Updated Valuations: AMAT, XYZ, FSLR, NVDA, and CRM

Another bunch of companies covered by Long-Term Pick (updated page) released their quarterly and yearly earnings reports (first bunch, second bunch). It's time to update their fair price valuations and review the latest reports. Please note that patrons of the project will receive an additional update on premium companies.

Some explanations regarding screenshots with fair price estimates:

I marked cells that I updated as grey (after the latest earning reports).

Fair-to-Current Price and Current Price/Fair Price: 🟢 undervalued, 🔵 fairly valued (+/- 5% is “fairly”), 🟡 overvalued.

Also, this time, I’ve decided to add a new subsection: Quick Overview, which contains the most important data for each company. Please click on the images to increase their size.

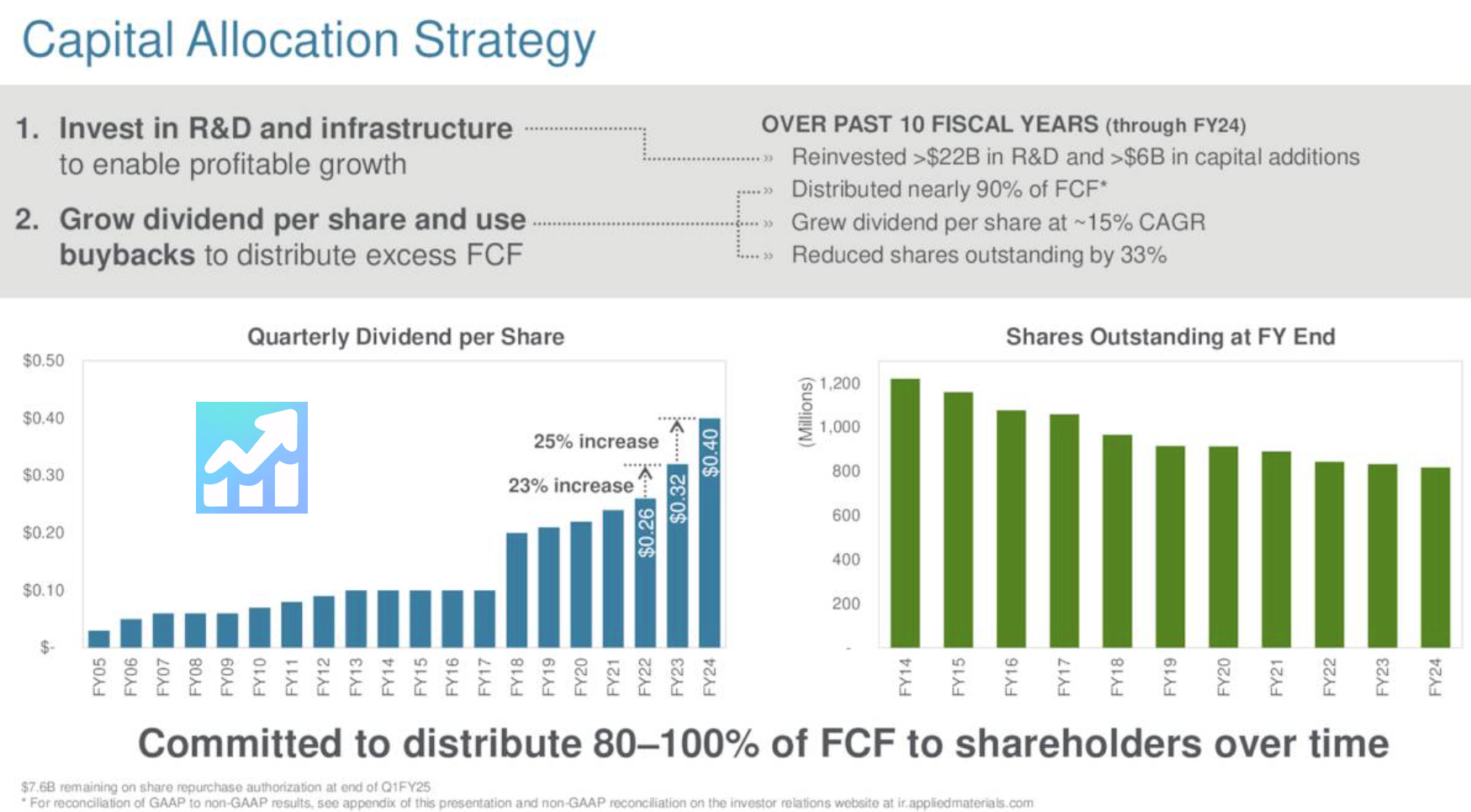

🟢 Applied Materials (AMAT)

🏷️ Updated Valuation

My previous fair price was $217. After changes, the new fair price has become $187 (lower). I’ve decreased the future EPS growth rate. The company is currently trading almost 8% below my fair price estimate.

📄 Latest Earnings Report

Q1 2025 (Feb 14, 2025):

CEO Gary Dickerson highlighted record revenues for Q1 2025, attributed to the company’s advancements in semiconductor technologies, particularly in AI and energy-efficient computing. He emphasized that foundational semiconductor innovations are critical to achieving system-level energy and cost efficiencies, positioning Applied for continued growth.

Dickerson noted the company’s leadership in device architecture inflections such as gate-all-around transistors, backside power delivery, and advanced packaging, which are driving growth opportunities. He stated that the transition to gate-all-around nodes could increase Applied’s revenue by 30% for equivalent wafer fab capacity.

Total net sales of $7.2 billion, with a non-GAAP EPS of $2.38, reflecting a 12% year-over-year increase. Attributed the performance to favorable product mix, adoption of leading-edge technologies, and disciplined cost reductions.

Semiconductor Systems revenue reached $5.36 billion, up 9% year-over-year, driven by 20% growth in foundry logic. However, DRAM sales declined due to reduced demand from China.

Applied Global Services generated $1.59 billion in revenue, an 8% year-over-year increase, supported by growth in services despite a decline in 200mm equipment sales. Non-GAAP operating margin for AGS was 28%.

Free cash flow for Q1 was $544 million, with $1.6 billion returned to shareholders through share repurchases and dividends. Cash and cash equivalents totaled $6.3 billion at the end of the quarter.

For Q2 2025, Applied Materials forecasts revenue of $7.1 billion, plus or minus $400 million, and non-GAAP EPS of $2.30, plus or minus $0.18. The company expects Semiconductor Systems revenue to reach approximately $5.3 billion.

Management projects continued momentum in advanced packaging, with plans to double revenues over the coming years. Gate-all-around revenues in 2025 are anticipated to double from $2.5 billion achieved in 2024.

CFO Hill stated that China's revenue as a percentage of total revenue is expected to decline by 5 percentage points in Q2 compared to Q1, reflecting the impact of expanded trade restrictions.

💲Current Valuation

📈 Price Forecast

↗️ Sales and EPS Forecast

⏺️ EPS Actual vs. Estimate

📈 5Y Performance

🧐 Quick Overview

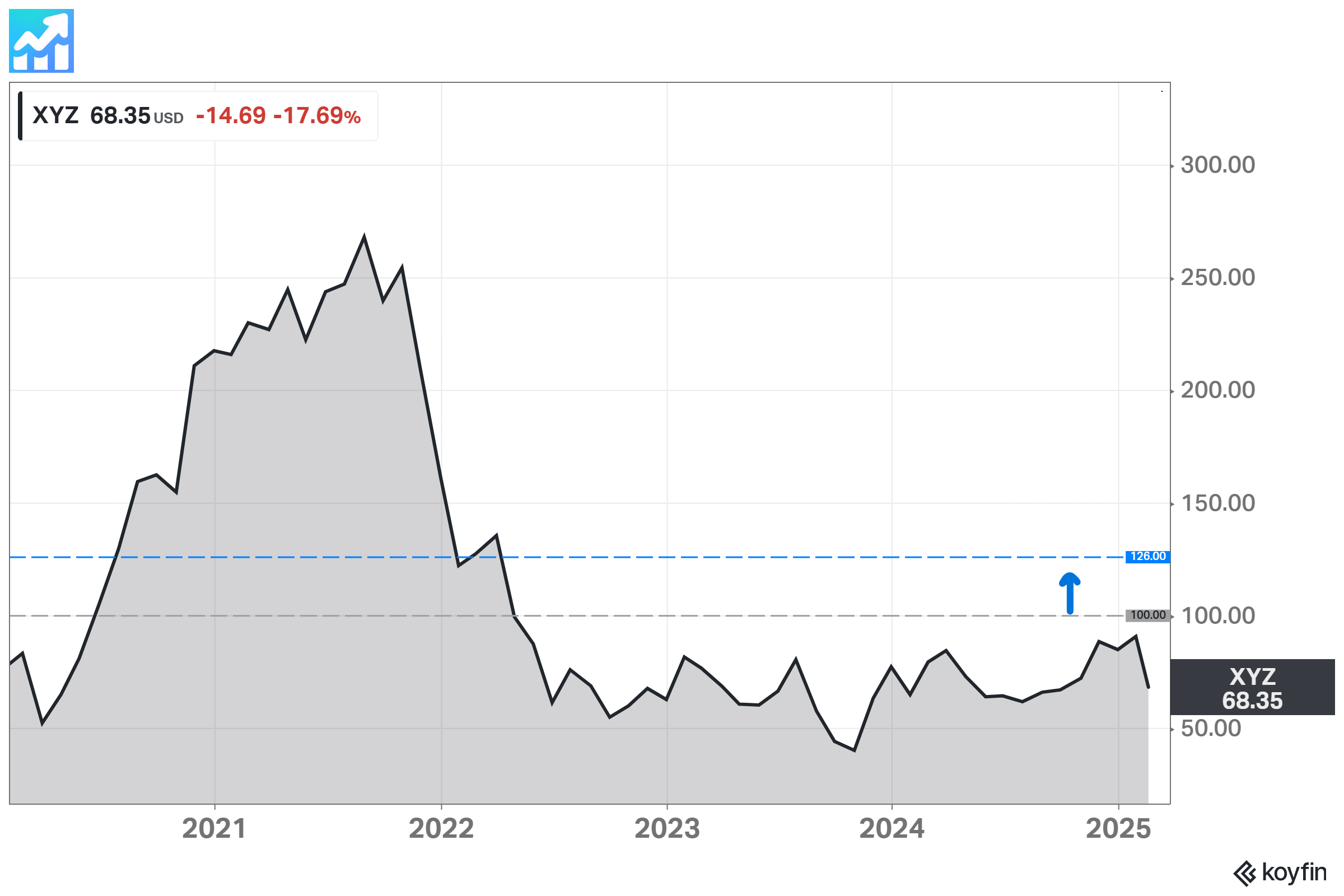

🟢 Block (XYZ)

🏷️ Updated Valuation

My previous fair price was $100. After changes, the new fair price has become $126 (higher). Forward 5Y EPS growth rate is above 24%. The price may be a bit optimistic, but at least the Bear Case is still almost 27% below the current price.

📄 Latest Earnings Report

Q4 2024 (Feb 20, 2025):

$8.89 billion in gross profit for 2024, up 18% year-over-year. Square contributed 15% growth, and Cash App grew 21% year-over-year.

Adjusted EBITDA reached $3.03 billion, a 69% increase year-over-year, while adjusted operating income rose to $1.61 billion, expanding by over 4.5 times compared to the prior year.

Adjusted free cash flow for the year was $2.07 billion, compared to $515 million in 2023.

Jack Dorsey highlighted significant progress in 2024, emphasizing the transition of Square into a full commerce platform and enhancements to Cash App's financial services. He also underscored investments in AI automation, Bitcoin infrastructure, and open-source innovation to expand global financial access.

The gross profit retention of more than 100% across Square and Cash App, driven by deepened customer engagement. Key metrics included Square GPV growth of 10% in Q4 2024 and Cash App's paycheck deposit actives reaching 2.5 million in December, a 25% year-over-year increase.

CFO Amrita Ahuja stated, "We achieved 36.5% on a Rule of 40 basis in 2024, up 7 points from the year prior," and emphasized the company’s focus on maintaining disciplined execution while balancing growth and cost efficiencies.

Management projected a minimum of $10.22 billion in gross profit for 2025, reflecting at least 15% year-over-year growth, despite facing incremental headwinds from FX rates.

A more pronounced acceleration in Cash App is anticipated as Block broadens access to Cash App Borrow, scales Afterpay on Cash App Card, and invests in marketing initiatives. The company plans to expand Cash App Borrow eligibility and offer higher limits through improved underwriting and state expansions.

Square GPV and gross profit are expected to improve throughout 2025, supported by marketing, partnerships, and platform investments. Management highlighted the rollout of Afterpay on Cash App Card, launched recently, as a key growth driver.

Adjusted operating income is forecasted at $2.1 billion for 2025, with a margin expansion of 240 basis points year-over-year.

💲Current Valuation

📈 Price Forecast

↗️ Sales and EPS Forecast

⏺️ EPS Actual vs. Estimate

📈 5Y Performance

🧐 Quick Overview

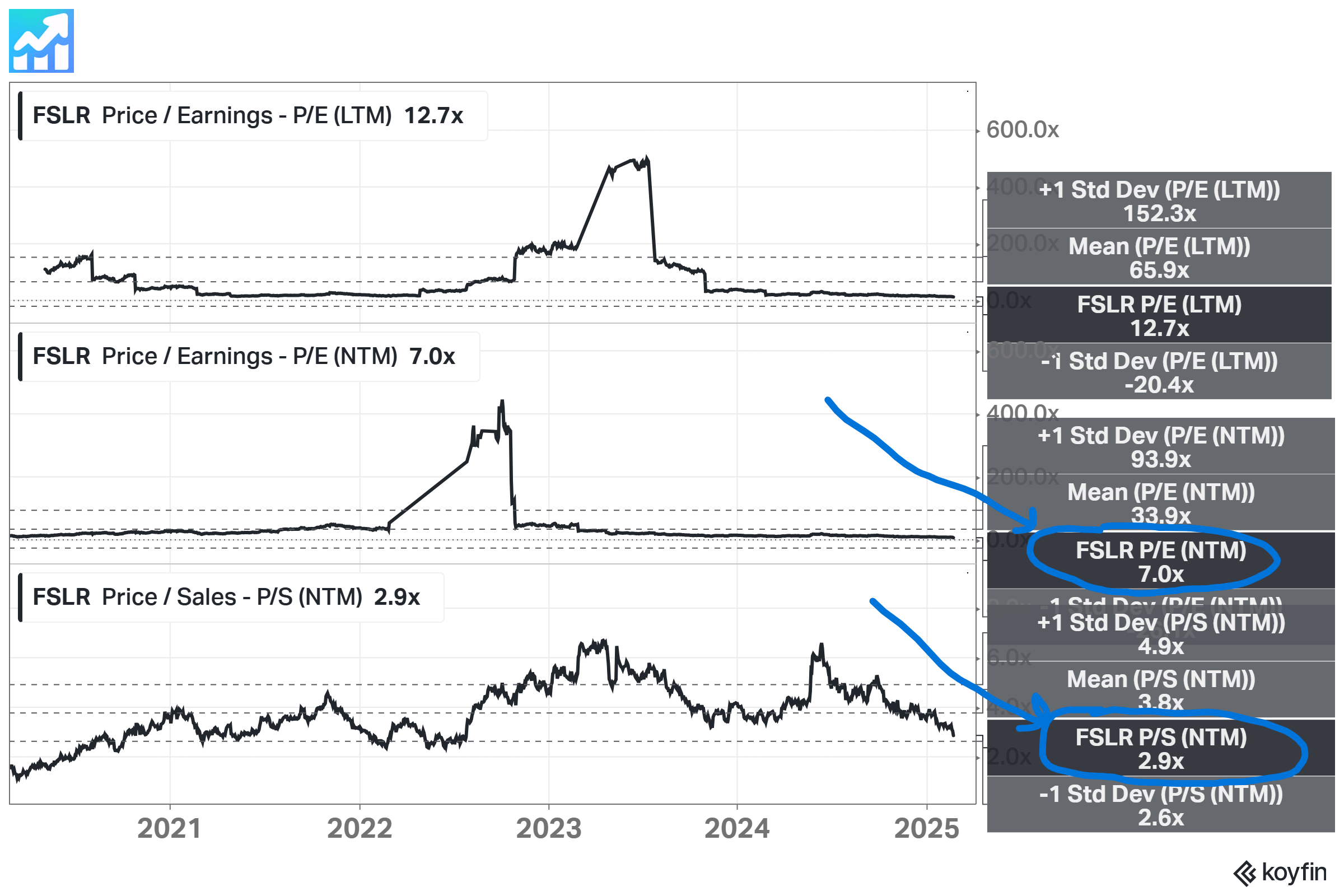

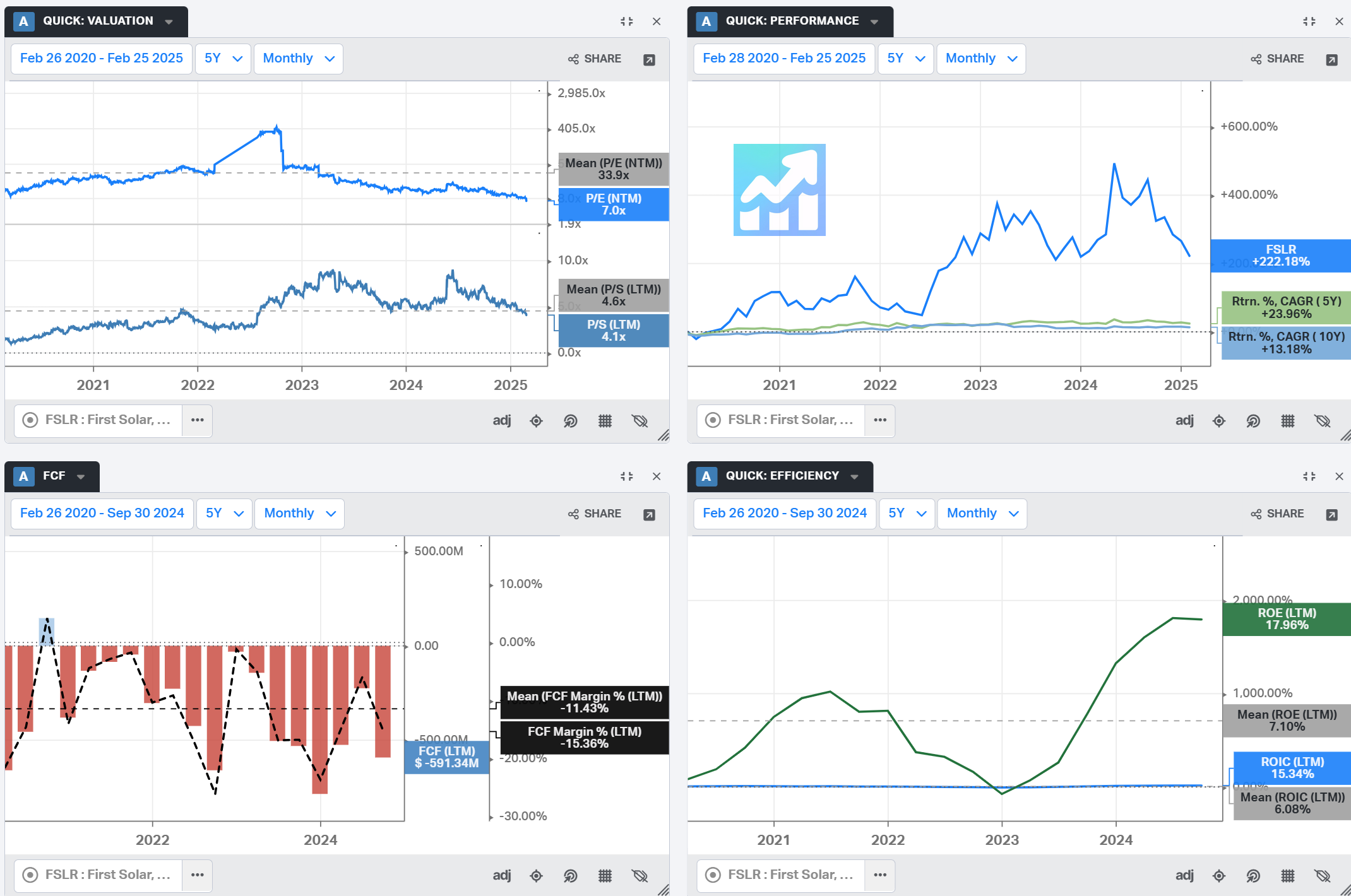

🟢 First Solar (FSLR)

🏷️ Updated Valuation

The most undervalued company on the market right now. My previous fair price was $373. After changes, the new fair price has become $447 (higher). I’ve decreased the future exit P/E value for all the cases (Base, Bull, and Bear).

📄 Latest Earnings Report

Q4 2024 (Feb 25, 2025):

First Solar reported $4.2 billion in net sales for 2024, up from $3.3 billion in the prior year, driven by increased module sales. Q4 2024 net sales reached $1.5 billion, marking a $0.6 billion sequential increase. Net income per diluted share for 2024 was $12.02, with Q4 earnings at $3.65 per share.

The company ended 2024 with a $1.2 billion net cash balance, up from $0.7 billion in the prior quarter. 2024 bookings totaled 4.4 GW, with an average selling price of 30.5 cents per watt, excluding adjustments.

CEO Mark Widmar emphasized First Solar's strategic expansion, including the commissioning of its Alabama plant and the ongoing construction of its Louisiana facility. The company also launched a new R&D center in Ohio to drive future innovation.

For 2025, First Solar expects net sales between $5.3 billion and $5.8 billion, with earnings per diluted share guidance of $17.00 to $20.00. Gross margin is projected at $2.45 billion to $2.75 billion, while capital expenditures will range from $1.3 billion to $1.5 billion. The company anticipates 18GW to 20GW in module sales, supported by ongoing capacity expansion and strong demand.

Management remains confident in its long-term growth trajectory, focusing on scaling operations and leveraging tax incentives under the Inflation Reduction Act.

💲Current Valuation

📈 Price Forecast

↗️ Sales and EPS Forecast

⏺️ EPS Actual vs. Estimate

📈 5Y Performance

🧐 Quick Overview

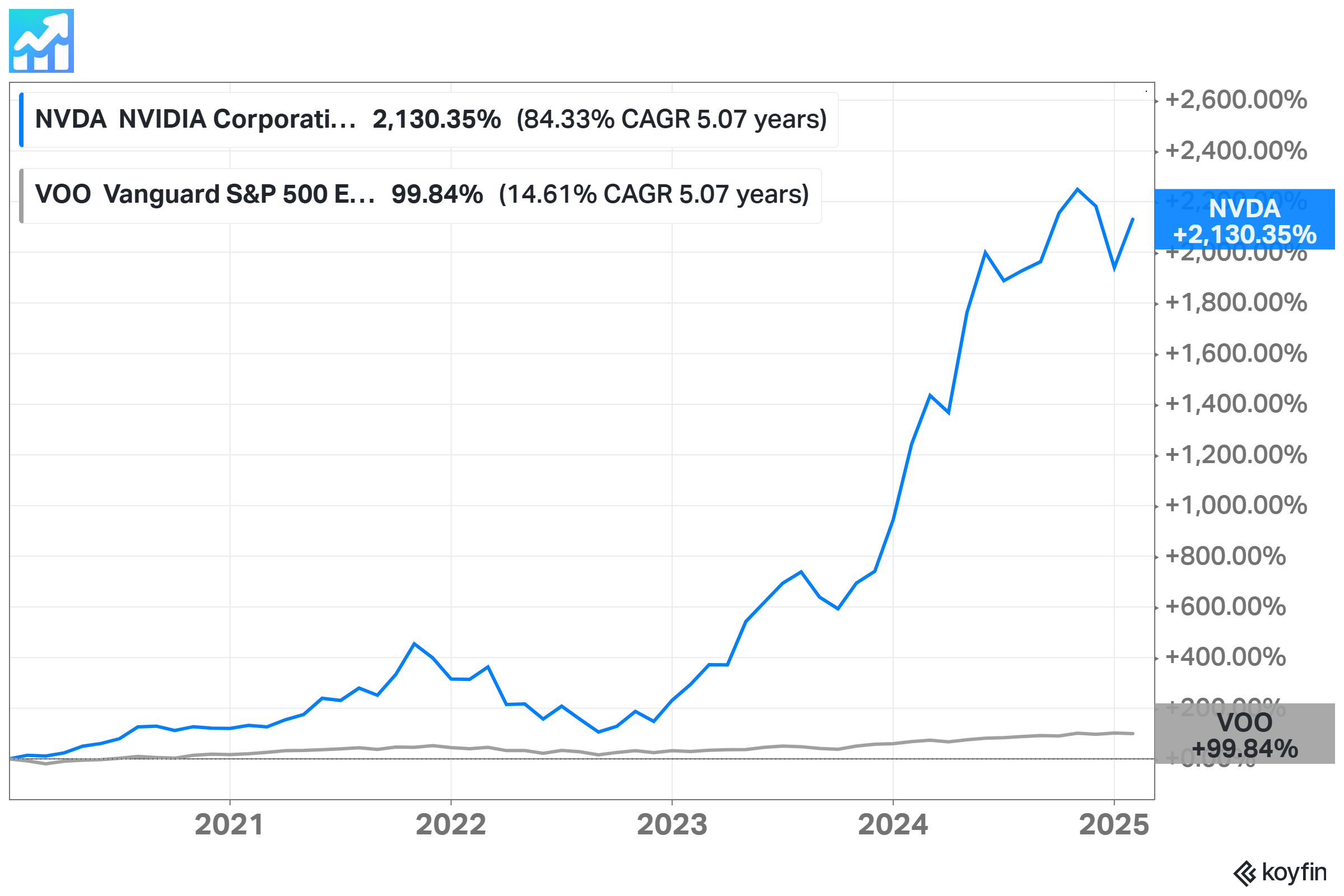

🟢 NVIDIA (NVDA)

🏷️ Updated Valuation

I would call the company “everything you need for your future business” (see my earnings overview below). My previous fair price was $145. After changes, the new fair price has become $187 (higher). I’ve decreased the future exit P/E value for all the cases (Base, Bull, and Bear), but the current P/E ratio is still far above the Bull Case, so my estimate might be even a bit pessimistic. The future estimated 5Y EPS growth rate is above 30%, but my maximum is 20%. The company is currently trading 30% below my fair price estimate.

📄 Latest Earnings Report

Q4 2025 (Feb 26, 2025):

Record quarterly revenue of $39.3 billion, up 12% from Q3 and up 78% from a year ago.

Record quarterly Data Center revenue of $35.6 billion, up 16% from Q3 and up 93% from a year ago.

Record full-year revenue of $130.5 billion, up 114%.

For the quarter, GAAP earnings per diluted share was $0.89, up 14% from the previous quarter and up 82% from a year ago. Non-GAAP earnings per diluted share was $0.89, up 10% from the previous quarter and up 71% from a year ago.

“Demand for Blackwell is amazing as reasoning AI adds another scaling law — increasing compute for training makes models smarter and increasing compute for long thinking makes the answer smarter,” said Jensen Huang, founder and CEO of NVIDIA.

“We’ve successfully ramped up the massive-scale production of Blackwell AI supercomputers, achieving billions of dollars in sales in its first quarter. AI is advancing at light speed as agentic AI and physical AI set the stage for the next wave of AI to revolutionize the largest industries.”

NVIDIA will pay its next quarterly cash dividend of $0.01 per share on April 2, 2025, to all shareholders of record on March 12, 2025.

2026 Outlook: Revenue is expected to be $43.0 billion, plus or minus 2%. GAAP and non-GAAP gross margins are expected to be 70.6% and 71.0%, respectively, plus or minus 50 basis points. GAAP and non-GAAP operating expenses are expected to be approximately $5.2 billion and $3.6 billion, respectively. GAAP and non-GAAP other income and expense are expected to be an income of approximately $400 million, excluding gains and losses from non-marketable and publicly-held equity securities. GAAP and non-GAAP tax rates are expected to be 17.0%, plus or minus 1%, excluding any discrete items.

NVIDIA will serve as a key technology partner for the $500 billion Stargate Project.

The Stargate Project is a new company which intends to invest $500 billion over the next four years building new AI infrastructure for OpenAI in the United States. We will begin deploying $100 billion immediately. This infrastructure will secure American leadership in AI, create hundreds of thousands of American jobs, and generate massive economic benefit for the entire world. This project will not only support the re-industrialization of the United States but also provide a strategic capability to protect the national security of America and its allies.

Cloud service providers AWS, CoreWeave, Google Cloud Platform (GCP), Microsoft Azure and Oracle Cloud Infrastructure (OCI) are bringing NVIDIA® GB200 systems to cloud regions around the world to meet surging customer demand for AI.

Partnered with AWS to make the NVIDIA DGX™ Cloud AI computing platform and NVIDIA NIM™ microservices available through AWS Marketplace.

Cisco will integrate NVIDIA Spectrum-X™ into its networking portfolio to help enterprises build AI infrastructure.

More than 75% of the systems on the TOP500 list of the world’s most powerful supercomputers are powered by NVIDIA technologies.

Announced a collaboration with Verizon to integrate NVIDIA AI Enterprise, NIM and accelerated computing with Verizon’s private 5G network to power a range of edge enterprise AI applications and services.

Unveiled partnerships with industry leaders including IQVIA, Illumina, Mayo Clinic and Arc Institute to advance genomics, drug discovery and healthcare.

Launched NVIDIA AI Blueprints and Llama Nemotron model families for building AI agents and released NVIDIA NIM microservices to safeguard applications for agentic AI.

Announced the opening of NVIDIA’s first R&D center in Vietnam.

Siemens Healthineers has adopted MONAI Deploy for medical imaging AI.

Announced new GeForce RTX™ 50 Series graphics cards and laptops powered by the NVIDIA Blackwell architecture, delivering breakthroughs in AI-driven rendering to gamers, creators and developers.

Launched GeForce RTX 5090 and 5080 graphics cards, delivering up to a 2x performance improvement over the prior generation.

Introduced NVIDIA DLSS 4 with Multi Frame Generation and image quality enhancements, with 75 games and apps supporting it at launch, and unveiled NVIDIA Reflex 2 technology, which can reduce PC latency by up to 75%.

Unveiled NVIDIA NIM microservices, AI Blueprints and the Llama Nemotron family of open models for RTX AI PCs to help developers and enthusiasts build AI agents and creative workflows.

Unveiled NVIDIA Project DIGITS, a personal AI supercomputer that provides AI researchers, data scientists and students worldwide with access to the power of the NVIDIA Grace™ Blackwell platform.

Announced generative AI models and blueprints that expand NVIDIA Omniverse™ integration further into physical AI applications, including robotics, autonomous vehicles and vision AI.

Introduced NVIDIA Media2, an AI-powered initiative transforming content creation, streaming and live media experiences, built on NIM and AI Blueprints.

Announced that Toyota, the world’s largest automaker, will build its next-generation vehicles on NVIDIA DRIVE AGX Orin™ running the safety-certified NVIDIA DriveOS operating system.

Partnered with Hyundai Motor Group to create safer, smarter vehicles, supercharge manufacturing and deploy cutting-edge robotics with NVIDIA AI and NVIDIA Omniverse.

Announced that the NVIDIA DriveOS safe autonomous driving operating system received ASIL-D functional safety certification and launched the NVIDIA DRIVE™ AI Systems Inspection Lab.

Launched NVIDIA Cosmos™, a platform comprising state-of-the-art generative world foundation models, to accelerate physical AI development, with adoption by leading robotics and automotive companies 1X, Agile Robots, Waabi, Uber and others.

Unveiled the NVIDIA Jetson Orin Nano™ Super, which delivers up to a 1.7x gain in generative AI performance.

💲Current Valuation

📈 Price Forecast

↗️ Sales and EPS Forecast

⏺️ EPS Actual vs. Estimate

📈 5Y Performance

🧐 Quick Overview

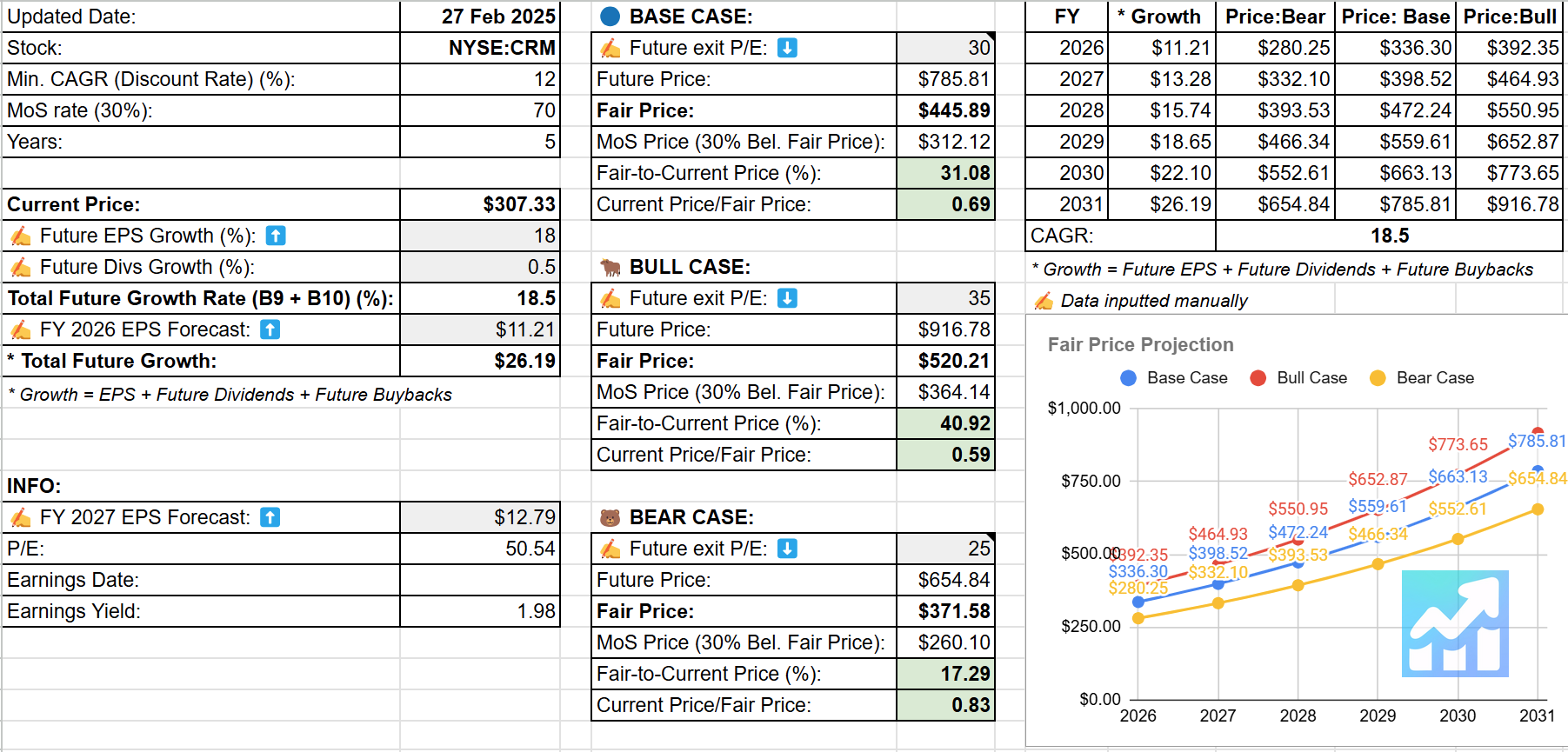

🟢 Salesforce (CRM)

🏷️ Updated Valuation

My previous fair price was $426. After changes, the new fair price has become $446 (higher). I’ve increased the future EPS growth rate but decreased the future exit P/E value for all the cases (Base, Bull, and Bear). The company is currently trading almost 30% below my fair price estimate.

📄 Latest Earnings Report

Q4 2025 (Feb 26, 2025):

$900 million Data Cloud & AI annual recurring revenue, up 120% year-over-year.

Since October, closed 5,000 Agentforce deals, including more than 3,000 paid.

Data Cloud surpassed 50 trillion records, which doubled Y/Y.

Nearly half of the Fortune 100 are both AI & Data Cloud customers, and all of our top 10 wins in Q4 included Data and AI.

On help.salesforce.com, Agentforce has handled 380,000 conversations, achieving an 84% resolution rate, with only 2% of the requests requiring human escalation.

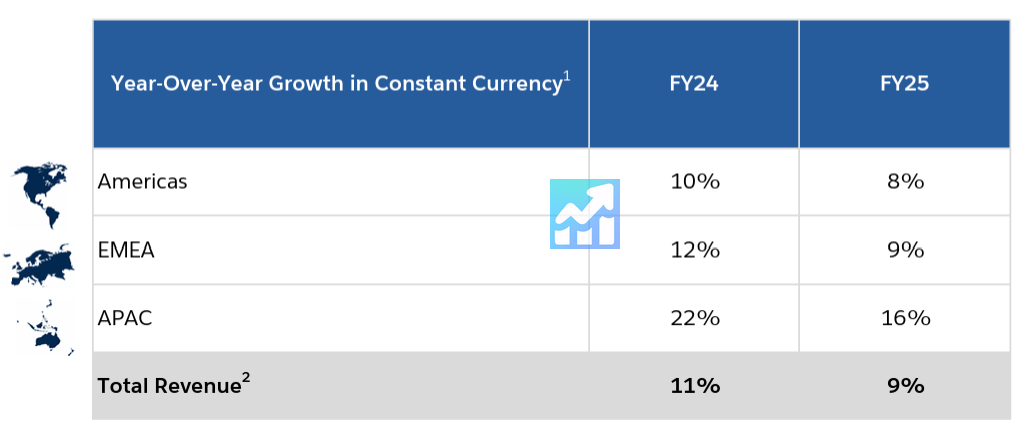

Fourth quarter revenue of $10.0 billion, up 8% Y/Y, up 9% in constant currency (CC), inclusive of subscription & support revenue of $9.5 billion, up 8% Y/Y, up 9% in CC.

Current remaining performance obligation of $30.2 billion, up 9% Y/Y, up 11% in CC.

Total remaining performance obligation of $63.4 billion, up 11% Y/Y.

FY25 revenue of $37.9 billion, up 9% both Y/Y & in CC, inclusive of subscription & support revenue of $35.7 billion, up 10% both Y/Y & in CC.

FY25 GAAP operating margin of 19.0% and non-GAAP operating margin of 33.0%.

FY25 operating cash flow of $13.1 billion, up 28% Y/Y, and free cash flow of $12.4 billion, up 31% Y/Y.

Returned $7.8 billion in the form of share repurchases and $1.5 billion in dividend payments to stockholders; total cash returned to stockholders of $9.3 billion in FY25.

FY26 Guidance: Initiates revenue guidance of $40.5 billion to $40.9 billion, up 7% - 8% both Y/Y & in CC. Initiates subscription & support revenue growth guidance of approximately 8.5% Y/Y & approximately 9% in CC. Initiates GAAP operating margin guidance of 21.6% and non-GAAP operating margin guidance of 34.0%. Initiates operating cash flow growth guidance of approximately 10% to 11% Y/Y.

“We had an incredible quarter and year, with strong performance across all our key metrics, including the highest cash flow in our company’s history and more than $60 billion in RPO,” said Marc Benioff, Chair and CEO.

“No company is better positioned than Salesforce to lead customers through the digital labor revolution. With our deeply unified platform, seamlessly integrating our Customer 360 apps, Data Cloud and Agentforce, we’re already delivering unprecedented levels of productivity, efficiency and cost savings for thousands of companies.”

💲Current Valuation

📈 Price Forecast

↗️ Sales and EPS Forecast

⏺️ EPS Actual vs. Estimate

📈 5Y Performance

🧐 Quick Overview

This is not a financial or investing recommendation. It is solely for educational purposes.

If you like the content, please hit the like icon, leave a comment, and share the publication with your friends and colleagues - this will motivate the author. If you're ready to support the project and get access to additional materials, visit this page.

Great article! I’m disappointed with First Solars stock performance recently but I can’t argue it’s good value. Same for AMAT and Nvidia