety: 30%

Years: 5

Future EPS Growth Rate: 16.5%

Future Dividend and Buyback Yield: 0%

Total Future Annual Growth Rate: 16.5 + 0 = 16.5%

For the Future Dividend and Buyback Yield, I took 0% since the company increased shares that were sometimes outstanding in the past. Despite this, the 3-year average share buyback ratio is 4.7. So, the Total Future Growth should be even higher!

For the Base Case, the Future Expit P/E is 28. 5-Yr average P/E ratio is 32 (I took this value for the Bull Case), the lowest P/E during the last ten years was 32 in 2018. For the Bear Case, I just took the Base Case - 3.

As we can see, the company is undervalued in the Base and Bull Case and fairly valued in the Bear Case.

☑️ Checklist

Profitability:

❌ Gross margin at least 40%: 29%

✅ Net margin at least 10%: 17%

✅ Management (ROIC, ROCE, ROE, ROA): Yes (All above 10%)

✅ Piotroski F-Score: 7 of 9 (Not passed: Less Shares Outstanding YoY, Higher Gross Margin YoY)

✅ Revenue surprises in last 7 years: Yes (Based on TradingView's data)

✅ EPS surprises in last 7 years: Yes (Based on TradingView's data)

✅ EPS growth YoY 7 years in a row: Yes

Valuation and Advantage:

❌ Valuation below its 5-yr average: No

✅ Does it have a moat: Yes

Shares:

✅ Insider ownership at least 5%: Yes (17.53%)

✅ Less shares outstanding YoY: Yes

❌ Insider buys last six months: No

Price:

✅ 1-year stock price forecast is above 10%: +17%

✅ Next 5-Yr CAGR is above S&P 500: Yes (16.52% vs 11.91%)

❌ DCF Value: $308.24 (Overvalued by 10%; 10 years, discount rate: 10%, terminal growth: 3%, equity model: FCFE)

✅ Short Interest below 5%: Yes (3%)

✍️ Due Diligence

Profitability:

✅ Positive Gross Profit: 579m USD

✅ Positive Operating Income: 381.4m USD

✅ Positive Net Income: 339.6m USD

✅ Positive Free Cash Flow: 502.8m USD

✅ Exceptional 1-Year Revenue Growth: 21%

✅ Exceptional 3-Years Revenue Growth: 25%

✅ Positive Revenue Growth Forecast: 15%

✅ Exceptional ROE: 59%

✅ Exceptional 3-Year Average ROE: 45%

✅ ROE is Increasing: 22% > 59%

✅ Positive ROIC: 24%

✅ Positive 3-Year Average ROIC: 19%

✅ ROIC is Increasing: 16% > 24%

Solvency:

❌ Short-Term Solvency (short-term liabilties (993m USD) exceed its short-term assets (873m USD))

✅ Long-Term Solvency

✅ Low D/E

✅ High Altman Z-Score: 7.91

This is not a financial or investing recommendation. It is solely for educational purposes.

I also added to my position. Earnings next week will move the stock higher or lower. Always double digit move. Hope it goes up again

Bought this one last week around 323,2 usd.