Updated Valuations: FTNT, PINS, MKTX, MPWR, and MEDP

Another bunch of companies covered by Long-Term Pick (updated page) released their quarterly and yearly earnings reports (first bunch). It's time to update their fair price valuations and review the latest reports. Please note that patrons of the project will receive an additional update on premium companies.

Some explanations regarding screenshots with fair price estimates:

I marked cells that I updated as grey (after the latest earning reports).

Fair-to-Current Price and Current Price/Fair Price: 🟢 undervalued, 🔵 fairly valued (+/- 5% is “fairly”), 🟡 overvalued.

Additionally, I included updated current valuations alongside their 5-year averages for easy comparison. I also added average future price estimates from other analysts to compare with my Base Fair Price Estimates and past quarterly EPS surprises vs. actuals for the latest 10-year period.

🟡 Fortinet (FTNT)

📝 Analyst Notes

My previous fair price was $95. After changes, the new fair price has become $78 (lower). I’ve decreased the future EPS growth rate. Please note that FTNT’s PEG ratio is over 3, which is high, and overall I see the stock as overvalued. When I was writing my analysis, Fortinet was more attractive than now in terms of valuation.

🏷️ Updated Valuation

Latest earnings report (Feb 6, 2025):

👍 Positive Points

Fortinet reported a record operating margin of 39% for the fourth quarter of 2024.

Total revenue grew by 17%, with product revenue increasing by 18%, marking the highest growth rate in six quarters.

Unified SASE growth was strong at 13%, accounting for 23% of the business, driven by an 85% increase in security service age building.

The company added a record 6,900 new logos, indicating strong market penetration and alignment with channel partners.

Fortinet was recognized on Forbes' most trusted company list, ranked number 7 overall, and the only cybersecurity company in the top 50, highlighting its transparency and commitment to customers.

👎 Negative Points

Billings growth for the first quarter of 2025 is projected to be weaker, with a midpoint growth of only 11%.

The guidance for product revenue in the next quarter does not reflect the strong performance seen in the fourth quarter, indicating potential volatility.

There is uncertainty regarding the impact of tariffs on demand and supply chain, particularly affecting Latin America, Canada, and US government sales.

The average contract term decreased by one month year over year, which could indicate shorter customer commitments.

The financial impact from recent acquisitions, including Lacework and Perception Point, is expected to decrease the operating margin by 50 basis points for the full year 2025.

💲Current Valuation

📈 Price Forecast

↗️ Sales and EPS Forecast

⏺️ EPS Actual vs. Estimate

📈 5Y Performance

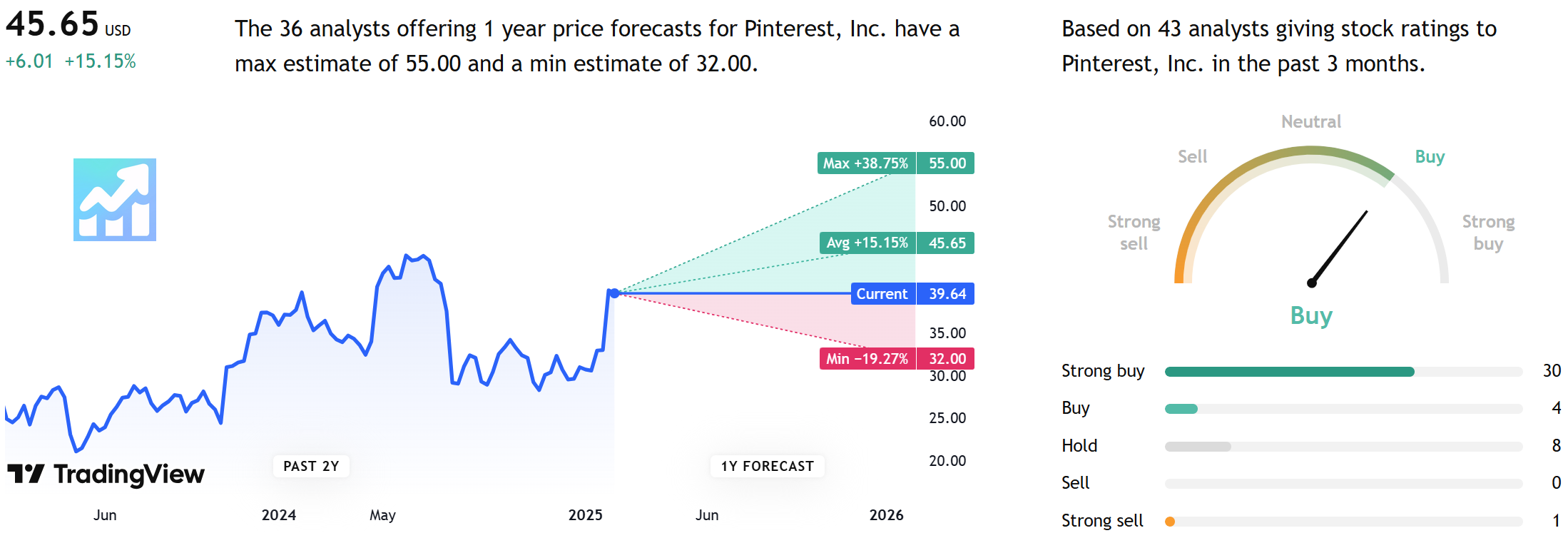

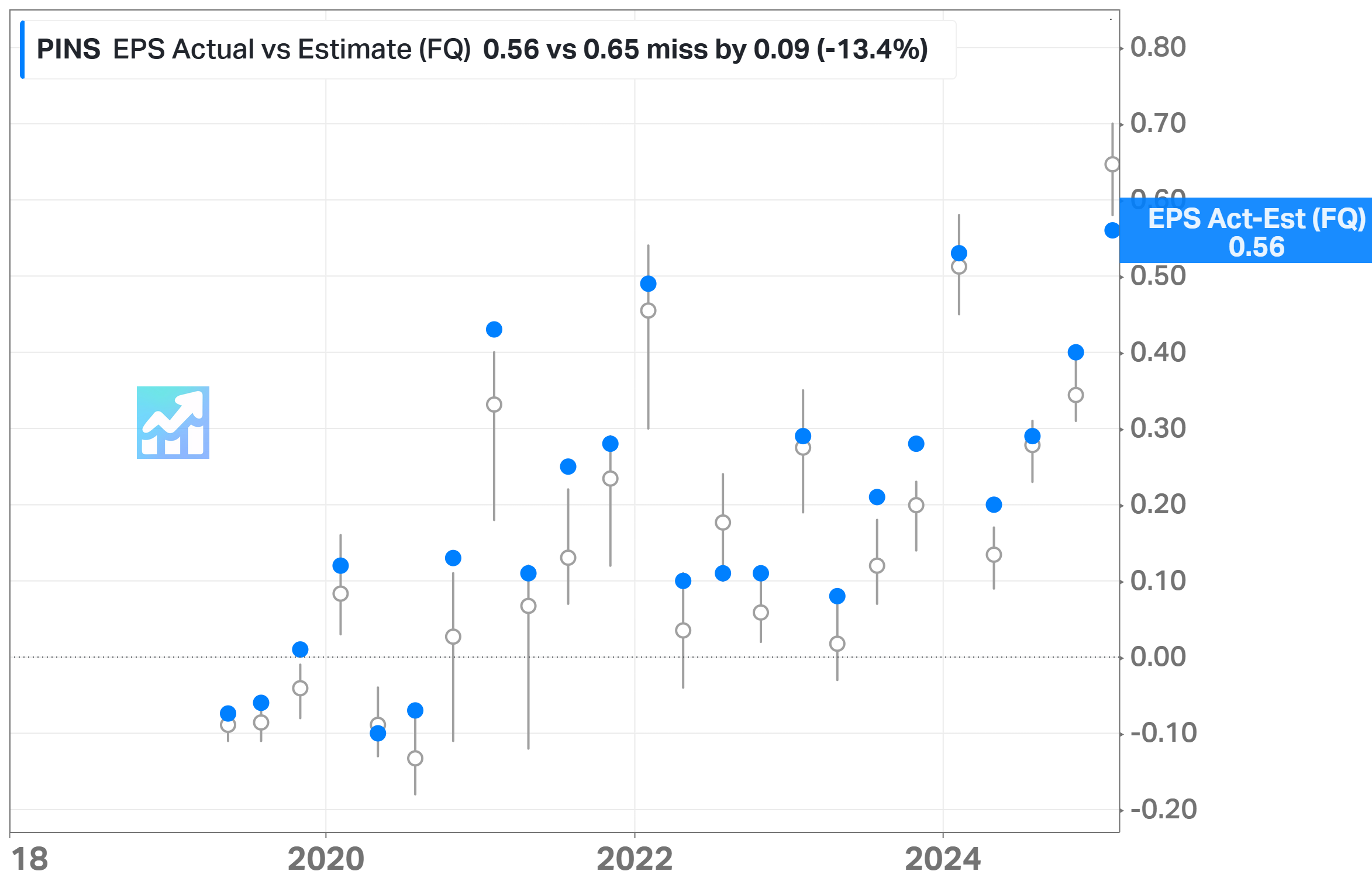

🟢 Pinterest (PINS)

📝 Analyst Notes

My previous fair price was $43. After changes, the new fair price has become $52 (higher). The future 5-year EPS growth rate is 28%, but my maximum is 20%.

🏷️ Updated Valuation

Latest earnings report (Feb 6, 2025):

👍 Positive Points

Pinterest achieved record high global users, surpassing 550 million MAUs globally, with significant growth in the U.S. and Canada.

The company reported its first $1 billion revenue quarter in Q4 2024, with an 18% revenue growth year-over-year.

PINS delivered over $1 billion in adjusted EBITDA, marking a roughly 50% increase, showcasing profitable growth.

The company successfully integrated AI into its platform, enhancing user experience and advertising performance, leading to a 90% increase in clicks to advertisers.

PINS achieved GAAP profitability on a net income basis for the first time since 2021, highlighting financial stability.

👎 Negative Points

The food and beverage subsector of CPG experienced softness, impacting overall growth, and the headwind is not fully behind the company.

Ad pricing declined by 18% year-over-year due to increased ad impression growth and a mix shift in the auction.

Despite strong growth, the company faces challenges in further improving the DAU to MAU ratio, particularly in mature markets.

The company does not accept political advertising, which limits potential revenue growth during election-related spending periods.

While third-party partnerships have been beneficial, the need for such demand is reduced as first-party business grows, potentially limiting future revenue streams from these partnerships.

💲Current Valuation

📈 Price Forecast

↗️ Sales and EPS Forecast

⏺️ EPS Actual vs. Estimate

📈 5Y Performance

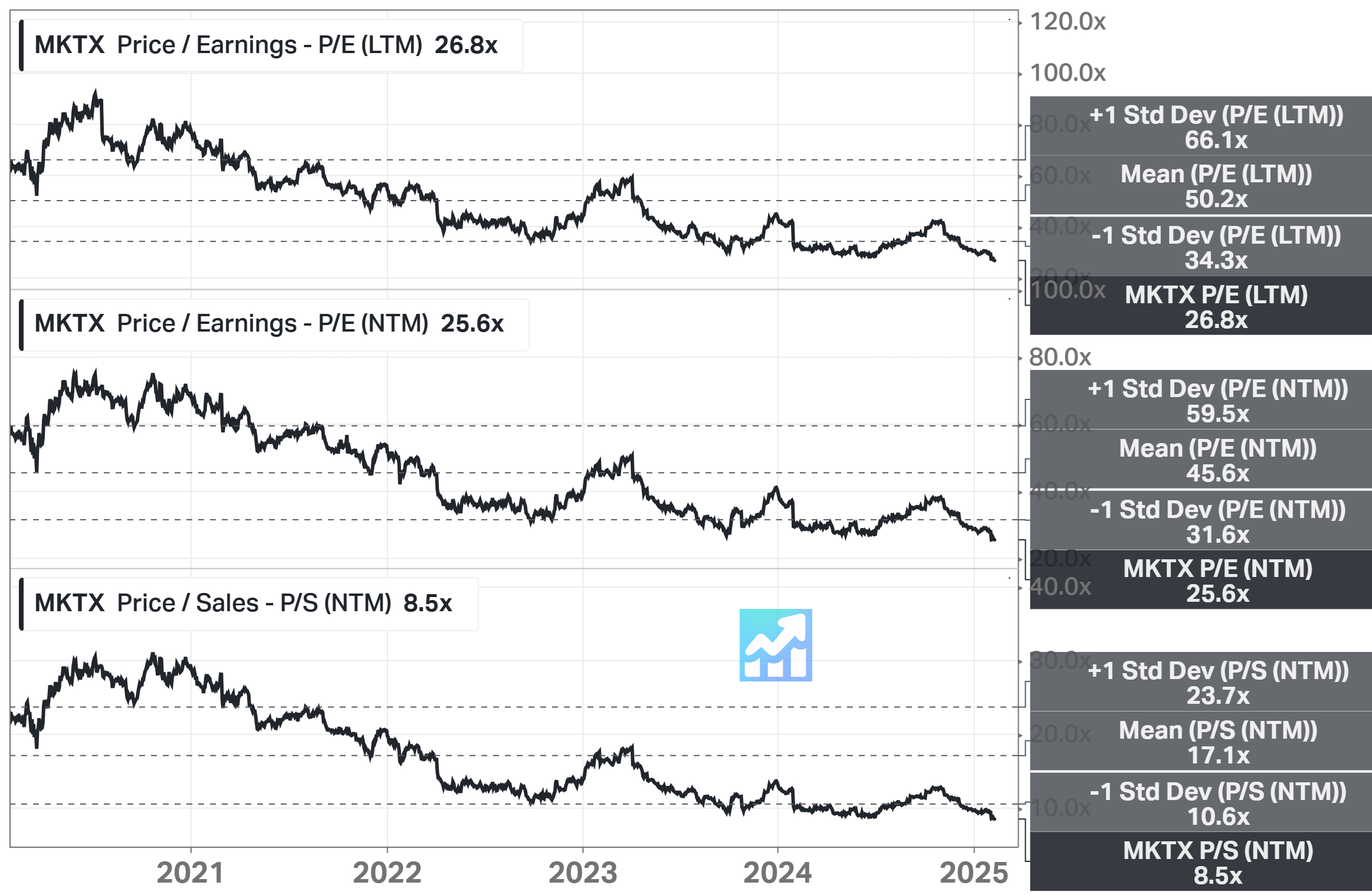

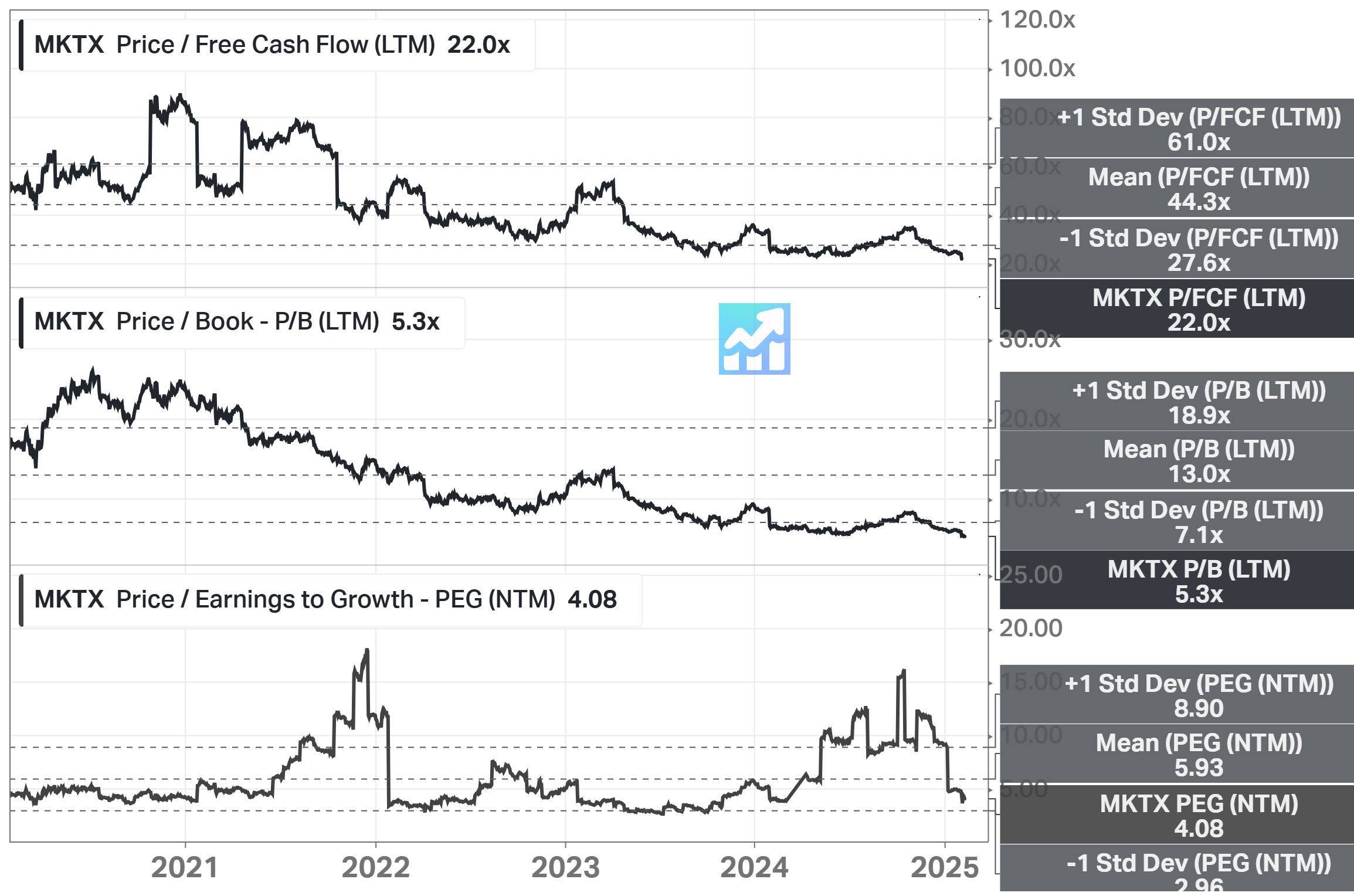

🔵 MarketAxess (MKTX)

📝 Analyst Notes

My previous fair price was $200. After changes, the new fair price has become $191 (lower). I’ve increased the future EPS growth rate but decreased the future exit P/E for all the cases (Base, Bull, and Bear). The PEG ratio is very high.

🏷️ Updated Valuation

Latest earnings report (Feb 6, 2025):

👍 Positive Points

MarketAxess Holdings reported a 9% growth in revenue for 2024, marking the strongest annual revenue growth rate since 2020.

The company achieved record commission revenue and record services revenue, with significant growth in portfolio trading and block trading.

MKTX launched a block trading solution in emerging markets and Eurobonds, with plans to expand to US credit in 2025.

The Rates business saw substantial growth, with trading ADV increasing from $2.9 billion per day in Q1 2024 to $11.4 billion in Q4 2024.

The company is focused on expanding its market share across client-initiated, portfolio trading, and dealer-initiated channels, with a clear strategy for 2025.

👎 Negative Points

MKTX faced challenges with US credit market share, particularly in high-grade market share, which was disappointing in January.

The company experienced a 19% decline in US high-yield commission revenue, attributed to lower levels of credit spread volatility.

Total other income decreased due to mark-to-market losses on the US treasury portfolio, impacting financial results.

Operating expenses increased by 2% compared to the prior year, driven by higher employee compensation and benefits, tech and communications, and marketing costs.

The company anticipates an 8% growth in total expenses for 2025, which may impact profitability if revenue growth does not keep pace.

💲Current Valuation

📈 Price Forecast

↗️ Sales and EPS Forecast

⏺️ EPS Actual vs. Estimate

📈 5Y Performance

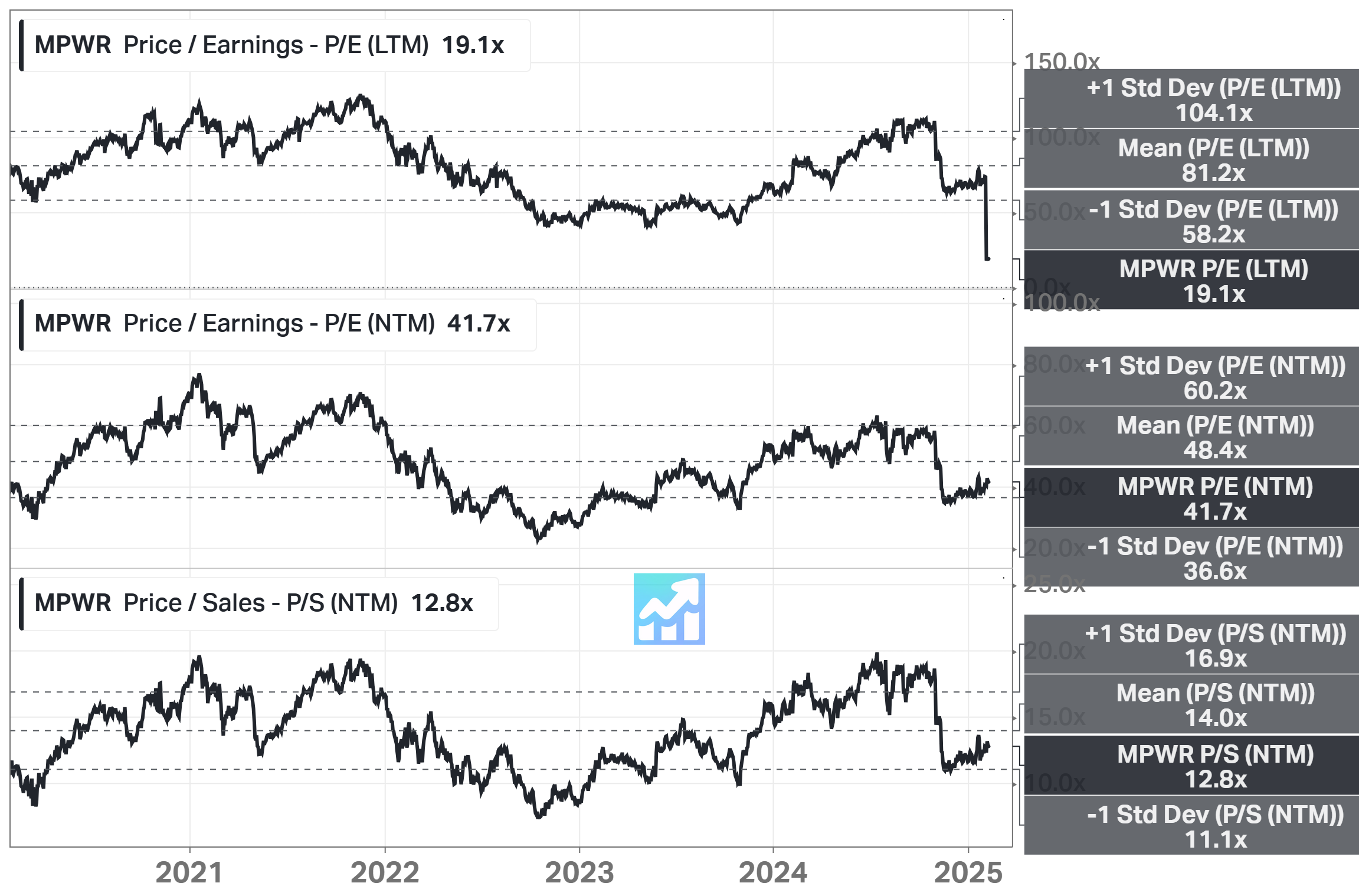

🟢 Monolithic Power Systems (MPWR)

📝 Analyst Notes

My previous fair price was $715. After changes, the new fair price has become $855 (higher). The future 5-year EPS growth rate is a bit more than 24%, but my maximum is 20%.

🏷️ Updated Valuation

Latest earnings report (Feb 6, 2025):

👍 Positive Points

Monolithic Power Systems achieved its 13th consecutive year of growth, with full-year revenue reaching $2.2 billion, a 21% increase from 2023.

The company reported record quarterly revenue of $621.7 million for Q4 2024, marking a 37% increase compared to Q4 2023.

MPS introduced innovative products such as the silicon carbide inverter for high-powered clean energy applications and a family of automotive audio products utilizing DSP technology.

The company announced a 25% increase in its quarterly dividend to $1.56 per share and completed share repurchases under a $640 million authorization.

MPS continues to focus on innovation and diversification, investing in new technology and expanding into new markets to capture future growth opportunities.

👎 Negative Points

The enterprise data segment is expected to have a flattish year, with growth weighted towards the second half of 2025.

There is uncertainty regarding the timing of product ramps, particularly in the automotive and communications sectors, which could affect revenue projections.

The company faces challenges in predicting the exact timing and magnitude of revenue from hyperscale projects due to customer launch delays.

MPS has limited visibility into the separation of CPU and GPU market dynamics, making it difficult to offer precise commentary on enterprise data components.

The company acknowledges the volatility in the AI side of enterprise data, which could impact revenue patterns throughout 2025.

💲Current Valuation

📈 Price Forecast

↗️ Sales and EPS Forecast

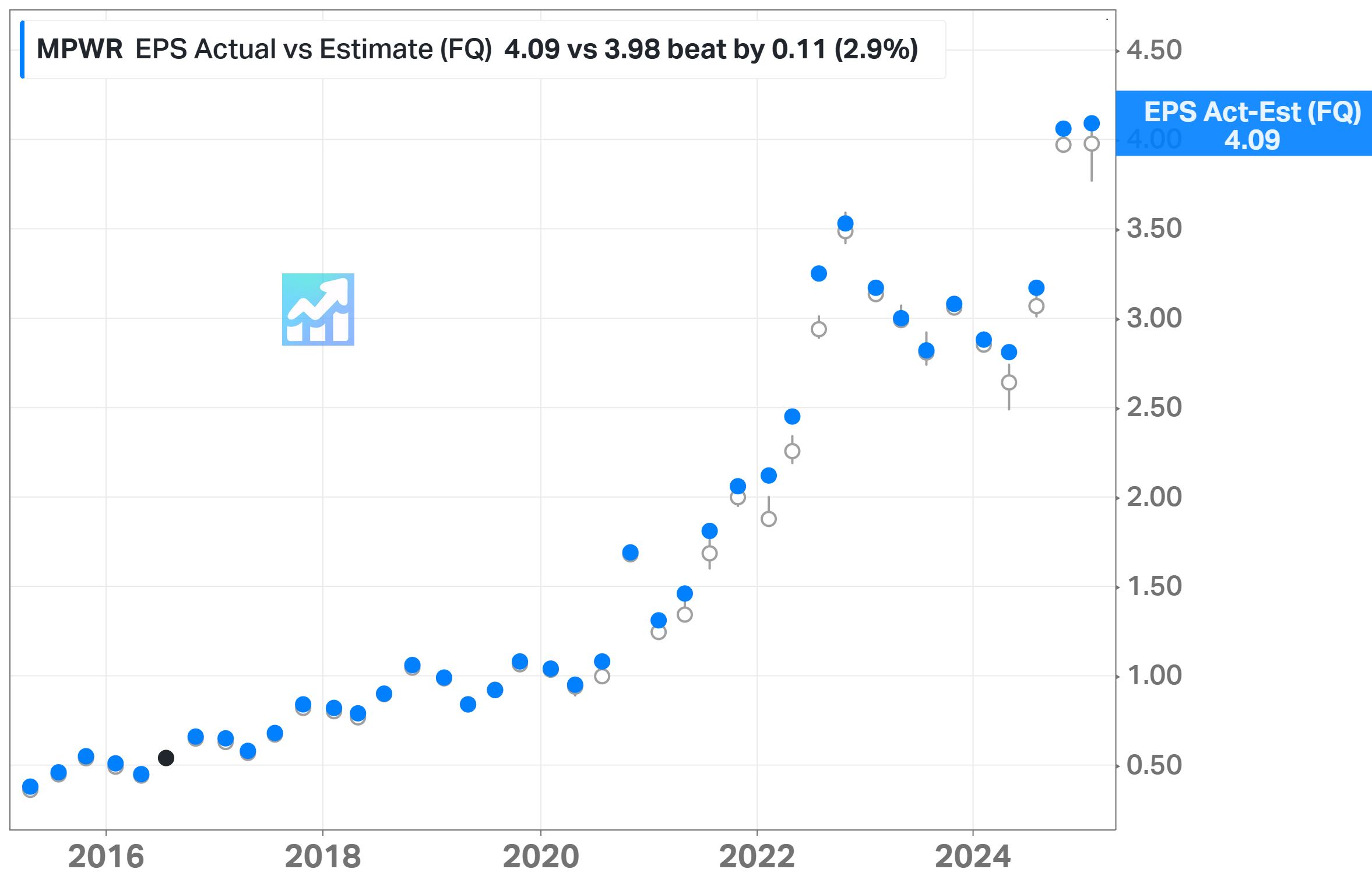

⏺️ EPS Actual vs. Estimate

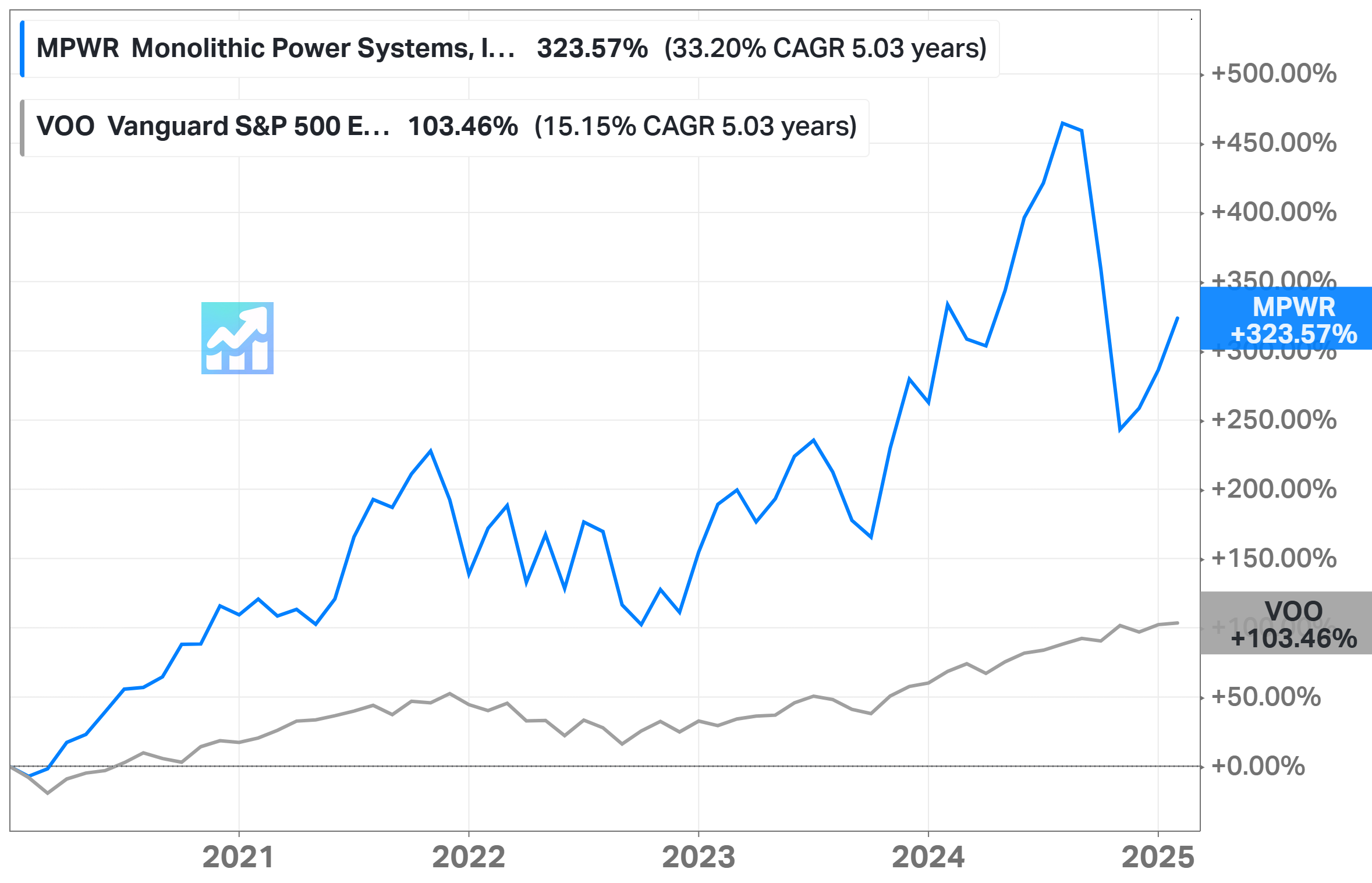

📈 5Y Performance

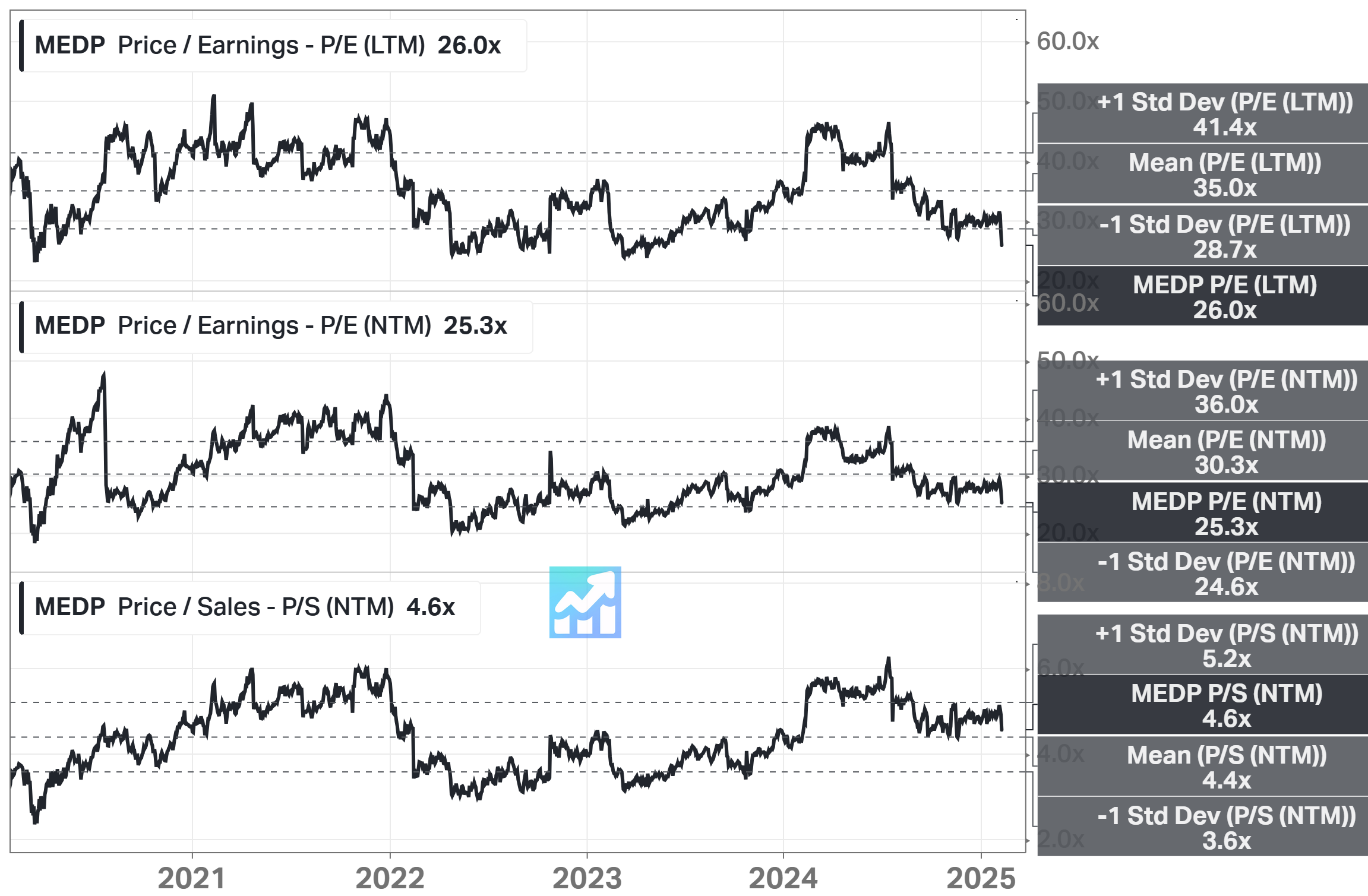

🟢 Medpace (MEDP)

📝 Analyst Notes

My previous fair price was $380. After changes, the new fair price has become $370 (lower). I’ve decreased the future exit P/E for all the cases (Base, Bull, and Bear).

🏷️ Updated Valuation

Latest earnings report (Feb 10, 2025):

👍 Positive Points

Medpace Holdings reported a 7.7% year-over-year increase in revenue for Q4 2024, reaching $536.6 million.

Full-year 2024 revenue grew by 11.8% compared to 2023, totaling $2.11 billion.

EBITDA for Q4 2024 increased by 39.3% year-over-year, reaching $133.5 million, with a margin improvement of 24.9%.

Net income for Q4 2024 rose by 49.5% compared to the previous year, amounting to $117 million.

The company has a strong cash position with $669.4 million in cash as of December 31, 2024, and generated $190.7 million in cash flow from operating activities in Q4 2024.

👎 Negative Points

The book-to-bill ratio for Q4 2024 was 0.99, indicating a slight decline in new business awards.

Net new business awards for the full year 2024 decreased by 5.4% compared to the previous year.

The business environment showed signs of weakening in Q4 2024, with a slight decrease in RFPs compared to Q3.

Guidance for 2025 indicates flat to low single-digit revenue growth, reflecting challenges in the business environment.

Elevated cancellation rates in 2024 have impacted the backlog and may continue to affect bookings in the first half of 2025.

💲Current Valuation

📈 Price Forecast

↗️ Sales and EPS Forecast

⏺️ EPS Actual vs. Estimate

📈 5Y Performance

This is not a financial or investing recommendation. It is solely for educational purposes.

Medpace's employees do not seem to be happy. Check out reddit /r/clinicalresearch and glassdoor. Any idea on this?

Fortinet’s PEG ratio is 1.2. I’m not sure where 3+ came from but that would require a very high PE near Palantir’s levels. Fortinet’s PE is in the 40s.