Veeva: Leading CRM Provider in Life Sciences

A comprehensive analysis of Veeva Systems (VEEV), a leading cloud software provider for the global life sciences industry.

Changelog:

Dec 10, 2024: Updated fair price valuation: $273.

With a dominant market share of over 80% in pharmaceutical CRM and rapidly expanding Vault applications, Veeva has established itself as a critical partner in the sector. The strategic transition of Veeva CRM to its own Vault platform demonstrates its commitment to innovation and independence. Veeva has an expanding product portfolio and serves 19 of the top 20 life sciences companies.

Previous analysis:

Content:

💡 Investment Thesis

🧐 Company Overview

🏰 Economic Moat

🚀 Business Strategy

✅ Advantages

❌ Disadvantages

🏛️ Capital Allocation

🥇 Competitors

📣 Recent News

⏮️ Past

📶 Future

💲Current Valuation

🏷️ Fair Price

☑️ Checklist

💡 Investment Thesis

Strong dominant position in the life sciences cloud software market. The company's transition of Veeva CRM to its own Vault platform demonstrates strategic independence and potential for enhanced integration across its product collection. High customer retention rates.

The company's debt-free balance sheet and strong cash flow provide financial flexibility for continued R&D investments and strategic acquisitions. While VEEV trades at premium multiples compared to broader software peers, its current valuation is below historical averages on several key metrics, but the estimated fair price for the Base Case is not so attractive.

As the leader in CRM solutions for the life sciences industry with a wide economic moat, Veeva Systems can be a compelling stock to add to your watchlist.

🧐 Company Overview

Incorporated: 2007

Sector: Healthcare

Industry: Health Information Services

Stock Style: Mid Growth

Market Cap: $35.29 Bil.

Earnings Date: Dec 4 - Dec 9, 2024Veeva Systems is a leading provider of cloud-based software solutions for the life sciences industry. Founded in Pleasanton in 2007, California, the company offers a comprehensive set of products including Veeva CRM, Veeva Vault, Veeva Network, and Veeva data services. These solutions serve various aspects of the life sciences sector, from customer relationship management to content and information management, as well as customer master and product data management.

Veeva's flagship product, Veeva CRM, operates on salesforce.com's SaaS platform. However, Veeva announced in late 2022 that it would migrate the product to its own Vault platform. Customer migration began in 2024 and existing users can use CRM on Salesforce’s platform until 2030. This move away from Salesforce gives the company the independence to run all its offerings. Veeva also announced an expanded business partnership with Accenture to help customers optimize their processes and leverage new innovations as part of their migration to Vault CRM.

The company has also expanded its offerings with the Veeva Commercial Cloud, which includes innovative features like Veeva CRM Engage Webinar and Veeva Vault PromoMats Brand Portal. These additions enhance digital asset management capabilities within the Veeva ecosystem.

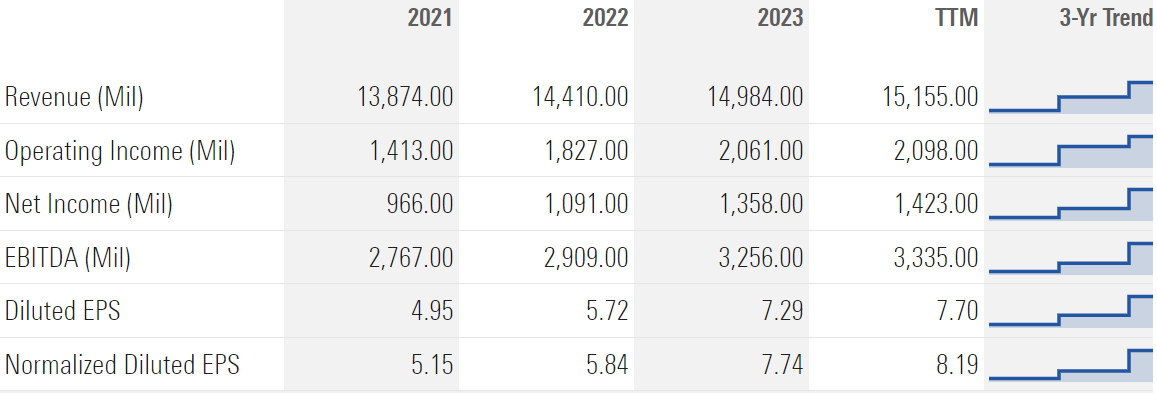

In fiscal year 2024, Veeva Systems reported total revenues of $2.36 billion, marking a 10% increase from the previous year. Subscription services accounted for 80.4% of net sales, while professional services and other revenues formed the remaining 19.6%. This financial performance emphasises Veeva's strong position in the market and its ability to generate consistent growth.

Peter Gassner (2007-present, 59) is the co-founder and CEO of the company. Prior to this role, he worked as Senior Vice President of Technology at Salesforce (2003-2005), and as Chief Architect and General Manager at PeopleSoft, a provider of enterprise application software (1995-2003). He also worked as a Staff Developer at IBM (1989-1994). On the board of directors for Zoom Video Communications (2015-present) (Public) and Guidewire Software (2015-2019) (Public). Peter Gassner has a Bachelor of Science in Computer Science from Oregon State University.

🏰 Economic Moat

Veeva Systems has a wide economic moat, primarily due to high customer switching costs and its dominant position in the life sciences software market. The company's solutions are deeply integrated into its customers' critical operations, making it difficult and costly for them to switch to competitors. Veeva's industry-specific focus has allowed it to accumulate extensive knowledge and experience, creating a significant barrier for generic CRM providers to compete effectively.

The company's market position in the global pharmaceutical CRM space has grown impressively, from about one-third of global pharmaceutical sales representatives using Veeva CRM in 2013 to over 80% by 2022. This substantial market penetration further strengthens Veeva's competitive advantage and makes it challenging for new entrants to gain a position in the industry.

Moreover, Veeva's strategy of offering additional applications to existing customers has increased the average add-on penetration rate from less than 10% in 2015 to 50-60% by 2021. This approach not only grows value per contract but also enhances customer stickiness, further widening the company's economic moat.

🚀 Business Strategy

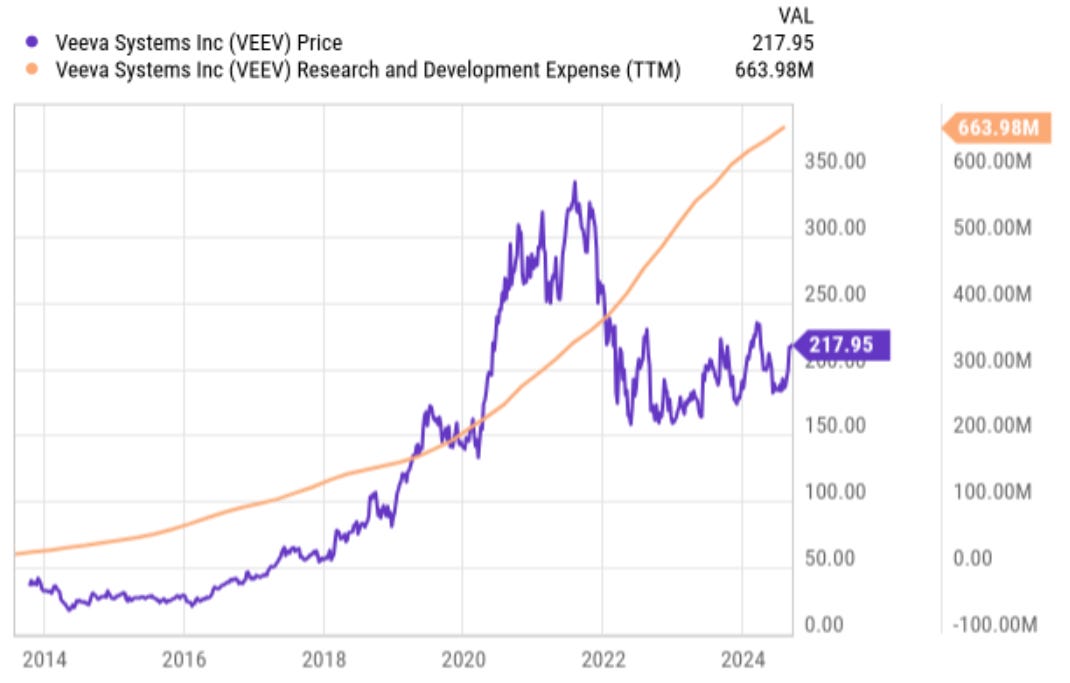

I view their business strategy as focusing on continuous innovation and expansion of its product portfolio. The company invests heavily in research and development to enhance existing solutions and develop new applications that address evolving industry needs. This focus on R&D is evident in the 10.7% increase in R&D expenses during the first quarter of fiscal 2025, primarily driven by employee compensation-related costs.

The company's strategy also involves expanding into new verticals within the life sciences industry. For instance, Veeva has been trying to get into medical devices and diagnostics companies, as well as consumer products and chemical industries. This diversification helps Veeva enter new markets and reduce its reliance on a single sector.

Veeva is also pursuing strategic partnerships and acquisitions to enhance its offerings. In June 2024, the company announced partnerships with Vita Global Sciences and Hangzhou Tigermed Consulting to implement Veeva Vault EDC. I believe this demonstrates the company's dedication to expanding its customer base and enhancing clinical data management processes.

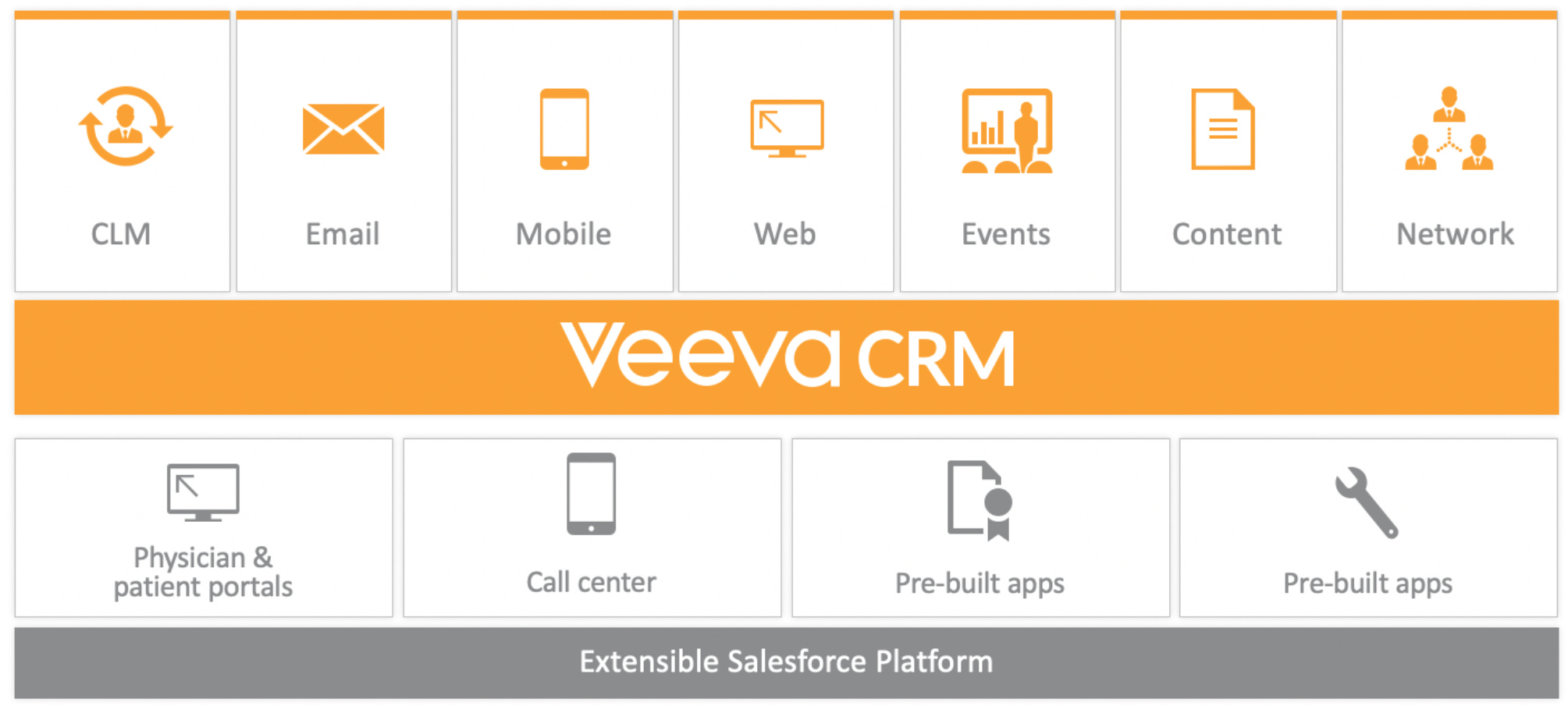

Core business segments:

Veeva Vault: This segment includes a suite of content management applications designed to streamline regulatory, quality, and clinical processes. Veeva Vault allows life sciences companies to manage documents, submissions, and other critical data in a secure and compliant manner. It plays a significant role in the management of clinical trials, regulatory submissions, and post-market surveillance.

Veeva CRM: This segment focuses on providing a comprehensive CRM solution specifically for the life sciences industry. Veeva CRM helps pharmaceutical and biotech companies manage their customer interactions, sales force effectiveness, and marketing strategies. It enables better communication with healthcare professionals by providing insights and data analytics.

Veeva Data and Analytics: This segment includes various data solutions, such as Veeva OpenData, which provides accurate and comprehensive healthcare professional data, and Veeva Network, a customer master data management solution. These tools enable life sciences organizations to make data-driven decisions and enhance their marketing efforts.

Veeva Clinical: This segment is dedicated to supporting the clinical development process. It includes applications for study design, patient recruitment, trial management, and data collection. By offering tools that streamline these processes, Veeva Clinical helps life sciences companies bring their products to market faster and more efficiently.

Veeva Commercial Cloud: This segment encompasses applications that support commercial operations, including marketing, sales, and medical affairs. Veeva’s Commercial Cloud solutions aim to enhance collaboration, improve customer engagement, and elevate the overall efficiency of commercial teams within life sciences organizations.

✅ Advantages

Comprehensive and adapted product portfolio for the life sciences industry. The company's solutions are specifically designed to address the unique challenges and regulatory requirements of this sector. This industry-specific focus allows Veeva to provide more value to its customers compared to generic, one-size-fits-all solutions.

Strong customer adoption and retention rates. The company has successfully penetrated the market, with its solutions being used by 19 out of the top 20 life sciences companies. This high adoption rate among industry leaders shows a powerful approval for Veeva's products and helps attract new customers.

The company's financial strength. As of the first quarter of fiscal 2025, Veeva had a strong liquidity position with cash and cash equivalents and investments of $4.77 billion. This strong financial position allows Veeva to invest in product development, pursue strategic acquisitions, and weather potential economic downturns.

Scalable business model. Veeva's subscription model allows for predictable revenue and flexibility in pricing, making it easier for customers to scale their usage according to their needs. This model promotes long-term customer retention and satisfaction.

Strong customer relationships. Veeva has built a reputation for excellent customer service and support. Its ability to engage closely with clients and respond to their needs stimulates loyalty and encourages long-term relationships.

❌ Disadvantages

The company operates in a highly regulated industry, and any unfavorable regulatory changes could impact its growth trajectory. The life sciences sector is also experiencing a slowdown in growth opportunities as the market saturates, which could affect Veeva's CRM sales growth rate in the future.

Veeva is also vulnerable to macroeconomic factors affecting the life sciences industry. Economic downturns, reduced revenue, and productivity challenges in the sector can directly impact their performance. The company's industry-specific focus, while a strength, also makes it more susceptible to sector-specific fluctuations.

Rising operational costs. In the first quarter of fiscal 2025, the company's total operating expenses increased by 7.8% year over year. Management expects these expenses to continue rising, primarily due to employee compensation-related costs and increased personnel to support sales and marketing efforts.

Dependency on key clients. A significant portion of Veeva's revenue may come from a limited number of large customers. Losing any key client could impact revenues substantially.

Customer retention and satisfaction. Veeva's business model relies on long-term subscriptions. Maintaining high customer satisfaction to avoid churn is critical amidst competitive pressures and evolving customer needs.

Talent acquisition and retention. The tech industry is competitive, and attracting and retaining skilled talent is vital for innovation and maintaining service quality.

🏛️ Capital Allocation

VEEV maintains a strong focus on research and development. The company consistently invests about 20% of its total sales in R&D to expand its collection of applications. This investment has paid off, with the average number of products per user for commercial cloud and Vault increasing from 2.91 to 4.02 and 2.10 to 2.71, respectively, over the last five years.

In terms of external investments, Veeva has historically made small, complementary software acquisitions. For instance, in 2019, the company purchased Crossix for $427 million and Physicians World for $55 million, both of which enhanced its Commercial Cloud offerings.

Veeva does not pay a dividend, which is in accordance with industry practices. The company focuses on reinvesting its profits to increase growth and innovation. This approach is appropriate given Veeva's status as a fast-growing company in a dynamic industry.

It's worth noting that the company has been increasing shares outstanding for the last decade, diluting shareholder yield.

🥇 Competitors

In the CRM space, the company competes with other cloud-based solution providers like Salesforce and IQVIA. For its Commercial Cloud and Veeva Vault application products, Veeva competes with established players such as Oracle and Microsoft Corporation, as well as smaller application providers.

The company also faces potential competition from cloud-based applications or platforms that are not specific to life sciences, such as Amazon Web Services, which some customers may choose for certain functions.

As you can see from the table above, VEEV is trading with some premium regarding its competitors. Again, I don't like the pretty high PEG ratio.

I would like to compare Veeva with IQVIA separately as the biggest direct competitors in the biotech/pharma CRM space:

Actually, now we can see why VEEV is trading higher in terms of valuation (see the table above). Also, let's take a look at shares outstanding and stock buybacks (I pay attention to this):

📣 Recent News

New Service Center in Veeva Vault CRM Suite Unifies Sales and Service (Aug 27, 2024)

Vault CRM Service Center is now available for life sciences inside sales, contact center, and hybrid reps. Vault CRM Suite to unify sales, marketing, medical, and service for true customer-centricity.

Veeva Systems' Vault EDC to Boost Vita Global's Data Management (Jun 19, 2024)

Veeva Systems announced a partnership with Vita Global Sciences that will help the latter improve its clinical data management processes as well as collaboration with key trial stakeholders.

Veeva Systems' Vault EDC to Boost Tigermed's Workflow (Jun 06, 2024)

Veeva Systems announced that Hangzhou Tigermed Consulting Co., Ltd. (Tigermed) has selected Veeva Vault EDC as its technology foundation for modern electronic data capture (EDC). With Vault EDC, Tigermed expects to simplify complex data management for faster study builds and mid-study amendments with zero downtime.

Veeva Systems Announces Vault Basics for Biotechs (May 16, 2024)

Veeva Systems announced the availability of Vault Basics, a new offering that includes technology, training, and support designed for biotechs.

⏮️ Past

In Q2 2025, Veeva Systems surpassed its guidance, achieving $676 million in revenue and $280 million in non-GAAP operating income. The company saw significant advances across major areas, notably with the expansion of Veeva Site Connect and the launch of the Service Center within the CRM suite. The quarter included 14 CRM wins, with strong adoption of Vault CRM since its April release. Despite some delays in service projects, the commercial content and Crossix segments drove an increased outlook for the year. Executives emphasize continued focus on product innovation and customer success.

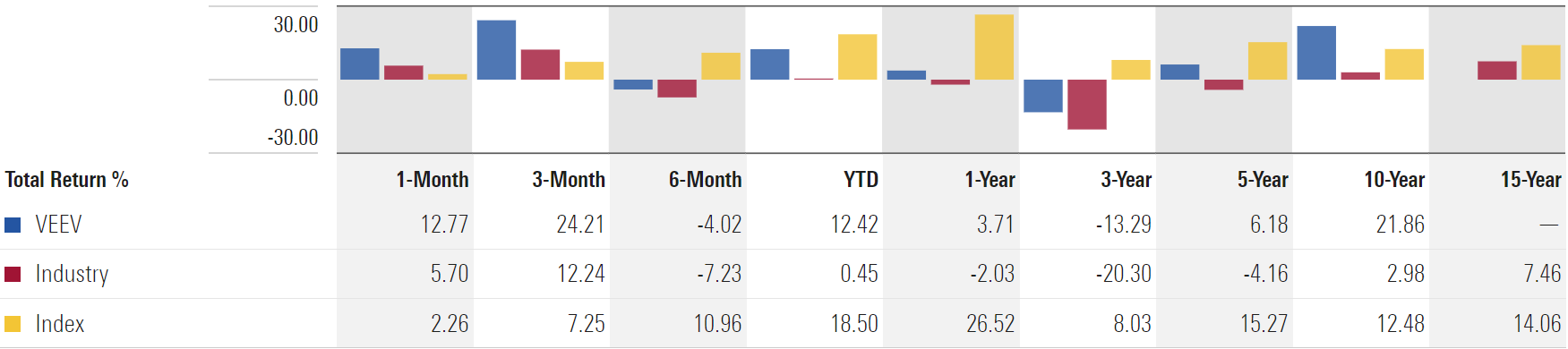

VEEV has demonstrated strong long-term performance, outperforming its industry over 10-year and 5-year periods with CAGR returns of 21.86% and 6.18% respectively. However, VEEV underperformed the index in the mid-term, with negative 3-year returns (-13.29%) compared to the index's positive performance.

From my perspective, Veeva's mid-term underperformance can be attributed to several factors. Industry-wide challenges in life sciences, including limited biotech funding and high interest rates. Rising operational costs and intensifying competition in the software market have pressured margins and market share. The transition of Veeva's CRM to its own platform may have created investor uncertainty. As Veeva's core products approach market saturation, slower growth in established lines could be affecting overall revenue.

📶 Future

Based on the last company's presentation, Veeva Systems projects continued growth, particularly in subscription revenues. Despite a slight decline expected in service revenue, Veeva anticipates improved profitability through operational efficiency. The company is standardizing customer contract terms and investing in product development, especially in Veeva Vault and data cloud solutions.

While near-term growth may vary across segments, Veeva's long-term outlook emphasizes balanced growth in high-value areas, strong cash flow, and sustained profitability.

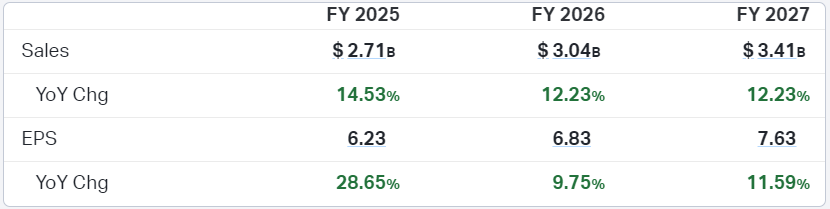

The analyst estimates show a positive growth trajectory over the next three fiscal years. Sales are projected to increase steadily, rising from $2.71 billion in FY 2025 to $3.04 billion in FY 2026, and reaching $3.41 billion in FY 2027. This represents year-over-year growth rates of 14.53% for FY 2025, followed by 12.23% for both FY 2026 and FY 2027.

Earnings per share (EPS) are also expected to grow, starting at $6.23 in FY 2025, increasing to $6.83 in FY 2026, and further rising to $7.63 in FY 2027. The year-over-year EPS growth is projected to be particularly strong at 28.65% for FY 2025, followed by more moderate increases of 9.75% and 11.59% in FY 2026 and FY 2027 respectively.

Analyst sentiment for Veeva Systems is mainly positive, with a consistent pattern of recommendations over the past three months. The majority of analysts rate the stock as a "Strong Buy," with a smaller number giving "Buy," "Hold," and "Sell" recommendations. This distribution has remained stable recently.

Regarding price targets, the average from 23 analysts is $230.65, suggesting a 4.87% upside from the last closing price of $219.94. There's a wide range in price targets, from a high of $281.00 (27.76% upside) to a low of $173.00 (21.34% downside).

💲Current Valuation

Honestly, I don't like the high PEG ratio, since I pay close attention to this ratio. It's higher than the 5-year average. But Price/Sales, Price/Forward Earnings, and Price/Cash Flow are lower than the 5-year averages.

Currently, VEEV is trading at valuation multiples that are generally lower than its 5-year averages, suggesting the stock may be relatively undervalued compared to its historical levels. The current earnings yield is above the 5-year average.

🏷️ Fair Price

➡️ Updated fair price valuation: https://longtermpick.com/p/updated-valuations-dec-24

The Long-Term Pick's Fair Price (Base Case) for VEEV is $181.36. The current price of $217.95 is higher by 20.17%.

Fair-to-Current Price (%): -20.17%

Current Price/Fair Price: 1.20

I used:

Discount Rate: 12% (S&P 500 Next 5-Yr Growth Estimates is 11.90%)

Margin of Safety: 30%

Years: 10

Future EPS Growth Rate: 13.70%

Future Dividend and Buyback Yield: 0%

Total Future Annual Growth Rate: 13.70 + 0 = 13.70%

For the Base Case, the Future Expit P/E is 25. 5-Yr average P/E ratio is 53, the lowest P/E during the last ten years was 20 in 2018 (I took 20 for my Bear Case).

I have made my Fair Price calculation after writing all the text above, and I thought the Fair Price would be fairly valued. It's also worth noting that VEEV regularly increases its shares outstanding, so the Fair Price could potentially be even lower.

☑️ Checklist

Profitability:

✅ Gross margin at least 40%: 73%

✅ Net margin at least 10%: 24%

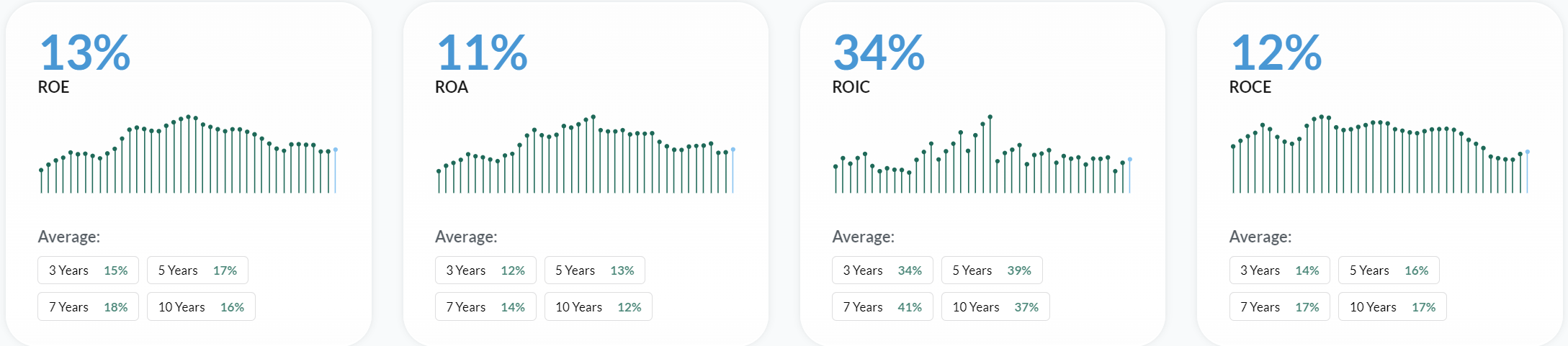

✅ Management (ROIC, ROCE, ROE, ROA): Yes (All above 10%)

❌ Piotroski F-Score: 6 of 9 (Not passed: Higher ROA YoY, Less Shares Outstanding YoY, Higher Asset Turnover YoY)

✅ Revenue surprises in last 10 years: Yes (Based on TradingView's data)

✅ EPS surprises in last 10 years: Yes (Based on TradingView's data)

✅ EPS growth YoY 10 years: Yes

Valuation and Advantage:

✅ Valuation below its 5-yr average: Yes (But not the PEG Ratio)

✅ Does it have a moat: Yes (wide)

Shares:

✅ Insider ownership at least 5%: Yes (8.30%)

❌ Less shares outstanding YoY: No

❌ Insider buys last six months: No

Price:

❌ 1-year stock price forecast is above 10%: +4.87%

✅ Next 5-Yr CAGR is above S&P 500: Yes (13.75% vs 11.90%)

❌ DCF Value: $112.70 (Overvalued by 48%; 10 years, discount rate: 10%, terminal growth: 3%, equity model: FCFE)

✅ Short Interest below 5%: Yes (1.31%)

This is not a financial or investing recommendation. It is solely for educational purposes.