Updated Valuations: TSM, LVMH, LRCX, V, and ASML

In January, some companies covered by Long-Term Pick (updated page) released their quarterly and yearly earnings reports. It's time to update their fair price valuations and review the latest reports. Some explanations regarding screenshots with fair price estimates:

I marked cells that I updated as grey (after the latest earning reports).

Fair-to-Current Price and Current Price/Fair Price: 🟢 undervalued, 🔵 fairly valued (+/- 5% is “fairly”), 🟡 overvalued.

Additionally, I included updated current valuations alongside their 5-year averages for easy comparison. I also added average future price estimates from other analysts to compare with my Base Fair Price Estimates, and past quarterly EPS surprises vs. actuals for the latest 10-year period.

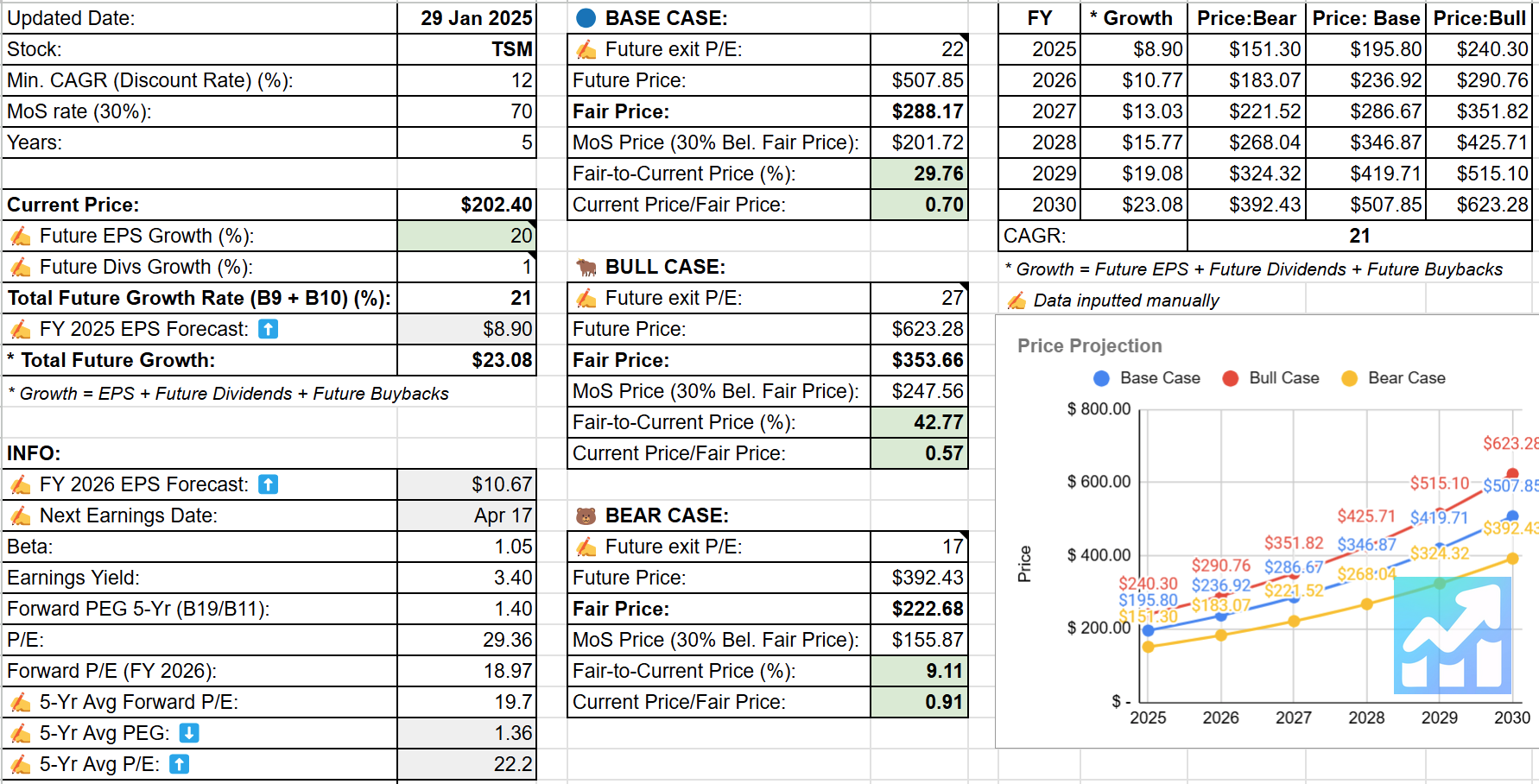

🟢 TSMC (TSM)

📝 Analyst Notes

My previous fair price was $228. After changes, the new fair price is $288. Please pay attention that the PEG ratio is still below 1 (the chart below).

🏷️ Updated Valuation

Latest earnings report (Jan 17, 2024):

👍 Positive Points

Fourth-quarter revenue increased by 14.3%, driven by strong demand for 3nm and 5nm technologies.

Gross margin improved by 1.2 percentage points to 59%, reflecting higher capacity utilization and productivity gains.

Advanced technologies (7nm and below) accounted for 74% of wafer revenue, indicating strong adoption of cutting-edge processes.

HPC revenue increased by 19% quarter over quarter, making up 53% of fourth-quarter revenue.

TSMC's cash and marketable securities reached TWD2.4 trillion, showing strong financial health.

👎 Negative Points

IoT revenue decreased by 15% quarter over quarter, indicating challenges in this segment.

DCE revenue decreased by 6%, reflecting potential weaknesses in this area.

First-quarter 2025 revenue is expected to decline by 5.5% due to smartphone seasonality.

Overseas fab expansions are expected to cause a 2% to 3% margin dilution annually over the next five years.

Inflationary costs, including higher electricity prices in Taiwan, are anticipated to impact gross margin by at least 1% in 2025.

💲Current Valuation

📈 Price Forecast

↗️ Sales and EPS Forecast

⏺️ EPS Actual vs. Estimate

🟢 LVMH (EPA: MC)

📝 Analyst Notes

Future projected EPS has increased, which I like. The 3-year average EPS growth is above 10%. My previous fair price was €551. After changes, the new fair price is €798. This significant increase is due to increased future EPS projections.

🏷️ Updated Valuation

Latest earnings report (Jan 28, 2025):

👍 Positive Points

LVMH reported a total revenue of €84.7 billion for 2024, reflecting a 1% organic growth despite a challenging economic environment, with a notable acceleration in the fourth quarter.

The profit from recurring operations reached €19.6 billion, resulting in an operating margin of 23.1%, which is significantly above pre-Covid levels.

The company generated a free cash flow of €10.5 billion, marking a 29% increase year-over-year, indicating strong financial health.

The Watches and Jewelry segment saw a 2% increase in revenue, showcasing resilience amid broader market challenges.

CEO Bernard Arnault expressed confidence in entering 2025, noting double-digit growth for Louis Vuitton early in the year.

👎 Negative Points

Overall revenue declined by 2% on a reported basis due to significant negative impacts from exchange rate fluctuations, particularly affecting the Fashion & Leather Goods and Wines & Spirits segments.

The Fashion and Leather Goods division experienced subdued performance, with a reported decline of 3% year-over-year.

LVMH faced headwinds from weakened Chinese consumer demand and high tariffs on French products.

💲Current Valuation

📈 Price Forecast

↗️ Sales and EPS Forecast

🟢 Lam Research (LRCX)

📝 Analyst Notes

My previous fair price was $102. After changes, the new fair price is $88. I lowered future “additional” growth to 1, so now it's 17% in total.

🏷️ Updated Valuation

Latest earnings report (Jan 29, 2025):

👍 Positive Points

Revenue increased by 5% quarter-over-quarter to $4.38 billion.

Operating income as a percentage of revenue improved to 30.5%.

Net income rose to $1.191 billion, with a 7% increase in diluted EPS to $0.92.

Strong performance in key markets, with China contributing 31% of revenue.

Positive outlook for the next quarter with projected revenue of $4.65 billion.

Aether® technology significantly improves EUV lithography, enhancing resolution and yield.

Offers cost and sustainability advantages by reducing energy and chemical usage.

Chosen by a leading memory manufacturer, indicating strong industry validation.

Facilitates precise, low-defect patterning, crucial for advanced DRAM nodes.

👎 Negative Points

Gross margin slightly decreased from the previous quarter.

Cash, cash equivalents, and restricted cash decreased to $5.7 billion.

Deferred revenue decreased slightly to $2.032 billion.

Potential risks from geopolitical tensions and trade regulations affecting operations.

Supply chain disruptions could impact manufacturing and sales capabilities.

💲Current Valuation

📈 Price Forecast

↗️ Sales and EPS Forecast

⏺️ EPS Actual vs. Estimate

🔵 Visa (V)

📝 Analyst Notes

My previous fair price was $320. After changes, the new fair price is $356. I lowered future “additional” growth but increased future exit P/E for all the cases (Base, Bull, and Bear).

🏷️ Updated Valuation

Latest earnings report (Jan 30, 2025):

👍 Positive Points

Visa reported a strong fiscal year with $9.5 billion in net revenue, up 10% year over year, and EPS up 14%.

Cross-border volume excluding intra-Europe rose 16%, indicating strong international growth.

Visa Direct transactions grew 34% year-over-year, highlighting significant expansion in new payment flows.

Value-added services revenue grew 18%, driven by strong growth in consulting, marketing services, and risk solutions.

Visa successfully renewed and expanded several key partnerships globally, including with ICBC in China and ICICI Bank in India, strengthening its international presence.

👎 Negative Points

Asia Pacific payments volume growth remained muted, reflecting a challenging macroeconomic environment in the region.

Operating expenses grew 11%, driven by increases in personnel and general and administrative expenses, which could impact profitability.

The restructuring charge of $213 million related to workforce changes indicates ongoing adjustments and potential disruptions.

Visa faces potential challenges from a strong US dollar, which could affect cross-border travel and spending patterns.

💲Current Valuation

📈 Price Forecast

↗️ Sales and EPS Forecast

⏺️ EPS Actual vs. Estimate

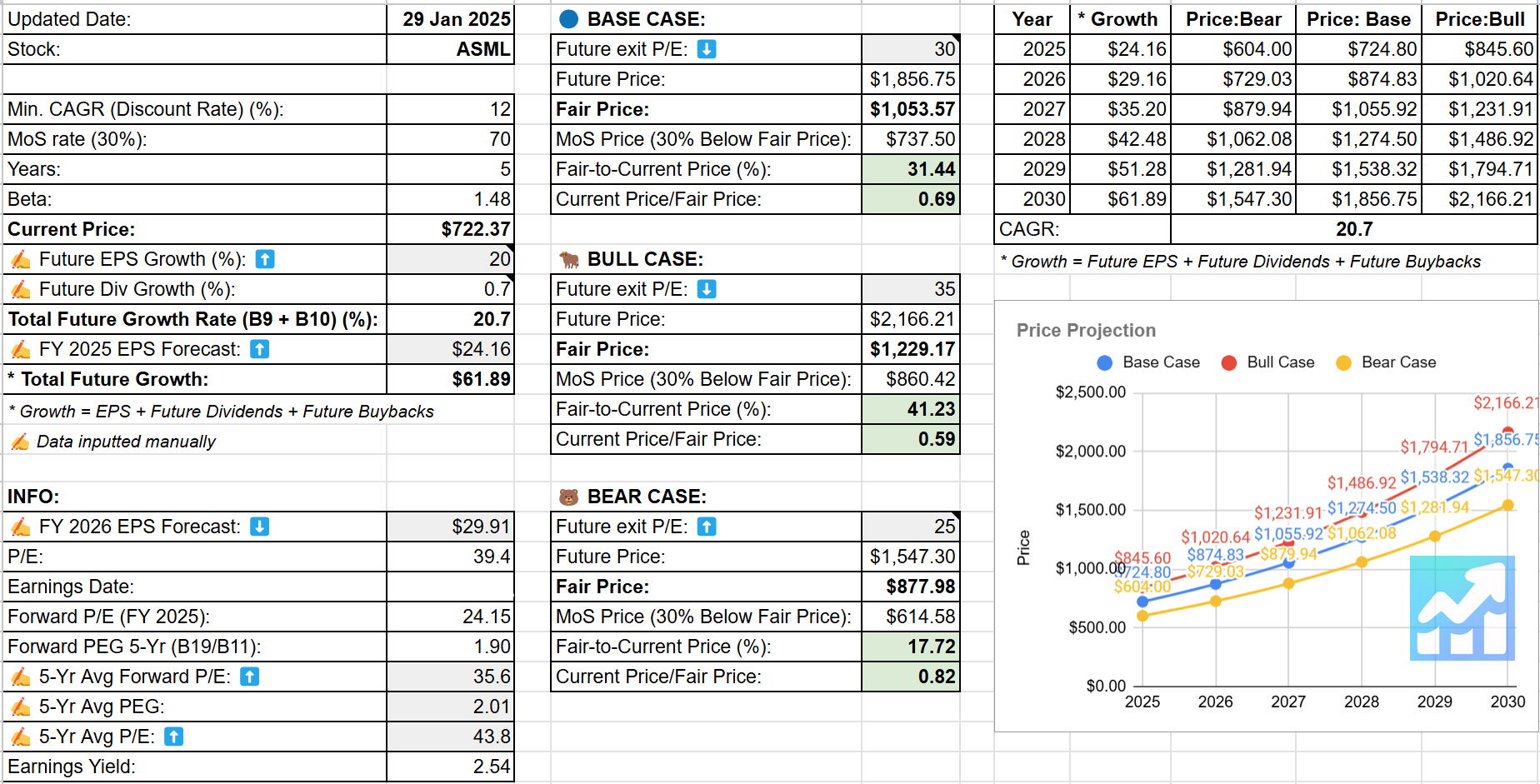

🟢 ASML Holding (ASML)

📝 Analyst Notes

The company anticipates total net sales for 2025 to range between €30 billion and €35 billion. Performance in 2024 demonstrates strong growth. The company exceeded its guidance in Q4 - strong market position and operational efficiency. The projected sales growth for 2025 shows continued demand for ASML's lithography technology. However, ASML sold 119 new lithography systems in Q4 2024, bringing the total for the year to 380 units, which is fewer than the 421 systems sold in 2023.

My previous fair price was $844. After changes, the new fair price is $1,053. I’ve lowered the Future exit P/E for the Base and Bull cases.

🏷️ Updated Valuation

Latest earnings report (Jan 29, 2025):

👍 Positive Points

Record Q4 total net sales of €9.3 billion, with a gross margin of 51.7%.

2024 total net sales reached €28.3 billion, with a net income of €7.6 billion.

ASML expects 2025 total net sales to be between €30 billion and €35 billion.

Dividend increase of 4.9% for 2024, with a total dividend of €6.40 per ordinary share.

👎 Negative Points

Decrease in the number of new lithography systems sold in 2024 compared to 2023.

No shares were purchased under the current share buyback program in Q4 2024.

💲Current Valuation

📈 Price Forecast

↗️ Sales and EPS Forecast

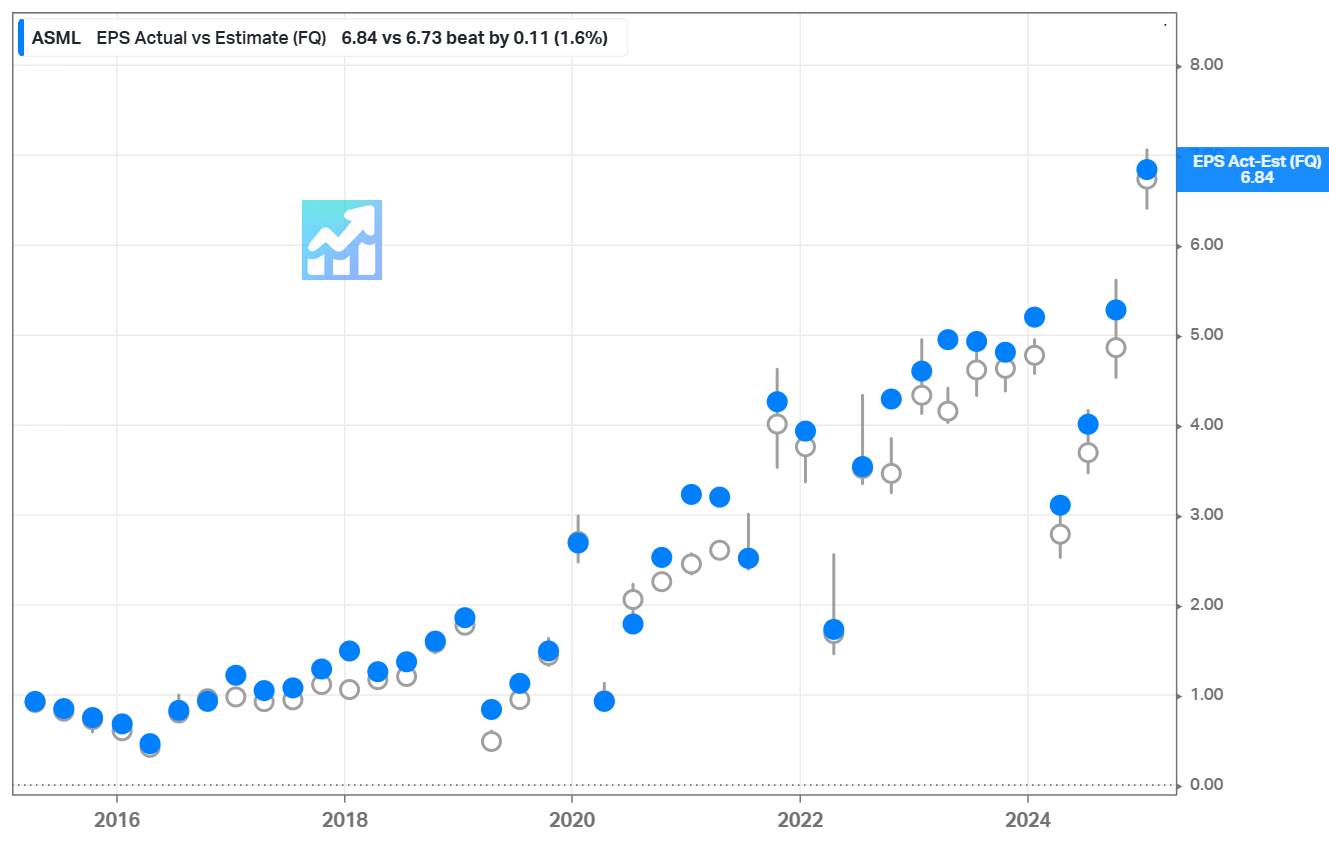

⏺️ EPS Actual vs. Estimate

🟣 Microsoft (MSFT)

The project's patrons will also receive an MSFT update with a comprehensive company analysis later. Additionally, the .XLS file containing all updated fair price valuations for easier access.

Please note that some covered companies are available only to patrons. This week, they received an analysis of InPost - an undervalued European leader in out-of-home delivery services.

This is not a financial or investing recommendation. It is solely for educational purposes.

Thanks!

Solid breakdown of valuations here. Seeing TSMC still under fair price is interesting, especially with their strong revenue growth and margins holding up. LVMH's resilience is impressive too, despite currency headwinds. Visa's long-term potential remains solid, but those rising expenses are something to watch. ASML’s demand staying high makes sense given their tech dominance. What’s the most surprising valuation shift for you?