Updated Valuations: ULTA, CRM, VEEV, and LVMH

Updated valuations of companies covered by Long-Term Pick after the latest quarter earnings reports.

In December and earlier, some companies covered by Long-Term Pick (updated page) released their quarterly earnings reports. It's time to update their valuations and review the latest reports. Some explanations regarding screenshots with fair price estimates:

I marked cells that I updated as grey (after the latest earning reports).

Fair-to-Current Price and Current Price/Fair Price: 🟢 green - undervalued, 🔵 blue - fairly valued (+/- 5% is “fairly”), 🟡 yellow - overvalued.

Additionally, I included updated current valuations alongside their 5-year averages for easy comparison. I also added average future price estimates from other analysts to compare with my Base Fair Price Estimates.

Previous Updates:

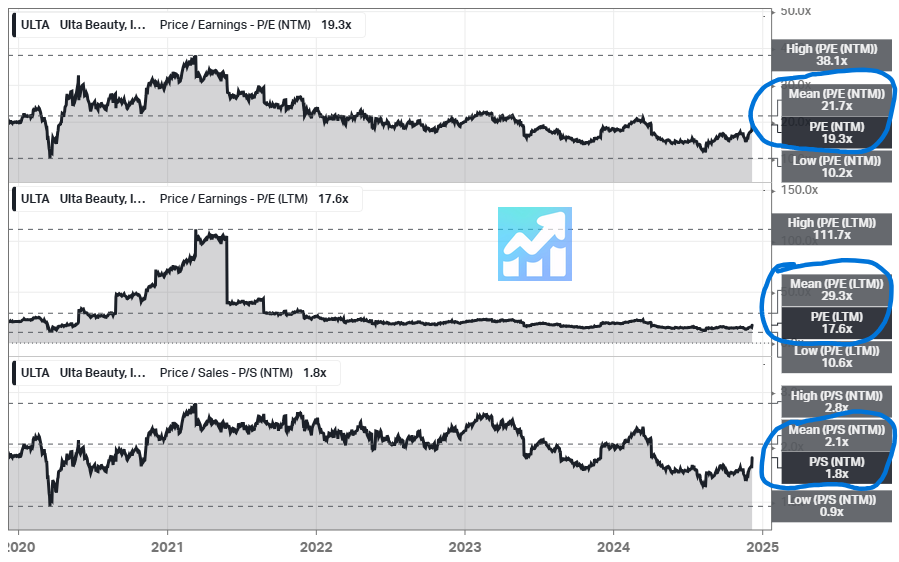

🔵 Ulta Beauty (ULTA): Fairly Valued

📝 Price Change And Analyst Notes

Since the date of my analysis, the company from Undervalued became Fairly Valued and gained 14% in price.

The EPS forecast for 2026 is lower than that for 2025, with estimates of $23.59 for 2025 compared to $23.19 for 2026. Additionally, the projected 5-year EPS growth rate has been reduced by 1%. The current PEG ratio stands at 2.39, which is above the 5-year average of 2.03.

While this great company appears to be slowing down, there are still significant share repurchases occurring. I still anticipate that ULTA will outperform the S&P 500 by about 2% in the long term (over the next 5+ years). I sold the entire position in the LTP Portfolio just before the earnings report was released.

🏷️ Updated Valuation

Latest earnings report (December 05, 2024):

✍️ Summary

Net Sales: Increased 1.7% to $2.5 billion.

Comparable Sales: Increased 0.6%.

Diluted EPS: Increased 1.4% to $5.14 per share.

Gross Margin: Decreased 20 basis points to 39.7%.

SG&A Expenses: Increased 3.2% to $682 million.

Operating Margin: 12.6% of sales, down from 13.1% last year.

Cash and Cash Equivalents: $178 million at the end of the quarter.

Inventory: Increased by 1.9% to $2.4 billion.

Operating Cash Flow: Generated $302 million year-to-date.

Capital Expenditures: $114 million for the quarter.

Share Repurchases: $267 million was returned to shareholders through the repurchase of 731,000 shares.

Loyalty Program: 44.4 million active members, a 5% increase from last year.

New Store Openings: 28 new stores opened, 2 stores closed, and 27 stores remodeled.

👍 Positive Points

Ulta Beauty reported better-than-expected sales and profitability for the third quarter, with net sales increasing by 1.7% to $2.5 billion.

The company saw a 5% increase in its loyalty program, ending the quarter with 44.4 million active members, indicating strong customer engagement.

Fragrance was the strongest category, delivering high single-digit comp growth, driven by new products and exclusive launches.

ULTA successfully launched new makeup and skincare brands, enhancing its brand portfolio and driving category growth.

The company's digital initiatives, including app adoption and enhanced online experiences, contributed to mid-single-digit sales growth in the e-commerce channel.

👎 Negative Points

ULTA faced headwinds from increased competition, particularly in the prestige beauty segment, which was impacting market share.

The makeup category saw a decrease in comp sales in the low single-digit range, primarily due to softness in mass makeup.

Gross margin decreased by 20 basis points to 39.7%, primarily due to deleverage of fixed costs and lower other revenue.

The company experienced a decline in prestige skincare, partially offsetting strong growth in body care.

ULTA anticipates continued promotional intensity during the holiday season, which may pressure margins.

💲Current Valuation

📈 Price Forecast

↗️ EPS Forecast

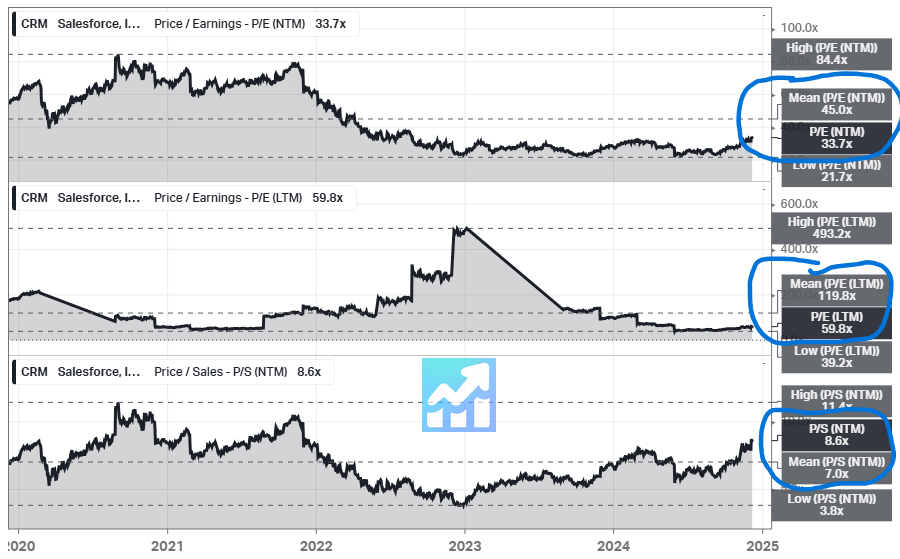

🟢 Salesforce (CRM): Undervalued

📝 Price Change And Analyst Notes

Since the date of my analysis, the company has been Undervalued and gained 56.46% in price.

I'm confident that Salesforce will achieve a 15% EPS growth rate over the next five years. The company initiated a regular share repurchase program in 2022 and began paying dividends in 2024. This could be a strong addition to your portfolio.

🏷️ Updated Valuation

Latest earnings report (December 03, 2024):

✍️ Summary

Revenue: $9.44 billion, up 8% year over year.

Subscription and Support Revenue: Grew 9% year over year.

Non-GAAP Operating Margin: 33.1%, up 190 basis points year over year.

GAAP Operating Margin: 20% for the first time in company history.

Non-GAAP EPS: $2.41, inclusive of a $0.18 charge from strategic investment adjustments.

Operating Cash Flow: $2 billion, up 29% year over year.

Free Cash Flow: $1.8 billion, up 30% year over year.

Remaining Performance Obligation (RPO): $53.1 billion, up 10% year over year.

Current RPO (CRPO): $26.4 billion, up slightly more than 10% year over year.

Share Repurchases and Dividends: $1.6 billion returned to shareholders in Q3.

Fiscal Year 2025 Revenue Guidance: $37.8 billion to $38 billion, growth of approximately 8% to 9% year over year.

Fiscal Year 2025 Non-GAAP Operating Margin Guidance: 32.9%, a 240 basis point improvement year over year.

Fiscal Year 2025 Operating Cash Flow Growth: Approximately 24% to 26%.

Q4 Revenue Guidance: $9.9 billion to $10.1 billion, up 7% to 9% year over year.

Q4 Non-GAAP EPS Guidance: $2.57 to $2.62.

👍 Positive Points

Salesforce reported strong financial performance with Q3 revenue of $9.44 billion, up 8% year over year.

The company achieved a non-GAAP operating margin of 33.1%, marking a 190 basis point improvement year over year.

Agentforce, Salesforce's new AI-driven platform, closed over 200 deals in just one week, indicating strong market demand.

Salesforce's Data Cloud was included in 8 of the top 10 deals in the quarter, showcasing its importance in AI transformations.

The company is expanding its workforce by hiring 1,400 account executives globally to meet the increased demand for Agentforce.

👎 Negative Points

Despite strong performance, CRM faces challenges with constrained growth in the United States and parts of EMEA.

The company anticipates a deceleration in license revenue growth for MuleSoft and Tableau due to tough prior-year comparisons.

Agentforce, while promising, is still in the early adoption phase and not yet a material contributor to CRPO.

Salesforce's professional services business is expected to experience a headwind in terms of revenue growth.

The company is experiencing a slightly above 8% revenue attrition rate, consistent with recent quarters.

💲Current Valuation

📈 Price Forecast

↗️ EPS Forecast

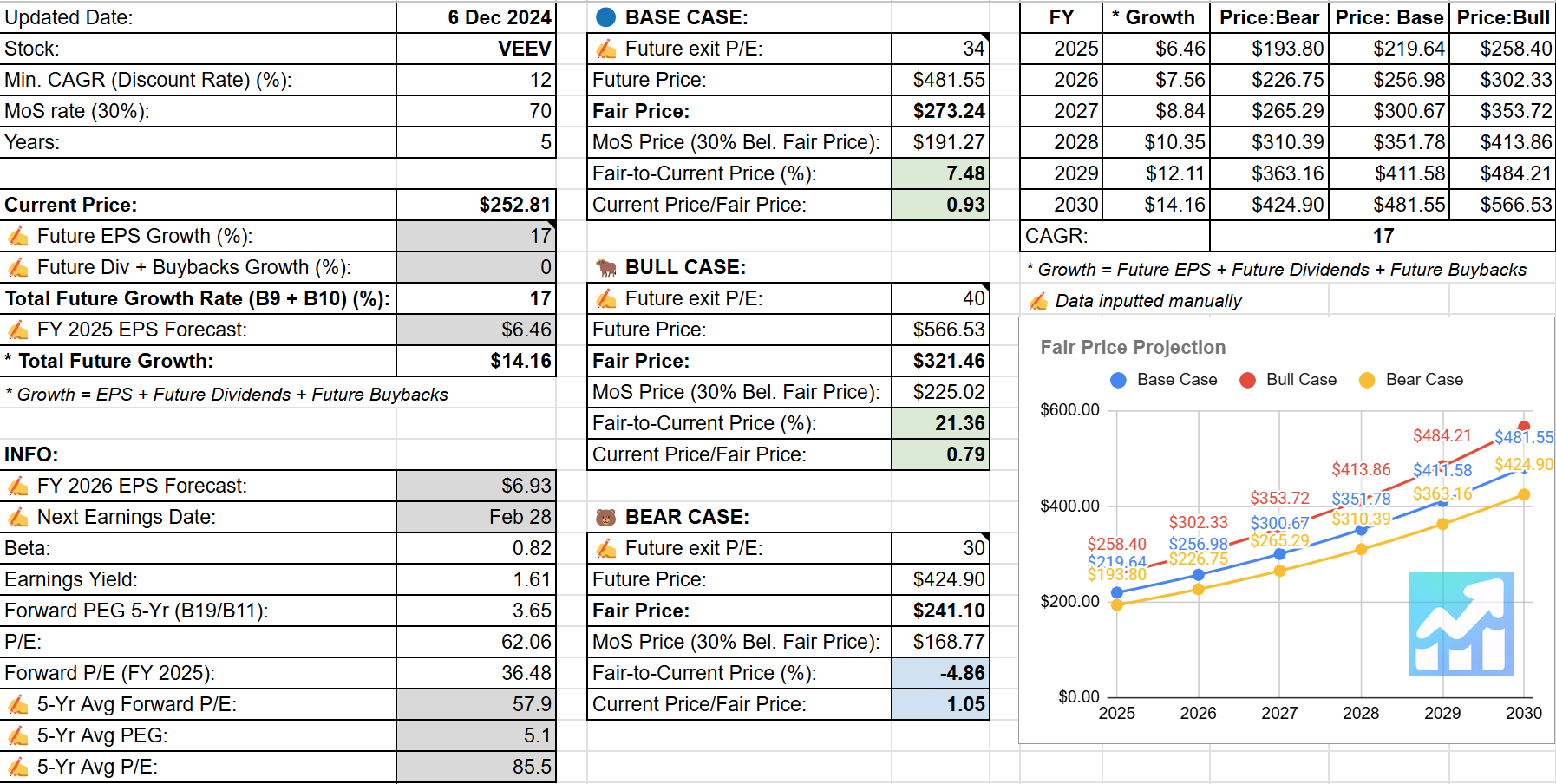

🟢 Veeva Systems (VEEV): Undervalued

📝 Price Change And Analyst Notes

Since my analysis, the company changed from Overvalued to Undervalued and gained 17.87% in price.

The company has been consistently increasing its shares outstanding, which I personally dislike, but for a growth company “it’s ok“. The market values the company very highly—read my analysis to understand the reason.

🏷️ Updated Valuation

Latest earnings report (December 05, 2024):

👍 Positive Points

Veeva Systems delivered financial results above guidance with a total revenue of $699 million and a non-GAAP operating income of $304 million.

There was broad-based adoption in all areas of Development Cloud, with significant milestones achieved in commercial, particularly with Vault CRM.

The company has seen strong interest and excitement around new innovations like the MLR Bot, which is expected to drive additional revenue.

VEEV has made progress on several large strategic partnership opportunities in the Development Cloud, indicating strong future growth potential.

The company reported a strong Q4 billings outlook, driven by a broad base of products rather than reliance on any single product.

👎 Negative Points

The migration from Veeva CRM to Vault CRM involves significant effort, particularly for larger companies with thousands of employees.

There is uncertainty regarding the potential impact of regulatory changes under a new administration, which could affect the business model.

The company faces competition from Salesforce, which is present in many of Veeva's larger customer accounts.

The impact of generative AI applications on gross margins is uncertain, though it is not expected to materially affect the company's long-term margin profile.

The CRO market, which represents a portion of Veeva's revenue, is experiencing challenges that could impact future growth.

💲Current Valuation

📈 Price Forecast

↗️ EPS Forecast

🟡 LVMH: Overvalued

📝 Price Change And Analyst Notes

Since my analysis, the company has been Overvalued and lost 8.81% in price.

LVMH's stock price dropped in 2024 due to weak sales, especially in China, where consumer spending on luxury goods has decreased. The company reported a 3% decline in sales for the third quarter, marking the first drop since the pandemic. Analysts have also lowered their price targets for LVMH, reflecting concerns about the luxury market's future. Overall, these factors have led to a challenging year for the company.

🏷️ Updated Valuation

💲Current Valuation

📈 Price Forecast

↗️ EPS Forecast

🟣 Lululemon Athletica (LULU)

LULU update is available on Patreon. For patrons, all estimated fair prices are available in a convenient XLS file. The complete Watchlist of our covered companies can be viewed graphically:

This is not a financial or investing recommendation. It is solely for educational purposes.

If you like the content, please hit the like icon, leave a comment, and share the publication with your friends and colleagues - this will motivate the author. In case you're ready to support the project financially and get access to additional materials, visit this page.

Hi Dan,

For me it is just incredible high what multiples the market is givin to Veeva, if you have a look to GAAP EPS and the last growth rates and forecasted earnings.

thanks, Dan for your analyses!