NVIDIA: World Leader in AI Computing Still Below Fair Price

Ok, it's time to discuss NVIDIA. Finally.

Changelog:

Feb 28, 2025: Updated fair price valuation: $187.

NVIDIA (NVDA) is the global leader in GPUs, driving everything from gaming to AI. Its chips power data centers, self-driving cars, and the latest AI models. With strong demand for high-performance computing and a solid market position, NVIDIA looks set for long-term growth.

Content:

💡 Investment Thesis

🧐 Company Overview

🏰 Economic Moat

🚀 Business Strategy

🏛️ Capital Allocation

✅ Advantages

❌ Disadvantages

🥇 Competitors

⏮️ Past

📶 Future

💲Current Valuation

🏷️ Fair Price

☑️ Checklist

✍️ Due Diligence

💡 Investment Thesis

NVIDIA is the leader in AI computing, with its GPUs powering everything from machine learning to data centers and autonomous vehicles. The company has built a strong competitive moat through its CUDA software ecosystem, deep industry partnerships, and continuous innovation in high-performance chips. Its expansion into AI-driven data centers, cloud computing, and automotive solutions strengthens its long-term growth potential.

Based on my estimate, NVIDIA is on track to sustain a CAGR of at least 20% through 2030. This growth is driven by accelerating AI adoption, growing demand for high-performance computing, and its increasing influence in enterprise software and cloud infrastructure. Its strong pricing power and high margins support long-term profitability.

NVIDIA still remains an attractive investment. Currently trading almost 15% below my fair price.

🧐 Company Overview

NVIDIA Corporation is a global leader in graphics processing units (GPUs) and artificial intelligence (AI) computing. The company, founded in 1993 and headquartered in Santa Clara, California, initially focused on enhancing PC gaming graphics. Over the years, it expanded into data centers, AI, professional visualization, and automotive technology.

The company dominates the discrete GPU market with approximately 90% market share and collaborates with leading cloud service providers like Amazon, Microsoft, and Google.

NVIDIA's CEO, Jensen Huang (LinkedIn), co-founded the company and has led it since its inception. Under his leadership, NVIDIA transformed from a gaming-focused chipmaker into a dominant force in AI, data centers, and autonomous vehicles. Huang is known for his strategic vision, emphasizing high-performance computing, AI, and deep learning, positioning NVIDIA as a critical player in the technology industry.

The company serves a diverse set of clients, including hyperscale cloud service providers, major automakers, healthcare organizations, and leading tech firms. Its GPUs are used by Amazon Web Services, Microsoft Azure, and Google Cloud for AI training and data processing. Automotive clients include Tesla, Mercedes-Benz, and Audi, using NVIDIA's DRIVE platform for autonomous vehicles. In healthcare, NVIDIA partners with medical institutions to advance AI-driven diagnostics and research.

🏰 Economic Moat

NVIDIA has a wide economic moat due to its strong hardware and software ecosystem. The company’s proprietary CUDA software platform, essential for AI model development, creates high switching costs, making it difficult for competitors to take market share.

NVIDIA has the industry-leading GPU technology, giving it an advantage in AI, gaming, and data center markets. The company's dominance in AI training and inference has been a key driver of growth. Its deep integration with major cloud providers further strengthens its market position.

Another key aspect of NVIDIA’s economic moat is its strong relationships with enterprise customers, including tech giants that rely on its GPUs for AI and high-performance computing. Worth noting its expansion into AI-driven automotive solutions, cloud computing, and networking solutions.

🚀 Business Strategy

Their business strategy is based on expanding its presence in AI, data centers, and autonomous vehicles.

The company continues to invest heavily in R&D, allowing it to maintain leadership in high-performance computing. NVIDIA's acquisition of Mellanox for $6.9 billion in 2020 strengthened its data center business, improving its networking solutions.

The company is also making strategic moves in automotive AI, working with over 320 automakers and suppliers to develop autonomous driving systems.

NVIDIA is increasingly focusing on enterprise AI solutions, positioning itself as a key player in cloud-based AI computing.

NVIDIA is also expanding into new AI-powered software and services. Its Omniverse platform, which enables real-time 3D simulation and collaboration, is being used in industrial applications, digital twin technology, and scientific research. Additionally, the company continues to enhance its Jetson AI computing solutions for robotics, automation, and edge computing.

Business segments:

Gaming: This is the company’s largest segment, driven by its flagship GeForce GPU products. NVIDIA GPUs are synonymous with high-performance graphics in gaming, with applications in PCs and consoles. The gaming segment benefits from the growing demand for immersive and realistic gaming experiences, supporting technologies like ray tracing and AI-enhanced graphics.

Professional Visualization: NVIDIA serves a wide range of industries through its Quadro GPUs. This segment targets professionals in fields such as media and entertainment, architecture, engineering, and product design. The Quadro line is designed to handle complex visualization tasks, including 3D modeling and rendering, simulations, and graphic design.

Data Center: Data centers represent one of NVIDIA’s fastest-growing segments. Their GPUs are crucial in powering AI, machine learning, and deep learning applications. NVIDIA’s data center products help enhance computing power for big tech firms, research institutions, and enterprises needing to process vast datasets efficiently.

Automotive: In the automotive sector, NVIDIA develops hardware and software platforms for vehicle infotainment systems, digital cockpits, and increasingly, autonomous vehicle technology. The NVIDIA DRIVE platform supports advanced driver-assistance systems (ADAS) and levels of autonomous driving.

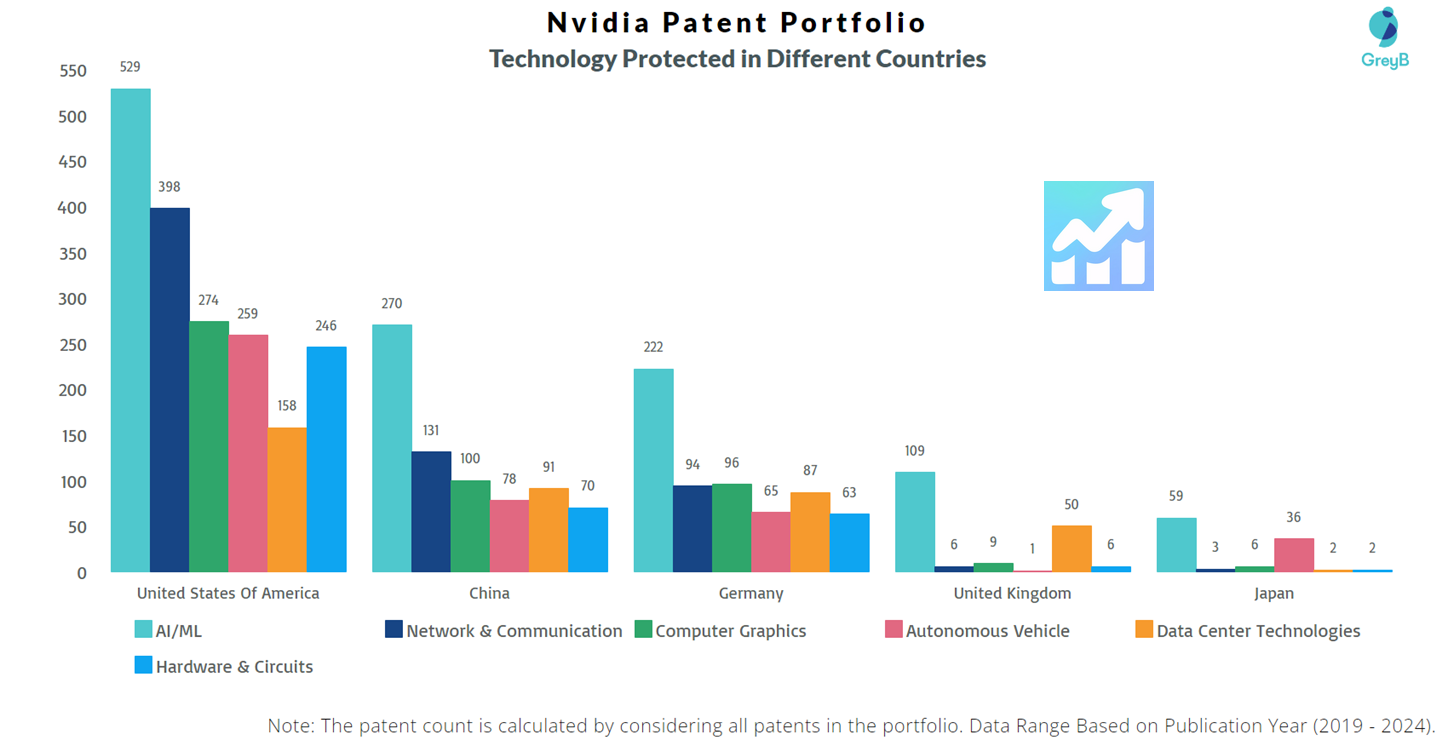

To read: Nvidia Self-Driving Car Patents

OEM and Other: This segment encompasses NVIDIA's other lines of business, including OEM sales and various other platforms. It includes products for cryptocurrency mining, internet of Things (IoT) devices, etc.

What you have missed not being a patron of the project:

🏛️ Capital Allocation

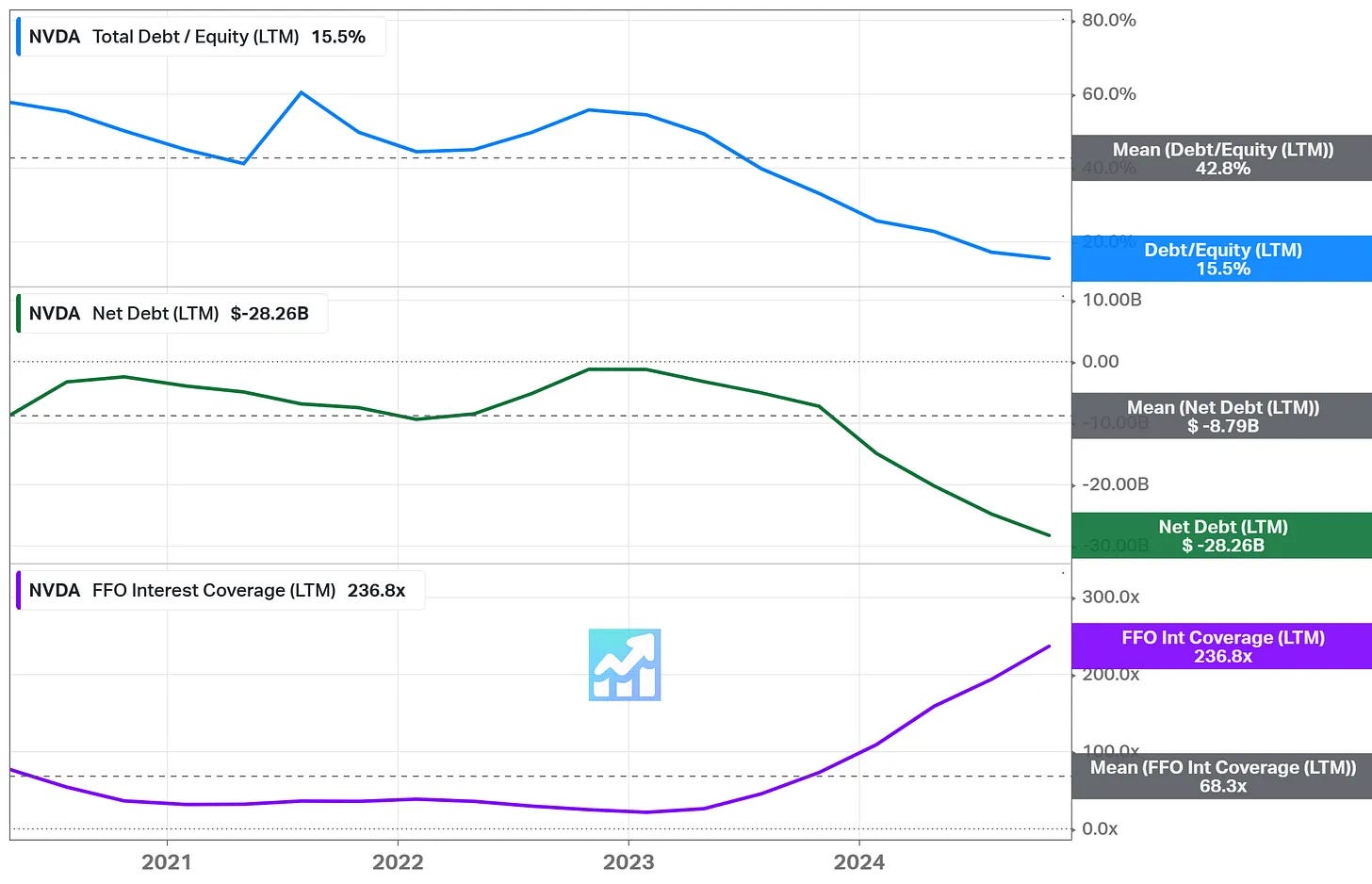

NVIDIA has an exemplary capital allocation strategy with a strong balance sheet and effective use of cash. The company held $38.5 billion in cash and investments (see the chart below in the Advantages section) against $10.22 billion in total debt. NVIDIA generates substantial free cash flow, with $56.55 billion recorded (see the chart in the Company Overview section). The company actively returns capital to shareholders through share buybacks.

Beyond share repurchases, NVIDIA reinvests a significant portion of its earnings into R&D, allowing it to stay ahead in AI, data centers, and high-performance computing. The company’s capital allocation strategy also supports strategic acquisitions, such as its Mellanox acquisition, which enhanced its data center networking capabilities.

Additionally, NVIDIA maintains a low debt-to-equity ratio, providing financial stability even in economic downturns.

✅ Advantages

Market Leadership in AI and Data Centers: NVIDIA dominates the AI computing market. The company's GPUs are essential in AI training and inference, allowing it to capture a significant share of the high-performance computing sector.

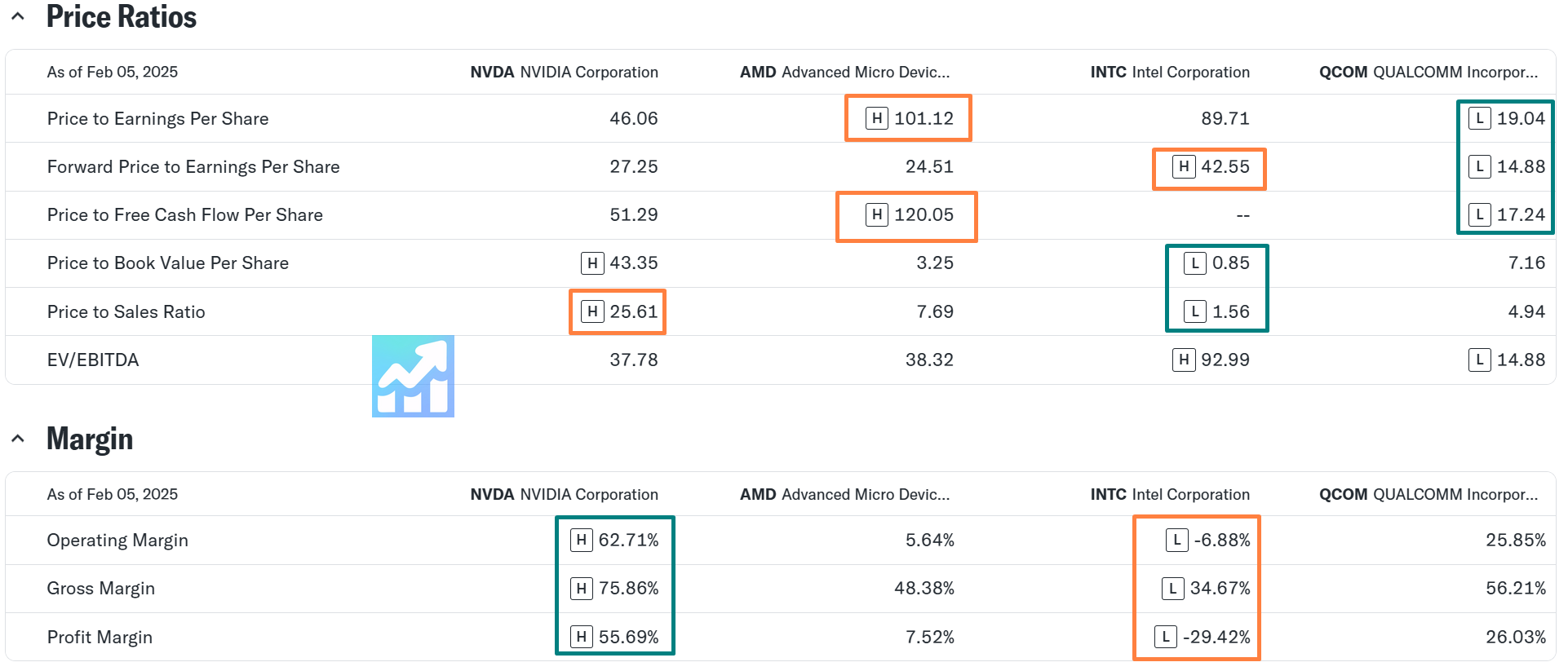

High Gross Margins: NVIDIA maintains strong profitability, with a gross margin of 75%. This high margin results from its advanced semiconductor technology, efficient manufacturing processes, and premium pricing strategy. The company's strong financial position allows for continued investment in new AI and cloud solutions while maintaining high shareholder returns.

Strategic Partnerships: NVIDIA collaborates with leading cloud service providers like Amazon, Microsoft, and Google, ensuring continued demand for its AI and GPU solutions. These partnerships help the company integrate its technology into cloud-based AI workloads, expanding its influence across industries such as healthcare, finance, and automation.

To read: NVIDIA’s Partnerships

Expanding into New Markets: The company’s presence in autonomous vehicles, robotics, and cloud computing allows for future growth beyond gaming and data centers. NVIDIA’s Jetson AI platform enables AI-powered automation in industrial applications, smart cities, and logistics. The company’s continued investment in AI-driven software solutions ensures its relevance in emerging markets.

Strong Balance Sheet: With $38.5 billion in cash and investments and relatively low debt, NVIDIA is financially well-positioned to invest in innovation and expansion. The company’s disciplined capital management ensures that it can pursue strategic acquisitions and R&D initiatives while maintaining stability during economic downturns.

❌ Disadvantages

U.S.-China Trade Tensions: NVIDIA faces restrictions on exporting its high-end AI chips to China, limiting potential revenue from one of its largest markets. Geopolitical uncertainties continue to create risks for the company, as China remains a key market for AI development and cloud services.

Growing Competition: AMD, Intel, and other firms are developing alternative AI chips, increasing competition in key markets. While NVIDIA leads in AI processing power, competitors are closing the gap through custom silicon and cloud-native AI accelerators, potentially reducing NVIDIA’s market share.

High Valuation Risks: Any slowdown in growth could negatively impact stock performance. Investors have high expectations for NVIDIA’s continued expansion, making it vulnerable to volatility if it fails to meet financial targets.

Cyclicality in Gaming and Cryptocurrency Markets: NVIDIA's gaming business is susceptible to demand fluctuations, particularly from the cryptocurrency mining sector. A downturn in gaming GPU demand or changes in cryptocurrency mining regulations could affect revenue from this segment.

Dependence on AI Demand: If hyperscale cloud providers reduce spending or shift to in-house solutions, NVIDIA’s revenue growth could be impacted. Companies like Google and Amazon are investing in proprietary AI chips, which could gradually replace NVIDIA’s solutions in large-scale cloud applications.

🥇 Competitors

AMD: While both companies compete in the GPU market, AMD focuses on offering cost-effective alternatives. NVIDIA holds a technological advantage, particularly in AI, due to its CUDA platform. AMD has made progress in gaming and high-performance computing. AMD’s recent advancements in AI-driven GPUs and custom silicon solutions have positioned it as a stronger competitor, but NVIDIA maintains a lead in AI training and inference performance, making it still the dominant player in data center AI computing.

Intel: Intel primarily competes in integrated graphics and AI accelerators. While Intel has made progress in AI chip development, it has struggled to match NVIDIA’s high-end GPU capabilities, particularly in AI training and inference workloads. Intel’s investments in AI chips, including its Gaudi series, aim to challenge NVIDIA in the AI accelerator space, but adoption remains limited compared to NVIDIA’s established ecosystem and software support.

Qualcomm: Qualcomm specializes in mobile and AI-driven semiconductors. While Qualcomm’s AI chips are optimized for mobile devices, NVIDIA’s focus remains on high-performance AI workloads. Qualcomm’s emphasis on energy-efficient AI processing gives it an advantage, but NVIDIA has processing power and a software ecosystem.

⏮️ Past

The compound annual growth rate (CAGR) for the NVDA stock over 5-, 10-, and 15-year time periods is shown above. During long-term periods, the stock significantly outperforms the S&P 500.

Above is a comparison of total returns with the S&P 500 (SPY) on a 10-year period. The number is enormous.

📶 Future

➡️ GPU future market overview is additionally available for patrons only.

Below is the 3-year forecast for future sales and EPS growth, which is projected to be around 61.70% and 68%, respectively. Compare these numbers with the current Price/Forward Earnings ratio (see the section below) to get some insights regarding the current valuation 😉

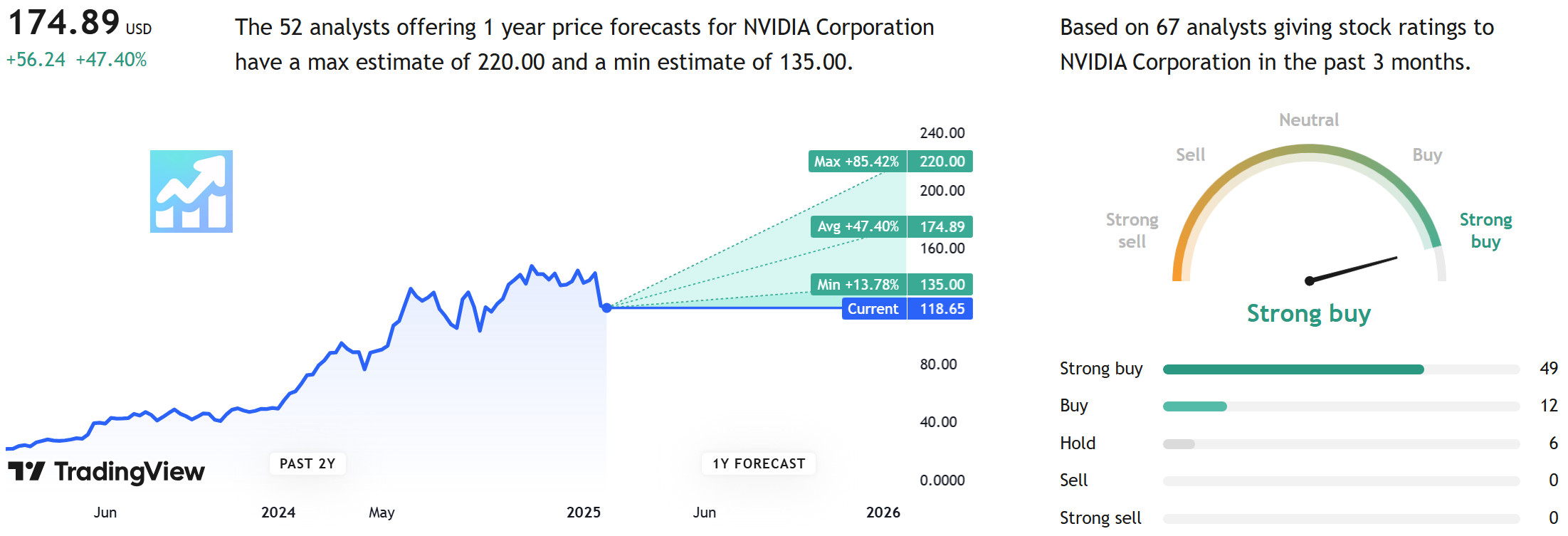

Based on 1-year price targets offered by other analysts, the average price target for NVDA comes to $175. The forecasts range from a low of $135 to a high of $220. The average price target represents an increase of 47.40%.

💲Current Valuation

Here are two charts showing the current valuation of NVDA stock. The company is trading below its 5-year averages, except for the Price/Book ratio. Pay attention that the PEG ratio is only 0.8.

➡️ The valuation comparison with the industry is additionally available for patrons only.

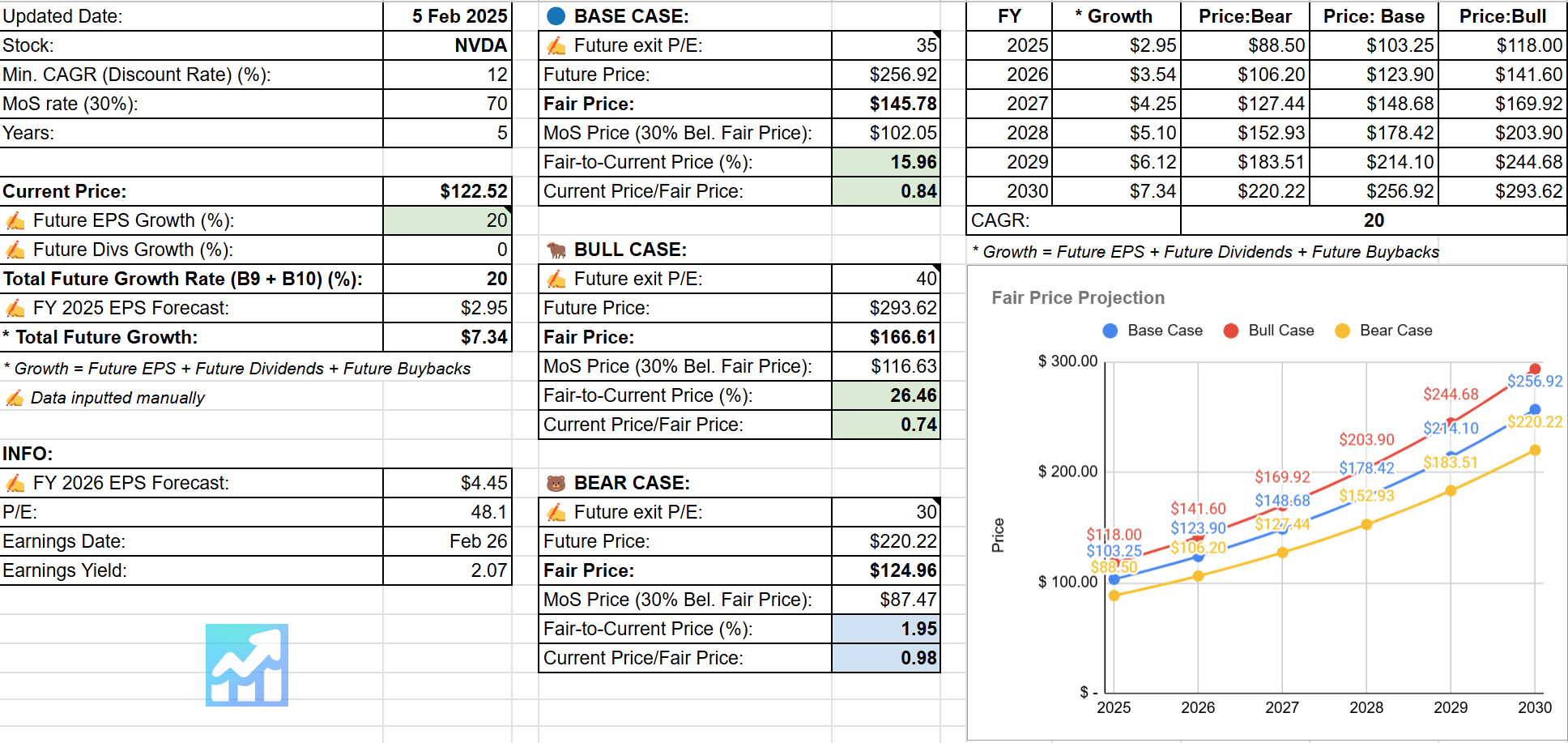

🏷️ Fair Price

The Long-Term Pick's Fair Price (Base Case) for NVDA is $145.78. The current price of $122.52 is lower by 15.96%.

Fair-to-Current Price (%): 15.96%

Current Price/Fair Price: 0.84

I used:

Discount Rate: 12%

Margin of Safety: 30%

Years: 5

Future EPS Growth Rate: 20% (I lowered the 3-year EPS forecast since my maximum is 20)

Future Dividend Yield: 0%

Total Future Annual Growth Rate: 20 + 0 = 20%

My estimate may be pessimistic since the market has always estimated the stock with high valuations.

For the Bull Case future exit Price/Earnings ratio, I used:

Future EPS Growth Rate x 2 = 40

which is still lower than the current Price/Earnings ratio (48.2) and the 10-year average value (61.5). For the Base Case, I subtracted 5 from the Bull Case, and for the Bear Case, I added 5 to the Base Case.

☑️ Checklist

Profitability:

✅ Gross margin at least 40%: 75%

✅ Net margin at least 10%: 55.7%

✅ FCF margin at least 10%: 50%

✅ Management (ROIC, ROCE, ROE, ROA): Yes (All above 10%)

✅ Piotroski F-Score: 8 of 9 (Not passed: CFROA > ROA)

🟨 Revenue surprises in last 7 years: No (Missed: 2018; Based on TradingView's data)

✅ EPS surprises in last 7 years: Yes (Based on TradingView's data)

🟨 EPS growth YoY 7 years in a row: No (Missed 2019 and 2022; Based on TradingView's data)

Valuation and Advantage:

✅ Valuation below its 5-year averages: Yes

❓ Valuation below the industry: available for patrons only

✅ Does it have a moat: Yes (wide)

✅ Outperformed the S&P 500 10-year CAGR: Yes (74% vs 13.61%)

Shares:

🟨 Insider ownership at least 5%: No (4%)

✅ Less shares outstanding YoY: Yes

❌ Insider buys last six months: No

Price:

✅ 1-year stock price forecast is above 10%: +47.40%

✅ Next 5-year EPS growth estimates (CAGR) is above 10%: Yes (38%)

❌ DCF Value: $75.61; Overvalued by 36% (5 years, discount rate: 10%, terminal growth: 3%, equity model: FCFF)

✅ Short Interest below 5%: Yes (1.22%)

✍️ Due Diligence

Profitability (10 of 10):

✅ Positive Gross Profit: 85.9B USD (for the last twelve months)

✅ Positive Operating Income: 71B USD (for the last twelve months)

✅ Positive Net Income: 63.1B USD (for the last twelve months)

✅ Positive Free Cash Flow: 56.5B USD (for the last twelve months)

✅ Exceptional 1-Year Revenue Growth: 152% (over the past 12 months)

✅ Exceptional 3-Year Revenue Growth: 67% (per year for the last 3 years)

✅ Exceptional Revenue Growth Forecast: 60% (per year over the next 3 years)

✅ Exceptional ROE: 135% (for the past 12 months)

✅ Exceptional 3-Year Average ROE: 63% (three-year average)

✅ ROE is Increasing: 45% → 135% (in the last 3 years)

✅ Exceptional ROIC: 147% (for the past 12 months)

✅ Exceptional 3-Year Average ROIC: 68% (three-year average)

✅ ROIC is Increasing: 56% → 147% (in the last 3 years)

Solvency (9 of 10):

✅ Short-Term Solvency: short-term assets (68B USD) exceed its short-term liabilities (16B USD)

✅ Long-Term Solvency: long-term assets (96B USD) exceed its long-term liabilities (30B USD)

✅ Negative Net Debt: -30B USD (the company has more cash and short-term investments (38B USD) than debt (8B USD))

✅ Low Debt-to-Equity Ratio: 0.13

✅ High Altman Z-Score: 73.68 (whether a company is headed for bankruptcy - takes into account profitability, leverage, liquidity, solvency, and activity ratios)

This is not a financial or investing recommendation. It is solely for educational purposes.

If you like the content, please hit the like icon, leave a comment, and share the publication with your friends and colleagues - this will motivate the author. If you're ready to support the project and get access to additional materials, visit this page.

Future is still so bright for NVIDIA!

Thanks for a detailed overview! The best as always!