💅 An Attractive Entry Point for the Largest Beauty Retailer in the US. ULTA Stock Analysis

A comprehensive analysis of Ulta Beauty, the largest beauty retailer in the United States with a diverse product range and loyal huge customer base. Provides innovative store experience.

Changelog:

Dec 10, 2024: Updated fair price valuation: $412.

💡 Investment Thesis

Ulta Beauty Inc. presents a compelling investment opportunity in the specialized beauty retail sector. As the largest beauty retailer in the United States, Ulta's narrow economic moat and unique business model combining mass and prestige products with salon services have driven consistent growth.

A robust loyalty program of over 43 million members and successful expansion into professional haircare strengthen its market position. Focus on store network expansion, e-commerce enhancement, and international growth positions it well for the future. Strong financial performance, debt-free balance sheet, and consistent share repurchases demonstrate its financial strength.

The stock offers an attractive entry point for investors seeking undervalued value stocks, despite challenges from competition and potential economic headwinds.

🧐 Company Overview

Founded in 1990, ULTA has arisen as the largest specialized beauty retailer in the United States. With a network of 1,385 stores at the end of fiscal 2023, the company offers a wide range of beauty products, including makeup, fragrances, skincare, hair care, and bath and body items. Ulta's product lineup comprises both private-label offerings and merchandise from over 500 vendors.

The company's unique proposition extends beyond retail, as it provides salon services such as hair, makeup, skin, and brow services in all of its stores.

📰 To Read: Leadership Team

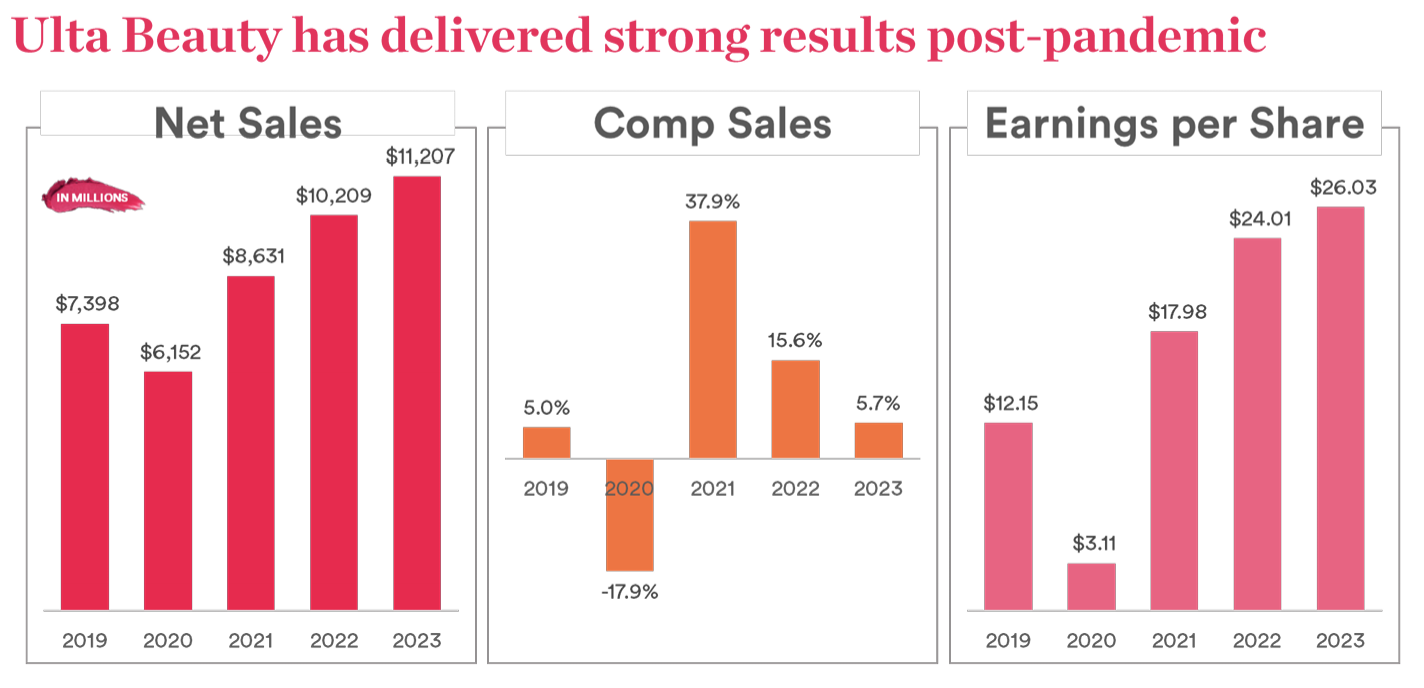

Ulta's strategic store placement, primarily in suburban strip centers, has contributed to its rapid growth and market dominance. ULTA's journey from its humble beginnings to becoming a beauty retail powerhouse is evident in its impressive sales growth, soaring from $912 million in 2007 to $11.2 billion in 2023.

🏰 Economic Moat

The company possesses a narrow economic moat, primarily derived from its strong brand intangible asset. The company's unique position in the beauty market has allowed it to thrive despite economic fluctuations and external challenges.

Ulta's transformation from a discount retailer of mass-market brands to a one-stop shop for mass, prestige, and professional beauty brands under one roof has been instrumental in creating its competitive edge. The company's consistent positive same-store sales growth since at least 2000 (excluding the pandemic-affected 2020) demonstrates the strength of its moat.

Ulta's ability to attract both mass-market and prestige beauty brands, coupled with its loyalty program of over 43 million active members, further reinforces its competitive advantage. The company's success in the professional haircare market, where it has grown about twice as fast as the market in recent years, also contributes to its narrow moat rating.

🚀 Business Strategy

Ulta Beauty's business strategy spins around several key initiatives aimed at maintaining its market leadership and driving growth. The company focuses on expanding its store network, with plans to grow from its current base of just under 1,400 stores to 1,500-1,700 stores in the long term.

Ulta's emphasis on suburban power center locations has allowed it to draw shoppers away from mall-based stores. The company is also investing heavily in its e-commerce capabilities, which now account for approximately 20% of total revenue.

Ulta's partnership with Target, involving the opening of shop-in-shops within Target stores, represents another strategic move to expand its reach and customer base. The company's first international expansion into Mexico through a partnership with Groupo Axo demonstrates its commitment to exploring growth opportunities beyond the U.S. market.

📰 To Read: Ulta Beuty at Target

💰 Profit Drivers

Ulta Beauty's profitability is driven by several factors that have contributed to its impressive financial performance. The company's ability to offer a wide range of products across various price points, from mass-market to prestige brands, allows it to serve a broad customer base and drive sales growth.

Ulta's loyalty program, with over 43 million active members, plays a crucial role in customer retention and increased spending. The company's salon services, available in all stores, not only generate additional revenue but also encourage more frequent store visits and higher spending among salon customers.

Ulta's strategic focus on the professional haircare market has proven to be a significant profit driver, with haircare products and styling tools composing 19% of its 2023 sales and representing one of its highest margin categories. The company's expansion into prestige beauty brands and its ability to attract exclusive product launches have also contributed to its strong financial performance.

✅ Advantages

Ulta Beauty's competitive advantages based on its unique market position and strategic initiatives. The company's large and growing loyalty program provides valuable customer data and encourages repeat purchases.

Ulta's wide selection of products, spanning mass-market to prestige brands, allows it to serve a diverse customer base and capture a larger share of beauty spending.

The company's store format, which combines retail products with salon services, creates a unique shopping experience that drives customer engagement and loyalty.

Ulta's strong relationships with beauty brands, including exclusive partnerships and product launches, give it a competitive edge in the market.

The company's growing e-commerce presence, accounting for approximately 20% of revenue, positions it well to capitalize on the shift towards online shopping in the beauty industry.

❌ Disadvantages

Despite its strong market position, Ulta Beauty faces several challenges and potential disadvantages. The company operates in a highly competitive beauty retail market, facing competition from both traditional retailers and e-commerce giants like Amazon.

Ulta's reliance on the U.S. market for the vast majority of its revenue exposes it to risks associated with economic fluctuations and changing consumer preferences in a single geographic region.

The company's expansion plans, including international growth and the partnership with Target, bring execution risks and may require significant investments.

📰 To Read: Ulta Beauty joins forces with Axo to launch in Mexico in 2025

Ulta's focus on prestige beauty brands, while driving higher margins, also exposes it to potential shifts in consumer spending patterns, particularly during economic downturns when customers may trade down to more affordable options.

📰 To Read: Ulta shares fall as CEO warns beauty demand is slowing

🏛️ Capital Allocation

The capital allocation strategy reflects its focus on growth and operational efficiency. The company has consistently invested in expanding its store network, opening approximately 50 stores per year in recent years.

ULTA's capital expenditures are expected to average about 3.7% of sales in the long run, primarily directed towards new store openings and maintaining existing locations. The company has also invested significantly in its e-commerce capabilities, including the opening of a second dedicated e-commerce fulfillment center in 2020 to support its growing online sales.

Ulta has maintained a strong balance sheet, operating without long-term debt, which provides financial flexibility for future investments and potential acquisitions. The company has also returned value to shareholders through stock buybacks, having repurchased more than $3 billion in shares since the beginning of 2018.

💲Current Valuation

Price/Earnings: The current P/E ratio is 12.78, which is significantly lower than the 5-year average of 23.31.

Forward P/E: The current forward P/E is 13.25, also lower than the 5-year average of 21.33.

Price/Sales: The current P/S ratio is 1.42, below the 5-year average of 2.24.

Price/Cash Flow: The current P/CF is 8.29, lower than the 5-year average of 13.21.

Price/Book: The current P/B ratio is 6.82, which is lower than the 5-year average of 9.53.

PEG Ratio: The current PEG ratio is 0.74, significantly lower than the 5-year average of 1.60. A PEG ratio below 1 typically suggests the stock may be undervalued relative to its growth prospects.

Earnings Yield: The current earnings yield is 7.82%, which is higher than the 5-year average of 3.34%. A higher earnings yield indicates better value, as investors are getting more earnings per dollar invested compared to historical norms.

Overall, these metrics consistently suggest that ULTA is currently trading at a discount compared to its historical valuation levels across multiple financial metrics.

ULTA vs. Specialty Retail industry:

Higher valuation multiples: P/E (12.76 vs 9.81), P/B (6.79 vs 1.70), P/CF (10.35 vs 6.57)

Better profitability: Net Profit Margin (11.13% vs 7.73%), ROE (58.06% vs 6.26%)

Stronger balance sheet: No Debt vs industry's 31.36 (Debt to Equity)

ULTA's premium valuation appears justified by its significantly better profitability metrics and potentially lower debt levels.

📈 Past and Future

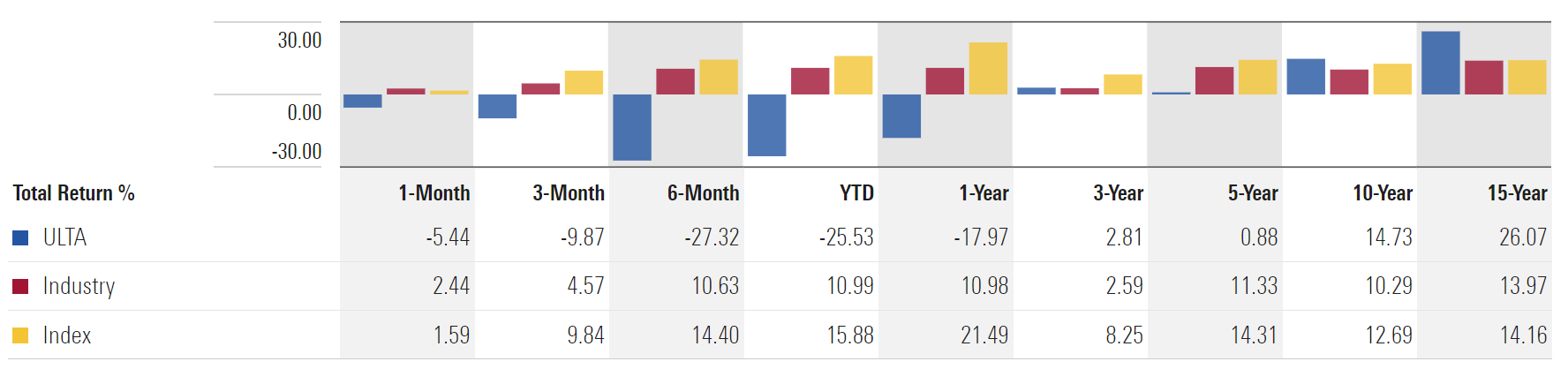

Long-term (10-year to 15-year) ULTA's performance outperforms both industry and index. Over 15 years, ULTA delivered a robust 26.07% CAGR return, substantially higher than the industry (13.97%) and index (14.16%).

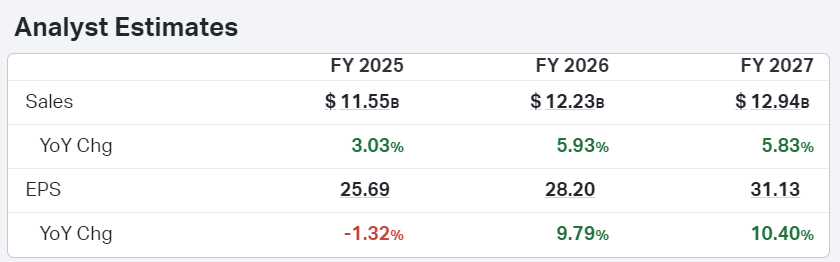

Sales are expected to grow steadily, increasing from 3.03% in FY 2025 to about 5.9% in FY 2026 and FY 2027.

EPS is projected to dip slightly (-1.32%) in FY 2025, but then show strong growth in the following years, reaching 10.40% growth in FY 2027.

Overall, analysts anticipate consistent sales growth for ULTA, with earnings rebounding and accelerating after a minor setback in FY 2025.

Analyst sentiment for ULTA is positive to neutral, with 48% Buy and 48% Hold ratings. The 1-year price forecast shows significant upside potential, with a median target of $500 (52.15% increase).

The stock currently has an average brokerage recommendation of 1.88 on a scale of 1 to 5 (Strong Buy to Strong Sell), calculated based on the actual recommendations (Buy, Hold, Sell etc.) made by 25 brokerage firms. The current ABR compares to an ABR of 1.80 a month ago based on 25 recommendations.

ULTA's projected growth vs Industry and S&P 500:

Next Year:

ULTA: 10.25% (lower than industry, slightly below S&P 500)

Industry: 20.00%

S&P 500: 11.34%

Next 5 Years:

ULTA: 8.40% (below industry)

Industry: 10.80%

ULTA's projected growth lags behind its industry for both short and long-term forecasts, and slightly trails the S&P 500's near-term outlook. This suggests potentially slower future growth compared to peers and the broader market.

🥇 Competitors

Ulta Beauty faces competition from various players in the beauty retail space. Its primary competitors include Sephora, which has been expanding its presence through a partnership with Kohl's, opening hundreds of shop-in-shops within Kohl's stores.

Traditional department stores, drugstores, and mass merchandisers also compete with Ulta in the beauty product market. E-commerce giants like Amazon pose a significant threat, particularly as they expand their prestige beauty offerings.

Specialty retailers such as Bath & Body Works and Sally Beauty compete with Ulta in specific product categories. Additionally, direct-to-consumer brands and emerging beauty startups challenge Ulta's market share by offering unique products and personalized experiences to consumers.

📊 Market Trends

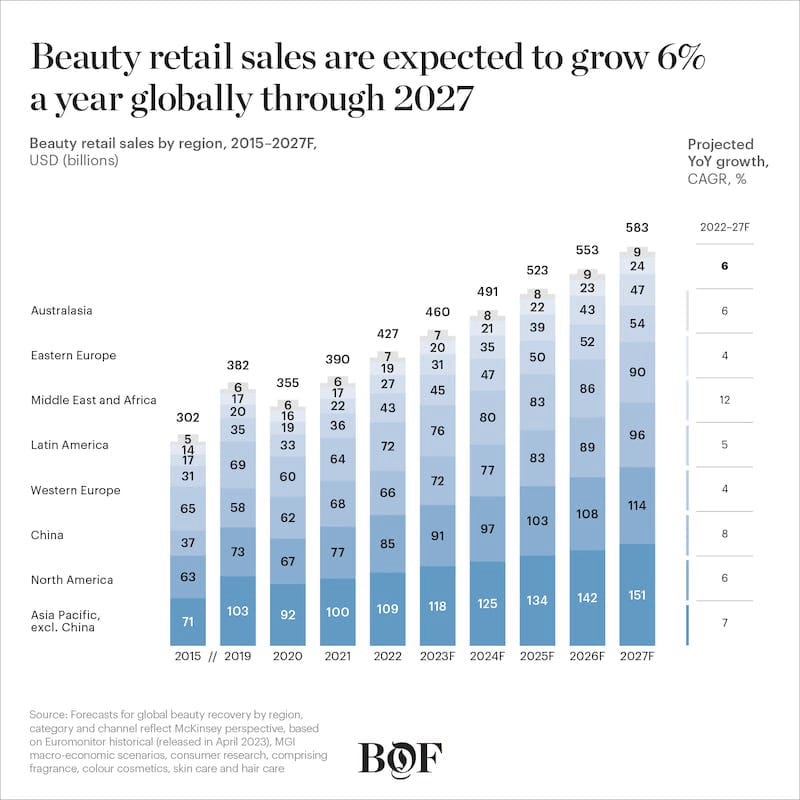

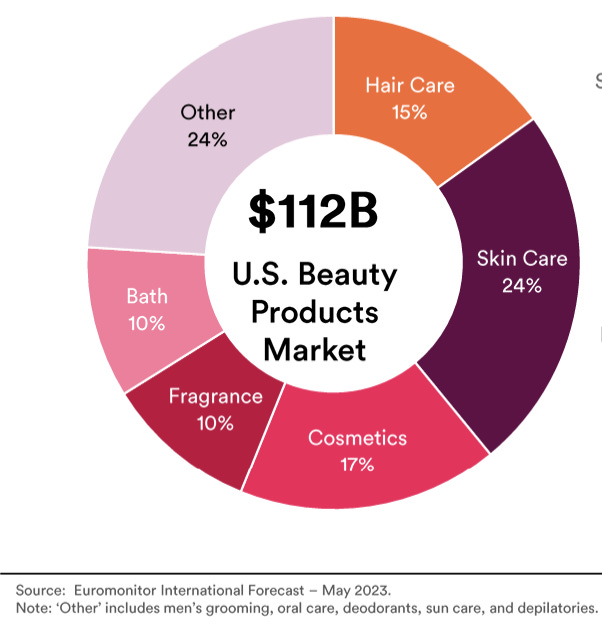

The beauty retail industry is set for significant growth, with global sales expected to increase by 6% annually through 2027. The U.S. Beauty Products Market, valued at $112 billion, shows diverse demand across categories, with Skin Care (24%), Cosmetics (17%), and Hair Care (15%) leading the market.

Geographically, China is projected to have the highest growth rate at 8% CAGR from 2022 to 2027, followed by Asia Pacific (7%) and North America (6%). This global growth trend presents expanding opportunities for companies like Ulta Beauty.

ULTA's strategic framework addresses these trends by focusing on expanding the definition of beauty, evolving the omnichannel experience, and deepening its presence in the beauty community.

The company also emphasizes operational excellence, talent cultivation, and environmental and social impact.

🏷️ Fair Price

➡️ Updated fair price valuation: https://longtermpick.com/p/updated-valuations-dec-24

Long-Term Pick Fair Price for ULTA is $436.95 which is lower 25.3% than the current price of $326.42. We used:

Discount Rate: 12% (S&P 500 Next 5-Yr Growth Estimates is 11.56%)

Margin of Safety: 30%

Years: 10

Future EPS Growth Rate: 7%

Future Buyback Yield: 3.2% (5-Yr Avg)

Total Future Growth Rate: 7 + 3.2 = 10.2%

Fair-to-Current Price (%): +25.3% (Undervalued)

☑️ Checklist

Profitability:

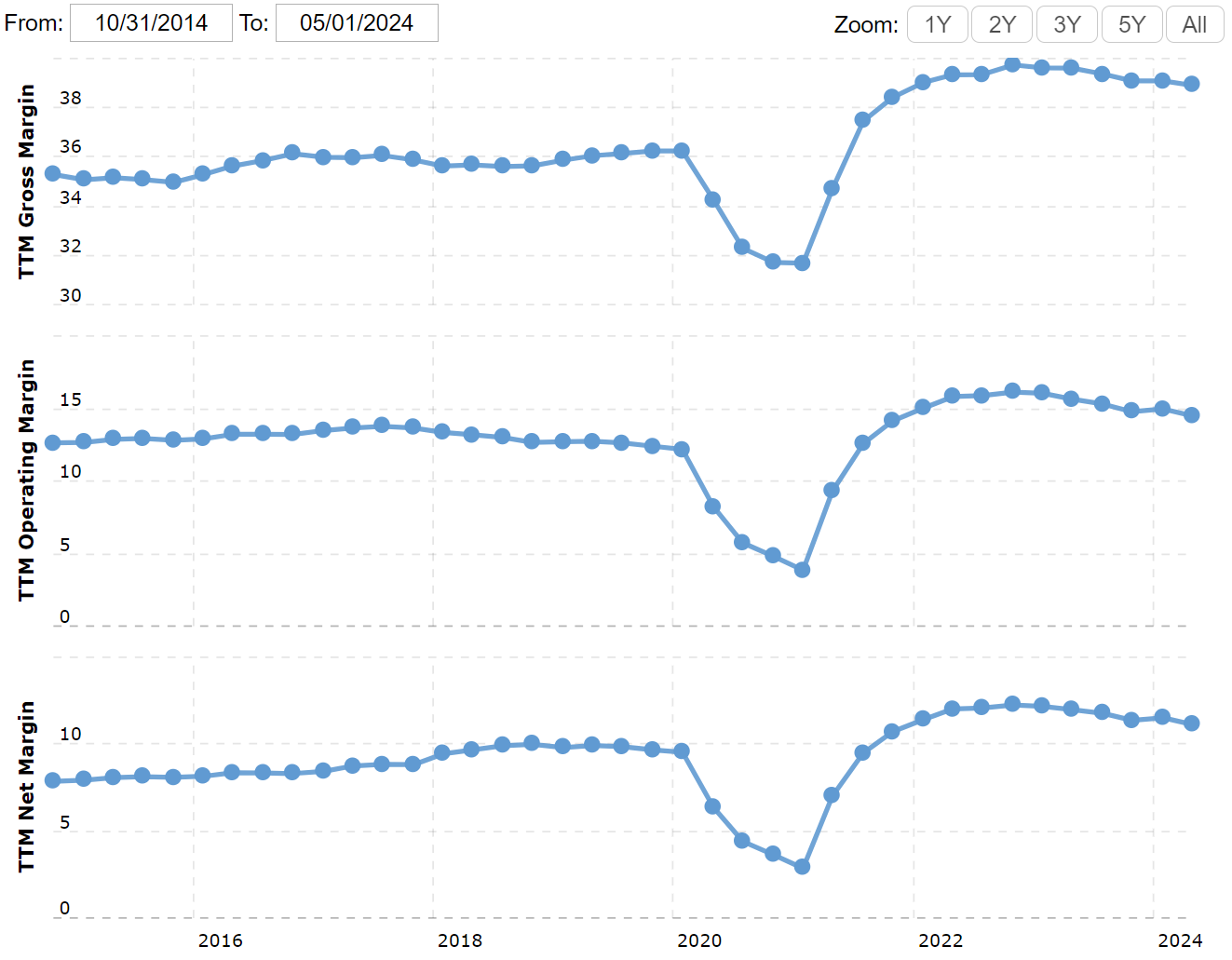

❌ Gross margin at least 40%: 38.91%

✅ Net margin at least 10%: 11.13%

✅ Management (ROIC, ROCE, ROE, ROA): Yes (All above 10%)

✅ Piotroski F-Score: 7 of 9 (Not passed: Higher ROA yoy, Higher Gross Margin yoy)

✅ Revenue surprises: Yes (Past 6 years)

✅ EPS surprises: Yes (Past 7 years)

✅ EPS growth YoY: Yes (Missed in 2020 - Covid)

Valuation and Advantage:

✅ Valuation below its 5-Yr average: Yes

✅ Does it have a moat: Yes (narrow)

Shares:

❌ Insider ownership at least 5%: No

✅ Fewer shares outstanding YoY: Yes

❌ Insider sells last three months: Yes ($446.2K)

Price:

✅ 1-year stock price forecast: +52.15%

❌ Next 5-Yr CAGR is above S&P 500: No (8.40% vs 11.68%)

✅ DCF Value: $384.65 (Undervalued 14%; 10 years, the discount rate is 10%, no termination)

✅ Short Interest below 5%: 4.35%

This is not a financial or investing recommendation. It is solely for educational purposes.