TSMC: Largest Contract Semiconductor Manufacturer Still Below Fair Price

TSMC is a global leader in semiconductor manufacturing, well-known for its advanced technology and focus on producing innovative chips for high-demand industries like AI and mobile computing.

Changelog:

Jan 30: Updated fair price valuation. The new fair price is $288.

Jan 14, 2025: Overview: Investment in Innolux Factory, Expansion of 2nm Plants, Collaboration with Amkor Technology, Doubling CoWoS Capacity, Sustainability Initiatives, and Impact of U.S.-China Trade Policies.

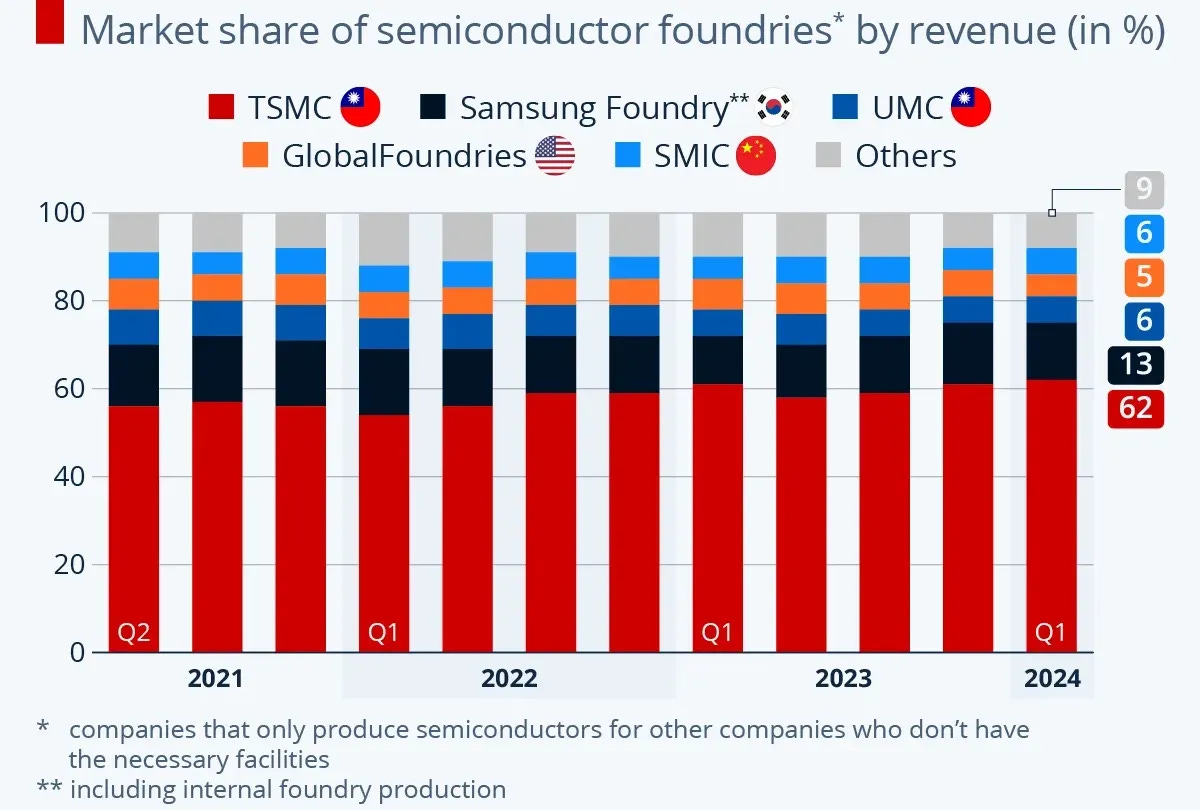

Taiwan Semiconductor Manufacturing Company (TSMC) is the world’s largest contract semiconductor manufacturer, producing advanced chips that run technologies ranging from smartphones to artificial intelligence (AI). Well-known for its advanced process technologies, TSMC maintains over 60% of the global foundry market share, partnering with industry leaders like Apple, Nvidia, and AMD. As a foundation of global semiconductor supply chains, TSMC is well-positioned to capitalize on rising demand for AI, high-performance computing, and mobile devices in the years to come.

For patrons, all the companies covered by Long-Term Pick are available in an XLS file and in graphic-readable format (PDF and PNG) and are updated weekly. Moreover, patrons also have access to additional companies not publicly covered on the website.

Content:

💡 Investment Thesis

🧐 Company Overview

🏰 Economic Moat

🚀 Business Strategy

🏛️ Capital Allocation

✅ Advantages

❌ Disadvantages

🥇 Competitors

⏮️ Past

📶 Future

💲Current Valuation

🏷️ Fair Price

☑️ Checklist

✍️ Due Diligence

💡 Investment Thesis

TSMC presents a compelling investment opportunity as the world’s largest contract semiconductor manufacturer. The company’s low PEG ratio, combined with its leadership in advanced process technology, suggests significant potential for long-term growth. Unlike all of its competitors, TSMC consistently delivers high profit margins and equity returns, which underscores its operational efficiency and ability to meet the rising global demand for semiconductors.

Currently trading below the semiconductor industry average valuation metrics and my fair price estimate of $228, which is still below its current price.

Given its current valuation and robust growth prospects, TSMC is a strong candidate for inclusion in a long-term portfolio.

➡️ Additional materials: PDF/PNG Quick Analysis, Market Overview, and others

🧐 Company Overview

Incorporated: 1987 IPO: 1997 Sector: Technology Industry: Semiconductors Stock Style: Large Growth Market Cap: $1.03 Tril Total Number of Employees: 76,478 Website: https://www.tsmc.com Earnings Date: Jan 10, 2025TSMC is the largest dedicated contract chip manufacturer in the world, controlling over 60% of the global market share. It was founded in 1987 as a joint venture between the government of Taiwan, Philips, and private investors. The company’s advanced technology and focus on producing chips designed by other companies have attracted prestigious customers, including Apple, Nvidia, and AMD. TSMC employs more than 73,000 people and generates consistent profits due to its leadership in chip manufacturing.

To watch: TSMC Fab Tour (YouTube)

The company’s CEO and Chair is Dr. C.C. Wei. He was President and Co-CEO from November 2013 to June 2018, and Co-Chief Operating Officer from March 2012 to November 2013. From 2009 to 2012, he was TSMC's Senior Vice President of Business Development. Before that, Dr. Wei was Senior Vice President of Mainstream Technology Business. Dr. Wei’s strategic focus on innovation allowed the company to meet the growing demands of AI, mobile, and automotive sectors.

In 2024, TSMC’s revenue reached TWD 2.87 trillion, exceeding prior estimates, driven by demand for advanced 3-nanometer products. Despite global challenges, such as rising electricity costs and geopolitical risks, the company has maintained strong financial performance, supported by customer relationships and steady demand for high-performance computing and AI chips.

🏰 Economic Moat

Taiwan Semiconductor has a wide economic moat due to its technological expertise and cost advantages. The company leads in advanced process technologies, such as 5-nanometer and upcoming 2-nanometer nodes. This guarantees excellent performance, efficiency, and cost-effectiveness in chip production. Historical gross margins are twice as high as those of its closest competitors, thanks to its economies of scale and premium technology pricing.

The company’s long-term investment in R&D creates barriers for smaller competitors. Innovations like FinFET and GAA technology further strengthen its leadership position. Over the years, the company has maintained over 50% market share in leading-edge processes, making it difficult for other firms to reach for. TSMC also benefits from close relationships with industry leaders like Apple and Nvidia, which help justify its significant investments in new process nodes. These collaborations ensure that TSMC remains a critical partner for the development of next-generation technologies.

🚀 Business Strategy

TSMC’s strategy is based on focusing on the most advanced nodes to serve industries with high demand for performance (AI, mobile devices, and automotive applications). By concentrating on high-value products, the company avoids the commoditization seen in older technologies.

Their Open Innovation Platform stimulates closer collaboration with clients, encouraging them to design products tailored to their manufacturing capabilities. This strategy attracts smaller clients and also strengthens relationships with industry leaders like Apple and Nvidia.

The company’s geographical diversification, including new facilities in Arizona, solves geopolitical risks and strengthens its resilience.

Core business segments:

Foundry Services: TSMC primarily operates as a pure-play foundry, meaning it manufactures semiconductor chips for other companies without designing its own chips. This segment has several aspects:

Wafer Fabrication: Manufactures silicon wafers based on designs provided by its customers.

Technology Platforms: Offers multiple technology nodes, including advanced process technologies (like 5nm and 7nm) and mature process technologies (like 28nm and above).

Advanced Technology: The company invests in R&D to maintain its leadership in advanced semiconductor technology. Key focus areas include:

Nanosheet Transistors: Innovations in transistor architecture to enhance chip performance.

3D IC and Chiplet Technologies: Advanced packaging solutions to improve integration and performance.

Customer Segments:

High-Performance Computing (HPC): Semiconductors for supercomputers, data centers, and AI applications. High demand in this area is driven by cloud computing and AI.

Mobile Devices: The company serves major smartphone manufacturers, providing chips that power mobile devices. This segment remains a significant revenue source.

Automotive: With the increasing demand for smart and electric vehicles (EVs), TSMC has been expanding its offerings in automotive semiconductor solutions.

Internet of Things (IoT): Semiconductors for connected devices, smart home applications, and wearables.

Consumer Electronics: Produces chips for various consumer electronics, including TVs, gaming consoles, and home appliances.

Mature Technology: In addition to advanced processes, they also offer mature technology nodes for a variety of applications, including:

Analog and RF Devices: For communications and signal processing applications.

Power Management ICs: Used in various electronic devices for efficient power control.

Collaboration and Partnerships: TSMC collaborates with a variety of technology companies and ecosystems, which helps to expand its market presence.

🏛️ Capital Allocation

The company consistently achieves ROE above 20%, supported by disciplined investment in advanced technologies. In recent years, it directed 30%-50% of its revenue toward capital expenditures to maintain its technological leadership.

TSMC’s stable earnings support consistent dividend growth, which reflects its strong financial health.

TSMC prioritizes dividends over share buybacks. Unlike many competitors, the company has avoided major acquisitions, focusing instead on organic growth and partnerships.

Their ability to balance heavy investments in new technologies with consistent shareholder returns highlights their strategic view and operational efficiency.

✅ Advantages

Economies of scale. This allows it to produce chips at lower costs than competitors. With its massive production capacity and advanced technology, TSMC can manufacture chips more efficiently, leading to lower unit costs. This scale advantage enables the company to maintain competitive pricing while generating high margins.

Leadership in cutting-edge technology ensures consistent demand. TSMC’s ability to produce advanced nodes, such as 3-nanometer and 5-nanometer chips, attracts companies like Apple and Nvidia, which require top-quality semiconductors for their products. This technological advantage allows TSMC to maintain a strong and growing customer base.

A strong financial position enables significant investments in R&D. TSMC consistently allocates a substantial portion of its revenue to R&D, ensuring continuous innovation. This investment not only strengthens its technological leadership but also creates barriers for competitors, securing its market dominance in advanced chip manufacturing.

Read also:

Close relationships with clients like Apple and Nvidia strengthen its market position. By collaborating closely with its customers, TSMC gains insights into future technology needs, allowing it to align its production capabilities accordingly.

Their reliable dividend payouts reflect their stable financial management and shareholder focus. The company has a long history of consistent dividend payments, which demonstrates its strong earnings stability and commitment to returning value to shareholders.

Read also:

Their advanced manufacturing processes allow quicker time-to-market for their clients’ products. TSMC helps its clients achieve faster deployment of their cutting-edge technologies. This reliability strengthens its reputation and bolsters long-term partnerships with industry leaders.

❌ Disadvantages

The semiconductor industry’s cyclicality leads TSMC to periods of oversupply and reduced margins. During industry downturns, demand for chips may decline, leading to underutilization of production capacity. This cyclicality can result in fluctuations in revenue and profitability, creating challenges for long-term planning.

Heavy reliance on key clients creates concentration risks. With Apple accounting for 25% of TSMC’s revenue, any disruption in this relationship could significantly impact the company’s financial performance. The loss of a major client would require TSMC to find alternative customers to fill the revenue gap.

Expansion plans, including facilities in Arizona, result in high capital expenditures. Building and equipping new manufacturing plants require significant upfront investments, which can strain financial resources. Additionally, these projects often take years to become operational and profitable, adding to the financial burden.

Rising operational costs, including electricity and raw materials, pose challenges. As production becomes more energy-intensive, higher utility costs can erode margins. Similarly, fluctuations in raw material prices can increase manufacturing expenses, impacting overall profitability.

Geopolitical risks, particularly involving Taiwan, can impact long-term stability. Taiwan’s political tensions with China create uncertainties for TSMC’s operations. Any escalation in geopolitical conflicts could disrupt the company’s supply chains and access to critical resources, affecting its global competitiveness.

🥇 Competitors

TSMC has the highest margins and equity returns among the direct competitors.

Samsung is a significant competitor in advanced semiconductor manufacturing. Their significant investments in innovative technologies, such as 3-nanometer nodes, position them as direct competitors.

Intel has re-entered the foundry business, aiming to challenge TSMC with substantial government backing. While Intel’s financial resources and legacy in the semiconductor industry are strengths, it struggles with delays in advanced node development, which limits its competitiveness against TSMC.

United Microelectronics Corporation (UMC) competes with TSMC in lower-end manufacturing. While UMC’s focus on mature nodes allows it to serve cost-sensitive markets, it lacks the technological advancements and scale of TSMC, making it less attractive to high-end clients.

State-backed Chinese companies like SMIC aim to close the technology gap with TSMC. However, SMIC’s limited access to advanced tools and reliance on less sophisticated nodes hinder its ability to compete in leading-edge technologies. TSMC’s established dominance in this space remains unchallenged.

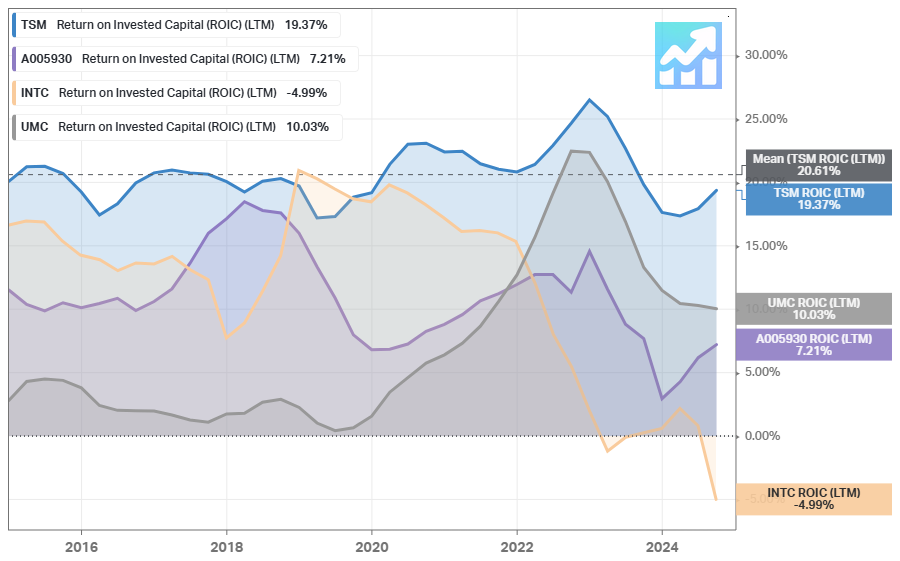

TSMC has the highest ROIC among the competitors over a 10-year period, almost twice as high as the closest competitor (UMC).

⏮️ Past

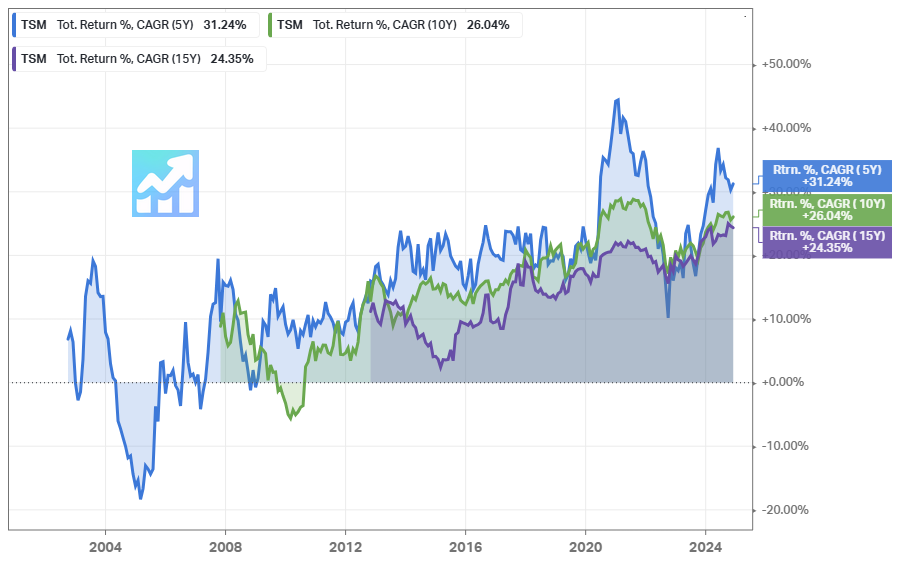

Above is the compound annual growth rate (CAGR) for the TSM stock over 5-year, 10-year, and 15-year time periods. The 5-year CAGR is 31.24%, the 10-year CAGR is 26.04%, and the 15-year CAGR is 24.35%. All periods are outperforming the S&P 500.

Above is a comparison of total returns with the S&P 500 (SPY) on a 10-year period. You can see the significant difference.

Latest important news:

December 2024: TSMC's subsidiary Foxsemicon Integrated Technology secured incentives from the Thai government to invest THB10.5 billion (approximately $310.8 million) for the construction of two chip factories in eastern Thailand. This initiative aims to create 1,400 jobs and bolster local semiconductor production capabilities.

November 2024: The company reported a net revenue of NT$276.06 billion for November 2024, marking a 34% year-over-year increase driven by strong demand for AI chips. Despite a 12.2% monthly decline from October, this revenue reflects sustained growth amid concerns regarding potential slowdowns in data center construction.

October 2024: TSMC began the construction of its first semiconductor fabrication plant in the EU, located in Dresden, Germany. This facility is part of a larger strategy to expand operations in Europe, with total investments expected to exceed €10 billion, supported by significant subsidies from the German government.

April 2024: The company revealed its latest advancements in packaging technology, introducing the CoWoS (Chip on Wafer on Substrate) 3D packaging solution. This innovation is designed to significantly improve performance and power efficiency for high-performance computing applications, satisfying the growing AI and data center markets.

January 2024: TSMC announced plans to invest $40 billion in its Arizona facilities, aiming to expand its production capacity and enhance its advanced semiconductor manufacturing capabilities. This investment is part of TSMC's strategy to meet the increasing demand for chips in various sectors, including automotive and AI.

Read also:

📶 Future

The market overview is available in additional materials for this analysis.

Below is the 5-year forecast for future EPS growth, which is projected to be a notable 24.23%.

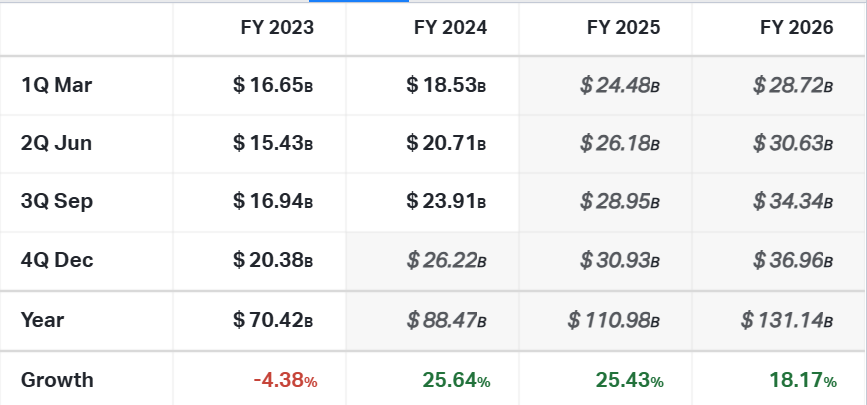

Sales are projected to grow within a 23% yearly growth rate until FY 2026.

Based on 1-year price targets offered by other analysts, the average price target for TSM comes to $240.26. The forecasts range from a low of $200.00 to a high of $260.00. The average price target represents an increase of 25.49%. Almost all analysts' recommendations are Buy and Strong Buy.

💲Current Valuation

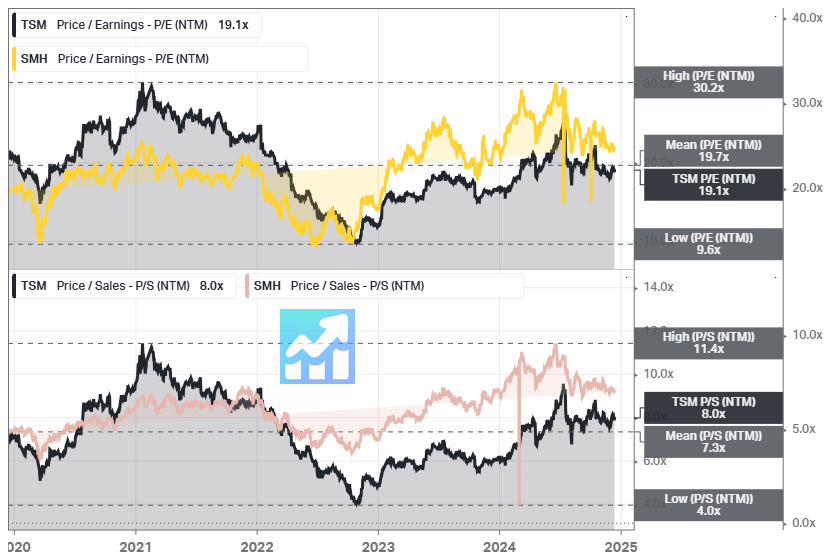

In terms of Price/Sales and Price/Forward Earnings ratios, the company is currently trading close to its 5-year average levels. In terms of the Price/Earnings ratio, with some premium.

Currently, the company is trading below its 5-year averages for Price/FCF and the PEG ratios. Pay close attention to the PEG ratio below 1, which means that the company is undervalued. In terms of the Price/Book ratio, the company is trading with some premium.

In addition, below is a comparison with the semiconductors industry (SMH ETF) in a 5-year timeframe.

As shown in the charts above, currently TMS is trading below the semiconductor industry.

🏷️ Fair Price

Jan 30: Updated fair price valuation. The new fair price is $288.

The Long-Term Pick's Fair Price (Base Case) for TSM is $228.59. The current price of $200.00 is lower by 12.71%.

Fair-to-Current Price (%): 12.71%

Current Price/Fair Price: 0.87

I used:

Discount Rate: 12%

Margin of Safety: 30%

Years: 5

Future EPS Growth Rate: 20% (The next 5-year EPS growth forecast is 24.23% annualized but my maximum is 20%)

Future Dividend and Buyback Yield: 1% (I used the 5-year average shareholder yield which is 1.01%)

Total Future Annual Growth Rate: 20 + 1 = 21%

Reviewing the historical long-term CAGR results (the Past section), my 21% CAGR is still below 5-, 10-, and 15-year CAGR values.

For the Base Case future exit P/E, I used the 5-year average P/E ratio. For the Bull Case, I added 5 to the Base Case, and for the Bear Case, I subtracted 5 from the Base Case.

☑️ Checklist

Profitability:

✅ Gross margin at least 40%: 54%

✅ Net margin at least 10%: 39%

✅ Management (ROIC, ROCE, ROE, ROA): Yes (All above 10%)

✅ Piotroski F-Score: 8 of 9 (Not passed: Higher Gross Margin yoy)

❌ Revenue surprises in last 7 years: No (2019 and 2023; Based on TradingView's data)

✅ EPS surprises in last 7 years: Yes (ased on TradingView's data)

❌ EPS growth YoY 7 years in a row: No (2019 and 2023; Based on TradingView's data)

Valuation and Advantage:

🟨 Valuation below its 5-yr average: No (Not all ratios)

✅ Does it have a moat: Yes (wide)

Shares:

❌ Insider ownership at least 5%: No (0%)

✅ Less shares outstanding YoY: Yes

❌ Insider buys last six months: No

Price:

✅ 1-year stock price forecast is above 10%: +25.49%

✅ Next 5-yr EPS growth estimates (CAGR) is above 10%: Yes (24.23%)

❌ DCF Value: 933.94 TWD; Overvalued by 12% (5 years, discount rate: 10%, terminal growth: 3%, equity model: FCFF)

✅ Short Interest below 5%: Yes

✍️ Due Diligence

Profitability (8 of 10):

✅ Positive Gross Profit: 1.4T TWD

✅ Positive Operating Income: 1.2T TWD

✅ Positive Net Income: 1T TWD

✅ Positive Free Cash Flow: 828.6B TWD

✅ Exceptional 1-Year Revenue Growth: 23%

✅ Exceptional 3-Year Revenue Growth: 21%

✅ Exceptional Revenue Growth Forecast: 25%

✅ Exceptional ROE: 28%

✅ Exceptional 3-Year Average ROE: 31%

❌ ROE is Declining: 30% → 28%

✅ Exceptional ROIC: 25%

✅ Exceptional 3-Year Average ROIC: 28%

❌ ROIC is Declining: 27% → 25%

Solvency (9 of 10):

✅ High Interest Coverage: 61.52 (earns more than enough operating income (1T TWD) to safely cover interest payments on its debt (19B TWD))

✅ Short-Term Solvency (short-term assets (3T TWD) exceed its short-term liabilities (1T TWD))

✅ Long-Term Solvency: (long-term assets (6T TWD) exceed its long-term liabilities (2T TWD))

✅ Negative Net Debt: -1.2T TWD (has more cash and short-term investments (2T TWD) than debt (964B TWD))

✅ Low Debt-to-Equity (D/E): 0.24

✅ High Altman Z-Score: 8.62

This is not a financial or investing recommendation. It is solely for educational purposes.

If you like the content, please hit the like icon, leave a comment, and share the publication with your friends and colleagues - this will motivate the author. If you're ready to support the project and get access to additional materials, visit this page.

thanks for the detailed analysis!!

the geopol risk is existential