Monolithic Power Systems: Key Semiconductor Supplier Poised for Growth Across Diverse Markets

A leading fabless semiconductor company specializing in high-performance power management solutions.

Changelog:

Feb 12, 2025: Updated fair price valuation: $855.

Monolithic Power Systems (MPWR) is a leading fabless semiconductor company specializing in high-performance power management solutions. With innovative proprietary technologies like its bipolar-CMOS-DMOS (BCD) process, MPS serves diverse markets including automotive, data centers, and industrial applications. The company partners with major clients such as NVIDIA and collaborates with third-party foundries to maintain cost efficiency and flexibility. MPS has the potential for sustained growth and long-term success as demand for electric vehicles, AI workloads, and advanced power management increases.

Content:

💡 Investment Thesis

❓ Nvidia's New Blackwell GPU Platform

🧐 Company Overview

🏰 Economic Moat

🚀 Business Strategy

🏛️ Capital Allocation

✅ Advantages

❌ Disadvantages

🥇 Competitors

⏮️ Past

📶 Future

💲Current Valuation

🏷️ Fair Price

☑️ Checklist

✍️ Due Diligence

💡 Investment Thesis

Monolithic Power Systems is a high-growth semiconductor company poised to capitalize on the increasing demand for power-efficient solutions across multiple industries. With a focus on analog and mixed-signal integrated circuits, MPS delivers highly differentiated products that have greater efficiency in key applications such as data centers, automotive, industrial automation, and consumer electronics.

Based on my estimate, the company is forecasted to achieve a CAGR of at least 20% through 2030, driven by tailwinds like the transition to electric vehicles, 5G infrastructure expansion, and AI-driven workloads in data centers. Its scalable business model and strong gross margins highlight its ability to generate consistent profitability.

Despite still high ratios, MPS is currently trading below its 5-year average valuations, providing an attractive entry point for investors.

❓ Nvidia's New Blackwell GPU Platform

MPS has lost market share on Nvidia's new Blackwell GPU platform due to performance issues with its voltage regulator modules (VRMs). Nvidia reportedly reduced MPS's allocations, leading to canceled orders and a smaller backlog. Competitors have gained market share as Nvidia placed rush orders with them. This news caused MPS's stock to drop by nearly 20%, while competitors are benefiting from the shift. MPS denies any technical problems but faces growing competition in this space.

CEO Michael Hsing is confident in the continuation of growth for 2025 (last earnings call):

Yes, I can tell very confident, confidently we will be, okay, let's say that. And when this market -- when this AI market turn into like a regular server market, MPS will be a significant player in that. And now this is not -- became a, what do you call it, reach to an equilibrium yet.

(...) yeah, this is still ramping up. And when this segment is ramping -- when you start to ramping, it's kind of lumpy. (...) And next -- and so to answer your question for next year, clearly, so we have a lot more customers as I said earlier, that will start to ramping those designs will turn into -- those designs will turn into revenues.

🧐 Company Overview

Monolithic Power Systems designs and develops high-performance analog and mixed-signal integrated circuits. The company focuses on power management solutions, serving industries like automotive, cloud computing, industrial applications, and consumer electronics. MPS operates as a fabless company, using third-party contractors for manufacturing while installing its proprietary process technologies in their facilities. This model reduces fixed costs and enhances the company’s flexibility to innovate.

Analyst’s comment:

The term “fabless company” refers to a company that designs and markets semiconductors while outsourcing that hardware's fabrication (or fab) to a third-party partner, who produces them in foundries. Read more.

Founded in 1997 and headquartered in Kirkland, Washington, MPS is led by its CEO, Michael Hsing. As co-founder, Hsing has played a key role in driving innovation and growth through a disciplined focus (see the section Capital Allocation) on proprietary technologies and customer-centric strategies. Under his leadership, the company has grown into a leader in power management solutions.

The company’s broad end-market exposure includes computing and storage (23.2% of revenue), automotive (17.9%), enterprise data (29.8%), industrial (7.1%), consumer (10.4%), and communications (11.6%). Monolithic’s major clients include NVIDIA and key players in the automotive and cloud computing sectors. These long-term relationships highlight MPS’s reliability and integration into customer supply chains.

🏰 Economic Moat

MPS has a wide economic moat built on proprietary process technology and strong customer relationships. Its BCD technology (but the technology was invented by STMicroelectronics; STM) combines analog, digital, and memory components into a single chip. This integration results in higher power density, greater efficiency, and smaller chip sizes. With a 55-nanometer process, MPS surpasses competitors who mostly operate at 90 or 110 nanometers, offering customers significant advantages in energy efficiency and space savings.

Switching costs enhance their moat. Customers often embed MPS chips into their systems for up to a decade, especially in markets like automotive and industrial applications. Redesigning a system to switch suppliers can be expensive and time-consuming, which makes customers unwilling to change providers. Additionally, MPS's ability to develop advanced chips at a lower cost, thanks to its fabless model, guarantees strong returns on invested capital. The company’s ROIC has consistently exceeded 20%, even during periods of high investment.

Read also:

🚀 Business Strategy

I would describe their business strategy as innovation and market share expansion. It focuses on organic growth, investing heavily in R&D to improve process efficiency and product capabilities. The company targets high-growth markets such as automotive and data centers. Automotive revenue reached $111.3 million in Q3 2024, driven by demand for advanced driver-assist systems and infotainment solutions. In the data center segment, sales surged 86% year-over-year due to the increasing adoption of AI and cloud computing technologies.

MPS is also building an AI-driven e-commerce platform to enhance customer experiences and expand its market reach. This platform aims to optimize the product selection process for customers, allowing them to input specific needs and receive tailored recommendations. This will help MPS attract small and medium-sized businesses.

To read: 2024 Micron Top Supplier

The company partners with several third-party foundries and contractors, primarily in Asia, for manufacturing. These partnerships allow MPS to maintain a low capital expenditure model while focusing on design and innovation. By collaborating with foundries that utilize older, fully depreciated digital fabs, production can remain cost-effective and meet high standards of quality and efficiency.

Business segments:

Computing and Storage: MPS provides power solutions for computing devices, including desktop PCs, laptops, servers, and storage systems. The focus is on delivering efficient power conversion and management to support high-performance computing needs and energy-efficient data centers.

Automotive: The company supplies advanced power solutions for the automotive market, including power management for electric and hybrid vehicles. MPS focuses on enhancing battery management systems, safety electronics, and advanced driver-assistance systems (ADAS), aligning with the increasing demand for electrification and smart automotive solutions.

Consumer Electronics: MPS develops power solutions for a range of consumer electronics. This includes components for smartphones, tablets, wearables, and smart home devices. The aim is to optimize power usage, enhance battery life, and improve the overall user experience by delivering energy-efficient technology.

Industrial: In the industrial sector, MPS's products are used in applications such as robotics, factory automation, renewable energy systems, and telecommunications infrastructure. The focus here is on robustness, reliability, and energy efficiency, which are essential for long-term industrial operations.

Communications: MPS provides power management solutions for networking and telecommunications equipment. This includes power modules that support the infrastructure for wired and wireless communication networks, ensuring consistent power delivery and minimizing energy consumption.

🏛️ Capital Allocation

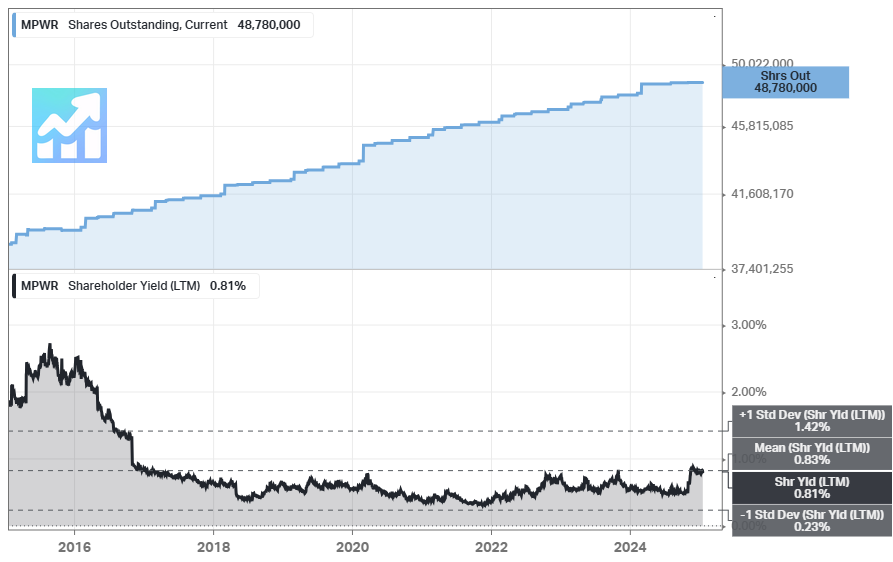

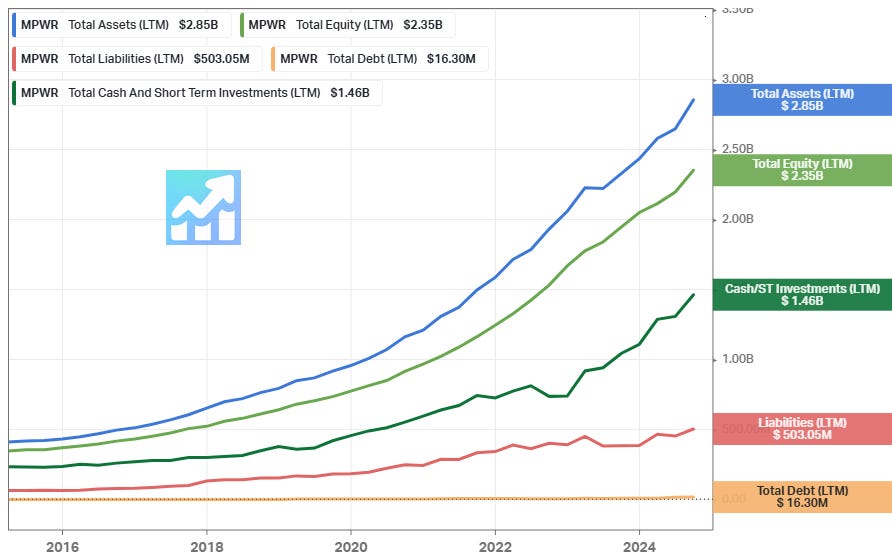

From my perspective, Monolithic Power's capital allocation demonstrates a disciplined approach. The company has no debt and solid operating cash flow. MPS reinvests heavily in research while paying a quarterly dividend, which represents nearly half of its free cash flow (see the chart with dividends above - payout ratio). Thus, the company maintains financial stability while funding growth initiatives. Pay attention to the fact that Monolithic Power has been increasing outstanding shares regularly (see the chart below).

MPS has historically prioritized organic growth over acquisitions. Its proprietary technologies are developed internally. This strategy has contributed to steadily increasing returns on invested capital. Worth noting that MPS has a strong balance sheet, which provides resources to fund future growth initiatives and weather market fluctuations.

✅ Advantages

Their proprietary BCD technology is a significant advantage. The integration of analog, digital, and memory components into a single chip result in higher power density, improved efficiency, and smaller sizes, giving the company a strong competitive advantage.

The company’s fabless model keeps capital requirements low while allowing it to innovate more quickly than competitors. By partnering with third-party contractors, MPS can focus on design and technology development.

The automotive segment presents immense growth opportunities. As electric vehicles and advanced driver-assist systems become more prevalent, MPS products are increasingly in demand: 17.9% contribution to Q3 2024 revenues from this sector.

Diversified end-market exposure. Serving industries like cloud computing, automotive, and industrial applications reduces the risk of overdependence on any single sector.

A strong balance sheet provides financial stability and flexibility. With $1.46 billion in cash/ST investments and no debt, the company is well-positioned to fund R&D and face possible economic uncertainties.

❌ Disadvantages

Reliance on Asia for manufacturing and revenue exposes it to geopolitical risks. The ongoing U.S.-China trade tensions and potential regulatory changes could negatively impact operations and profitability.

Customer concentration is a concern. A significant portion of MPS revenue comes from a limited number of clients, which makes the company vulnerable to losing major customers.

The semiconductor industry’s cyclical nature creates revenue volatility. Fluctuations in demand can lead to uneven financial performance, which is a challenge for long-term planning.

The company operates in a highly competitive market. Larger players like Texas Instruments (TXN) and Analog Devices (ADI) have more resources and broader distribution networks, which could erode MPS's market share over time.

MPS stock's high valuation (see the section Valuation).

🥇 Competitors

Analyst’s comment:

I forgot to include STM in the comparison charts below. MPWR has higher price ratios (trading higher) and higher margins, as well as higher ROIC, ROE, and ROA.

Compared to Texas Instruments (TXN), MPS stands out for its focus on innovation and fabless model. While TXN relies on in-house manufacturing with lagging technology, MPS’s use of advanced 55-nanometer processes allows it to deliver better power density and efficiency.

Analog Devices (ADI) competes with MPS in the analog and mixed-signal chip space. ADI has a larger market capitalization and broader distribution network, but MPS’s proprietary BCD technology gives it an advantage in high-power density applications.

To read: Sales Distributors

STMicroelectronics (STM) offers BCD technology similar to MPS, but its processes are less advanced, operating at 90 or 110 nanometers. MPS’s ability to innovate more rapidly and at a lower cost provides a significant competitive advantage.

Skyworks Solutions (SWKS) focuses heavily on wireless connectivity, which differentiates it from MPS’s power management focus. MPS’s diversified end markets give it an advantage in revenue stability compared to SWKS’ narrower focus.

Power Integrations (POWI) competes in the power management space but focuses on lower-power applications. MPS’s ability to serve high-power and high-growth markets like data centers and automotive sets it apart.

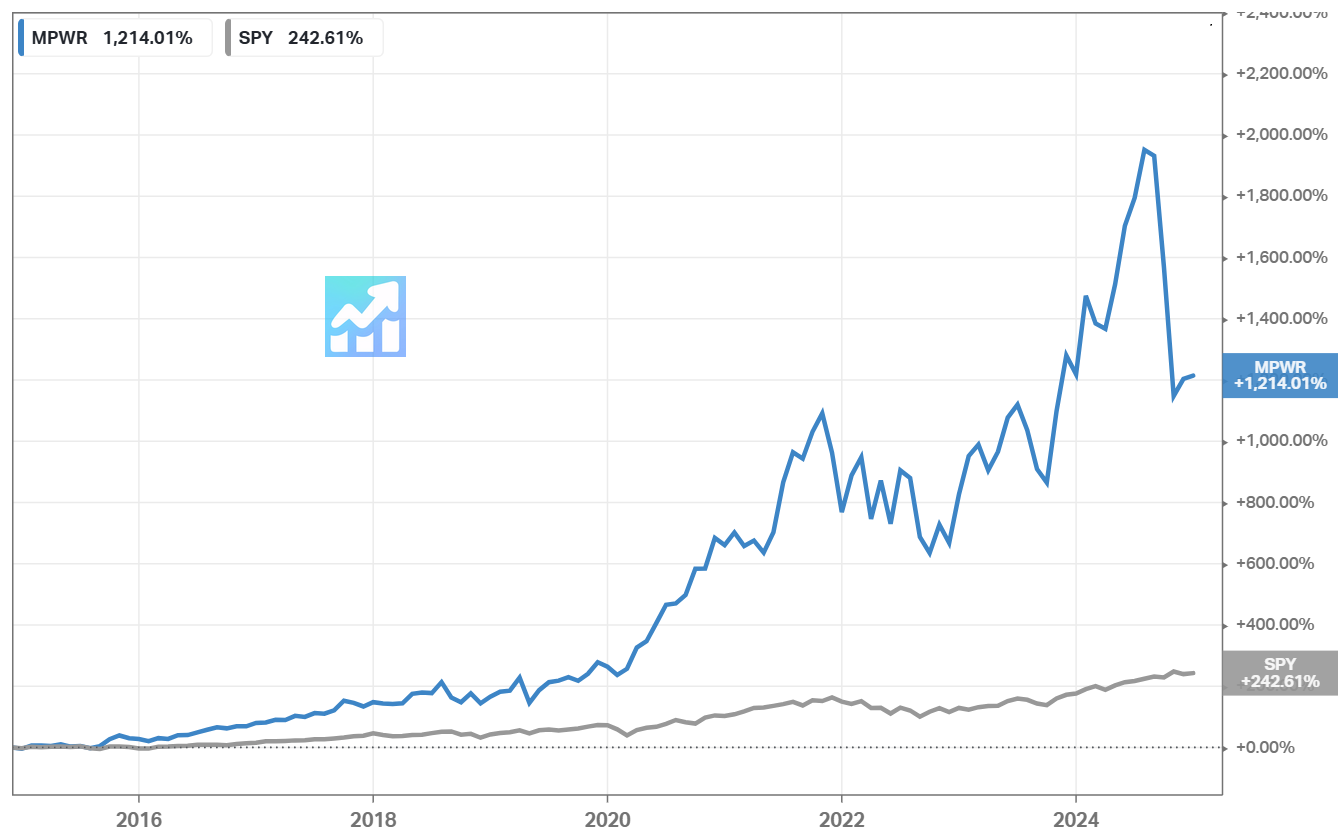

⏮️ Past

Above is the compound annual growth rate (CAGR) for the MPWR stock over 5-year, 10-year, and 15-year time periods. During long-term periods the stock outperforms the S&P 500 significantly.

Above is a comparison of total returns with the S&P 500 (SPY) on a 10-year period.

📶 Future

The automotive segment is expected to grow significantly, driven by advancements in electric vehicle systems and driver-assist technologies. In the data center market, MPS benefits from strong placements alongside GPUs for AI workloads, with both segments contributing to sustained long-term growth.

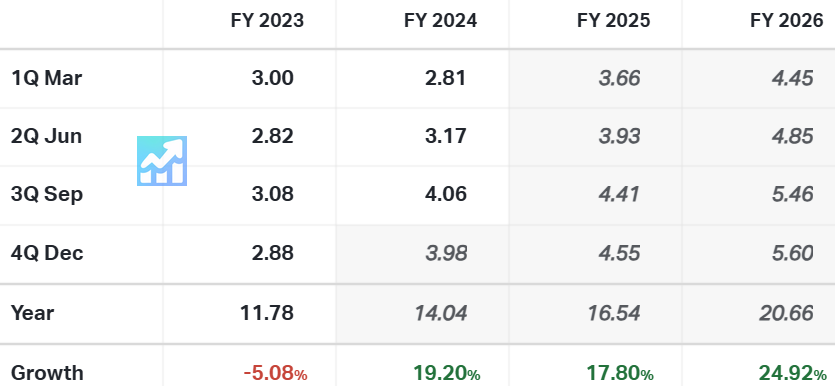

Below is the 3-year forecast for future EPS growth, which is projected to be around 20.60%. This value remains high.

Sales are projected to grow at an 18.83% annual rate until FY 2026.

Based on 1-year price targets offered by other analysts, the average price target for MPWR comes to $817. The forecasts range from a low of $610 to a high of $1,100. The average price target represents an increase of 36.97%.

💲Current Valuation

In terms of Price/Forward Sales, Price/Forward Earnings, and Price/FCF ratios, the company is currently trading below its 5-year average levels. But the values still remain high.

The same is true for Price/Earnings, Price/Book Value, and PEG ratios - below 5-year averages. Worth noting that the current PEG ratio is the lowest for the last five years.

The valuation comparison with the industry is additionally available for patrons only.

🏷️ Fair Price

The Long-Term Pick's Fair Price (Base Case) for MPWR is $715.78. The current price of $625.82 is lower by 12.57%.

Fair-to-Current Price (%): 12.57%

Current Price/Fair Price: 0.87

I used:

Discount Rate: 12%

Margin of Safety: 30%

Years: 5

Future EPS Growth Rate: 20% (I lowered the 3-year EPS forecast since my maximum is 20)

Future Dividend Yield: 0.75% (I used the 5-year average dividend yield)

Total Future Annual Growth Rate: 20 + 0.75 = 20.75%

Reviewing the historical long-term CAGR results (the Past section), my 20.75% CAGR is still below 5-, 10- and 15-year values.

Overall, my estimate may be a bit pessimistic since the market has always estimated the stock with high valuations. 10-year historic Price/Earnings ratio:

For the Bull Case future exit Price/Earnings ratio, I used:

Future EPS Growth Rate x 2 = 40

which is still lower than the current Price/Earnings ratio (67.3) and the 10-year average value (75.3). For the Base Case, I subtracted 5 from the Bull Case, and for the Bear Case, I added 5 to the Base Case.

Thank you for being a part of Long-Term Pick! This post is public, so please consider becoming a patron of the project. Use the promo code 2025 to receive 60% off your first month of subscription. This offer is valid until the end of January.

☑️ Checklist

Profitability:

✅ Gross margin at least 40%: 55.3%

✅ Net margin at least 10%: 21.3%

✅ FCF margin at least 10%: 30.8%

✅ Management (ROIC, ROCE, ROE, ROA): Yes (All above 10%)

❌ Piotroski F-Score: 3 of 9 (Not passed: Higher ROA yoy, Lower Leverage yoy, Higher Current Ratio yoy, Less Shares Outstanding yoy, Higher Gross Margin yoy, Higher Asset Turnover yoy)

✅ Revenue surprises in last 7 years: Yes (Based on TradingView's data)

✅ EPS surprises in last 7 years: Yes (Based on TradingView's data)

🟨 EPS growth YoY 7 years in a row: No (Missed 2023; Based on TradingView's data)

Valuation and Advantage:

✅ Valuation below its 5-year averages: Yes

❓ Valuation below the industry: available for patrons only

✅ Does it have a moat: Yes (wide)

✅ Outperformed the S&P 500 10-year CAGR: Yes (29.21% vs 13.03%)

Shares:

❌ Insider ownership at least 5%: No (3.40%)

❌ Less shares outstanding YoY: No

❌ Insider buys last six months: No

Price:

✅ 1-year stock price forecast is above 10%: +36.97%

✅ Next 5-year EPS growth estimates (CAGR) is above 10%: Yes (25.77%)

❌ DCF Value: 372.38; Overvalued by 38% (5 years, discount rate: 10%, terminal growth: 3%, equity model: FCFE)

✅ Short Interest below 5%: Yes (4.80%)

✍️ Due Diligence

Profitability (7.5 of 10):

✅ Positive Gross Profit: 1.1B USD (for the last twelve months)

✅ Positive Operating Income: 486m USD (for the last twelve months)

✅ Positive Net Income: 434.2m USD (for the last twelve months)

✅ Positive Free Cash Flow: 627.5m USD (for the last twelve months)

🟨 Positive 1-Year Revenue Growth: 12% (over the past 12 months)

✅ Exceptional 3-Year Revenue Growth: 23% (per year for the last 3 years)

🟨 Positive Revenue Growth Forecast: 20% (per year over the next 3 years)

🟨 Positive ROE: 20% (for the past 12 months)

✅ Strong 3-Year Average ROE: 25% (three-year average)

❌ ROE is Declining: 22% → 20% (in the last 3 years)

✅ Exceptional ROIC: 32% (for the past 12 months)

✅ Exceptional 3-Year Average ROIC: 37% (three-year average)

❌ ROIC is Declining: 35% → 32% (in the last 3 years)

Solvency (8.5 of 10):

✅ Short-Term Solvency: short-term assets (2B USD) exceed its short-term liabilities (337m USD)

✅ Long-Term Solvency: long-term assets (3B USD) exceed its long-term liabilities (503m USD)

✅ Low Debt-to-Equity: 0

✅ High Altman Z-Score: 55.75 (whether a company is headed for bankruptcy - takes into account profitability, leverage, liquidity, solvency, and activity ratios)

This is not a financial or investing recommendation. It is solely for educational purposes.

If you like the content, please hit the like icon, leave a comment, and share the publication with your friends and colleagues - this will motivate the author. If you're ready to support the project and get access to additional materials, visit this page.