👜 Luxury Market Dominance. LVMH Stock Analysis

A comprehensive analysis of LVMH (Louis Vuitton Moët Hennessy), a global luxury goods conglomerate currently overvalued by 34.59% but showing compelling long-term potential.

Changelog:

Jan 30, 2025: Updated fair price valuation. The new fair price is €798.

Jan 14, 2025: Overview: Sale of Off-White Brand, Investment in Db Bags, 10-Year Partnership with Formula 1, Launch of the 2025 LVMH Prize, Acquisition of Stake in Moncler, Focus on Sustainability, and Expansion Plans.

Dec 10, 2024: Updated fair price valuation: €551.35.

With a portfolio of over 75 prestigious brands, LVMH dominates the luxury market, demonstrating excellent financial health and high profitability metrics. Despite recent market volatility, LVMH's strategic focus on brand administration and expansion, coupled with Bernard Arnault's recent share purchases, positions it for continued leadership in the global luxury goods market, projected to grow to $112.01 billion in sales by FY 2026.

📢 Dear reader, it takes lots of time to do research and conduct such analyses. If you like the content, please subscribe and share it with your friends and colleagues 🙏

Previous analyses:

📌 The Most Undervalued Social Media Stock. PINS Stock Analysis

💅 An Attractive Entry Point for the Largest Beauty Retailer in the US. ULTA Stock Analysis

Content:

💡 Investment Thesis

🧐 Company Overview

🏰 Economic Moat

🚀 Business Strategy

💰 Profit Drivers

✅ Advantages

❌ Disadvantages

🏛️ Capital Allocation

🥇 Competitors

💲Current Valuation

📈 Past and Future

⏮️ Q2 24 and The First Half of 2024

📊 Market Trends

🏷️ Fair Price

☑️ Checklist

💡 Investment Thesis

The stock is overvalued by 34.59% but has excellent financial health and profitability, as well as high ROIC and ROE. Compared to a 5-year valuation, it's below its average valuations for the last five years. You may consider paying a premium for such a great stock.

LVMH's strength is further underscored by Bernard Arnault's recent active share purchases. A diverse collection of iconic names, including Louis Vuitton, Dior, Hennessy, and Bulgari, among others, provides LVMH with a strong competitive advantage.

Considering the anticipated deceleration in 2024 sales growth and the possibility of margin pressure as a result of the industry slowdown, it is important to remain mindful of the cyclical nature of the luxury industry. Historically, downturns have typically been limited to one to two years.

📥 Download Quick Analysis in PDF (3 pages, 590 KB)

📥 Download Quick Analysis: Page 1 (PNG), Page 2 (PNG), Page 3 (PNG)

{kind=link}

{kind=link}

{kind=link}

Important comment:

LVMH is trading as LVMUY and LVMHF, the price for VMHF is higher. In the analysis below the LVMUY is used, but sometimes in images, you can meet higher estimates or other numbers - it's for VMHF.

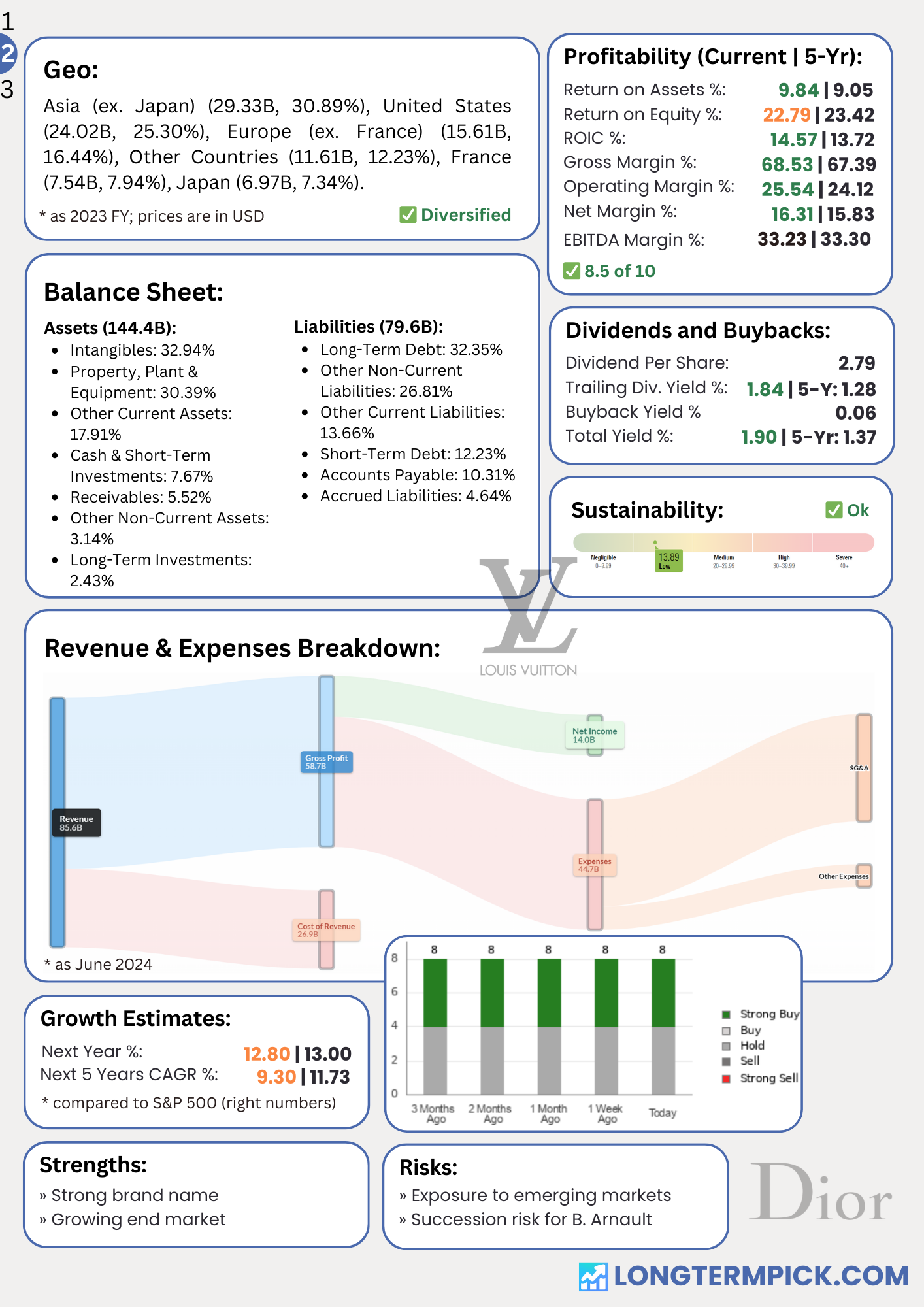

🧐 Company Overview

Moët Hennessy Louis Vuitton SE, commonly known as LVMH, is a global producer and distributor of luxury goods. The company operates across multiple segments, including fashion and leather goods, wines and spirits, perfumes and cosmetics, watches and jewellery, and selective retailing.

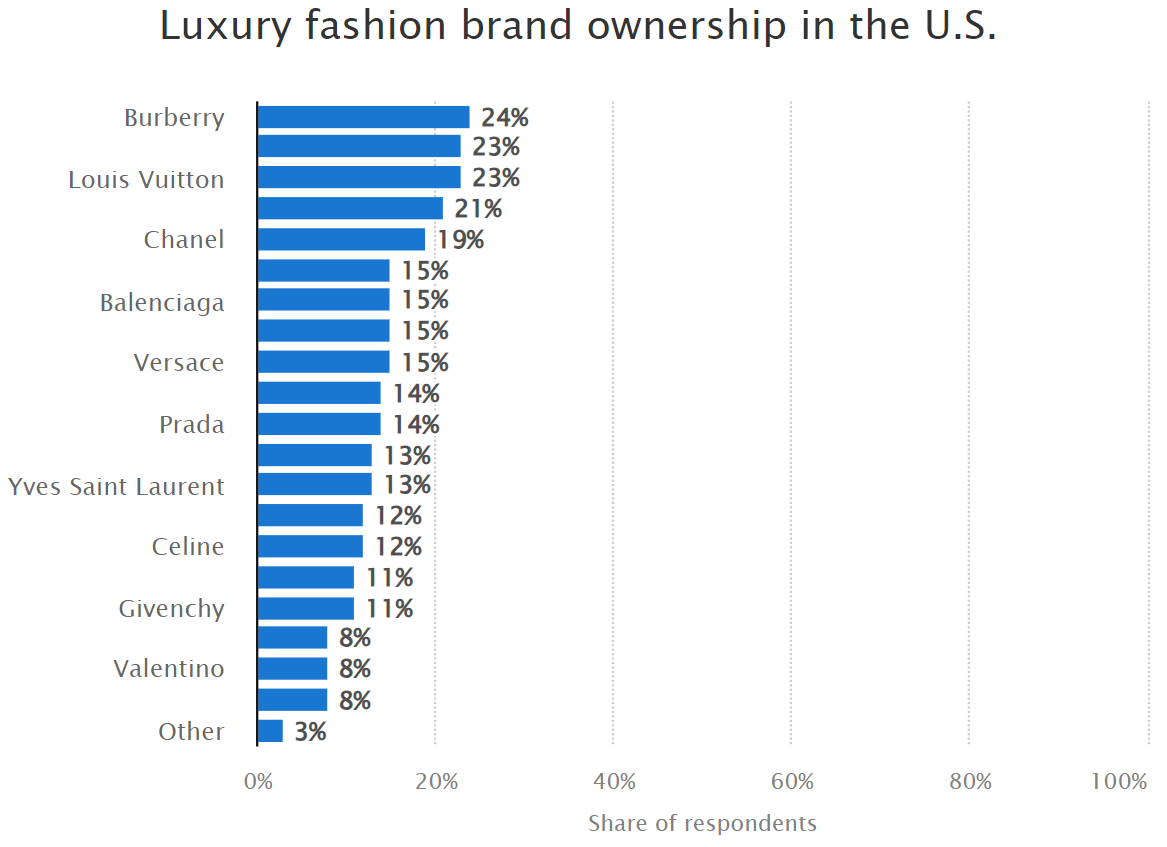

LVMH's portfolio has an impressive collection of iconic brands, with Louis Vuitton, Bulgari, Fendi, Givenchy, Tag Heuer, Hennessy, Moet & Chandon, Glenmorangie, Sephora, and Benefit among its higher-profile names.

The company's expansive reach is evidenced by its network of more than 5,000 stores worldwide, which allows it to maintain a strong presence in key luxury markets worldwide.

Bernard Arnault (Age: 75) has led the Group since 1989 and is the majority shareholder, pursuing a focused vision: make LVMH the world leader in luxury. He has been awarded Grand-Croix de la Légion d’Honneur honorary titles and Commandeur des Arts etdes Lettres.

To Read: LVMH History

🏰 Economic Moat

LVMH has a wide economic moat, primarily because of a portfolio of strong leading brands across several luxury niches. This diversified portfolio grants the company a significant competitive advantage, allowing it to generate profits well into the future.

The fashion and leather goods division, which accounts for over half of the company's profits, is backed by the century-old, globally recognized Louis Vuitton brand. This brand and other iconic names like Dior and Loro Piana benefit from long product cycles and fully controlled distribution.

In the wines and spirits segment, LVMH has a strong market share and brand recognition in noticeable market niches. The company's brands are deeply entrenched in distributors' supply chains. Long production cycles, high inventory requirements in Champagnes and cognacs, and limited land availability for production create substantial barriers for new entrants.

🚀 Business Strategy

The company has demonstrated a keen ability to develop and acquire brands that resonate with luxury consumers worldwide. LVMH's approach to brand management is evident in its handling of Louis Vuitton, which has seen its revenue increase more than tenfold since the company's formation in 1987.

The company's strategy also emphasizes maintaining full control over distribution, particularly for its top brands. This approach allows LVMH to preserve its luxury image, avoid discounting, and maintain high profitability. For instance, Louis Vuitton's fully controlled distribution enables the brand to avoid discounting its products, boosting profitability with operating margins well over 40% and helping to maintain its value perception.

To Read: The Luxury Empire: LVMH's Most Notable Acquisitions Since Inception

💰 Profit Drivers

The fashion and leather goods division stands out for growth and profits. This division (includes Louis Vuitton and Dior) consistently achieves high operating margins.

Geographically, LVMH's profit drivers vary across regions. Japan has emerged as a strong performer, showing exceptional organic growth. Asia, excluding Japan, has also demonstrated robust performance, benefiting from China's reopening and increased luxury spending in the region. Europe continues to maintain strong growth, while the United States has experienced some moderation in luxury spending.

The company's wines and spirits division, despite recent challenges in the U.S. market, particularly affecting cognac sales, has historically been a significant profit driver.

The selective retailing segment, including Sephora and DFS, has shown impressive growth. This performance is driven by strong growth in Sephora and a rebound in travel retail.

The watches and jewellery division's performance varies among its brands, with Bulgari outperforming Tiffany.

✅ Advantages

The exceptionally strong brand name in the luxury goods market makes significant consumer recognition globally. This strong brand positioning allows LVMH to control premium pricing and maintain customer loyalty.

Operates in a growing end market, which presents opportunities for expansion and increased revenue. The global luxury goods market has shown consistent growth over the years, driven by factors such as increasing wealth in emerging markets, growing consumer appetite for premium products, and the rising popularity of luxury experiences.

Fully controlled distribution system for Louis Vuitton, its flagship brand. This strategic approach allows LVMH to maintain strict control over pricing, effectively avoiding discounts on Louis Vuitton products. As a result, the brand consistently achieves impressive profitability. This pricing power not only boosts financial performance but also plays a crucial role in maintaining the brand's premium value perception among consumers.

Another notable advantage is the defensive quality of LVMH's top brands. These leading brands typically demonstrate resilience during industry downturns, often outperforming competitors and even gaining market share in challenging economic conditions. This characteristic provides LVMH with a degree of stability and strength across various market cycles.

Furthermore, many of LVMH's brands hold dominant positions in their respective industries. These brands have established track records of above-industry growth rates and consistent market share gains, underscoring the company's ability to cultivate and maintain strong, desirable brands across multiple luxury segments.

❌ Disadvantages

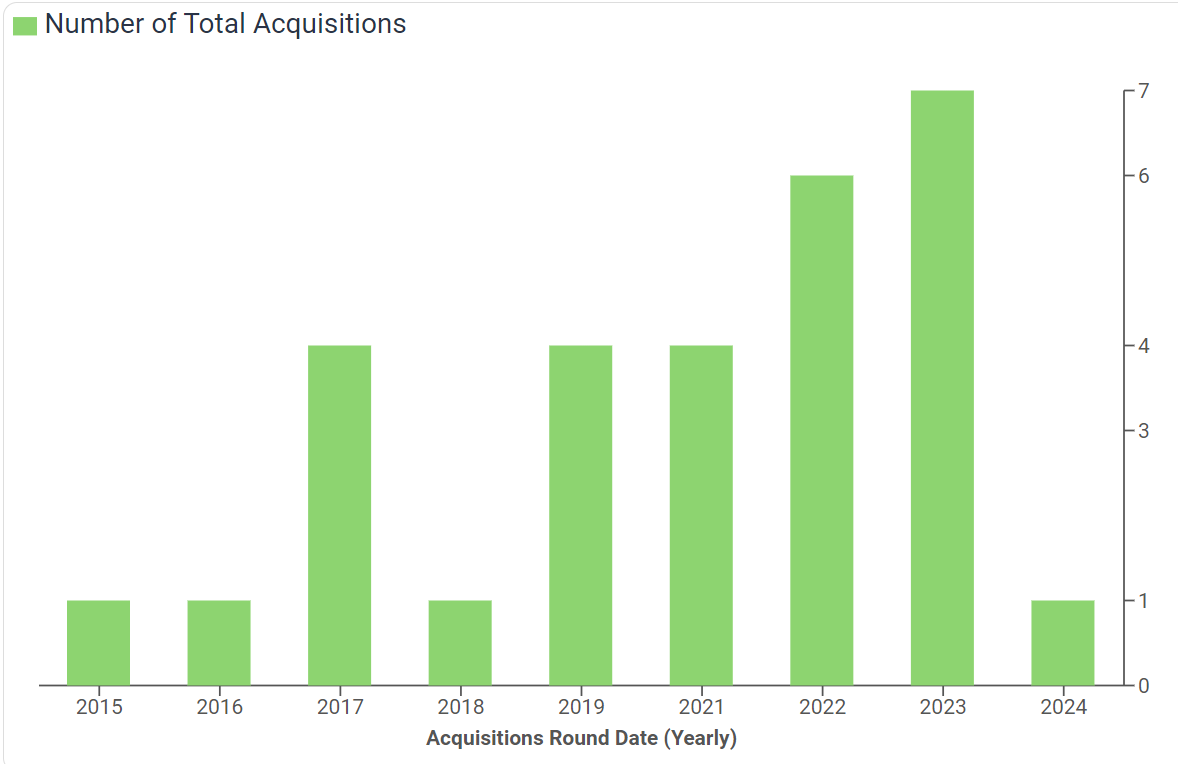

One significant issue is its aggressive acquisition strategy. While LVMH has successfully built an impressive brand portfolio, its approach to acquisitions often involves competitive bidding. This strategy can result in high purchase prices, leading to substantial capital being tied up in goodwill and purchased intangibles. Consequently, these high acquisition costs can potentially reduce the company's overall capital returns, impacting long-term financial efficiency.

While the company's top brands are strong performers, several smaller brands in the portfolio tend to detract from overall returns. This situation suggests that not all of LVMH's acquisitions or brand developments have been equally successful, potentially diluting the profitability achieved by the company's star performers. Additionally, LVMH's selective retailing segment presents a structural disadvantage due to its inherently lower margins compared to other luxury goods categories. This segment's underperformance relative to the company's high-end luxury brands may lug overall profitability.

LVMH's exposure to emerging markets presents another potential disadvantage. While these markets offer significant growth opportunities, they also come with increased risks such as economic volatility, regulatory challenges, and geopolitical uncertainties. The company's performance in these regions can be subject to sudden shifts in consumer sentiment or economic conditions, potentially impacting overall financial results.

Lastly, the group faces a notable succession risk centred around Bernard Arnault. As the company's long-standing chairman and CEO, Arnault has been instrumental in shaping LVMH's strategy and success. The eventual transition of leadership from Arnault could potentially lead to uncertainty about the company's future direction and management approach.

🏛️ Capital Allocation

LVMH's capital allocation strategy reflects a balanced approach between organic growth, acquisitions, and shareholder returns. The company has a history of strategic acquisitions to expand its brand portfolio and enter new market segments. Notable acquisitions include Bulgari in 2011 and Tiffany in a more recent deal.

While these acquisitions have generally been successful, LVMH often bids competitively for its targets, which can result in a high capital link in goodwill and purchased intangibles. This approach may potentially reduce capital returns.

The company also invests significantly in organic growth, including expanding its retail network and enhancing its e-commerce capabilities.

In terms of shareholder returns, LVMH maintains a dividend policy. The company's strong cash flow generation and relatively low leverage provide financial flexibility to pursue growth initiatives while maintaining shareholder returns.

An LVMH shareholder who invested €1,000 on July 1, 2019, would have a capital of €2,051 on June 30, 2024, based on reinvested dividends. This represents a twofold increase over five years, equating to an average annual return of around 15.4%.

🥇 Competitors

Louis Vuitton has historically been quicker than its competitors in identifying new regional opportunities. This early recognition allowed the brand to secure prime locations in emerging markets ahead of others, giving it a significant advantage.

LVMH operates in a competitive luxury goods market, facing rivalry from both large conglomerates and specialized luxury brands. Key competitors include Kering, owner of brands like Gucci and Saint Laurent, and Richemont, which owns Cartier and Van Cleef & Arpels.

Hermes International, known for its high-end leather goods and accessories, also competes directly with LVMH in certain product categories. In the premium spirits market, LVMH faces competition from companies like Pernod Ricard and Diageo.

💲Current Valuation

LVMH's current valuation metrics suggest the stock is trading at levels somewhat below its 5-year averages. The current Price/Earnings ratio of 25.26 is lower than the 5-year average of 30.02, indicating the stock may be relatively cheaper based on earnings. Similarly, the Price/Cash Flow ratio of 15.64 is below the 5-year average of 18.42, suggesting potentially better value in terms of cash flow generation. Worth noting that the Forward Price/Earnings ratio is 24.81 (the 5-year average is 26.17) which has never been below 20 for the last six years.

The current PEG ratio of 1.55 is lower than the 5-year average of 2.43, which could suggest the stock is undervalued relative to its expected growth rate. The current earnings yield of 3.96% is higher than the 5-year average of 2.91%.

📈 Past and Future

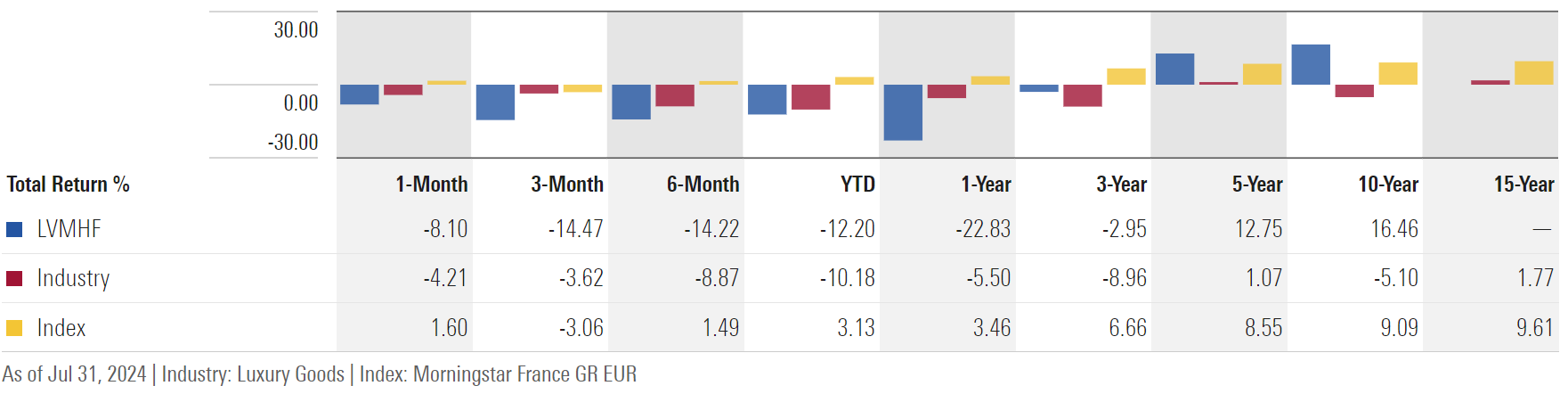

5-year Compound Annual Growth Rate (CAGR) is an impressive 12.75%. This significantly outperforms both the industry average of 1.07% and the broader index return of 8.55% over the same period (Morningstar France GR EUR). 10-year CAGR of 16.46%. This performance is remarkable. S&P 500 CAGR for 5 years is 14.31%, and CAGR for 10 years is 12.69%.

Sales are projected to grow steadily, rising from $97.59 billion in FY 2024 to $104.42 billion in FY 2025, and further to $112.01 billion in FY 2026. This represents year-over-year growth rates of 2.60%, 7.00%, and 7.27% respectively. Earnings per share (EPS) are also expected to increase, although with a slight dip in FY 2024. The forecast shows EPS growing from $33.37 in FY 2024 to $37.06 in FY 2025 and reaching $40.49 in FY 2026. The corresponding year-over-year changes are -0.33%, 11.05%, and 9.25%.

The average price target for LVMH stock stands at 169.60, indicating an 11.21% upside potential from the current price. This target is based on a range of analyst estimates, with the lowest price target at 134.21 and the highest at 205.00.

Regarding broker recommendations, the sentiment appears largely positive. Out of 8 recommendations, half rate the stock as a "Strong Buy" while the other half suggest a "Hold" position. Notably, there are no "Sell" or "Strong Sell" recommendations. This distribution of recommendations has remained consistent over the past three months, indicating a stable positive outlook among brokers.

⏮️ Q2 24 and The First Half of 2024

LVMH had disappointing sales in the second quarter, with only 1% growth in constant currency. Even so, this was better than weaker competitors like Burberry and Swatch and was on par with Richemont.

The fashion and leather division, which is the most profitable, also saw just 1% growth. Most segments experienced pressure on margins, except for the selective retailing segment. This pressure was due to increased general and administrative spending to support higher post-pandemic revenue, which was delayed, and a shift in sales to Japan, which saw a 44% increase in the first half. Japan's weaker currency and more variable store costs compared to the rest of Asia-Pacific contributed to this shift.

As a result, the group's margin dropped to 25.6% from 27.4% in the previous year. Regionally, sales in the US and Europe saw single-digit growth, with slightly better trends in the second quarter. However, sales in Asia, excluding Japan, were weak, declining by 14% in the quarter as Chinese consumers shifted their spending to Japan to take advantage of the weaker yen.

Globally, sales to Chinese consumers increased by high single digits in the first half, though there was a slight slowdown in the fashion and leather division during the second quarter. The watches and jewellery division saw a 4% decline in sales for the quarter, mainly due to Tiffany's poor performance. This was impacted by weak bridal demand and sluggish demand from aspirational consumers in the US, as well as a drop in sales among Chinese consumers.

Based on the company's report, highlights of the first half of 2024 include:

Continued organic revenue growth,

Substantial negative impact of exchange rate fluctuations, particularly on Fashion & Leather Goods,

Growth in revenue in Europe and the United States, exceptional growth in Japan arising in particular from purchases made by Chinese travellers,

Performance of Wines & Spirits reflecting the ongoing normalization of demand that began in 2023,

Good resilience in Fashion & Leather Goods, which saw its operating margin remain at an exceptional level, especially for flagship brands Louis Vuitton and Christian Dior,

Rapid growth in fragrances and makeup, and the ongoing success of our Maisons’ iconic lines,

Powerful creative momentum at all the Watches & Jewelry Maisons, and sustained investments in communications and in renovating stores,

Exceptional performance by Sephora, which consolidated its position as the world leader in beauty retail,

Significant increase in operating free cash flow, which came to more than €3 billion.

Related Analysis: ULTA Stock Analysis

📊 Market Trends

The luxury goods market shows strong growth potential and evolving consumer behaviors. LVMH's sales have been on an upward trajectory since 2020, with projections indicating continued growth through 2026. The company's operating profit and net income have also shown resilience and growth, suggesting a positive outlook for the luxury sector despite global economic challenges.

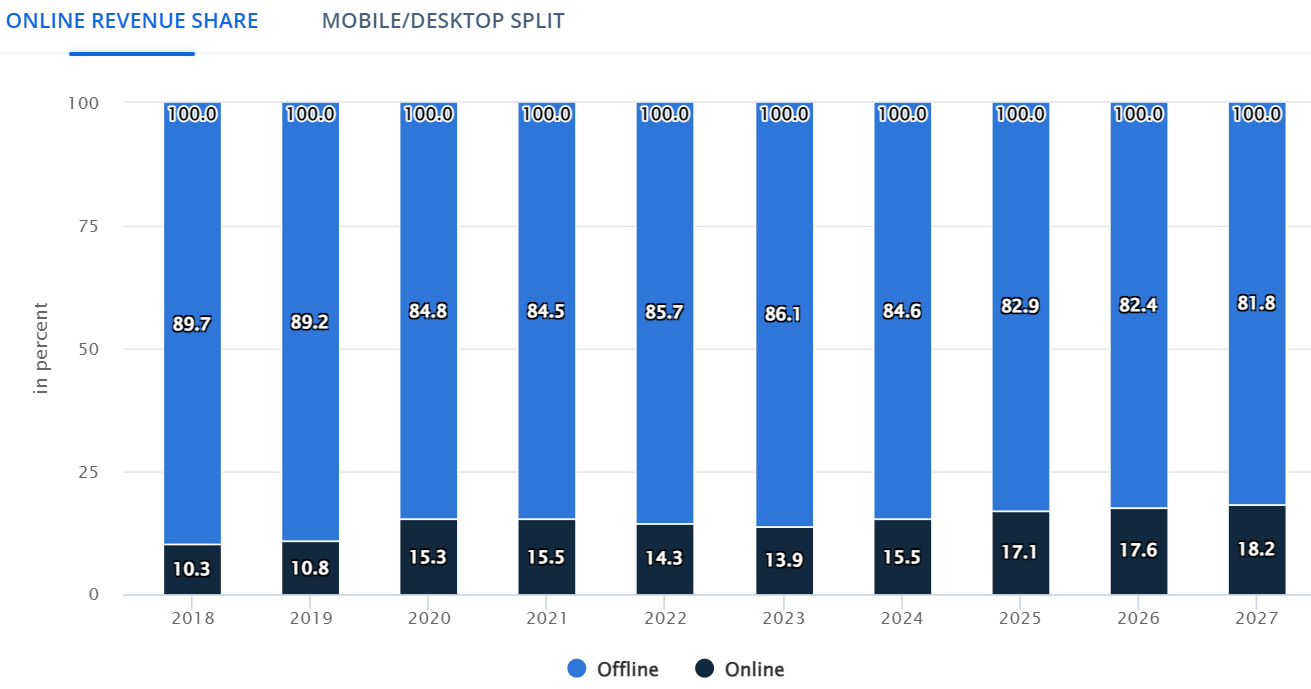

A notable trend in the luxury market is the gradual shift towards online sales. While offline sales still dominate, online revenue share is expected to grow from 13.9% in 2023 to 18.2% by 2027. This indicates the growing importance of e-commerce in the luxury sector, with LVMH likely to invest more in its digital capabilities to capture this growing online market.

A steady increase in average revenue per capita across various luxury segments until 2028. Luxury fashion and luxury leather goods are projected to be the largest contributors to this growth, aligning well with LVMH's strong position in these categories.

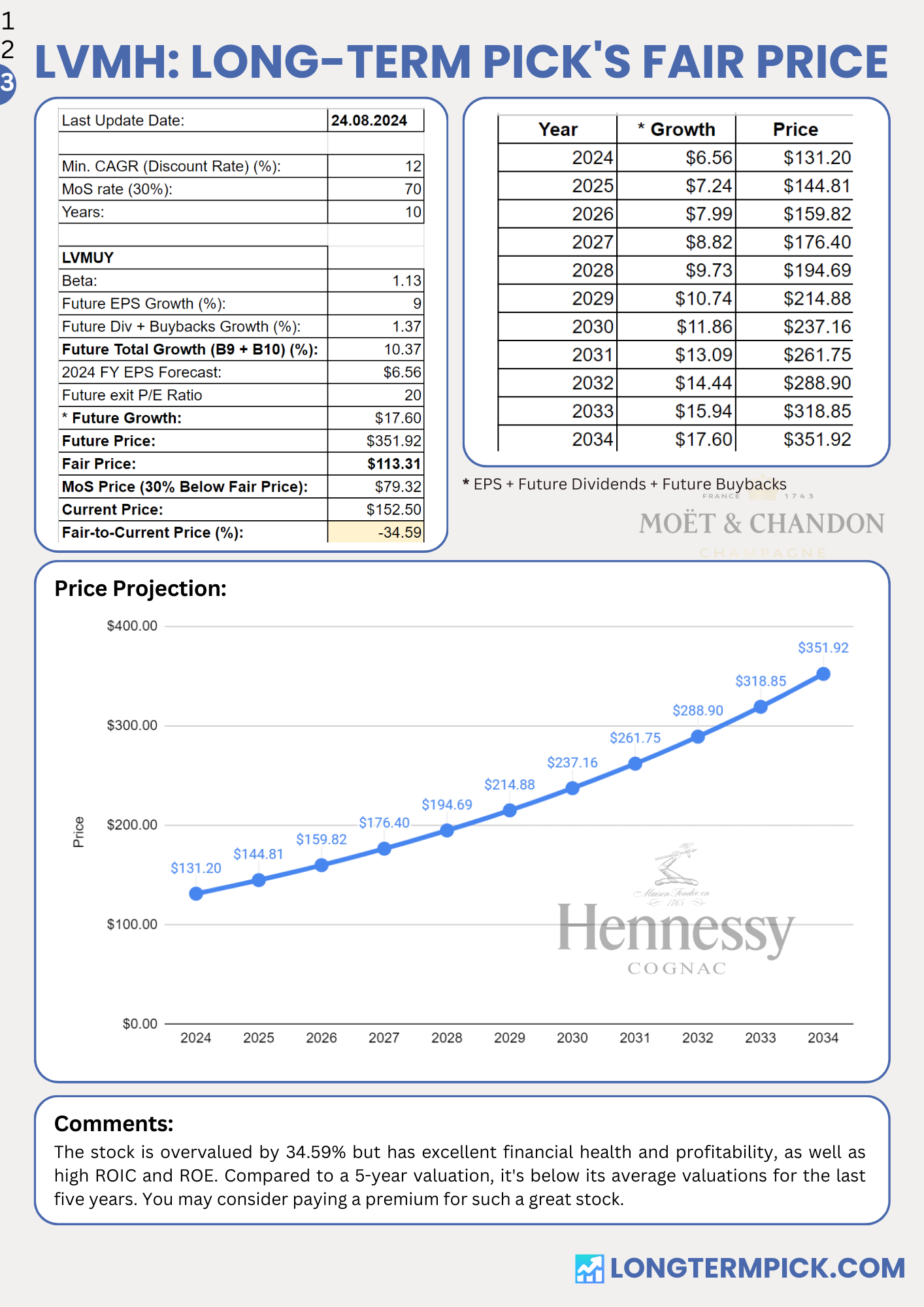

🏷️ Fair Price

Jan 30, 2025: Updated fair price valuation. The new fair price is €798.

Long-Term Pick Fair Price for LVMUY is $113.31. The current price of $152.50 is higher 34.59%. I used:

Discount Rate: 12% (S&P 500 Next 5-Yr Growth Estimates is 11.58%)

Margin of Safety: 30%

Years: 10

Future EPS Growth Rate: 9%

Future Dividend and Buyback Yield: 1.37% (5-Yr Avg)

Total Future Growth Rate: 9 + 1.37 = 10.37%

Fair-to-Current Price (%): -34.59% (Overvalued)

☑️ Checklist

Profitability:

✅ Gross margin at least 40%: 68.53%

✅ Net margin at least 10%: 16.31%

✅ Management (ROIC, ROCE, ROE, ROA): Yes (All above 10%)

✅ Piotroski F-Score: 8 of 9 (Not passed: Lower leverage YoY)

❌ Revenue surprises: No

❌ EPS surprises: No

✅ EPS growth YoY: Yes (Missed in 2020 - Covid)

Valuation and Advantage:

✅ Valuation below its 5-Yr average: Yes

✅ Does it have a moat: Yes (wide)

Shares:

✅ Insider ownership at least 5%: Yes (B. Arnault is its majority shareholder)

❌ Less shares outstanding YoY: No (But has been decreasing since 2021)

✅ Insider buys last six months: Yes (B. Arnault has been actively buying for the last few months)

Price:

✅ 1-year stock price forecast: +11.20%

❌ Next 5-Yr CAGR is above S&P 500: No (9% vs 11.58%)

✅ DCF Value: $147.92 (Undervalued 3%; 10 years, the discount rate is 10%, no termination, equity model: FCFE)

✅ Short Interest below 5%: Yes

This is not a financial or investing recommendation. It is solely for educational purposes.

Finally someone that doesn’t say LVMH is undervalued by a lot!

This company cannot grow 10%+ each year like the post Covid era growth numbers will normalize around 8-9, therefore like you said with a div of 1.5% we’re looking at 9.5-10.5% return each year without PE expansion. PE of 21 for a company that grows at 9% seems a bit excessive so I don’t even expect PE expansion at these levels.

Thanks for your work here!

Most analysts have a 1-year price target of €800 (the stock closed today at €612). It is one of the stocks that is part of my core portfolio and some substack newsletters. The most concensual opinion is that at these prices the annual return will be around 12%. Time will tell who is right. Perhaps the difference lies in the security margin you applied. In the last 10 years MC had better performance than Google, another stock i like at this prices. I think both stocks resist well to a recession cenario (increasingly likely).