Visa: Outperforming the S&P 500 by 2029

A comprehensive analysis of Visa Inc. (V), a global leader in digital payments demonstrates strong long-term growth potential.

Changelog:

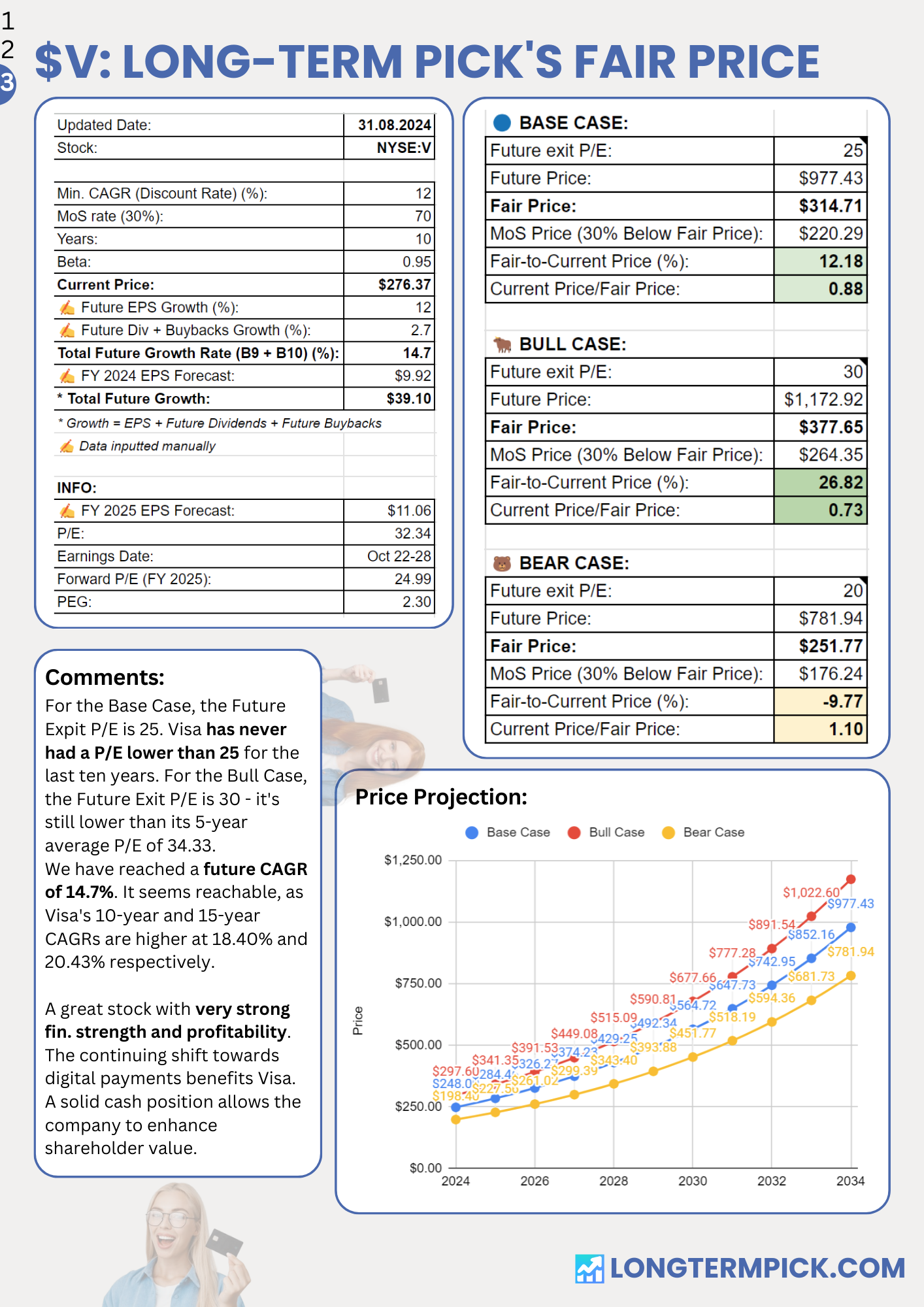

Jan 30: Updated fair price valuation. The new fair price is $288.

Nov 01, 2024: Updated fair price valuation: $320.28.

Jan 14, 2025: Overview: New Cyber Protection Charge, Expansion of Value-Added Services, Partnership with Pismo, Regulatory Challenges, and Strategic Focus on AI and Innovation.

With a vast network spanning over 200 countries and processing capabilities of 65,000 transactions per second, Visa dominates the electronic payment infrastructure. The company has impressive financial metrics, including high margins and strong returns on invested capital. With projected double-digit revenue growth and a massive $200 trillion market opportunity, the stock presents a compelling case for long-term investors in the fintech sector.

📢 Dear reader, it takes lots of time to create research and conduct such analyses. If you like the content, please subscribe and share it with your friends and colleagues 🙏

Previous analyses:

Content:

💡 Investment Thesis

🧐 Company Overview

🏰 Economic Moat

🚀 Business Strategy

✅ Advantages

❌ Disadvantages

🏛️ Capital Allocation

🥇 Competitors

📣 Recent News

⏮️ Past

📶 Future

💲Current Valuation

🏷️ Fair Price

☑️ Checklist

💡 Investment Thesis

“It's far better to buy a wonderful company at a fair price, than a fair company at a wonderful price” - Warren Buffett. It's definitely about Visa.

Visa's strategic acquisitions and partnerships are driving long-term growth and revenue increases. The company is experiencing significant profit growth due to persistent increases in payment volumes, cross-border transactions, and ongoing technology investments. The continuing shift towards digital payments benefits Visa. A solid cash position allows the company to enhance shareholder value.

Based on our fair price estimate, Visa is projected to yield higher returns than the S&P 500 in the next five years (projected CAGR is 14.7%). The current price is 12.18% lower than our Fair Price Basic Case estimate.

⬇️ Download Quick Analysis: Page 1 (PNG), Page 2 (PNG), Page 3 (PNG)

{kind=link}

{kind=link}

{kind=link}

🧐 Company Overview

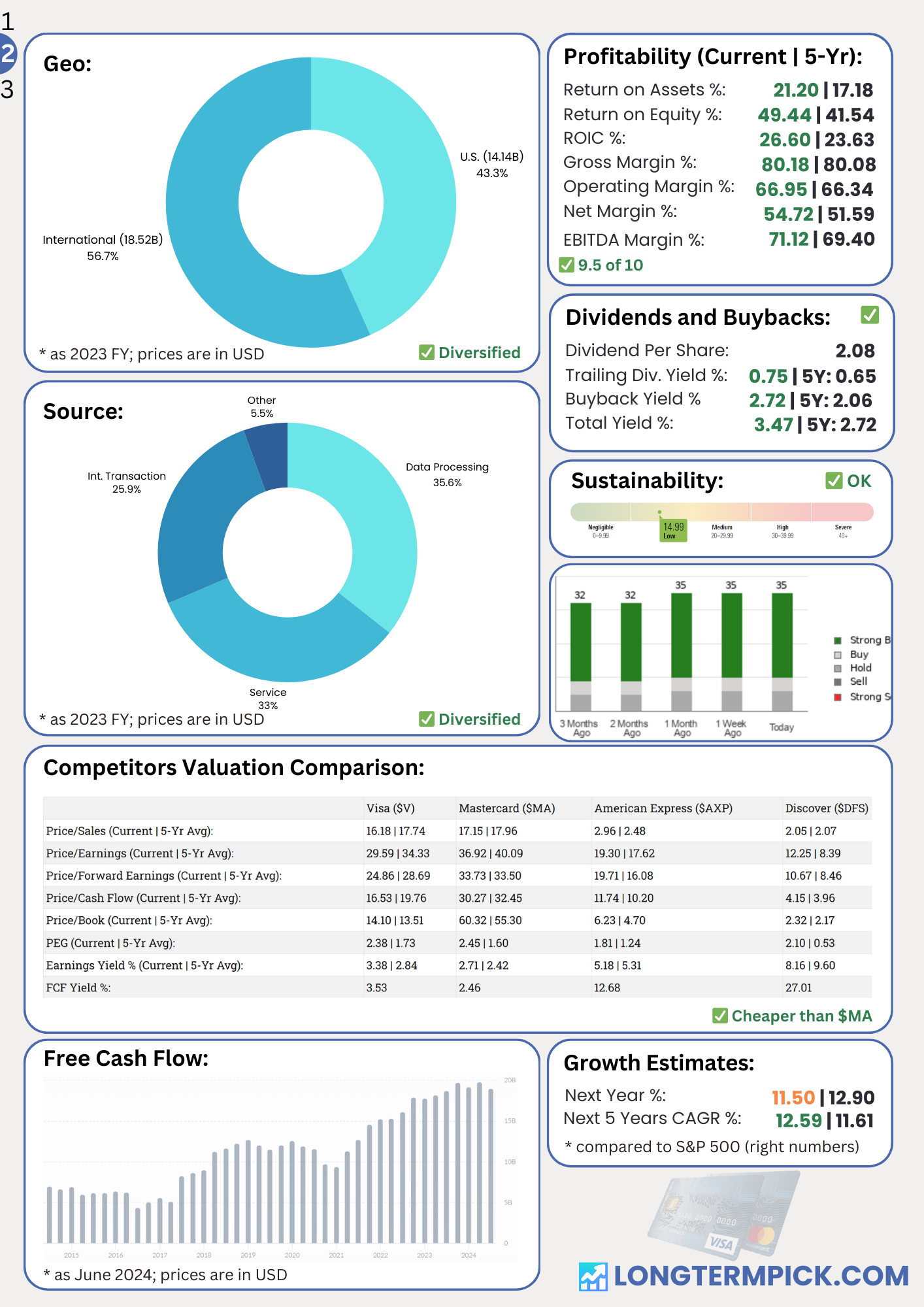

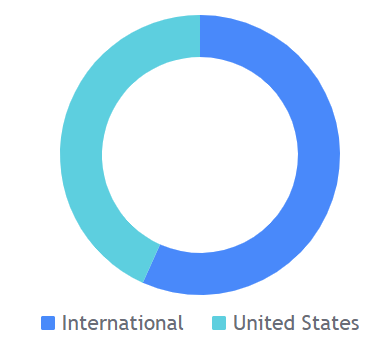

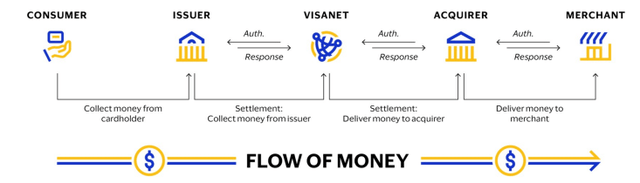

Incorporated: 2007; IPO: 2008 Sector: Financial Services Industry: Credit Services Stock Style: Large Growth Market Cap: $537.22 Bil Earnings Date: Oct 22 - Oct 28, 2024Visa is a global leader in digital payments, operating one of the world's largest electronic payment networks. Founded in 1958, the company has evolved from its roots as a Bank of America credit card program to become a key player in the global financial infrastructure. Visa processes a staggering volume of transactions, handling almost $15 trillion in total volume during fiscal 2023, with over $12 trillion specifically in purchase transactions.

Operations spanning over 200 countries and the ability to process transactions in more than 160 currencies, systems capable of processing over 65,000 transactions per second.

Visa's network includes partnerships with approximately 14,500 financial institutions and over 50 million merchants globally. According to the Nilson Report, Visa holds over 50% market share (by purchase volume) in several key regions including the US, Europe, Latin America, and the Middle East/Africa. This dominant position emphasises Visa's importance in the global payments ecosystem.

Ryan McInerney became Visa's CEO in February 2023, after serving as the company's president since 2013. In his previous role, he oversaw Visa's global operations. Before joining Visa, McInerney was the CEO of consumer banking at JPMorgan Chase, managing a division with 75,000 employees and approximately $14 billion in revenue. Earlier in his career, McInerney worked as a principal at McKinsey & Company, focusing on retail banking and payments.

🏰 Economic Moat

Visa has a wide economic moat, primarily driven by the powerful network effect. As more consumers use Visa cards, the network becomes increasingly attractive to merchants, which makes it more convenient for consumers, creating a self-reinforcing cycle. This network effect has allowed Visa to achieve near-universal acceptance in most developed markets, making it extremely difficult for new entrants to challenge its position.

The company's vast scale also grants significant cost advantages, as the highly scalable nature of payment processing leads to substantial economies of scale.

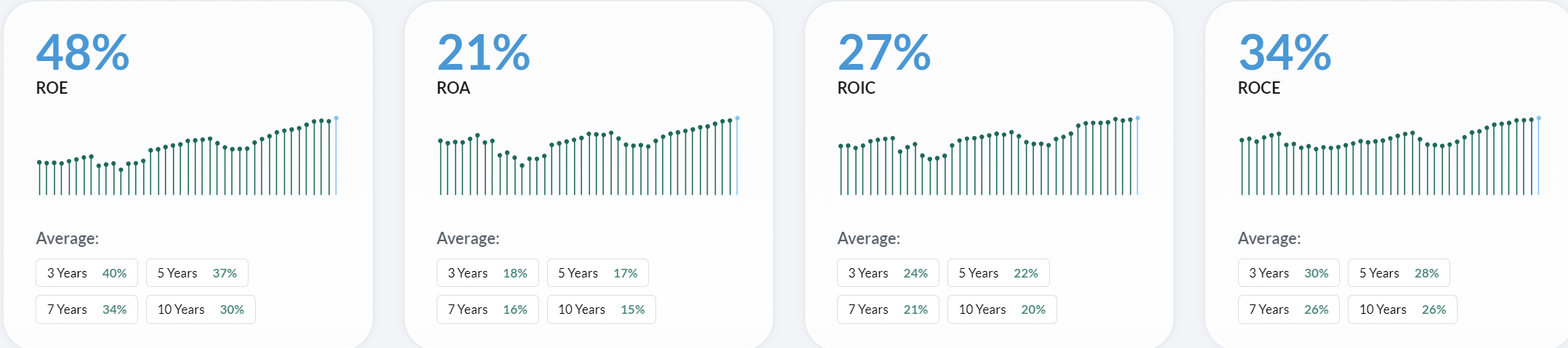

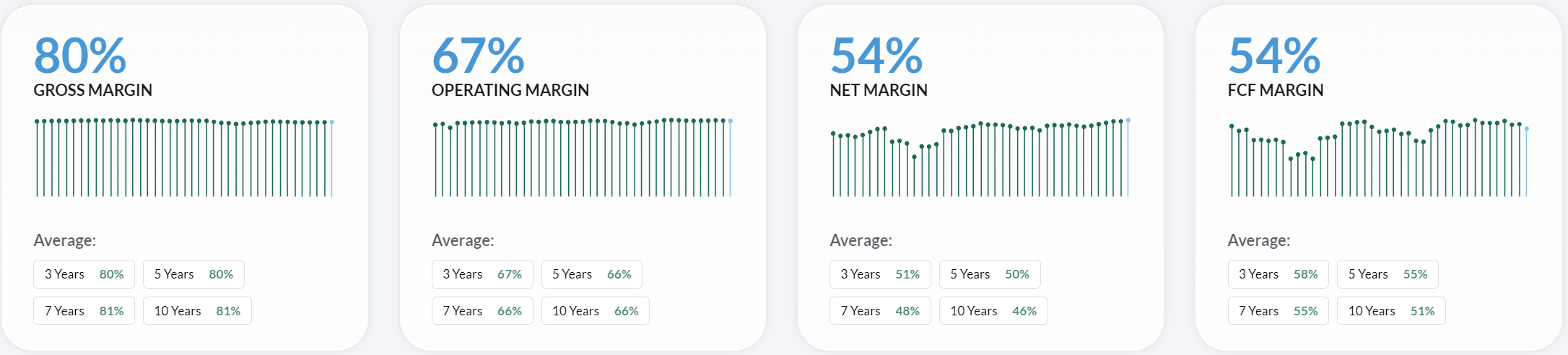

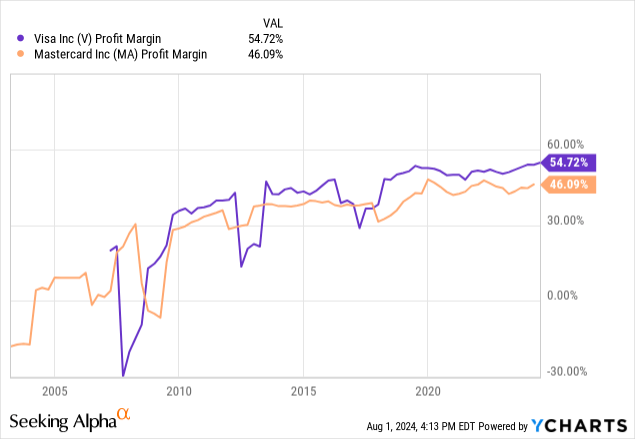

Visa has a dominant position in the global payments ecosystem. The strength of Visa's economic moat is reflected in its impressive financial metrics, with operating margins (using net revenue) reaching 67% in fiscal 2023. Returns on invested capital are quite healthy, averaging 34% over the past five years and 58% if goodwill is excluded. It's a clear indication of the company's competitive advantages and its ability to generate substantial value from its assets and investments.

🚀 Business Strategy

The business strategy concentrates on leveraging its global network and technological capabilities to capitalize on the ongoing shift from cash to digital payments. The company has been actively expanding its presence in emerging markets, recognizing the significant growth potential as these economies increasingly adopt electronic payment methods. Visa has also been investing heavily in new technologies.

Visa has made its APIs available to encourage new developments and increase access to its network, products, and services. The company operates innovation focusing globally to encourage new ideas and solutions in the payments space.

In recent years, Visa has been focusing on accelerating the migration of digital payments across new channels including e-commerce, mobile, and wearables. The company has been adopting new digital payment and security technologies, such as contactless payments and tokenization. In January 2024, Visa launched its Visa Web3 Loyalty Engagement solution, which is expected to enhance engagement with customers and improve client retention.

The company benefits from a take rate on every transaction processed through its network, meaning that as overall payment volumes grow, so does Visa's revenue.

Cross-border transactions are particularly profitable for Visa, and the recovery in global travel following the pandemic has provided a significant boost to this high-margin segment of the business.

Visa's ability to leverage its fixed-cost infrastructure as transaction volumes grow also contributes to profit expansion, allowing for margin improvements over time.

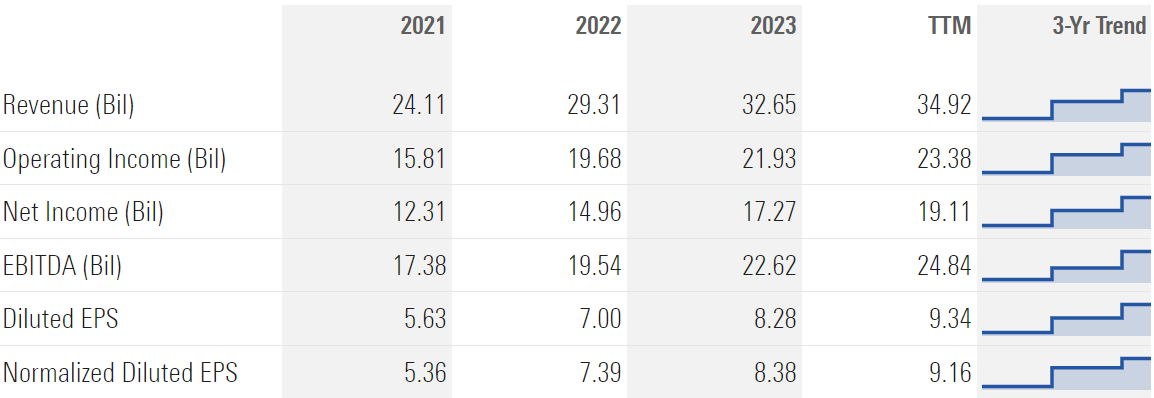

In fiscal 2023, Visa's net revenue grew by 11.4%. For the first nine months of fiscal 2024, payments volume increased 6.9% year over year, driving a 9.4% revenue growth in the same period. The company expects net revenues to grow in high single-digit to low double-digits on an adjusted constant-dollar basis in fiscal 2024.

Visa's business model is structured around six key segments:

1. Domestic Payments: This core segment facilitates electronic transactions within a single country using Visa-branded debit and credit cards for both in-store and online purchases.

2. International Payments: Focusing on cross-border transactions, this segment generates revenue from fees charged for facilitating payments across different countries and currencies.

3. Value-Added Services: Visa offers additional services such as fraud detection, data analytics, and cybersecurity to enhance the payment ecosystem and improve client operations.

4. Visa Direct: A real-time payment platform enabling quick money transfers for person-to-person payments, business disbursements, and remittances.

5. Payment Network: The backbone of Visa's operations, this segment manages the vast network connecting merchants, banks, and consumers, handling transaction processing and settlement.

6. Merchant Services: Visa provides merchants with solutions for payment acceptance, including point-of-sale technology and online payment gateways for both physical and e-commerce transactions.

✅ Advantages

The primary advantage lies in its unparalleled global network, which connects millions of merchants, thousands of financial institutions, and billions of consumers worldwide. This vast network creates a significant barrier to entry for potential competitors and allows Visa to benefit from the ongoing growth in electronic payments globally.

Visa is one of the most recognized and trusted names in the financial services industry. Technological capabilities, including its ability to process tens of thousands of transactions per second, provide a competitive advantage.

The company's financial strength, characterized by high margins and strong cash flow generation, allows it to invest heavily in new technologies and market expansion while returning significant capital to shareholders.

The strong market position is evident in its processing volumes. In fiscal 2023, processed transactions increased by 10.4% year over year. This trend continued into fiscal 2024, with processed transactions increasing 10% year over year in the first nine months of the fiscal year.

Visa is expanding its global presence through strategic acquisitions and partnerships. The company has acquired firms like Earthport, Payworks, Verifi, YellowPepper, Pismo, and Tink, enhancing its capabilities. The company has also formed alliances with entities such as Toast, Banco XP, and Rabobank, while establishing partnerships with Santander-Chile, Vodacom South Africa, Caixa-Brazil, and Bcash-Bangladesh. These strategic moves have significantly broadened Visa's global network, resulting in consistent growth in cross-border transaction volumes over recent quarters. Through these actions, Visa is not only maintaining its leading position in the payment industry but also actively strengthening it, focusing on both defending its current market share and seeking new expansion opportunities.

❌ Disadvantages

The dominant market share in many regions makes it a target for regulatory scrutiny and legal challenges. Visa has historically paid substantial fines related to antitrust issues, and this regulatory risk is likely to persist given the oligopolistic nature of the payments industry. The Credit Card Competition Act of 2023, aimed at increasing market competition and reducing merchant costs, may further impact Visa's growth rate.

The company's revenue is closely tied to consumer spending, making it vulnerable to economic downturns.

In some emerging markets, Visa faces competition from local payment networks that may receive preferential treatment from governments, potentially limiting its growth opportunities in these regions. UnionPay provides an example of how governments can favor local networks; this could shut Visa out of some emerging-market opportunities.

One specific challenge Visa faces is the increasing cost of client incentives, which are necessary to build payment volumes and increase product acceptance. In the first nine months of fiscal 2024, client incentives increased 14.4% year over year. This trend is expected to continue, potentially putting pressure on the company's adjusted revenues.

Visa suspended operations in Russia due to the Ukraine invasion, significantly affecting its business. Russia was Visa Direct's second-largest market, contributing 17% of its transactions in 2021 and representing 2% of Visa's net revenue in 2022. This decision is expected to slow payment volume growth.

🏛️ Capital Allocation

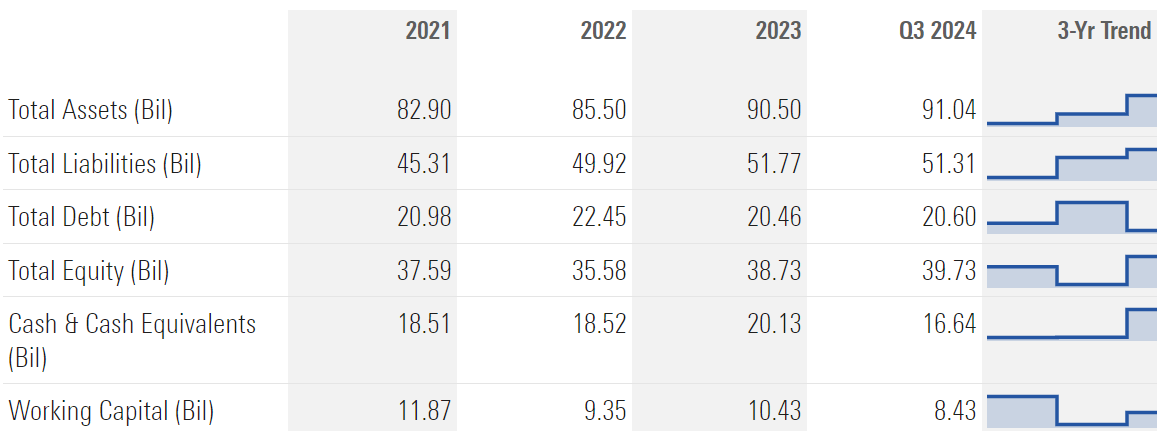

Capital allocation strategy is a balanced approach between investing in the business and returning capital to shareholders. The company has maintained a strong balance sheet, which provides financial flexibility to pursue strategic opportunities. As of the most recent report, Visa had $12.9 billion in cash and an impressive interest coverage ratio of 36.8X, higher than the industry average of 18.1X.

In terms of investments, the most significant move in recent years was the acquisition of Visa Europe for approximately $20 billion in 2016, which consolidated its global network. The company has also made smaller, strategic acquisitions to enhance its technological capabilities and expand its service offerings.

To Read: List of Visa's Acquisitions

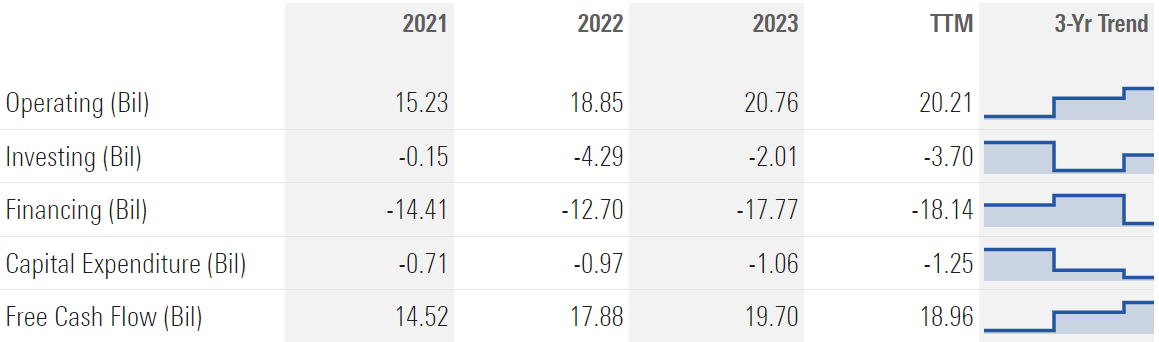

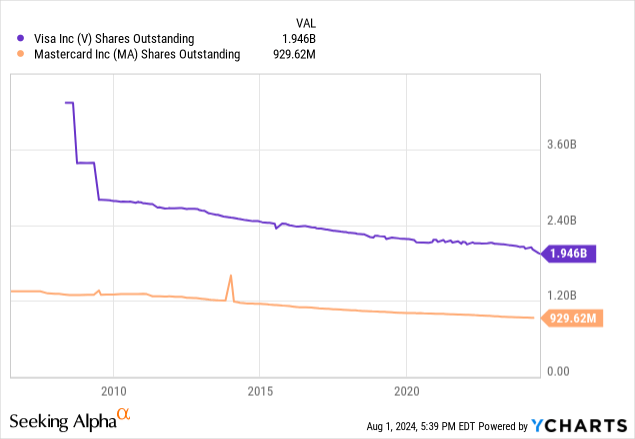

The company has been very active in returning cash to shareholders, with dividends and stock buybacks over the past three years equating to 87% of free cash flow. The company has consistently increased its dividend. In the third quarter of fiscal 2024 alone, Visa repurchased shares worth $4.8 billion. As of the most recent report, Visa had $18.9 billion remaining under its share repurchase program, demonstrating its ongoing commitment to returning value to shareholders.

🥇 Competitors

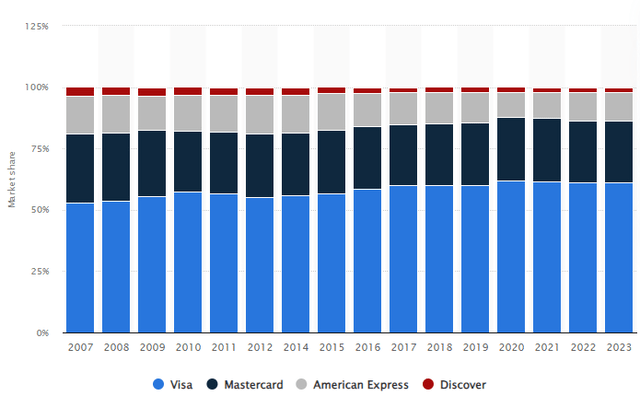

Visa's primary global competitor is Mastercard, which operates a similar payment network on a slightly smaller scale. Other competitors include American Express and Discover, which operate closed-loop networks that combine issuing and acquiring functions. In certain regions, Visa faces competition from local networks, such as China UnionPay.

The company also increasingly competes with fintech companies and other digital payment providers that are seeking to disrupt traditional payment methods. However, Visa's scale and network effects provide significant competitive advantages against both traditional and emerging competitors. Visa processes roughly twice as many transactions as its closest competitor, Mastercard.

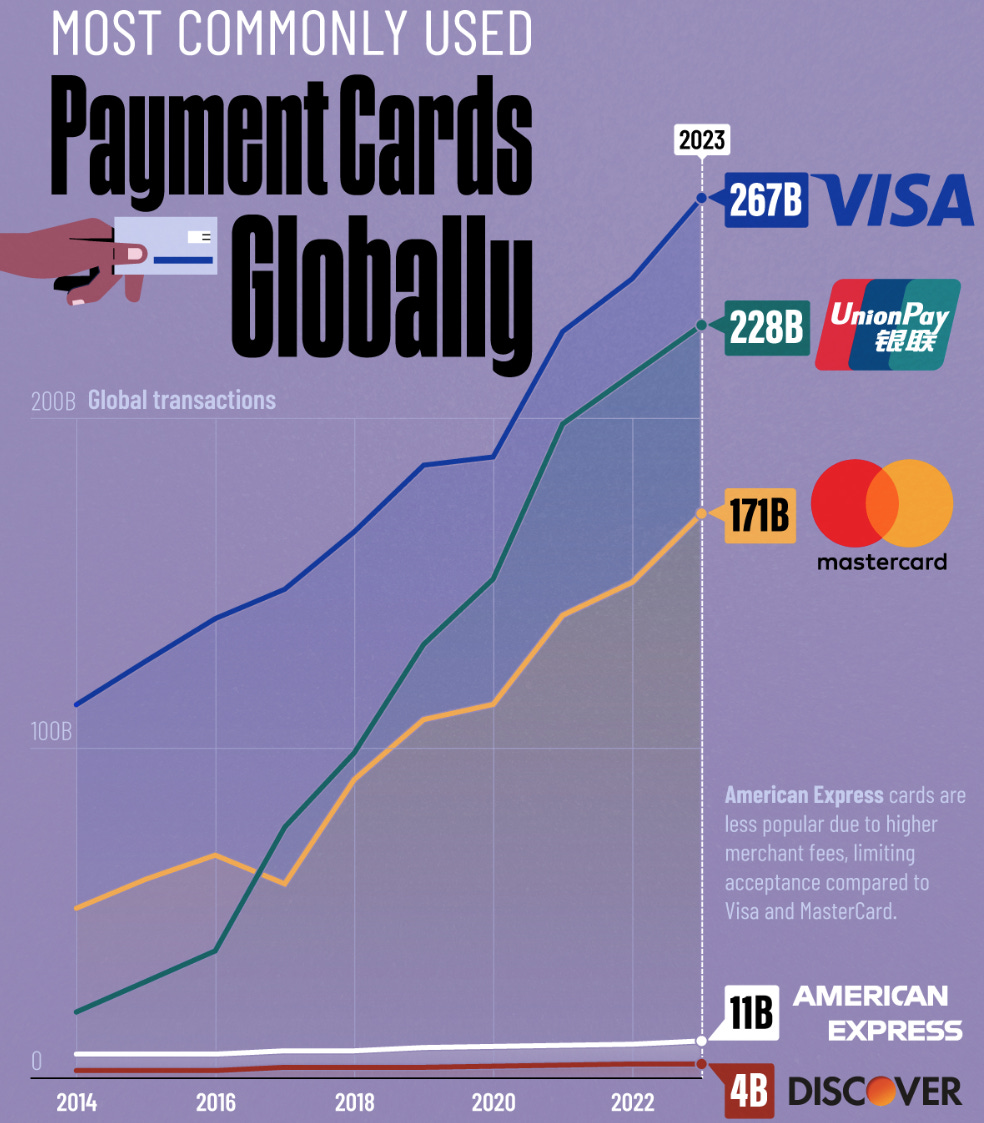

The global payment landscape has shifted significantly with the rise of China's UnionPay. Founded in 2002, UnionPay has rapidly grown to become a major competitor to Visa and Mastercard.

In 2023, UnionPay processed 228 billion transactions globally, placing it firmly in second place behind Visa's 267 billion. Moreover, UnionPay has surpassed both Visa and Mastercard in overall payment value, according to Retail Banking Research. It underscores the growing importance of emerging markets, particularly China.

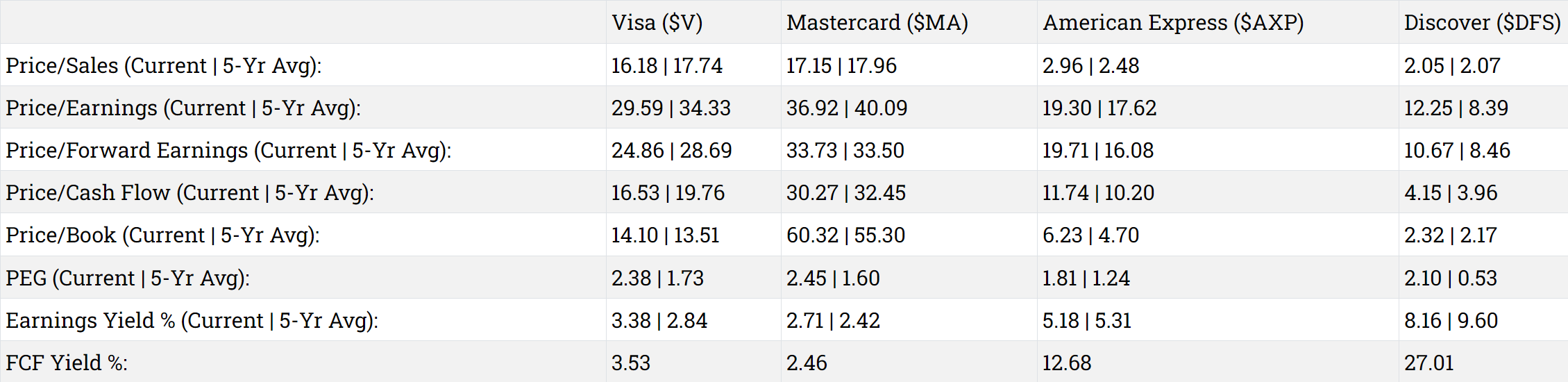

Below is a detailed table of Visa's valuation compared to its competitors:

📣 Recent News

Visa to Enhance Digital Payments With New Advisory Service – Aug. 27, 2024

Visa has launched the Money Movement Advisory Practice in the US and Canada through its Consulting & Analytics arm. This service helps businesses navigate digital payments, addressing the demand for efficient solutions. Visa's Money Movement solutions, including Visa Direct, enable real-time global transactions across 8.5 billion endpoints. This initiative targets a market Visa estimates at $200 trillion globally, positioning the company to capitalize on the expanding digital payment sector.

Visa and HSBC Collaborate to Transform Global Payments – Jul 9, 2024

Visa has recently announced a collaboration with HSBC to launch a new international payments application called Zing. This innovative app allows users to manage funds in 10 different currencies and facilitates money transfers in over 30 currencies. Furthermore, it enables transactions across 200 countries and territories worldwide.

The core of this service is a smart multi-currency card, integrated with a single application, both developed by Visa. This partnership showcases Visa's commitment to expanding its digital payment services and enhancing its cross-border transaction capabilities. By joining forces with a major global bank like HSBC, Visa is positioning itself to capture a larger share of the international money transfer and multi-currency transaction market.

Visa & Amazon Offer Flexible Payments for Canadian Consumers – June 27, 2024

Visa has formed a partnership with Amazon to introduce an instalment payment option for Canadian consumers. This new feature allows customers using Royal Bank of Canada and Scotiabank credit cards to split their Amazon purchases into multiple payments. The initiative is designed to offer online shoppers more financial flexibility and control over their spending. This collaboration demonstrates Visa's efforts to adapt to changing consumer preferences and expand its service offerings in the e-commerce sector, while also strengthening its relationships with major retailers and financial institutions.

Visa Enhances SavingsEdge for Small Business Cardholders – June 13, 2024

Visa has updated its Visa SavingsEdge program, introducing new features to encourage smarter spending and increase savings for eligible business cardholders in the United States and Canada. This program, which has been in operation since 2008, applies to Visa Business credit, debit, and reloadable prepaid cards. It continues to provide rebates to qualifying cardholders on purchases made within the program's network of participating merchants. This enhancement demonstrates Visa's ongoing commitment to adding value for its business customers and strengthening its position in the commercial card market.

⏮️ Past

Visa posted strong results for Q3 with $8.9 billion in net revenue, a 10% year-over-year rise. EPS grew 12%. Key drivers included a 7% growth in overall payment volume and a 10% growth in processed transactions. Cross-border volume excluding intra-Europe rose 14%. New flows revenue surged 18%, with Visa Direct transactions up 41%.

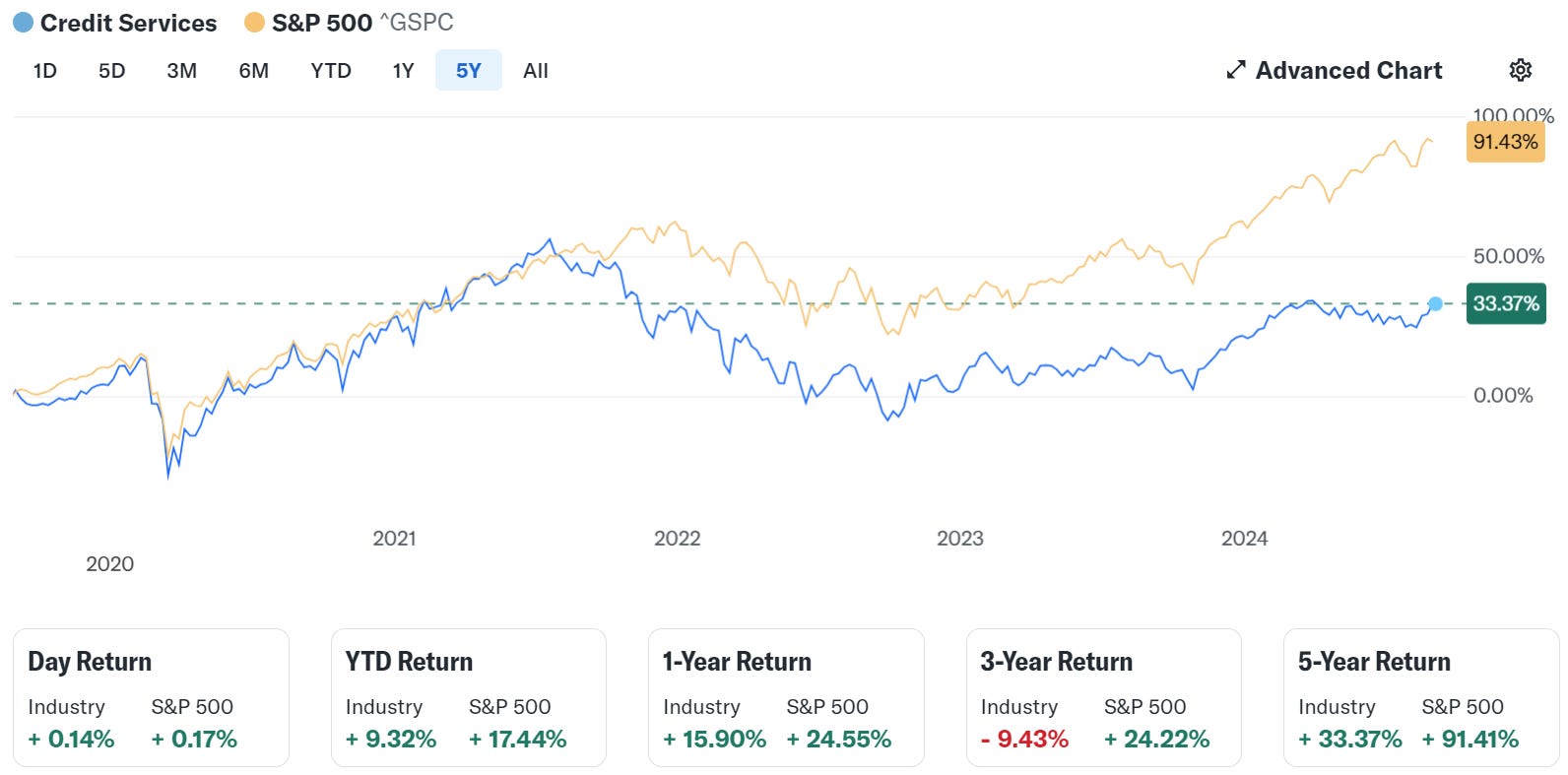

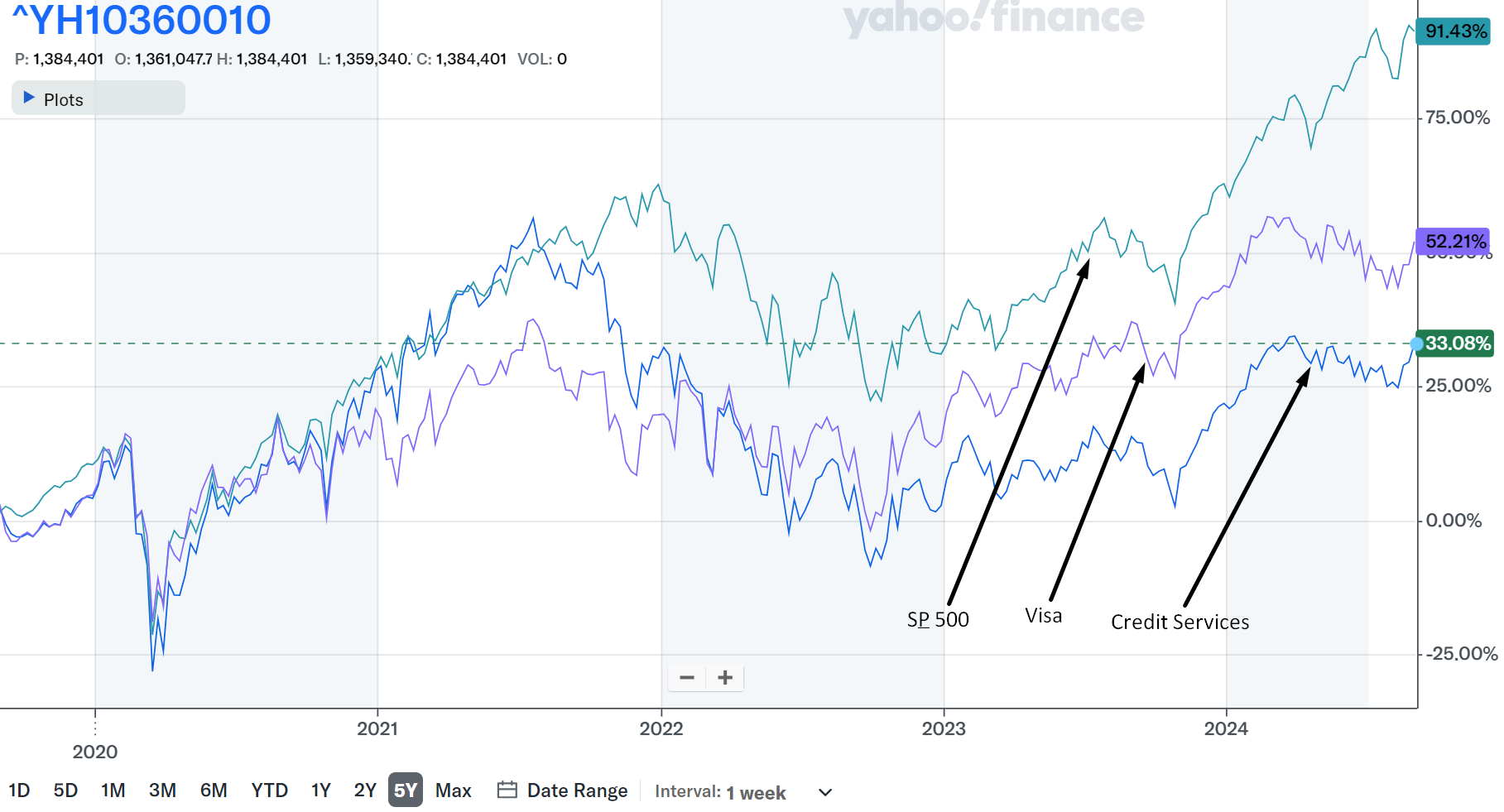

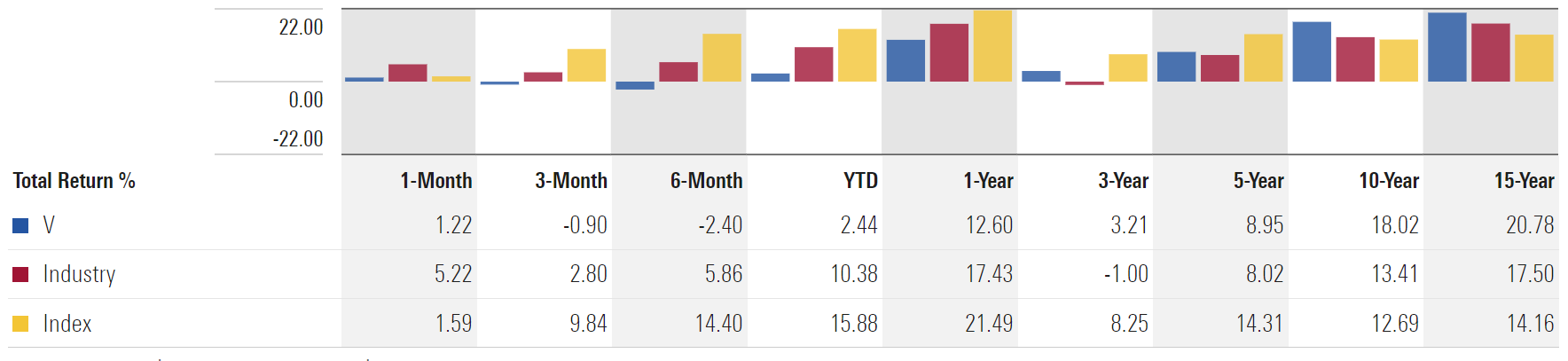

Visa has demonstrated excellent long-term performance and outperformed both its industry index (Credit Services) and the S&P 500 over 10-year and 15-year periods. The company's 10-year compound annual growth rate (CAGR) of 18.02% and 15-year CAGR of 20.78% outperforms the index returns of 12.69% and 14.16% respectively for the same periods.

However, Visa's performance has lagged in more recent timeframes. Over the past 5 years (CAGR), 3 years (CAGR), and 1 year, Visa's growth rates of 8.95%, 3.21%, and 12.60% respectively have fallen short of the index returns of 14.31%, 8.25%, and 21.49% for the same periods.

Macroeconomic factors such as interest rates and inflation influenced Visa's underperformance compared to the S&P 500. These factors affect business performance and investor sentiment, leading to varying impacts on stock performance.

Higher interest rates can increase borrowing costs, which may deter consumer spending and negatively impact companies like Visa that rely on transaction volumes. Rising interest rates correlate with reduced business performance, particularly in sectors sensitive to consumer credit.

To Read: How the Fed affects credit cards

Moderate inflation can sometimes benefit financial services by increasing nominal transaction values, but excessive inflation typically leads to economic instability, which can harm stock performance.

📶 Future

Management continues to expect net revenues to grow in low double digits on an adjusted constant-dollar basis in fiscal 2024. Operating expense is expected to see high single-digit to low double-digit growth on an adjusted constant-dollar basis. It also anticipates EPS to see growth of about 13%.

Visa is expected to demonstrate consistent growth in both sales and earnings per share (EPS) over the next three fiscal years:

Sales are projected to grow steadily, with year-over-year increases of 9.62% in FY 2024, 9.81% in FY 2025, and 10.02% in FY 2026. This indicates a slight acceleration in revenue growth over the period.

EPS growth is forecasted to be even stronger, with year-over-year increases of 13.10% in FY 2024, 11.53% in FY 2025, and 13.24% in FY 2026. While there's a slight dip in the EPS growth rate for FY 2025, it rebounds in FY 2026 to exceed the FY 2024 rate.

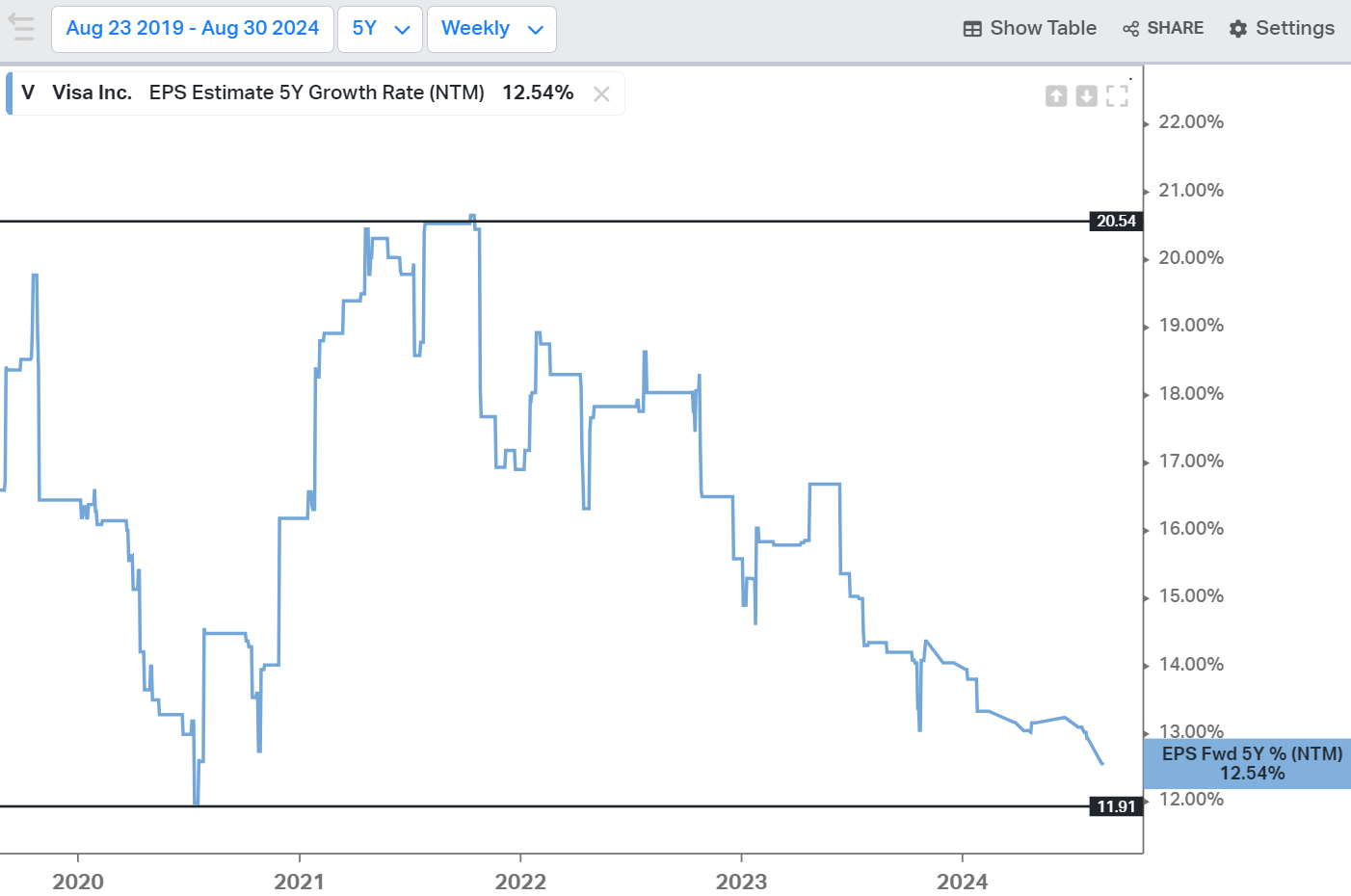

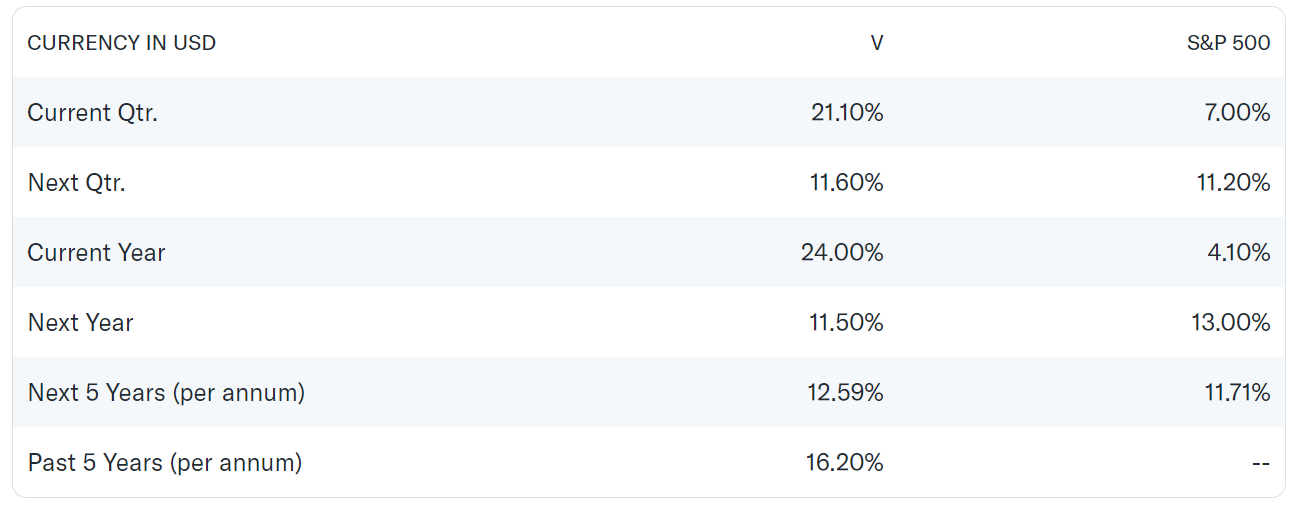

It's worth noting that the next 5-year Visa's growth estimates (12.59% per annum) are higher than the S&P 500 (11.71% per annum):

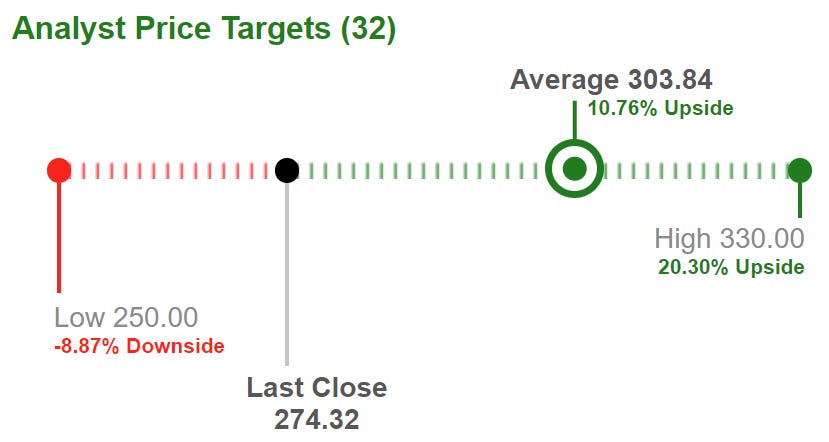

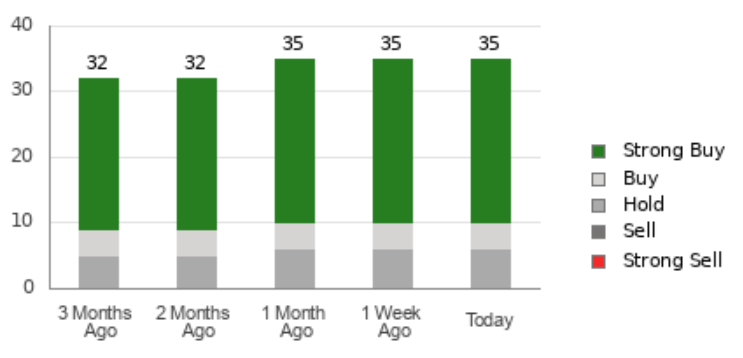

The brokerage recommendations for Visa stock show a highly positive sentiment among analysts. Currently, 35 analysts rate the stock as a Strong Buy, with a small number issuing Buy recommendations and about 5-6 analysts maintaining a Hold rating. Notably, there are no Sell or Strong Sell recommendations.

💲Current Valuation

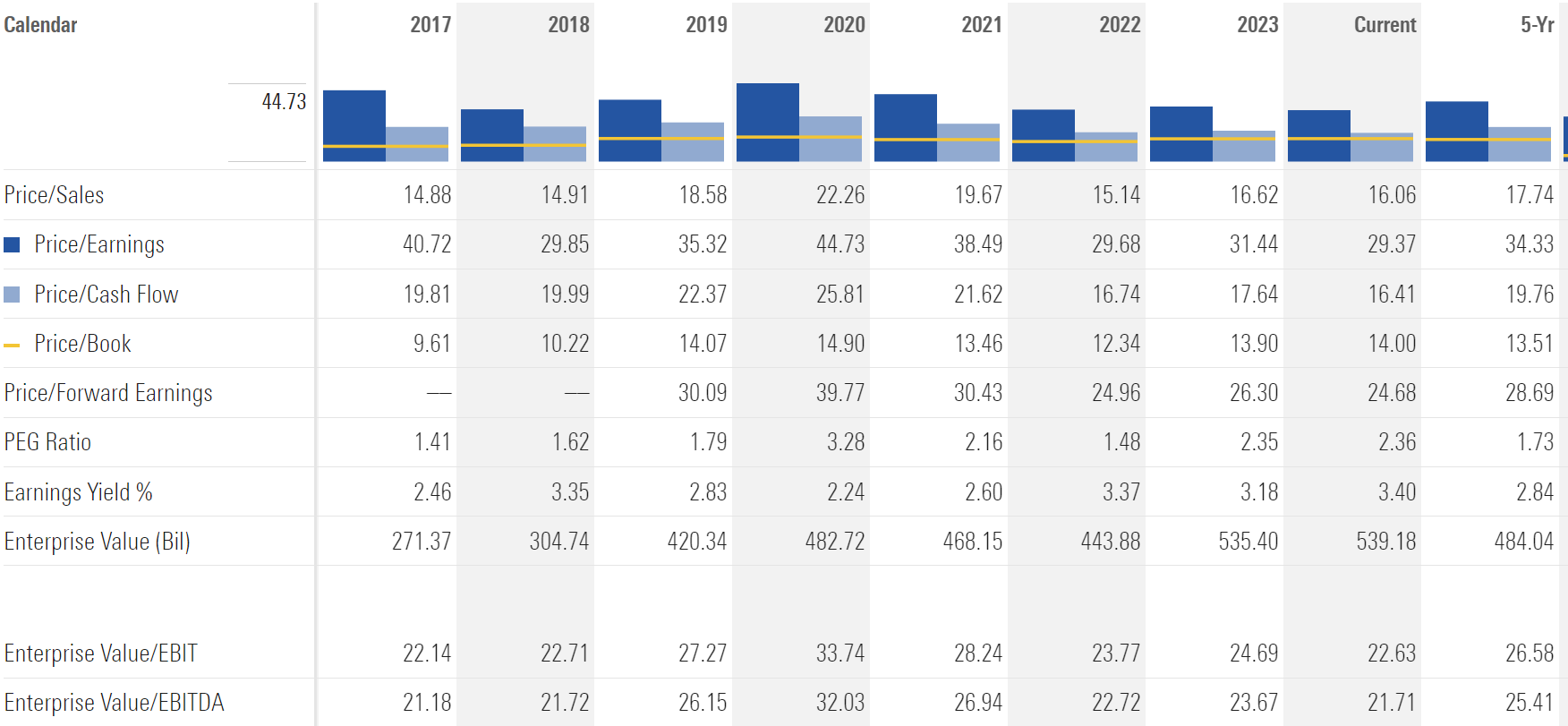

Visa's current valuation presents a mixed picture compared to its 5-year averages. Most metrics suggest the stock is undervalued, including Price/Sales (16.06 vs 17.74), Price/Earnings (29.37 vs 34.33), Price/Cash Flow (16.41 vs 19.76), and Price/Forward Earnings (24.68 vs 28.69). The Earnings Yield is higher at 3.40% compared to 2.84%, indicating better value. However, the Price/Book ratio (14.00 vs 13.51) and PEG ratio (2.36 vs 1.73) suggest slight overvaluation.

Visa appears generally undervalued compared to its historical metrics, particularly in terms of earnings and cash flow.

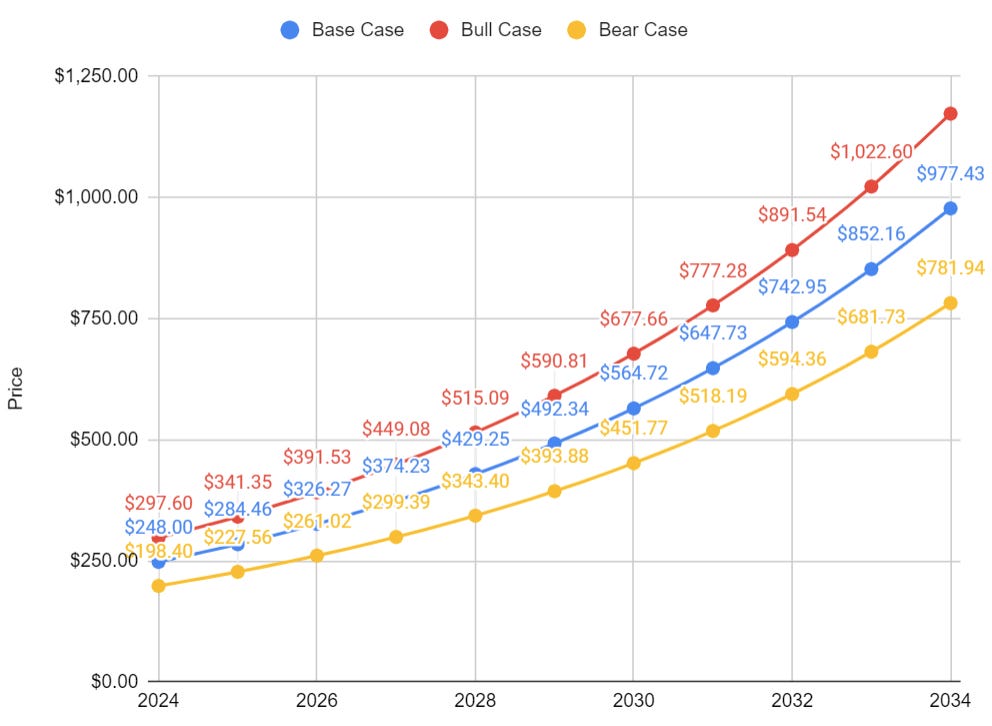

🏷️ Fair Price

➡️ Updated fair price valuation: https://longtermpick.com/p/updated-valuations-nov-24

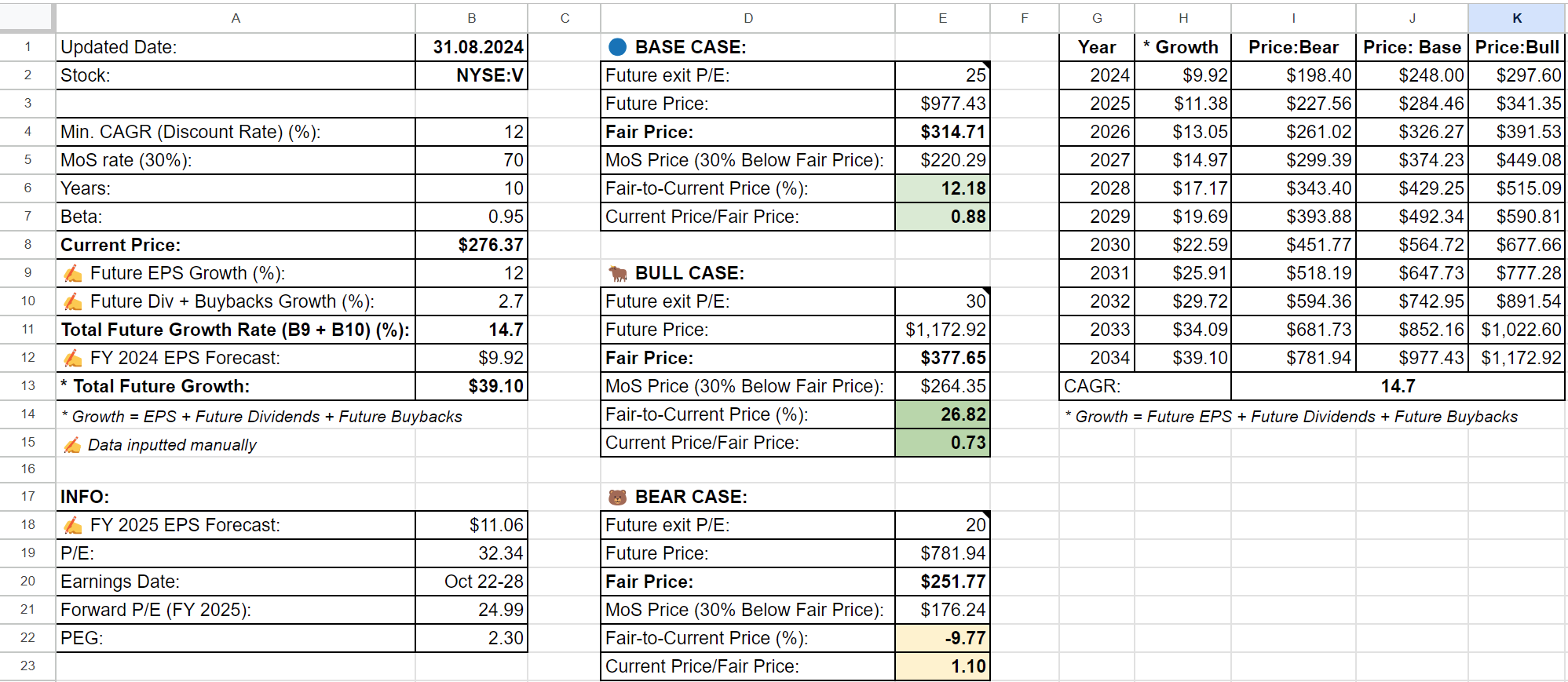

Long-Term Pick's Fair Price (Base Case) for Visa is $314. The current price of $276.37 is lower by 12.18%. So, we can say that currently Visa is undervalued.

Fair-to-Current Price (%): 12.18%

Current Price/Fair Price: 0.88

I used:

Discount Rate: 12% (S&P 500 Next 5-Yr Growth Estimates is 11.71%)

Margin of Safety: 30%

Years: 10

Future EPS Growth Rate: 12%

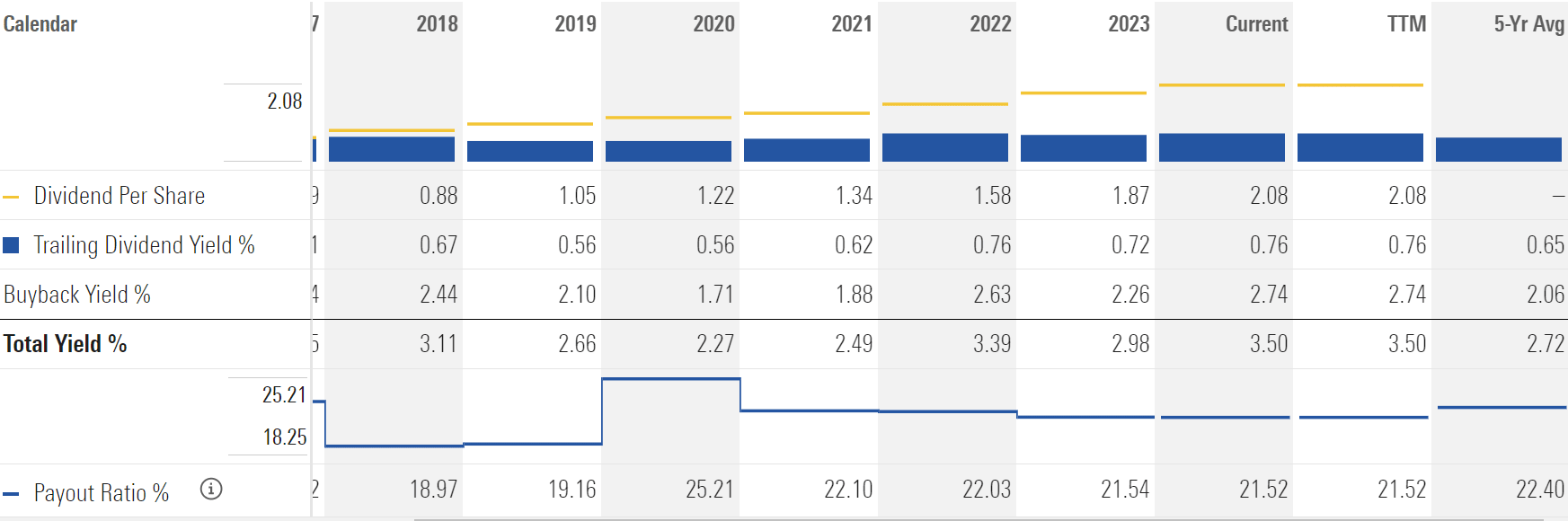

Future Dividend and Buyback Yield: 2.7% (5-Yr Avg)

Total Future Annual Growth Rate: 12 + 2.7 = 14.7%

For the Base Case, the Future Expit P/E is 25. I wanted to set it at 20, but Visa has never had a P/E lower than 25 for the last ten years. For the Bull Case, the Future Exit P/E is 30 - it's still lower than its 5-year average P/E of 34.33.

I have reached a future CAGR of 14.7%. It seems reachable, as Visa's 10-year and 15-year CAGRs are higher at 18.40% and 20.43% respectively.

☑️ Checklist

Profitability:

✅ Gross margin at least 40%: 80%

✅ Net margin at least 10%: 54%

✅ Management (ROIC, ROCE, ROE, ROA): Yes (All above 10%)

✅ Piotroski F-Score: 8 of 9 (Not passed: Higher Current Ratio YoY)

❌ Revenue surprises last 10 years: No (Missed: 2014, 2018)

✅ EPS surprises last 10 years: Yes (All last 10 years)

✅ EPS growth YoY: Yes (Missed in 2020 - Covid)

Valuation and Advantage:

✅ Valuation below its 5-Yr average: Yes

✅ Does it have a moat: Yes (wide)

Shares:

❌ Insider ownership at least 5%: No

✅ Less shares outstanding YoY: Yes

✅ Insider buys last six months: Yes (B. Arnault has been actively buying for the last few months)

Price:

✅ 1-year stock price forecast: +10.76%

✅ Next 5-Yr CAGR is above S&P 500: Yes (12.59% vs 11.71%)

✅ DCF Value: $274.46 (Overvalued by 1%; 10 years, discount rate: 10%, terminal growth: 3%, equity model: FCFE)

✅ Short Interest below 5%: Yes (1.32%)

This is not a financial or investing recommendation. It is solely for educational purposes.