ASML: Sole EUV Systems Provider Currently Undervalued

ASML is the sole provider of Extreme Ultraviolet (EUV) lithography systems, a technology that has revolutionized chip production.

Changelog:

Jan 30, 2025: Updated fair price valuation. The new fair price is $1,053.

Jan 14, 2025: Overview: Revenue Growth Target for FY25, Securities Class Action Lawsuit, Increased R&D Spending, and Challenges from Geopolitical Tensions.

ASML Holding NV is a Dutch company that has become essential to the global semiconductor industry. Specializing in photolithography systems, ASML provides the machines that are crucial for producing advanced microchips. Their cutting-edge Extreme Ultraviolet (EUV) technology enables the production of smaller, faster, and more efficient chips, making ASML a critical supplier for companies like Intel, TSMC, and Samsung. As the only company offering EUV systems, ASML holds a unique position, making it indispensable for industries ranging from smartphones to artificial intelligence.

Previous publication:

📢 Dear reader,

Feel free to follow Long-Term Pick on Twitter (X), Facebook, and Telegram, where you can find more interesting short content and, hopefully, some valuable insights. I would also be delighted to have you as a paid patron on Patreon, where you can access the Long-Term Pick Portfolio, Watchlist, and premium publications.

Content:

💡 Investment Thesis

🧐 Company Overview

🏰 Economic Moat

🚀 Business Strategy

✅ Advantages

❌ Disadvantages

🏛️ Capital Allocation

🥇 Competitors

📣 Recent News

⏮️ Past

📶 Future

💲Current Valuation

🏷️ Fair Price

☑️ Checklist

✍️ Due Diligence

💡 Investment Thesis

With no direct competitors in EUV, ASML’s unique position is vital to its customers like TSMC, Intel, and Samsung. As of the latest quarter in 2024, ASML reported a significant backlog exceeding €36 billion, ensuring strong demand for its products over the coming years.

The company continues to maintain high margins. Despite challenges from cyclical demand and geopolitical risks, I expect ASML’s ability to innovate and provide critical systems for advanced chipmaking positions it well for future growth. For long-term investors, ASML offers a compelling opportunity due to its dominance in a high-demand industry. Strong financial performance. Their role in the semiconductor value chain is crucial, and its strategic importance will only grow as the world continues to rely on more advanced technology.

Currently trading below its 5-year averages and more than 30% below my fair price estimate.

⬇️ Download Quick Analysis in PDF (Free)

🧐 Company Overview

Incorporated: 1984 Sector: Technology Industry: Semiconductor Equipment & Materials Stock Style: Large Growth Market Cap: $283.67 Bil Earnings Date: Jan 29, 2025ASML is a Dutch multinational corporation and a global leader in the development and production of photolithography systems used for the manufacturing of microchips. Founded in 1984, the company has grown to become a critical supplier to the world's largest semiconductor foundries, including Taiwan Semiconductor Manufacturing Company (TSMC), Intel, and Samsung. ASML’s machines use cutting-edge technology to etch complex circuits onto silicon wafers, which are then used to create microchips found in various electronic devices like smartphones, computers, and AI systems. The company plays a pivotal role in advancing the performance of chips and, consequently, many technological devices.

To Read: About ASML

ASML is the sole provider of Extreme Ultraviolet (EUV) lithography systems, a technology that has revolutionized chip production. EUV lithography enables the production of smaller, more efficient, and more powerful chips. ASML’s main products, including EUV and Deep Ultraviolet (DUV) lithography machines, are critical for semiconductor manufacturing, making it an indispensable player in the tech industry.

ASML is led by CEO Christophe Fouquet, who took over in 2024 following the successful tenure of Pieter Wennink. Fouquet has been with the company for over 15 years, holding various key roles. Under Fouquet's leadership, the company is expected to continue its long-term focus on innovation, driven by investments in research and development. His background positions him well to maintain ASML’s leadership in the semiconductor market.

🏰 Economic Moat

ASML has a wide economic moat. One of the key components of ASML's moat is its unrivaled technological capability in producing lithography machines, particularly its EUV systems. These machines are essential for manufacturing the most advanced semiconductor chips used in everything from AI and 5G technologies to consumer electronics. ASML's EUV machines are unmatched, with no other company able to produce similar systems, giving ASML a near-monopoly in this market.

High switching costs. Its customers—TSMC, Intel, and Samsung—have invested heavily in redesigning their fabs (factories) to accommodate ASML’s technology. Any switch to a competitor’s equipment would require significant changes to their production lines, making it economically unfeasible. This creates a powerful lock-in effect that strengthens ASML’s position in the market. Moreover, the company’s long-standing relationships with suppliers and partners provide another layer of protection for its moat.

Also, significant intangible assets in the form of its patents, extensive R&D expertise, and decades of internal know-how. This expertise allows ASML to continuously improve its technology, providing customers with increasingly productive machines.

🚀 Business Strategy

Their business strategy is based on continuous innovation and maintaining its technological leadership in lithography. The company’s R&D budget, which exceeds EUR 4 billion annually, is central to this strategy. For instance, the company is working on High-NA EUV systems, the next generation of lithography machines, which are expected to become key tools for manufacturing even more advanced semiconductor chips.

Another aspect of ASML’s strategy is its outsourcing model. ASML operates primarily as an assembler, sourcing key components from suppliers and focusing on integrating these parts into its highly complex lithography machines. This allows ASML to remain flexible and manage costs more effectively, especially in a cyclical industry like semiconductors. By partnering with specialized suppliers, ASML can maintain the highest quality standards while keeping production efficient. This approach has helped ASML scale its operations and maintain profitability even in periods of market volatility.

Worth also noting recurring revenue through service contracts. Once a customer purchases a machine, it enters into a long-term relationship with ASML. These machines have a lifespan of over 30 years, and ASML continues to generate service revenue through maintenance, software upgrades, and performance enhancements. This not only boosts profitability but also strengthens customer relationships, as customers rely on ASML for ongoing support to optimize their machines’ performance. As machines get more complex, the potential for service revenue grows, creating a long-term, sustainable revenue stream.

✅ Advantages

Technological leadership in EUV lithography. Being the sole producer of EUV systems gives ASML a near-monopoly in the market for cutting-edge semiconductor manufacturing. This unique position allows the company to set high prices for its machines, some of which sell for up to EUR 300 million each. ASML’s EUV systems are essential for the production of advanced microchips, giving it a critical role in the global technology supply chain. The demand for these chips is expected to continue growing, fueled by innovations in artificial intelligence, 5G, and other emerging technologies.

Strong customer relationships. The company’s clients, such as TSMC, Intel, and Samsung, have made substantial investments to incorporate ASML’s technology into their production lines. This creates a high level of dependency on ASML, as switching to another supplier would involve costly redesigns of their fabs. Additionally, ASML’s machines are highly complex, and customers rely on the company for service and upgrades, further strengthening these relationships. This lock-in effect creates a strong barrier to entry for potential competitors.

Ability to generate recurring revenue. Its machines have a long operational life, and the company continues to profit from them through service agreements, maintenance, and software upgrades. This recurring revenue provides ASML with financial stability, even during periods when new machine sales may slow down. The company’s focus on improving service margins ensures that this revenue stream will grow over time, contributing to long-term profitability.

❌ Disadvantages

The cyclical nature of the semiconductor industry. ASML’s machines are expensive, and during economic downturns or periods of lower demand, customers may delay purchasing new equipment. This cyclical demand can lead to fluctuations in ASML’s revenue, making it vulnerable to shifts in the broader economy.

Reliance on a few key customers. TSMC, Samsung, and Intel account for a significant portion of ASML’s revenue. This concentration of customers means that any slowdown in orders from one of these companies can have a large impact on ASML’s financial performance. For example, recent delays in Intel’s fab openings contributed to a downward revision in ASML’s 2025 revenue forecast. High customer concentration exposes ASML to risks that are largely beyond its control.

ASML’s biggest customers include Intel Corp., Samsung Electronics Co., and Taiwan Semiconductor Manufacturing Co. In terms of markets, Taiwan, China, and South Korea were the top three countries in which ASML did business in 2023. — From company reports

Geopolitical risks (particularly concerning US-China trade tensions). ASML’s machines contain US-made components, which means the company must comply with US export restrictions. Tighter regulations on exporting technology to China could limit ASML’s access to a large and growing market. As the geopolitical landscape continues to evolve, ASML must navigate these challenges carefully to avoid disruptions to its business.

🏛️ Capital Allocation

The company has a representative capital allocation strategy, balancing investments in growth with shareholder returns. Over the years, the company has made several strategic acquisitions that have strengthened its position in the market. One of the most notable acquisitions was Cymer in 2012, a key supplier of EUV light sources, for EUR 1.95 billion. This acquisition allowed ASML to control a crucial part of its supply chain and accelerate the development of EUV technology. In 2016, ASML acquired Hermes Microvision, a metrology and inspection provider, for EUR 2.75 billion, further expanding its product offerings.

In terms of shareholder returns, ASML has been actively buying back shares and paying dividends. The company has reduced its outstanding shares by 10% since 2013, and in November 2022, it announced a new share buyback program worth up to EUR 12 billion, to be executed by the end of 2025. This program demonstrates ASML’s confidence in its financial health and its commitment to returning value to shareholders. ASML has also been paying dividends since 2008, with the dividend for 2023 set at EUR 6.10 per share.

Their balance sheet is strong, with the company maintaining a net cash position for many years. It typically holds EUR 4 billion to EUR 7 billion in cash to fund working capital and cushion against potential downturns. This financial prudence ensures that ASML can continue to invest in R&D and innovation, even during challenging times, while still rewarding shareholders.

🥇 Competitors

The company operates in a highly specialized sector of the semiconductor industry, but direct competition is limited. Its closest competitors include Nikon, Canon, Applied Materials, Lam Research, and KLA.

Nikon and Canon primarily focus on Deep Ultraviolet (DUV) lithography systems, which are less advanced than ASML’s Extreme Ultraviolet (EUV) technology. While DUV machines are still widely used in chip manufacturing, especially for less advanced chips, Nikon and Canon have not managed to compete with ASML in the high-end segment of the market. Their machines are also used in more mature nodes, but the gap between them and ASML continues to widen as ASML advances its EUV technology.

Applied Materials and Lam Research are leading companies in semiconductor equipment, but they do not specialize in lithography. Instead, they focus on other critical processes like deposition, etching, and wafer inspection. These companies are strong players in their respective areas but do not directly challenge ASML's dominance in lithography.

Related analysis:

KLA specialises in metrology and process control solutions. KLA's tools are used to measure and inspect semiconductor wafers to ensure quality and precision during manufacturing. While it operates in a different segment from ASML, KLA plays a crucial role in ensuring the functionality and efficiency of semiconductor manufacturing equipment.

These companies provide valuable solutions within the semiconductor industry but have not been able to match ASML’s leadership in lithography systems, particularly in EUV technology.

📣 Recent News

June 3, 2024: Imec, a world-leading research and innovation hub in nanoelectronics and digital technologies, and ASML Holding announced the opening of the High NA EUV Lithography Lab in Veldhoven, the Netherlands, a lab jointly run by ASML and Imec. After a build and integration period of years, the Lab is ready to provide leading-edge logic and memory chip makers, as well as advanced materials and equipment suppliers access to the first prototype High NA EUV scanner (TWINSCAN EXE:5000) and surrounding processing and metrology tools.

May 23, 2024: ASML and Eindhoven University of Technology (TU/e) signed an agreement on a significant expansion of their collaboration. They will conduct more joint research and train more PhD students in areas such as plasma physics, mechatronics, optics and AI, based on common roadmaps. The expansion is an investment in the unique position of the Brainport region in the field of semiconductors and a strong boost for the Future Chips flagship of TU/e.

February 29, 2024: ASML announced two initiatives that will add 379 affordable homes to the Brainport Eindhoven region. Social rent and mid-rent apartments will be created in the city of Eindhoven and the municipality of Veldhoven through collaboration with Focus On Impact and Stichting TAC, and BPD | Bouwfonds Gebiedsontwikkeling and Van Santvoort, respectively, as part of ASML’s program to boost long-term affordable housing.

January 30, 2024: ASML produced its latest brand film ‘Standing on the shoulders of Giants’ with cutting-edge generative Artificial Intelligence (AI), a technology made possible by the very computing power that ASML’s advanced lithography systems help enable.

⏮️ Past

ASML reported strong results for the third quarter of 2024, with total net sales reaching EUR 7.5 billion, driven by higher-than-expected DUV sales and robust performance in the Installed Base Management segment, which contributed EUR 1.54 billion. Gross margins held steady at 50.8%, and the company recorded a net income of EUR 2.1 billion. The quarter's net bookings amounted to EUR 2.6 billion, mainly from significant EUV system orders, pushing the company’s backlog to over EUR 36 billion.

The company has provided an optimistic outlook for the final quarter of 2024, with expected net sales between EUR 8.8 billion and EUR 9.2 billion. This growth is primarily driven by anticipated increases in Installed Base revenues, which are expected to reach approximately EUR 1.9 billion. Much of this is tied to performance targets for EUV systems and several productivity upgrades that are scheduled for delivery.

The company has significantly outperformed (CAGR) the S&P 500 in long-term periods of 5, 10 and 15 years.

📶 Future

For the full year of 2024, ASML forecasts total revenue of about EUR 28 billion, with a gross margin target of around 50.6%. Looking ahead to 2025, the company has revised its revenue guidance to between EUR 30 billion and EUR 35 billion, largely due to reduced demand for Low-NA EUV tools. Nonetheless, the company remains optimistic about its product pipeline and continued technological advancements.

Sales are expected to grow from $30.38 billion in FY 2024 to $35.32 billion in FY 2025, and further to $40.64 billion in FY 2026. The year-over-year sales growth is projected to improve from -0.15% in FY 2024 to 16.25% in FY 2025, and then slightly moderate to 15.07% in FY 2026. EPS is anticipated to increase from $20.59 in FY 2024 to $26.68 in FY 2025 and reach $33.08 in FY 2026. The year-over-year EPS growth is forecasted to recover strongly from -6.25% in FY 2024 to 29.60% in FY 2025, before moderating to 23.97% in FY 2026.

Based on short-term price targets offered by eight analysts, the average price target for ASML comes to $1,056.00. The forecasts range from a low of $939.00 to a high of $1,207.00. The average price target represents an increase of 50.73% from the last closing price of $700.60.

The company currently has an average brokerage recommendation (ABR) of 1.38 on a scale of 1 to 5 (Strong Buy to Strong Sell), calculated based on the actual recommendations (Buy, Hold, Sell etc.) made by 21 brokerage firms. The current ABR compares to an ABR of 1.40 a month ago based on 20 recommendations.

Based on Markets&Markets forecast, the global EUV lithography market is expected to reach $25.3 billion by 2028, growing at a 21.8% CAGR.

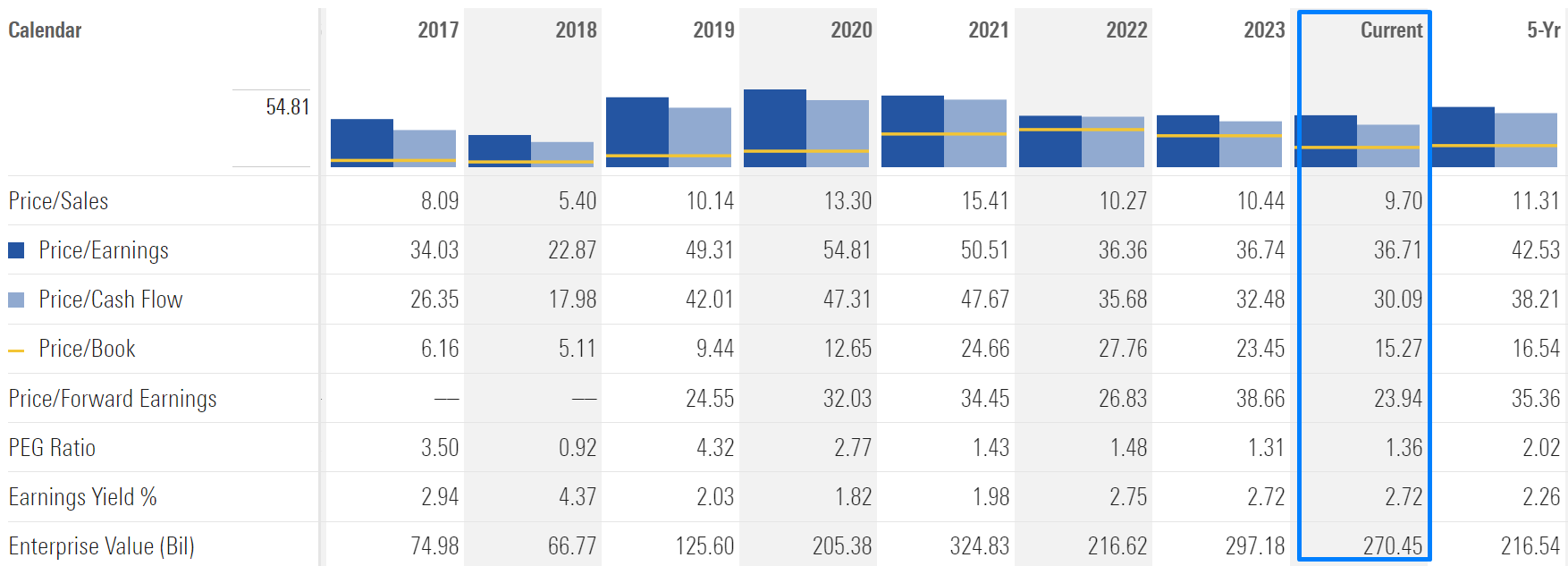

💲Current Valuation

The current valuation shows that the stock is trading at a lower premium compared to its 5-year average. Key metrics like Price/Sales and Price/Earnings ratios have declined, suggesting the market is more cautious about the stock despite its strong performance. Investors are also paying less for the company’s cash flow, as indicated by a lower Price/Cash Flow ratio.

While these metrics suggest a more moderate market sentiment, ASML’s enterprise value has increased significantly, reflecting its continued dominance in the semiconductor industry. Overall, the stock appears more reasonably priced compared to its recent history, potentially offering a good opportunity for long-term investors.

Let’s also take a look at the company’s ROIC in terms of comparing with previous periods. The current ROIC stands at 22.3%, slightly below its 5-year average of 25%. This indicates a slight decrease in efficiency compared to previous years, but the company remains well ahead of the industry average, which is only 3.3%. It demonstrates its strong operational performance and the robust demand for its products, even during market fluctuations. Despite the minor drop, ASML continues to effectively allocate capital to generate impressive returns for shareholders.

🏷️ Fair Price

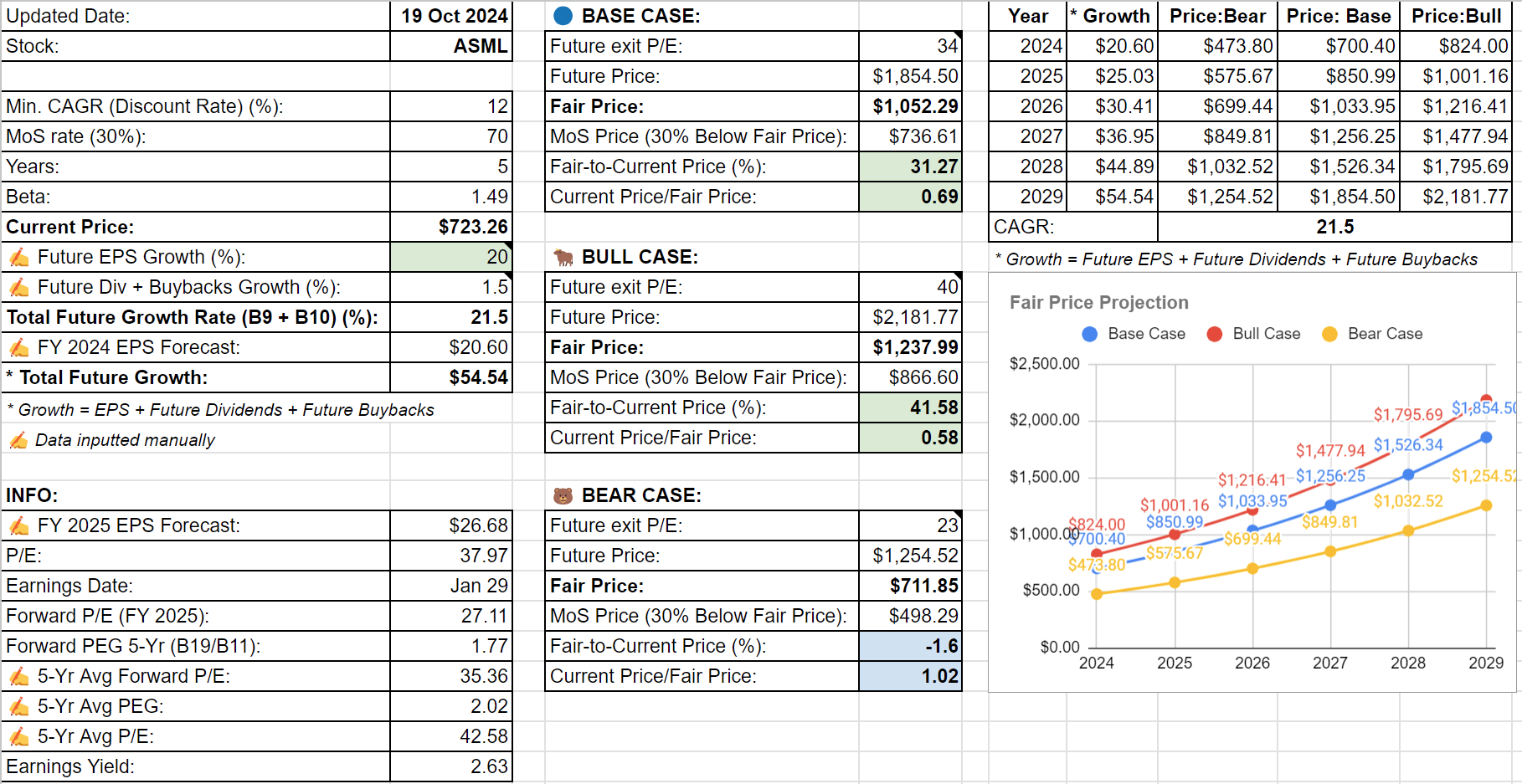

Jan 30, 2025: Updated fair price valuation. The new fair price is $1,053.

The Long-Term Pick's Fair Price (Base Case) for ASML is $1,052. The current price of $723 is lower by 31.27%.

Fair-to-Current Price (%): 31.27%

Current Price/Fair Price: 0.69

I used:

Discount Rate: 12% (S&P 500 Next 5-Yr Growth Estimates is 11.88%)

Margin of Safety: 30%

Years: 5

Future EPS Growth Rate: 20% (Based on Yahoo Finance, Koyfin and Seeking Alpha)

Future Dividend and Buyback Yield: 1.5% (5-year average value is 1.65; dividends and buybacks)

Total Future Annual Growth Rate: 20 + 1.5 = 21.5%

It is worth noting that a future CAGR of 21.5% is doable since the company has an even higher CAGR for 5, 10, and 15-year periods — see the “Past” section above. Also, pay attention that my Base Case Fair Price is almost the same as the 1-year projected price — see the “Future” section.

5-year average P/E is 42.58; the lowest P/E was 22.87 in 2018. For the Bear Case, I just took the lowest P/E for the last 10 years. For the Bull Case, I just multiplied the Future ESP Growth Rate by 2 (20 x 2 = 40), and it’s still lower than the 5-year average P/E (42.58). For the Base Case, I took 34 as “a good value” between highs and lows.

Even with the Bear Case, the company is currently is fairly valued.

☑️ Checklist

Profitability:

✅ Gross margin at least 40%: 51%

✅ Net margin at least 10%: 29%

✅ Management (ROIC, ROCE, ROE, ROA): Yes (All above 10%)

❌ Piotroski F-Score: 5 of 9 (Not passed: Higher ROA yoy, CFROA > ROA, Higher Gross Margin yoy, Higher Asset Turnover yoy)

❌ Revenue surprises in last 7 years: No (2021; Based on TradingView's data)

❌ EPS surprises in last 7 years: No (2019; Based on TradingView's data)

❌ EPS growth YoY 7 years in a row: No (2019, 2022)

Valuation and Advantage:

✅ Valuation below its 5-yr average: Yes

✅ Does it have a moat: Yes (wide)

Shares:

❌ Insider ownership at least 5%: No (0.02%)

✅ Less shares outstanding YoY: Yes

❌ Insider buys last six months: No

Price:

✅ 1-year stock price forecast is above 10%: +50.73%

✅ Next 5-Yr Growth Estimates (CAGR) is above S&P 500: Yes (21.77% vs 11.88%; Based on Yahoo Finance)

✅ DCF Value: $1,114 (Undervalued by 40%; 10 years, discount rate: 10%, terminal growth: 3%, equity model: FCFE)

✅ Short Interest below 5%: Yes

✍️ Due Diligence

Profitability (8 of 10):

✅ Positive Gross Profit: 12.9B EUR

✅ Positive Operating Income: 8.7B EUR

✅ Positive Net Income: 7.4B EUR

✅ Positive Free Cash Flow: 3B EUR

❌ Negative 1-Year Revenue Growth: -2%

✅ Positive 3-Years Revenue Growth: 15%

✅ Positive Revenue Growth Forecast: 14%

✅ Exceptional ROE

✅ Exceptional 3-Year Average ROE

✅ ROE is Increasing

✅ Positive ROIC

✅ Positive 3-Year Average ROIC

❌ Declining ROIC

Solvency (8 of 10):

✅ High Interest Coverage: 51.88

✅ Short-Term Solvency

✅ Long-Term Solvency

✅ Negative Net Debt: -410.7m EUR

✅ Low D/E: 0.26

✅ High Altman Z-Score: 10.97

This is not a financial or investing recommendation. It is solely for educational purposes.

It’s a great company.

Great work…Ty