First Solar: Significant Growth Ahead

A leading global provider of comprehensive photovoltaic (PV) solar energy solutions. Specializes in designing, manufacturing, and selling solar electric power modules using thin-film technology.

Changelog:

Feb 28, 2025: Updated fair price valuation: $447.

Jan 27, 2025: Overview: First Solar endows Missouri S&T professorship, Solar manufacturing facility in Lawrence County, and New industry benchmarks.

Nov 01, 2024: Updated fair price valuation: $380.

First Solar (FSLR) specializes in designing and producing solar photovoltaic panels, modules, and systems, primarily for large-scale utility projects. The company’s solar modules utilize cadmium telluride, a key material in what is known as thin-film technology, to efficiently convert sunlight into electricity. As the world’s largest manufacturer of thin-film solar modules, First Solar operates production facilities in Vietnam, Malaysia, the United States, and India.

👉 Download the FLSR three-pager in PDF format (1.85MB). Also, available as three PNG images.

Previous publication:

Content:

💡 Investment Thesis

🧐 Company Overview

🏰 Economic Moat

🚀 Business Strategy

✅ Advantages

❌ Disadvantages

🏛️ Capital Allocation

🥇 Competitors

📣 Recent News

⏮️ Past

📶 Future

💲Current Valuation

🏷️ Fair Price

☑️ Checklist

💡 Investment Thesis

A major player in the solar photovoltaic field, with a concentration on large-scale solar projects and a dedication to improving its thin-film solar module technology. FSLR is able to capitalize on its U.S. market presence thanks to favorable policy incentives (Inflation Reduction Act), despite facing hard competition from traditional crystalline silicon technologies. Strong financial position, with a backlog of 75.9 GW in contracts through 2030 and a solid cash position of $1.74 billion. The new R&D innovation center in Ohio and the adoption of its bifacial Series 6 Plus modules place the company in a position for future growth.

Low Price/Forward Earnings and PEG ratios, compared to its 5-year averages. Based on my Fair Price estimate, currently may be undervalued by a significant 51.86%. I believe there is a good opportunity for potential entry, or at least, to add it to your watchlist.

🧐 Company Overview

Incorporated: 2006

Sector: Technology

Industry: Solar

Stock Style: Mid Growth

Market Cap: $27.75 Bil

Earnings Date: Oct 29 - Nov 4, 2024

Main competitors: ENPH, SEDG, RUNFirst Solar is a leading manufacturer of solar photovoltaic panels, modules, and systems for utility-scale development projects. The company specializes in thin-film solar technology, utilizing cadmium telluride to convert sunlight into electricity. As the world's largest thin-film solar module manufacturer, First Solar has established a significant presence in the global solar industry. The company operates production facilities in Vietnam, Malaysia, the United States, and India, with a focus on expanding its manufacturing capacity in recent years.

To read: Thin-film solar cell

First Solar's primary target market is the utility-scale solar sector, where it has historically maintained an estimated 30% market share in the United States. The company's strategy involves forward contracting, which provides a high degree of visibility into its near-term financial performance. As of June 30, 2024, First Solar's cash and cash equivalents stood at $1.74 billion, reflecting its strong financial position within the solar module industry.

🏰 Economic Moat

Despite its prominence in the solar industry, I don’t see that First Solar may have an economic moat. The solar module industry is characterized by intense competition and primarily competes on cost, resulting in a long history of poor returns on invested capital. However, the passage of the Inflation Reduction Act in 2022 has significantly improved First Solar's competitive position in its core U.S. market.

The thin-film technology, while unique, does not in essence provide a durable cost advantage over crystalline silicon competitors. The company's costs per watt are generally considered to be modestly higher than those of its crystalline silicon equivalent. However, First Solar's ongoing investments in research and development, including the completion of a dedicated R&D innovation center in Ohio featuring a high-tech pilot manufacturing line, may help the company maintain its technological edge and potentially improve its cost position in the future.

To read: Solar Panel Cost

🚀 Business Strategy

First Solar's business strategy is based on leveraging scale benefits to drive margin improvement and expanding its manufacturing capacity to meet growing global demand. The company has become increasingly focused on select end markets, particularly the United States and India, where policies provide a more favorable competitive position.

In the second quarter of 2024, First Solar manufactured a record 3.7 GW and sold 3.4 GW of solar modules. As of June 30, 2024, the company's total installed nameplate production capacity across all its facilities was approximately 17.6 GW. The company is in the process of expanding its manufacturing capacity by an additional 7.6 GW, with the goal of reaching an annual manufacturing capacity of more than 25 GW by the end of 2026.

The company's forward contracting strategy has provided stability in pricing and demand. As of June 30, 2024, First Solar had entered into contracts with customers for the future sale of 74.6 GW of solar modules, representing an aggregate transaction price of $22.3 billion, which it expects to accept as revenues through 2030.

First Solar is heavily investing in its U.S. manufacturing capabilities, aligning with the incentives provided by the Inflation Reduction Act of 2022. The company is constructing its fourth and fifth manufacturing facilities in the United States, expected to commence operations in the second half of 2024 and late 2025. First Solar anticipates investing approximately $1.4 billion in these U.S. facilities and upgrades throughout 2024 and 2025.

The company's core business segments:

Photovoltaic (PV) Module Manufacturing. The company is one of the world's largest manufacturers of thin-film photovoltaic modules. They utilize a unique cadmium telluride (CdTe) technology, which provides a more sustainable and efficient alternative compared to traditional silicon-based solar panels. This segment serves various markets, including utility-scale solar projects, commercial applications, and residential installations.

Utility-Scale Solar Power Plants. FS develops, constructs, and operates large-scale solar power plants. This segment includes the installation of solar arrays that generate significant amounts of energy, typically feeding into the electrical grid. The company focuses on large utility projects, providing energy to utility companies and contributing to long-term power purchase agreements (PPAs).

Project Development. In this segment, First Solar engages in the development of solar energy projects from inception to completion. This includes site acquisition, permit processing, financing, and project management. The company also focuses on building strong relationships with investors and utilities to facilitate the growth of its project pipeline.

Operations and Maintenance (O&M). The company provides operations and maintenance services for solar power plants it has developed, as well as for third-party installations. This segment includes monitoring performance, ensuring optimal operation of solar power systems, and providing maintenance services to enhance energy production and system lifespan.

Energy Sales. Through its developed projects, FS also engages in energy sales, where it sells electricity generated from its solar facilities directly to utilities and other customers under long-term contracts. This strategically aligns with their goal of securing stable, recurring revenue streams.

Read more premium insightful content on my Patreon 👇

✅ Advantages

Strong balance sheet and financial position. As of June 30, 2024, the company's current ratio was 2.23, indicating sufficient capital to meet near-term debt obligations. The company's debt-to-capital ratio has also been declining, further strengthening its financial position.

Focus on technological innovation. In October 2023, the company began commercial production of its bifacial Series 6 Plus modules, featuring an innovative transparent back contact that allows for higher energy yield. This ongoing product development helps First Solar maintain its competitive edge in the market.

The company is well-positioned to benefit from U.S. solar manufacturing incentives, particularly those introduced in the Inflation Reduction Act. These incentives are expected to contribute significantly to First Solar's earnings power in the coming years.

❌ Disadvantages

A highly mass-marked industry where differentiation is limited, and innovations are quickly copied by competitors. First Solar's cost per watt is generally higher than that of crystalline silicon peers, which can be a disadvantage in price-sensitive markets.

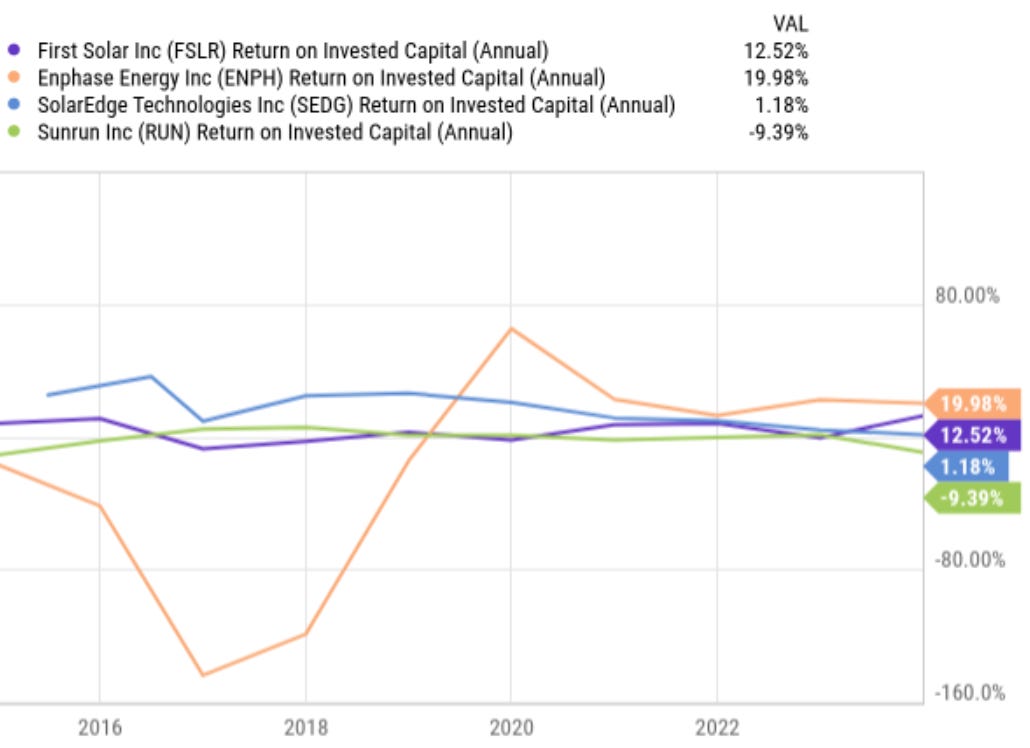

Historical returns on invested capital and margins have lagged behind industry-leading peers. This underperformance in key financial metrics may raise concerns for investors seeking best-in-class profitability.

Their end markets are relatively concentrated, with the U.S. and India. This geographical concentration could expose the company to risks associated with policy changes or economic downturns in these specific markets.

Related analysis:

🏛️ Capital Allocation

From my perspective, their capital allocation strategy is focused on expanding their manufacturing capacity and investing in R&D. In 2024, the company expects to invest between $1.8 billion and $2.0 billion in building new manufacturing facilities, expanding existing ones, and upgrading machinery and equipment.

The company has maintained a conservative capital structure, which is viewed as a competitive advantage in the volatile solar industry. Long-term debt as of June 30, 2024, totaled $0.42 billion, with current debt at $0.14 billion, significantly lower than its cash reserves of $1.74 billion.

First Solar has not paid a dividend in its history and is not expected to do so in the near future. The company has a limited record of equity issuance, which is viewed positively, and its stock-based compensation is relatively modest compared to broader solar industry peers.

First Solar acquired some smaller companies. For example, in May 2023, First Solar agreed to pay $38 million to buy Swedish manufacturing startup Evolar AB, as it seeks to expand the development of high-efficiency tandem PV tech.

The previous acquisition was in 2026 — Enki Tech (San Francisco). Enki Technology develops and markets coatings for the glass casing of PV modules for the solar photovoltaic industry. The company offers drop-in solutions which enable module manufacturers to control the properties of the casing glass like durability, optical performance, and surface energy during the manufacturing process.

🥇 Competitors

First Solar operates in a highly competitive industry dominated by crystalline silicon technology, which accounts for approximately 95% of the market. While their thin-film technology represents only about 5% of the overall market, the company faces competition from both traditional crystalline silicon manufacturers and new entrants in the solar module space.

In the U.S. utility-scale solar market, where First Solar has historically held a strong position, the company competes with a range of domestic and international manufacturers. The competitive landscape is evolving rapidly, with increasing attention on domestic production capabilities due to recent policy initiatives favoring U.S.-made solar products.

📣 Recent News

On Sep 26, 2024, First Solar opened a $1.1B, 3.5 GW solar factory in Alabama.

On July 18, 2024, First Solar commissioned a new R&D innovation center in Lake Township, Ohio, believed to be the largest facility of its kind in the Western Hemisphere. The facility covers 1.3 million square feet and includes a high-tech pilot manufacturing line allowing for the production of full-sized prototypes of thin film and tandem PV modules.

On June 04, 2024, First Solar became the solar industry’s first EPEAT Climate+ Champion, setting a new global standard for ultra-low carbon solar.

⏮️ Past

FS reported net sales of $1 billion in Q2 2024, up $200 million from Q1 2024, driven by a 24% increase in megawatts sold. The company's gross margin improved to 49%. Operating income reached $373 million. The firm earned $3.25 per diluted share and maintained a cash position of over $1.8 billion. With a continued focus on technological advancements and manufacturing efficiency, First Solar kept its full-year 2024 guidance steady. The company remains well-positioned despite political and market uncertainties, with a strong backlog of 75.9 GW and robust demand from data centers expected to drive future growth.

First Solar has outperformed the industry and the S&P 500 for three, five, and ten years (CAGR).

📶 Future

Based on their latest earnings report, with year-to-date net bookings of 3.6 GW and a substantial contracted backlog of 75.9 GW, demand remains strong. The company's manufacturing capabilities are expanding, as evidenced by record Q2 production of 3.7 GW and ongoing expansion projects in multiple states.

Technologically, First Solar continues to innovate, achieving a world record CdTe research cell conversion efficiency of 23.1% and progressing with their CuRe technology launch.

Looking ahead, First Solar has reiterated its 2024 guidance, projecting net sales between $4.4B to $4.6B and earnings per diluted share of $13.00 to $14.00. The company expects a stronger second half of the year, with 60% of earnings forecasted for Q4.

Analyst estimates reflect strong growth expectations over the next three fiscal years. In FY 2024, sales are projected to reach $4.49 billion, representing a year-over-year increase of 35.23%. EPS is expected to be $13.50, showing a robust 67.78% year-over-year growth. The positive trend continues in FY 2025, with sales forecasted to grow by 26.13% to $5.66 billion and EPS climbing to $22.07, marking a 63.50% increase. By FY 2026, sales are anticipated to reach $6.73 billion, up 18.88%, while EPS is projected to grow to $30.69, with a slightly slower but still impressive 39.04% increase. These estimates suggest sustained momentum for the company across sales and profitability metrics.

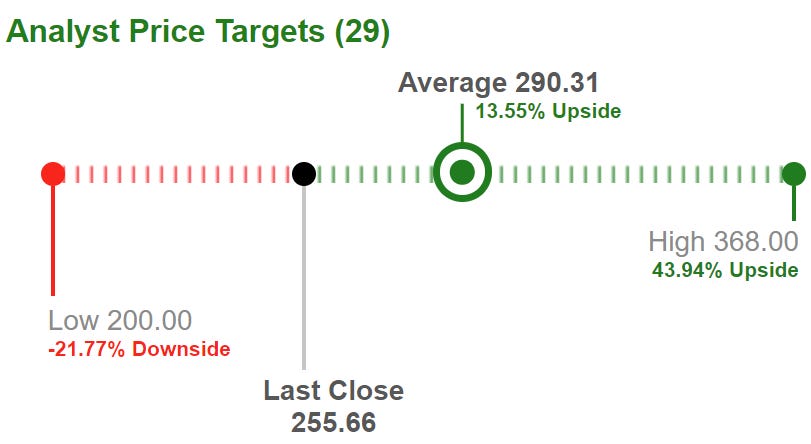

The current average price target is $290.31, representing a 13.55% upside from the last closing price of $255.66. On the bullish end, the high price target is set at $368.00 (43.94% upside). However, on the bearish side, the low price target stands at $200.00 (21.77% downside). This range highlights a mix of optimism and caution among analysts regarding the stock's future trajectory.

The broker rating breakdown has remained quite consistent over the past three months, with a strong consensus on a bullish outlook.

💲 Current Valuation

Based on data provided by Morningstar, we can see that FSLR is currently trading below some key metrics compared to its 5-year averages. Especially, Price/Cash Flow, Price/Forward Earnings, and the PEG ratio. Also, worth noting is a high Earnings Yield (4.39%).

Due to high future estimates in terms of earnings, the current PEG ratio is very low.

Valuation relative to the sector (Solar):

Forward values for cash flow, earnings, and PEG are higher than the sector. But some, no less important, values (Price/Book, Price/Sales) are higher.

Curious about my personal investment choices? Get access to the Long-Term Pick Portfolio and Watchlist.

🏷️ Fair Price

➡️ Updated fair price valuation: https://longtermpick.com/p/updated-valuations-nov-24

The Long-Term Pick's Fair Price (Base Case) for FSLR is $541.45. The current price of $260.68 is lower by 51.86%.

Fair-to-Current Price (%): 51.86%

Current Price/Fair Price: 0.48

I used:

Discount Rate: 12% (S&P 500 Next 5-Yr Growth Estimates is 11.90%)

Margin of Safety: 30%

Years: 10

Future EPS Growth Rate: 20% (See comments below)

Future Dividend and Buyback Yield: 0%

Total Future Annual Growth Rate: 20 + 0 = 20%

Based on Yahoo Finance and Koyfin data, the next 5-year CAGR forecast is insanely 56%. Why did I take 20%:

Constant shares outstanding dilution

I expect an economic slowdown in the next 1-2 years

High competition landscape

By the way, pay attention that my forward 5-yr PEG ratio is 1.16, which is low.

For the Base Case, the Future Expit P/E is 20. 5-year average P/E ratio is 34; I decided to just take the future EPS growth rate which is 20.

As you can see, the stock is undervalued in all cases — Base, Bull, and Bear. This is due to high future growth expectations. In justification of my assessments, I made a DCF valuation (see the Checklist below) and I got $529 which is very close to my Base Case Fair Price estimate ($541.45).

☑️ Checklist

Profitability:

✅ Gross margin at least 40%: 46%

✅ Net margin at least 10%: 32%

✅ Management (ROIC, ROCE, ROE, ROA): Yes (All above 10%)

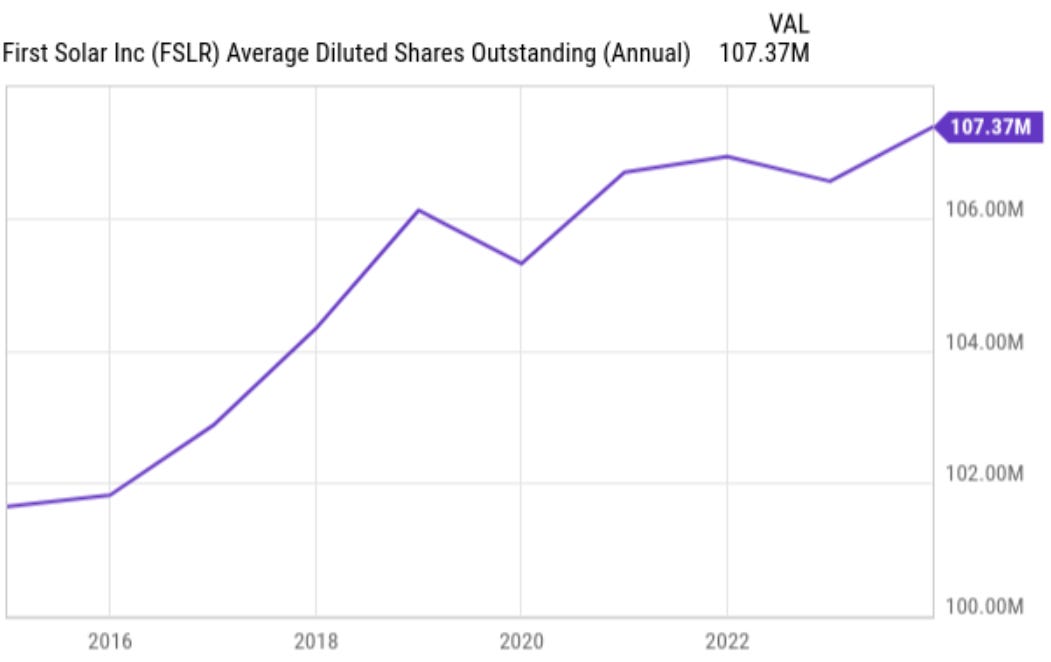

❌ Piotroski F-Score: 6 of 9 (Not passed: CFROA > ROA, Higher Current Ratio YoY, Less Shares Outstanding YoY)

❌ Revenue surprises in last 7 years: No (Missed all last seven years — Based on TradingView's data)

❌ EPS surprises in last 7 years: No (Missed: 2018, 2019, 2020 — Based on TradingView's data)

❌ EPS growth YoY last 7 years: No (Declines in 2018 and 2022)

Valuation and Advantage:

✅ Valuation below its 5-yr average: Yes

❌ Does it have a moat: No

Shares:

✅ Insider ownership at least 5%: Yes (5.34%)

❌ Less shares outstanding YoY: No

❌ Insider buys last six months: No

Price:

✅ 1-year stock price forecast is above 10%: +13.55%

✅ Next 5-Yr CAGR is above S&P 500: Yes (56.70% vs 11.90%)

✅ DCF Value: $529 (Highly undervalued by 51%; 10 years, discount rate: 10%, terminal growth: 3%, equity model: FCFE)

✅ Short Interest below 5%: Yes (4.04%; Data by SeekingAlpha)

This is not a financial or investing recommendation. It is solely for educational purposes.