The Most Undervalued Social Media Stock. PINS Stock Analysis

A comprehensive analysis of Pinterest, a unique visual discovery platform bridging social media and e-commerce currently undervalued by 46.73%.

Changelog:

Feb 12, 2025: Updated fair price valuation: $52.

Jan 24, 2025: Overview: Trend Predictions for 2025.

Nov 19, 2024: Updated fair price valuation: $42.92.

With 522 million monthly active users and a growing advertiser base, Pinterest offers a distinctive value proposition in the digital advertising landscape. Despite recent underperformance, the company shows strong growth projections and improving profitability. The focus on enhancing its ad platform and expanding e-commerce capabilities positions it for potential long-term success.

Content:

💡 Investment Thesis

🧐 Company Overview

🏰 Economic Moat

🚀 Business Strategy

💰 Profit Drivers

✅ Advantages

❌ Disadvantages

🏛️ Capital Allocation

🥇 Competitors

💲Current Valuation

📊 Last Earnings Report

🚀 Future of Social Media

🏷️ Fair Price

☑️ Checklist

💡 Investment Thesis

Pinterest (PINS) presents an attractive investment in the digital advertising sector. As a unique visual discovery platform with 522 million monthly active users, Pinterest bridges social media and e-commerce, driving growth and improving monetization.

The company's focus on enhancing advertising, expanding e-commerce, and international growth, coupled with strategic partnerships (e.g., Amazon), positions it well for future expansion. Strong financial performance (Q2 2024 revenues up 21% YoY) and debt-free balance sheet demonstrate financial strength.

🧐 Company Overview

Pinterest, founded in 2008 and headquartered in San Francisco, has established itself as a unique player in the digital landscape. The platform serves as a visual discovery engine where users, known as Pinners, can explore and save visual recommendations (Pins) based on their personal interests. These Pins can be organized into collections called Boards, creating a personalized space for inspiration and ideas.

As of June 30, 2024, Pinterest boasted a global monthly active user (MAU) base of 522 million, with a significant portion being female users. The platform's appeal spans various categories, including home decor, fashion, recipes, travel, and more, making it a versatile tool for both casual browsing and intentional shopping.

To Read: Pinterest's Newsroom

Pinterest generates revenue primarily through digital advertising on its website and mobile application. The company offers various ad formats, including cost per click (CPC), cost per thousand impressions (CPM), and cost per view (CPV) for video ads. In the second quarter of 2024, Pinterest reported revenues of $853.7 million, with the average revenue per user in the United States and Canada reaching $6.85.

The company has undergone recent leadership changes, with co-founder Benjamin Silbermann transitioning to executive chair in June 2022. Bill Ready, formerly of Google's commerce and payments operations, took over as CEO, signalling a stronger focus on enhancing Pinterest's commerce capabilities.

To Read: Pinterest has a new CEO, who has one job: to build the internet’s shopping mall

🏰 Economic Moat

PINS has established a narrow economic moat, primarily anchored in its intangible brand asset and the network effect among its users. The company's unique positioning as an idea discovery platform sets it apart from traditional social media and e-commerce sites, creating a valuable niche in the digital advertising landscape.

The platform's network effect is evident in its consistent user growth and increasing average revenue per user. As more users join Pinterest and contribute content, the platform becomes more valuable to both existing and new users, creating a virtuous cycle. This network effect is further enhanced by Pinterest's Taste Graph, a sophisticated data analysis tool that helps the company and advertisers better understand user interests and preferences.

Pinterest's economic moat is reinforced by its high control over the sales process. The company primarily sells its advertising products through direct channels, allowing for greater control over pricing, ad inventory, and campaign management. This direct-to-advertiser model contributes to Pinterest's ability to maintain premium pricing and generate attractive returns on invested capital.

The platform's unique value proposition lies in its ability to capture users at various stages of the purchase journey, from initial inspiration to final decision. Unlike search engines or e-commerce sites where users often have a specific item in mind, Pinterest provides discovery, presenting advertisers with an audience that is open to new ideas and products. This positioning has allowed Pinterest to build a distinct space in the digital advertising market, attracting a diverse range of advertisers from consumer discretionary brands to emerging verticals like financial services and technology.

However, it's important to note that while Pinterest's moat is notable, it faces intense competition from larger players in the digital advertising space. The company's ability to maintain and widen its moat will depend on its continued innovation in ad products, enhancement of user experience, and expansion of its user base, particularly in international markets.

🚀 Business Strategy

Pinterest's business strategy centers around three key pillars: enhancing its advertising platform, expanding e-commerce capabilities, and driving international growth. The company is leveraging its unique position in the digital advertising market to capitalize on the growing demand for visual discovery and inspiration-driven shopping.

In terms of advertising, Pinterest is continuously working to improve its ad targeting capabilities and expand its suite of ad products. The company leverages its Taste Graph to provide advertisers with valuable insights into user interests and behaviors, enabling more effective and personalized ad targeting. Pinterest has been introducing innovative ad formats, such as Product Pins, which contain real-time pricing and availability information, making it easier for users to move from inspiration to purchase.

The company is placing significant emphasis on enhancing its e-commerce features. Under the leadership of CEO Bill Ready, Pinterest is making more aggressive investments in commerce capabilities. This includes features like Shop the Look and visual search tool Lens, which make it easier for users to find and purchase products they discover on the platform. The company's partnership with Amazon, announced in 2023, is a significant step in this direction, potentially opening up new revenue streams and enhancing the shopping experience for users.

To Read: Pinterest announces partnership with Amazon to bring third-party ad demand to the platform

International expansion forms the third pillar of Pinterest's strategy. With only 20% of its users residing in the US and Canada but accounting for 80% of revenue in 2023, Pinterest sees significant potential for growth in overseas markets. The company is particularly focused on building its brand and expanding its user base in Europe and other international markets. This expansion strategy includes not only growing the user base but also improving monetization of international users, who currently generate significantly less revenue per user compared to North American users.

Pinterest is investing heavily in research and development, with R&D expenses accounting for 35% of revenue in 2023. This investment is focused on enhancing the platform's technology infrastructure, improving its recommendation algorithms, and developing new features to keep users engaged and attract advertisers. The company is also emphasizing the incorporation of advanced AI-integrated tools to support user engagement and ad effectiveness.

The strategy also includes a focus on video content, which continues to grow on the platform. Pinterest believes that video content will attract both direct-response and brand advertisers, likely at higher ad rates, contributing to revenue growth and increased user engagement.

💰 Profit Drivers

The company's unique position as an intent-driven discovery platform sets it apart in the digital advertising landscape and forms the foundation of its profit generation

One of the primary profit drivers for Pinterest is its ability to attract and retain a large, engaged user base. With 522 million monthly active users as of June 30, 2024, Pinterest provides advertisers with access to a significant audience. More importantly, these users often come to the platform with the intention of discovering products or ideas, making them particularly valuable to advertisers. This intent-driven user behavior translates into higher engagement rates and potentially better conversion rates for advertisers, allowing Pinterest to control premium advertising rates.

By analyzing user behavior and preferences, Pinterest can deliver more relevant ads, which in turn leads to better performance for advertisers and higher ad rates for Pinterest. Innovative ad formats, such as Product Pins and Promoted Pins, further enhance its ability to monetize user engagement effectively.

Expansion into e-commerce functionality represents a significant opportunity for profit growth. By making it easier for users to purchase products they discover on the platform, Pinterest can potentially capture a share of transaction revenue or set higher advertising rates from merchants who see direct sales results from their Pinterest presence.

The acquisition of the AI-powered fashion-shopping platform, The Yes, has enabled Pinterest to create a strategic organization to help steer the evolution of its features and enhance the shopping experience for users.

International expansion is another key profit driver for Pinterest. While international users currently generate significantly less revenue per user compared to North American users, this presents a substantial opportunity for growth. As Pinterest improves its ability to monetize international users and expands into new markets, it has the potential to significantly increase its revenue and profitability.

Pinterest's focus on video content is expected to drive profitability in the coming years. Video ads typically set higher rates than static ads, and the increasing prevalence of video content on the platform could lead to increased user engagement and higher ad revenue.

Lastly, Pinterest's operating leverage is a significant factor in its profit potential. As the company grows its revenue, it has the opportunity to improve its operating margins. The company expects operating margin expansion to reach 22% by 2028, up from an operating loss in 2023, driven by revenue growth outpacing increases in operating expenses.

✅ Advantages

One of Pinterest's primary advantages is its distinct positioning as an idea discovery platform. Unlike traditional social media platforms focused on personal connections and content sharing, Pinterest serves as a visual discovery engine where users actively seek inspiration, ideas, and products. This intent-driven user behavior makes the platform particularly attractive to advertisers, as users are often in a mindset conducive to considering and potentially purchasing products.

Strong brand recognition and a loyal user base provide a solid foundation for growth. Pinterest has successfully got a niche in the market, becoming synonymous with visual idea discovery. This brand strength allows Pinterest to maintain premium pricing for its advertising products and attract both users and advertisers to its platform.

Pinterest's user demographics represent another significant advantage. With approximately two-thirds of its user base being female, Pinterest provides advertisers with access to a valuable and often hard-to-reach audience. This demographic strength is particularly appealing to advertisers in categories such as fashion, home decor, and lifestyle products. Additionally, Pinterest is observing solid traction among Gen Z users, who account for more than 40% of the users and represent one of the fastest-growing demographics on the platform.

To Read: It’s a Gen Z world. Here’s how brands can thrive in it

The company's innovative approach to advertising products sets it apart from competitors. Features like Product Pins, Shop the Look, and visual search tool Lens provide unique ways for advertisers to reach consumers and for users to discover and purchase products seamlessly. These innovations help Pinterest maintain its competitive edge and justify premium advertising rates.

The direct-to-advertiser sales model gives it greater control over its advertising inventory and pricing. This model allows Pinterest to maintain higher margins compared to platforms that rely more heavily on programmatic advertising, contributing to its financial performance.

The platform's international growth potential represents a significant advantage. With only 20% of its users residing in the US and Canada but accounting for 80% of revenue in 2023, Pinterest has substantial room for growth in overseas markets. As the company improves its ability to monetize international users, it has the potential to significantly increase its revenue and profitability.

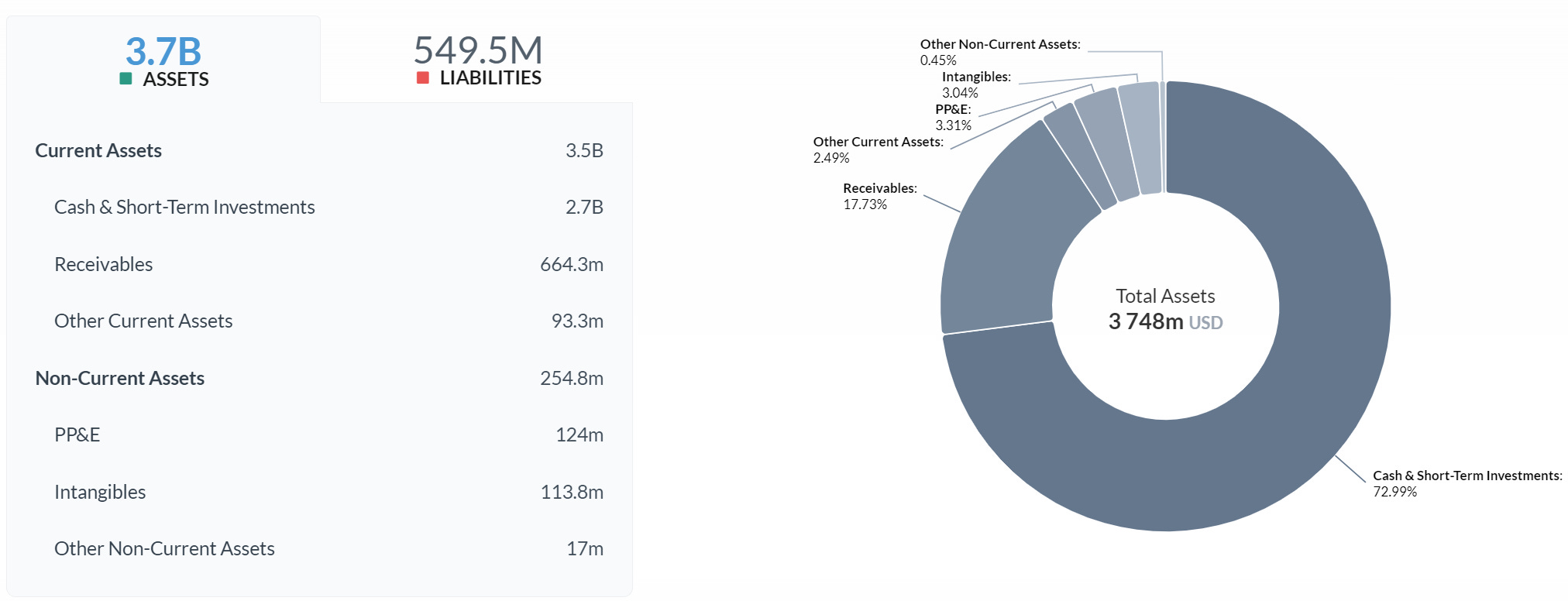

Lastly, Pinterest's strong balance sheet and cash flow generation provide financial flexibility to invest in growth initiatives and navigate potential market challenges. As of June 30, 2024, Pinterest had cash and cash equivalents of $1.38 billion, with $151.7 million of operating lease liabilities. The company generated $462.6 million of cash from operations for the six months that ended on June 30, 2024, up from $246.2 million in the prior-year period.

❌ Disadvantages

One of the primary challenges Pinterest faces is intense competition in the digital advertising market. It competes for advertising dollars with tech giants like Google, Facebook, and Amazon, which have significantly larger user bases and more extensive advertising ecosystems. These competitors have greater financial resources and data capabilities, which could potentially limit Pinterest's ability to capture market share in the digital advertising space.

Pinterest's revenue concentration in North America presents both an opportunity and a risk. While the company has significant potential for international growth, its current reliance on the US and Canadian markets for 80% of its revenue makes it vulnerable to economic downturns or regulatory changes in these regions. The challenge of effectively monetizing international users, who currently generate significantly less revenue per user, remains a hurdle for the company's global expansion plans.

The platform's demographic skew, while advantageous in some respects, could also be seen as a limitation. With approximately two-thirds of its user base being female, Pinterest may face challenges in attracting a broader advertiser base that seeks to reach a more diverse audience. Expanding its appeal to male users without alienating its core female audience could prove to be a delicate balancing act.

Pinterest's focus on visual discovery and inspiration could potentially limit its use cases compared to more versatile social media platforms. While this specialization is a strength in many ways, it could also make Pinterest more vulnerable to shifts in user behavior or the emergence of new platforms that offer similar services.

The company's dual-class share structure, with a 20-1 voting ratio between Class B and Class A common stock, limits the voice of minority shareholders. This governance structure could potentially lead to decisions that are not in the best interest of all shareholders and may deter some investors.

Pinterest's reliance on stock-based compensation to attract and retain talent could be a disadvantage in a competitive labor market, particularly if the company's stock price underperforms. In 2023, the company issued nearly $650 million in stock-based compensation to employees. A prolonged period of weak stock performance could force the company to shift more compensation to cash, potentially impacting its financial flexibility.

Pinterest anticipates operating expenses to increase substantially in the near term for expanding operations domestically and internationally, enhancing product offerings, broadening its user and advertiser base, expanding marketing channels, hiring additional employees, and developing technology. These efforts may prove more expensive than currently anticipated and are likely to weigh on the company's top-line growth in the near term.

Lastly, as a platform for content sharing, Pinterest faces ongoing challenges related to content moderation and the potential spread of misinformation. The company has implemented policies to control health misinformation and other harmful content, but managing these issues while maintaining an open platform for idea sharing remains an ongoing challenge.

🏛️ Capital Allocation

Pinterest's capital allocation strategy reflects a focus on reinvesting in the business to drive growth and enhance its competitive position. The company's approach prioritizes investments in research and development, platform enhancements, and international expansion over acquisitions or significant shareholder returns.

Research and development (R&D) represents a significant area of investment for Pinterest. In 2023, the company allocated 35% of its revenue to R&D expenses. This substantial investment demonstrates Pinterest's commitment to innovation and continuous improvement of its platform. The focus of these R&D efforts includes enhancing the company's advertising technology, improving its recommendation algorithms, developing new features to increase user engagement, and expanding its e-commerce capabilities.

Pinterest's capital expenditures have been relatively modest compared to its cash flow generation. Over the past decade, the company has generated an annual average of about $540 million in free cash flow to the firm while spending approximately $300 million per year on capital expenditures. These investments have primarily been directed towards expanding and improving the company's technology infrastructure to support user growth and enhance platform performance.

In terms of acquisitions, Pinterest has maintained a conservative approach. The company has not made any material acquisitions in recent years, with less than $125 million spent on two transactions over the past five years. This strategy suggests that Pinterest prefers organic growth and internal development over growth through acquisitions. However, the acquisition of the AI-powered fashion-shopping platform, The Yes, represents a strategic move to enhance its e-commerce capabilities.

Regarding shareholder returns, Pinterest has focused on share repurchases rather than dividends. The company repurchased $500 million in shares in 2023 under a buyback program and another $335 million to satisfy tax withholdings on employee stock awards. In September 2023, the board of directors authorized another $1 billion share-buyback program, which was still available at the end of 2023. These share repurchases demonstrate the company's confidence in its long-term prospects and its commitment to returning value to shareholders.

Pinterest's strong balance sheet provides financial flexibility for its capital allocation strategy. As of the end of the first quarter of 2024, the company had $2.8 billion of cash on hand and no debt outstanding. This robust financial position allows Pinterest to invest in growth initiatives, weather potential market challenges, and pursue strategic opportunities as they arise.

The effectiveness of Pinterest's capital allocation strategy is reflected in its high returns on invested capital. The company has maintained impressive adjusted ROICs including goodwill, averaging 44% over the past five years. This demonstrates the ability to generate substantial value from its investments and supports the company's focus on organic growth and internal development.

🥇 Competitors

Pinterest operates in a highly competitive digital advertising and social media landscape, facing competition from various players with different strengths and market positions.

Key competitors include:

Snap Inc. (SNAP): Snapchat competes with Pinterest for user attention and advertising dollars, particularly among younger demographics.

Match Group (MTCH): While primarily known for its dating apps, Match Group's platforms compete with Pinterest for user engagement time and advertising budgets, particularly in lifestyle and social discovery categories.

Meta Platforms (META): Facebook and Instagram, owned by Meta, represent significant competition for Pinterest. Instagram, in particular, has increasingly moved into the visual discovery and e-commerce space, directly competing with Pinterest's core functionalities. Meta's extensive user base and advanced advertising capabilities pose a substantial challenge.

To Read: Several reasons why Pinterest is better than Facebook

Alphabet (GOOGL): Google, Alphabet's primary subsidiary, competes with Pinterest in several areas. Google's visual search capabilities, shopping features, and vast advertising network make it a competitor in both the discovery and advertising aspects of Pinterest's business.

TikTok: As a rapidly growing video-centric platform, TikTok competes with Pinterest for user attention, particularly among younger audiences. TikTok's increasing focus on e-commerce and its powerful recommendation algorithm presents a significant challenge in the visual discovery space.

Reddit (RDDT): While different in format, Reddit competes with Pinterest in terms of idea sharing and community-driven content. Reddit's diverse range of topics and engaged user base make it a competitor for both user time and advertising dollars.

💲Current Valuation

📈 Past and Future

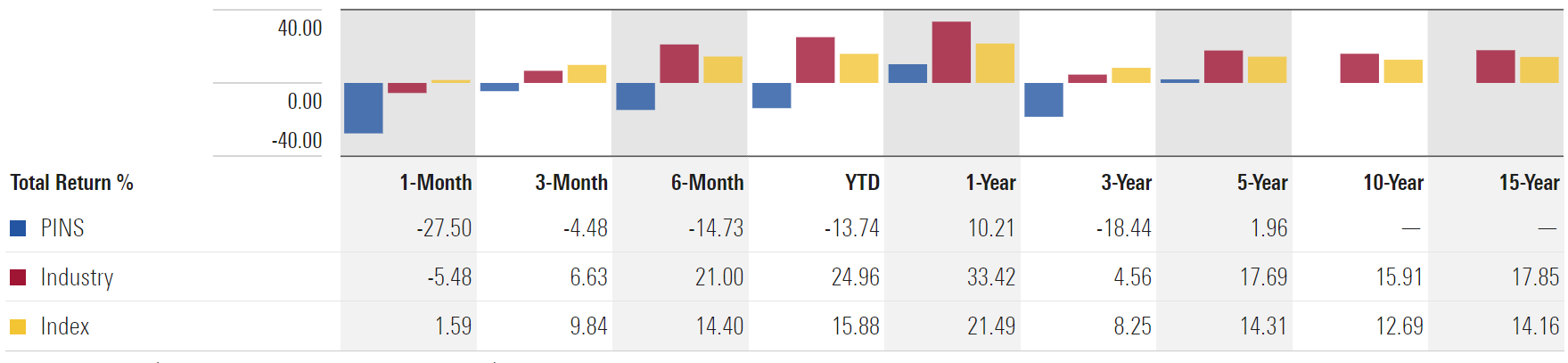

PINS has underperformed both its industry (Internet Content & Information) and the broader index across most timeframes.

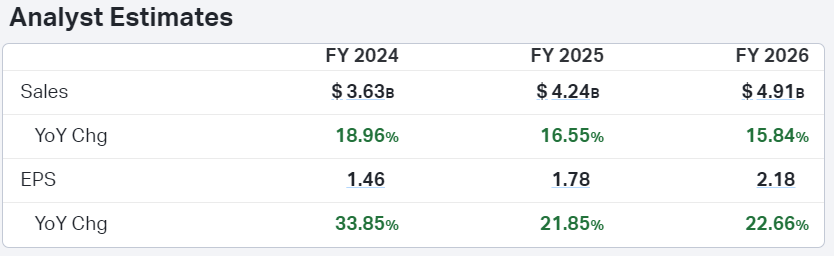

Analyst estimates for PINS project continued strong growth in both sales and earnings through FY 2026. Sales are expected to rise from $3.63B to $4.91B, with growth rates gradually decreasing from 18.96% to 15.84%. EPS is forecasted to increase from $1.46 to $2.18, maintaining robust year-over-year growth above 20%. These projections suggest analysts anticipate sustained financial expansion for Pinterest, despite a slight deceleration in sales growth rate.

Analyst sentiment for PINS is predominantly positive, with 68% recommending a Buy and 32% suggesting a Hold. No analysts advise Selling. The 1-year price forecast shows significant upside potential, with a median target of $43.50 (40.28% increase) and a high estimate of $52.00 (67.69% gain). Even the low estimate of $32.00 represents a slight 3.19% increase from the current price of $31.01. This outlook suggests analysts are optimistic about PINS's near-term prospects.

The broker rating breakdown for PINS demonstrates consistent positive sentiment over the past 3 months. With 30 total ratings unchanged throughout this period, most analysts favor "Strong Buy" or "Buy" recommendations, while a smaller portion maintains "Hold" ratings. Notably absent are any "Sell" or "Strong Sell" recommendations. This stable distribution of ratings suggests sustained analyst confidence in PINS's outlook, regardless of recent market conditions or company developments.

Pinterest shows strong growth rates compared to its industry and the S&P 500. Next year, PINS's growth is projected at 20.28%, slightly below the industry's 23.70% but still above the S&P 500's 11.34%. Looking ahead, PINS is expected to maintain robust growth over the next 5 years at 22.80%, outpacing the industry's 20.00% projection.

📊 Last Earnings Report

Pinterest reported strong second-quarter 2024 results. The company's performance was driven by strong user growth across all regions and improvements in its advertising platform.

To Read: Latest quarterly report

User Growth: Global monthly active users (MAUs) grew 12% year-over-year to 522 million. The United States and Canada saw a 3% increase to 98 million MAUs, while the Rest of the World segment grew 17% to 288 million MAUs.

Average Revenue Per User (ARPU): Global ARPU stood at $1.64, up from $1.53 in the year-ago quarter. ARPU in the United States and Canada rose 16% to $6.85, while Europe improved 14% to $1.03.

Regional Performance: The United States and Canada generated $673 million in revenues, up 19% year over year. Europe totalled $143 million, up 25%, and the Rest of the World rose to $38 million from $29 million.

Cash Flow: For the first six months of 2024, Pinterest generated $462.6 million of cash from operating activities, up from $246.2 million in the prior-year period.

The company's performance was driven by several factors, including strong momentum in retail and emerging verticals like financial services and technology. Pinterest also noted healthy traction among Gen Z users, who now account for more than 40% of the platform's users.

Looking ahead, Pinterest provided guidance for the third quarter of 2024, expecting revenues in the range of $885-900 million, indicating 16-18% year-over-year growth. Non-GAAP operating expenses are projected in the range of $485-500 million, indicating 17-20% growth year over year.

🚀 Future of Social Media

To Read: The Future of Social Media [Research]: What Marketers Need to Know

A striking trend is the rise of short-form video content. According to a HubSpot survey conducted in January 2023, 33% of social media marketers planned to invest most heavily in short-form videos, such as those on TikTok, in 2023.

This represents a significant focus, outpacing other content types like long-form videos (11%), live audio chat rooms (10%), and even emerging technologies like VR or AR (9%). The popularity of short-form videos underscores the changing consumption habits of social media users and the need for brands to adapt their content strategies accordingly.

Another crucial development is the projected overtaking of TV viewership by social network users in the United States. Data from eMarketer suggests that by 2025, there will be more social network users (235.1 million) than TV viewers (230.0 million) in the US. This shift marks a pivotal moment in media consumption, with social networks becoming the primary channel for audience engagement. The growth trajectory of social network users has been steady since 2008, with significant milestones including Facebook passing 100 million users in 2010, Instagram reaching 100 million users in 2018, and TikTok surpassing 100 million users in 2021.

These trends highlight the increasing importance of social media in marketing strategies and the need for brands to evolve their approaches. The dominance of video content, particularly short-form, on platforms like YouTube, TikTok, and Instagram Reels, requires that brands develop engaging, platform-specific video content to capture audience attention.

The integration of social commerce into social media platforms is a key trend. As more consumers turn to social apps for shopping, brands must optimize their presence for seamless purchasing experiences, blurring the lines between social interaction and e-commerce.

🏷️ Fair Price

➡️ Updated fair price valuation: https://longtermpick.com/p/updated-valuations-nov-24-2

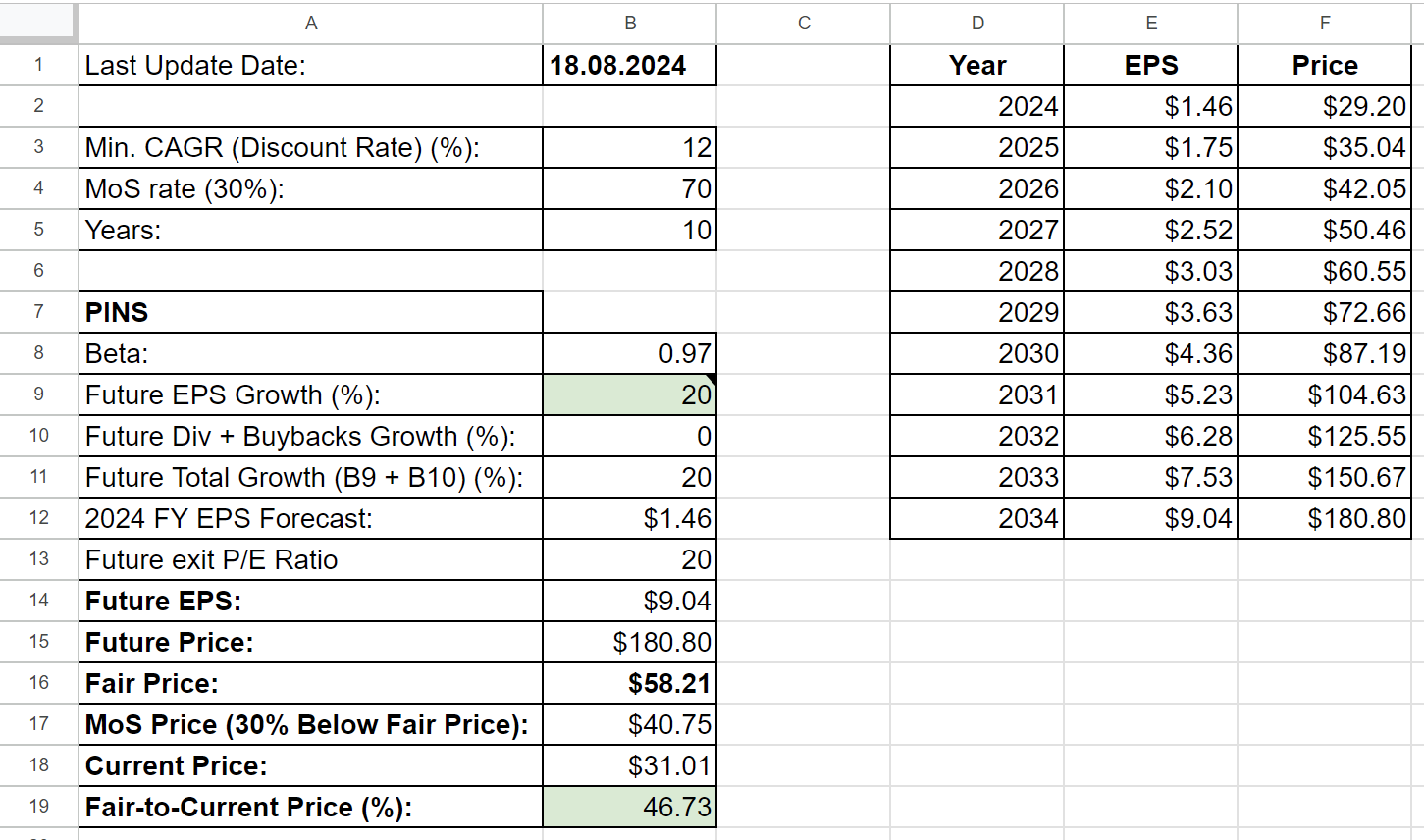

Long-Term Pick Fair Price for PINS is $58.21 which is lower 46.73% than the current price of $31. I used:

Discount Rate: 12% (S&P 500 Next 5-Yr Growth Estimates is 11.64%)

Margin of Safety: 30%

Years: 10

Future EPS Growth Rate: 20% (it's 22% but I don't take anything above 20%, so decreased to 20%)

Future Buyback Yield: 0% (due to combined buybacks and stock-based compensations together)

Total Future Growth Rate: 20 + 0 = 20%

Fair-to-Current Price (%): +46.73% (Undervalued)

☑️ Checklist

Profitability:

✅ Gross margin at least 40%: 78%

❌ Net margin at least 10%: 4.64%

❌ Management (ROIC, ROCE, ROE, ROA): No (All below 10%)

✅ Piotroski F-Score: 8 of 9 (Not passed: Less Shares Outstanding YoY)

✅ Revenue surprises: Yes (Past 5 years)

✅ EPS surprises: Yes (Past 5 years)

❌ EPS growth YoY: No

Valuation and Advantage:

✅ Valuation below its 5-Yr average: Yes

✅ Does it have a moat: Yes (narrow)

Shares:

✅ Insider ownership at least 5%: Yes (10.72%)

❌ Less shares outstanding YoY: No

✅ Insider buys last six months: Yes ($269K - Morningstar)

Price:

✅ 1-year stock price forecast: +40.28%

✅ Next 5-Yr CAGR is above S&P 500: Yes (22% vs 11.64%)

✅ DCF Value: $54.4 (Undervalued 43%; 10 years, the discount rate is 10%, no termination, equity model: FCFE)

✅ Short Interest below 5%: 4.66%

This is not a financial or investing recommendation. It is solely for educational purposes.

Your thoughts?