Toast: Platform Scale, Margin Expansion, and Long-Term Value Creation

A comprehensive analysis of Toast Inc. (TOST).

Content:

• Company Overview

• Market Overview

• Economic Moat

• Business Strategy

• Capital Allocation

• Advantages

• Disadvantages

• Competitors

• Past

• Future

• Current Valuation

• Fair Price

• Due Diligence

• Investment Thesis

Company Overview

IPO Date: Sep 22, 2021

Market Cap: ~$19.87B

Sector: Technology

Industry: Software - Infrastructure

Type: Mid Growth

Total Number of Employees: ~5,700

Next earnings report: Feb 12, 2026 (approved; after-market)

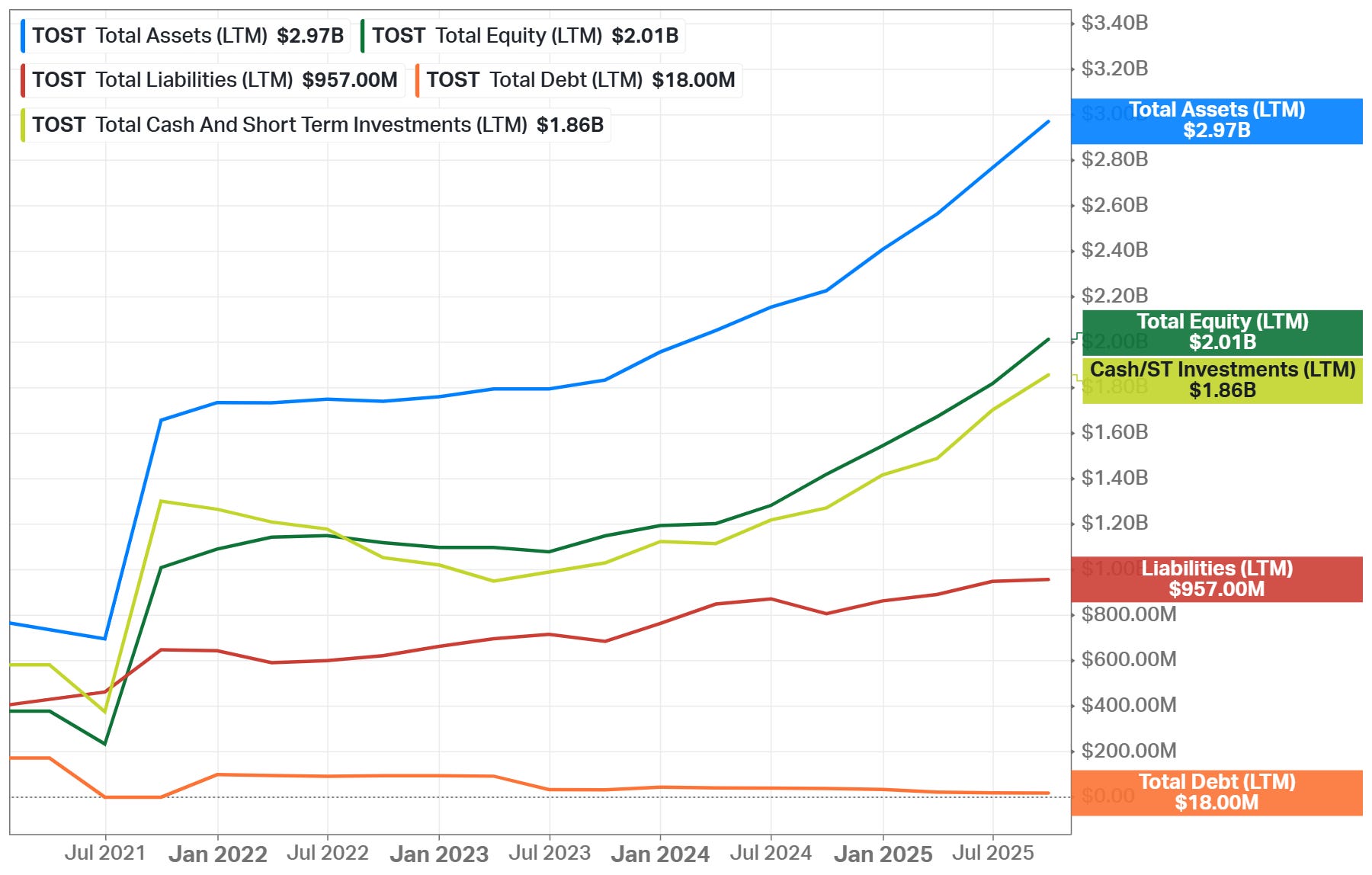

Total Debt: $18M

Cash & Investments: $1.86B

Beta: 1.94

Website: pos.toasttab.com

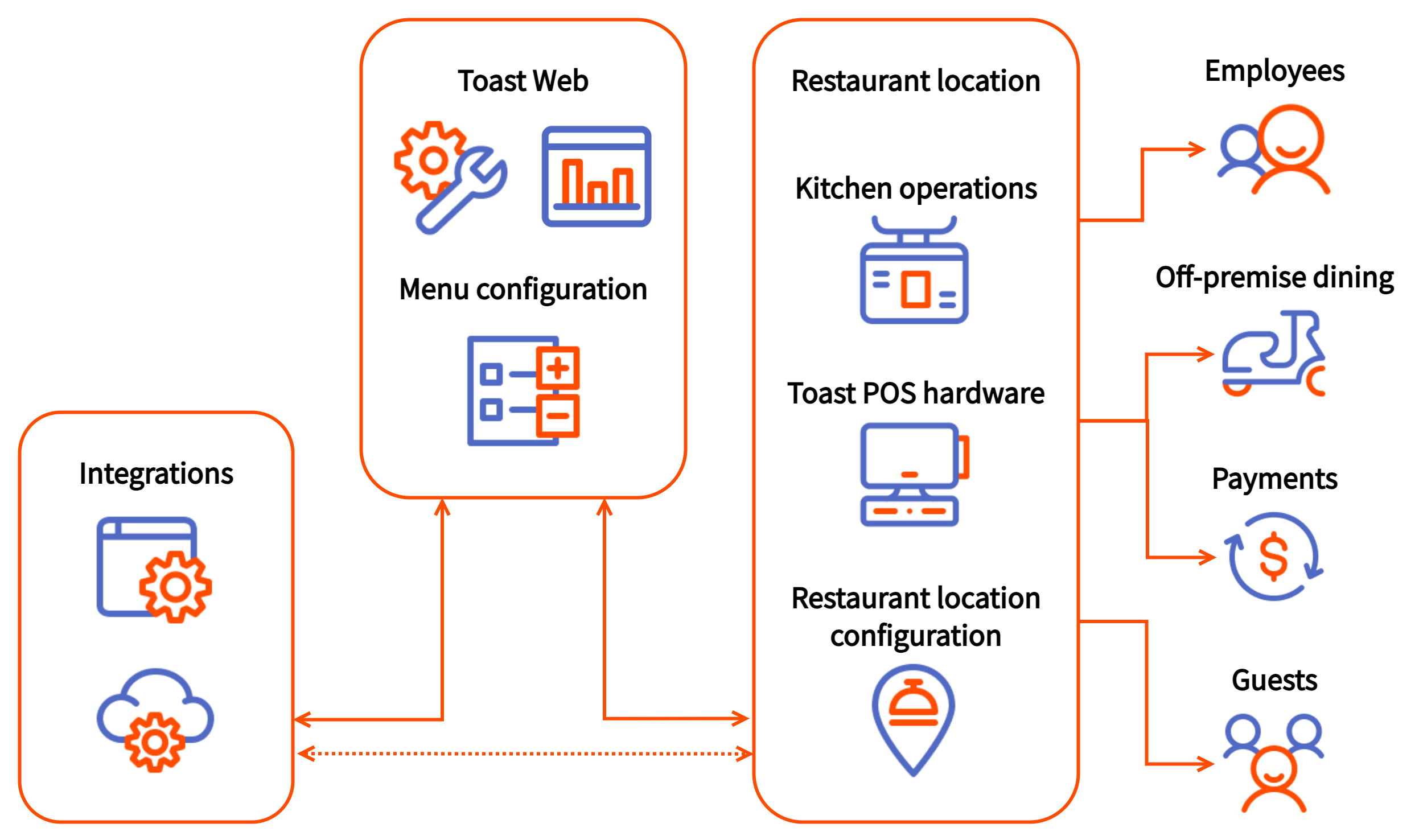

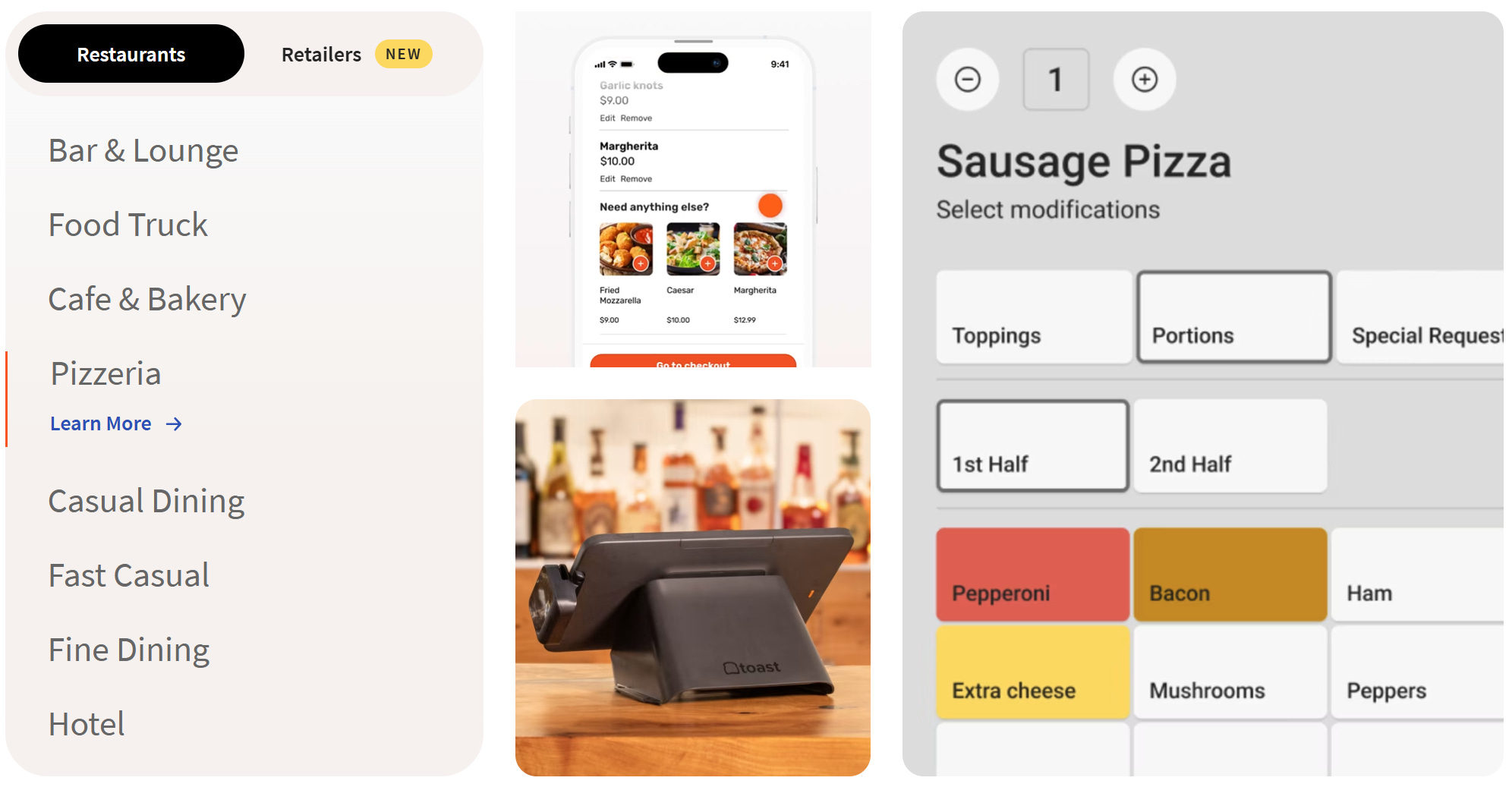

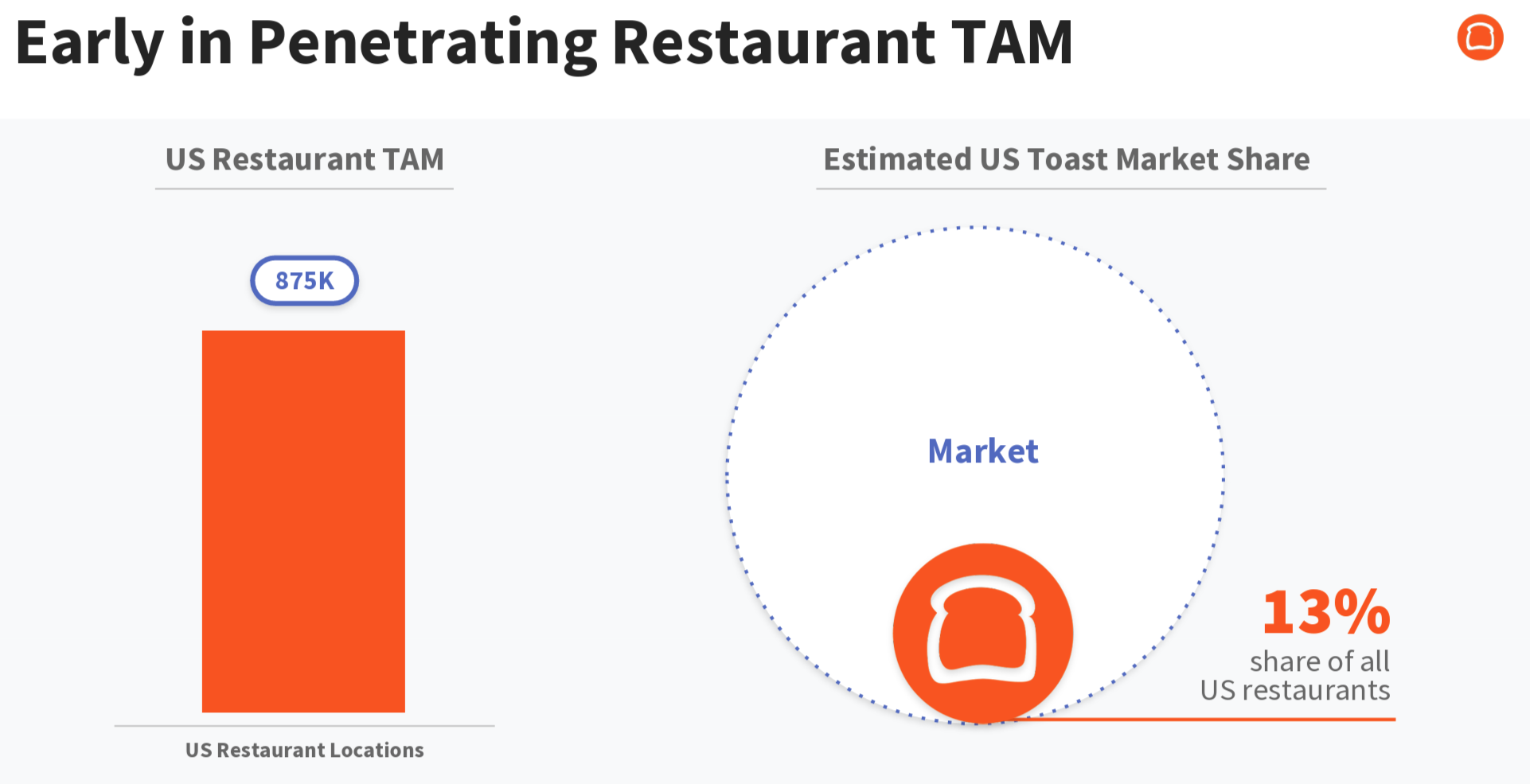

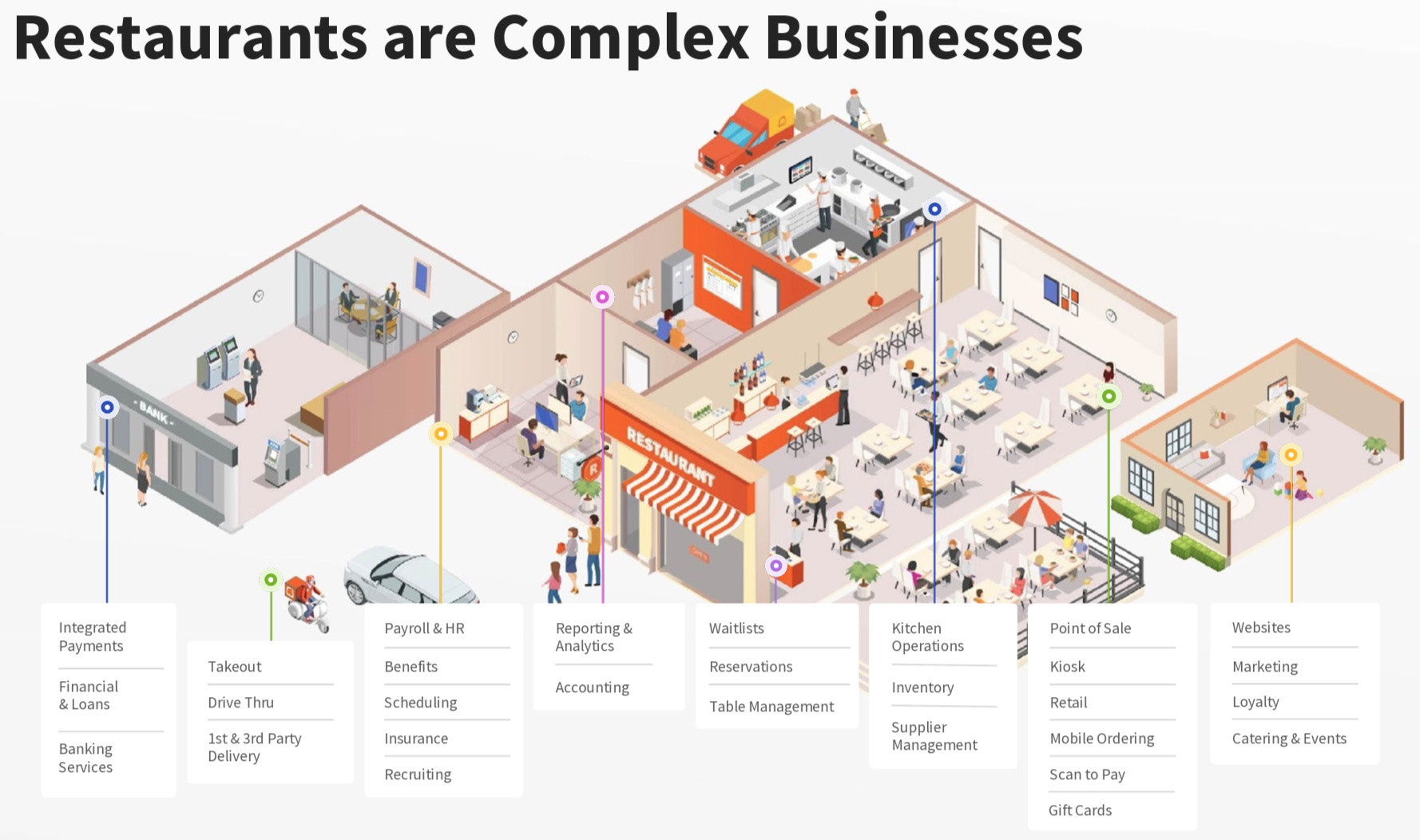

Toast Inc. (NYSE: TOST) is a cloud-based technology company that builds a full digital operating platform for restaurants. The platform combines point-of-sale software (POS), payment processing, and purpose-built hardware into one integrated system. Toast mainly serves small and mid-sized restaurants in the United States, but it has been expanding into enterprise restaurant groups, international markets, and food and beverage retail. As of the third quarter of 2025, the platform supported approximately 156,000 active locations, showing steady adoption across different restaurant formats.

To Watch: Meet Toast in 90 seconds

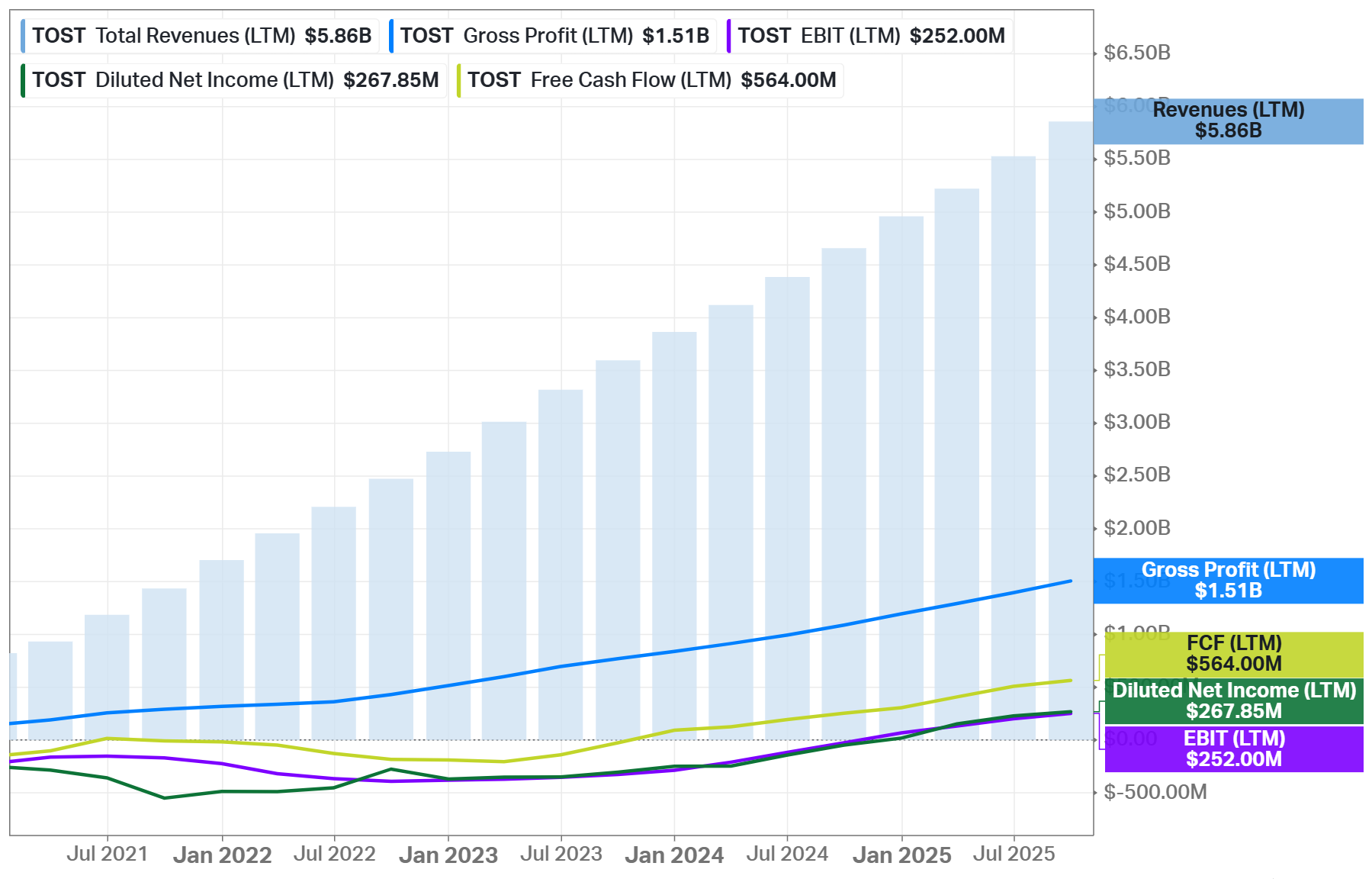

Toast’s revenue model is recurring income. The company earns revenue from software subscriptions, transaction-based financial technology solutions, and hardware-related services. In Q3 2025, Toast surpassed $2.0 billion in annualized recurring run-rate revenue, which marks a structural shift from early-stage growth to scaled operations. Total quarterly revenue reached $1.63 billion during the same period, supported by strong performance in subscription services and payment processing activity.

Analyst’s Note:

Revenue Run Rate is an indicator of financial performance that takes a company’s current revenue in a certain period (a week, month, quarter, etc.) and converts it to an annual figure to get the full-year equivalent. This metric is often used by rapidly growing companies, as data that’s even a few months old can understate the current size of the company. Another term for this is the Sales Run Rate. Read more.

Toast is led by its co-founder and CEO, Aman Narang. He guided the company from its early development into a scaled public business and remains closely involved in long-term strategy. Management emphasizes controlled expansion, disciplined investment, and gradual margin improvement. This approach allowed the company to remain growth-oriented while reaching consistent profitability at the operating level.

The platform is used by a broad range of restaurant clients. Toast serves independent operators, regional chains, and large enterprise customers. Notable customers include Nordstrom, which is rolling out Toast across nearly 200 dining locations, TGI Fridays, which is moving its existing U.S. restaurants from another POS system to Toast, and Everbowl, a fast-growing multi-location brand. Toast is also used by many fine-dining restaurants, including a significant share of Michelin-recognized locations and restaurants featured by Bon Appétit.

In addition, Toast works with third-party partners such as Uber, which supports delivery and off-premise ordering, and Coca-Cola, which collaborates on data-driven beverage sales initiatives.

To Read: Toast and Uber Announce Strategic Partnership to Help Restaurants Drive Guest Demand

Market Overview

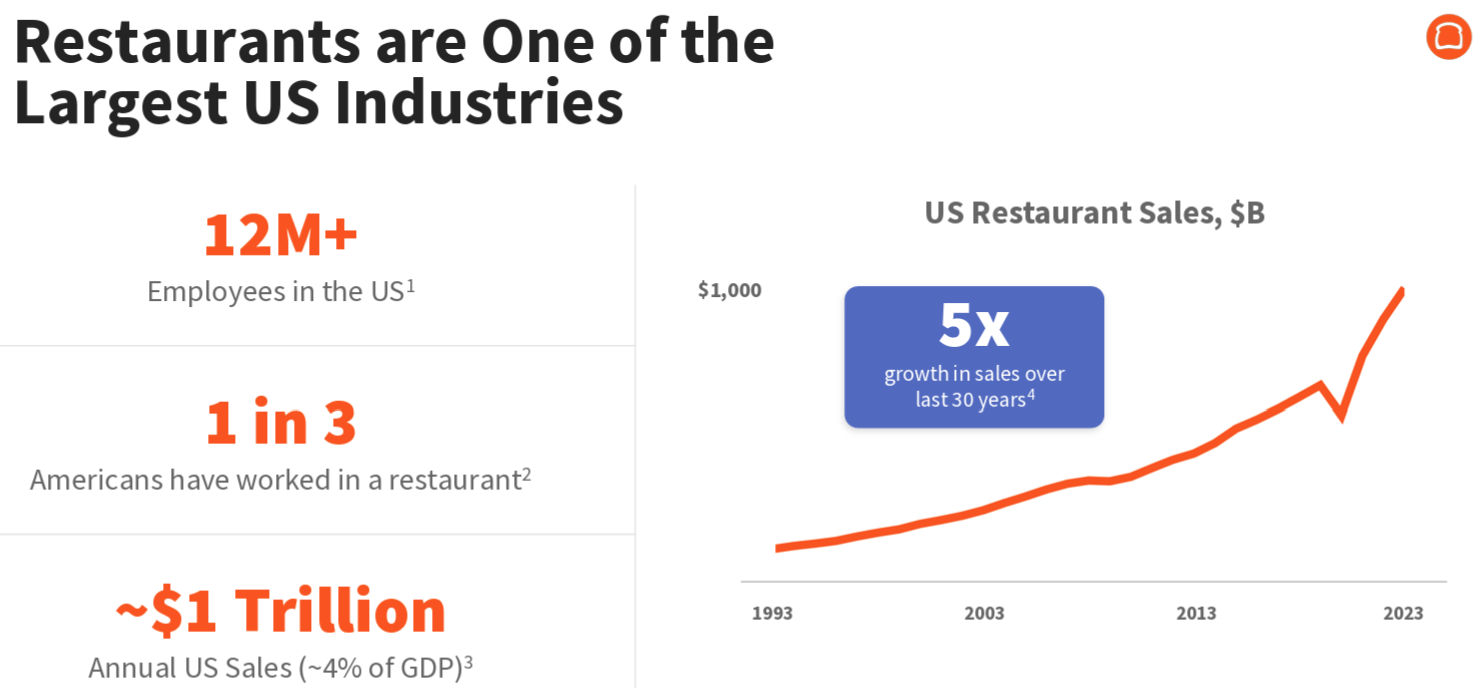

The restaurant industry is one of the largest service sectors globally and provides the economic foundation for restaurant-focused technology platforms. In the United States, restaurant and foodservice sales reached approximately $1.5 trillion in 2025, with activity remaining resilient into early 2026. The sector includes more than one million restaurant locations and employs over 15 million people, highlighting both scale and operational complexity.

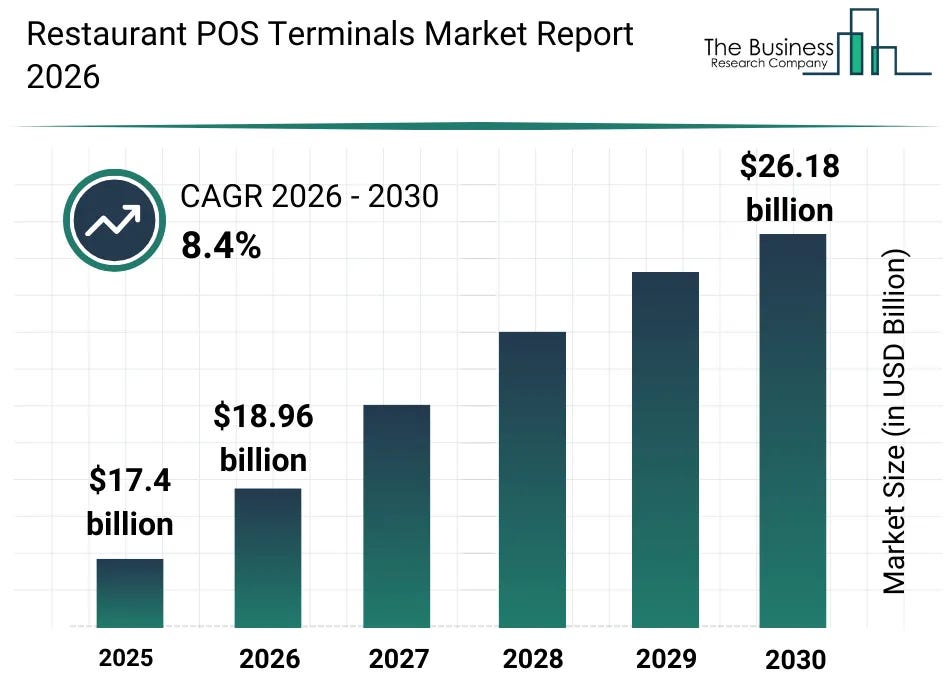

The technology layer serving restaurants is expanding alongside the industry. The global restaurant POS terminal market was estimated at $17.4 billion in 2025 and is projected to grow at around an 8% compound annual growth rate (CAGR) through the end of the decade. Growth is driven by the replacement of legacy systems, rising digital payment usage, and demand for secure and compliant payment infrastructure.

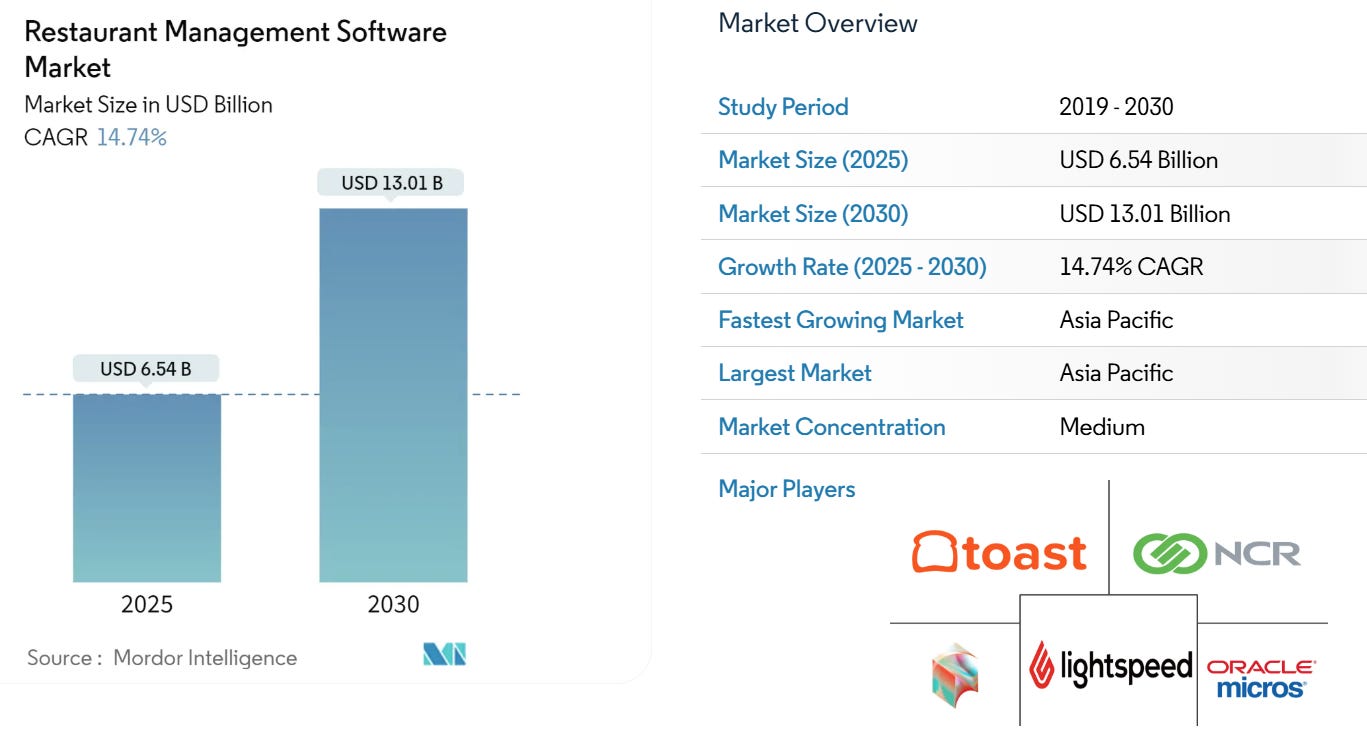

Software-focused segments are growing faster than hardware alone. Research firms estimate the global restaurant POS software and restaurant management software markets to grow at approximately a 14-15% CAGR through 2030. This reflects rising demand for subscription platforms that integrate ordering, payments, analytics, inventory, and labor management into a single system.

Payment economics also influence the market. McKinsey’s industry research shows long-term pressure on transaction take rates in pure payment processing due to competition and regulation. For vertically integrated platforms like Toast, this trend is less negative because a large share of value is captured through software subscriptions and operational services, rather than relying only on payment margins.

Analyst’s Note:

The numbers above:

~8% CAGR → applies to POS terminals/hardware

~14–15% CAGR → applies to POS software & restaurant management software

POS hardware is a mature market. Restaurants replace terminals every few years, but adoption is already high. Growth mainly comes from upgrades, compliance, and incremental expansion. That leads to mid-single-digit growth, around 8%.

POS software, on the other hand, is still in an expansion phase. Restaurants are moving from basic systems to cloud platforms with analytics, marketing, labor tools, and integrations. This drives double-digit growth, often in the mid-teens, which is where the 14–15% CAGR comes from.

Toast operates across both, but its long-term value is much more exposed to the faster-growing software layer.

Economic Moat

The company has a narrow economic moat driven primarily by switching costs. The platform is deeply embedded in restaurant operations, covering order flow, payments, inventory, staffing, payroll, and reporting. Replacing the platform would require coordinated changes across hardware, software, and internal workflows, creating operational disruption and risk.

Customer behavior. Toast reports retention close to 90%, which implies long customer relationships even in an industry with high failure rates. Most churn results from restaurant closures rather than competitive displacement, indicating operational dependence once adopted.

Unit economics support durability. Toast recovers customer acquisition costs in a relatively short period compared with the length of customer relationships. Hardware subsidies accelerate adoption, while recurring software and payment revenue generate value over many years, supporting sustained reinvestment.

Business Strategy

The company focuses on expanding its leadership in U.S. small and mid-sized restaurants while building additional growth engines. The core restaurant segment remains the primary revenue contributor, supported by continued location growth and deeper product adoption through cross-selling.

At the same time, Toast is investing in enterprise restaurants, international markets, and food and beverage retail. These segments are smaller today but are scaling and are expected to become meaningful contributors over time. Management believes the same vertical integration strategy can be applied across these markets.

Long-term scale ambition. Management announced a vision to expand from roughly 156,000 locations today to more than 500,000 locations over time.

Product innovation, including AI-driven tools such as Toast IQ and Toast Advertising, is central to increasing platform value and customer reliance.

Capital Allocation

The company follows a disciplined capital allocation strategy supported by a strong balance sheet and no long-term debt. A large cash position provides flexibility to invest through economic cycles without external financing.

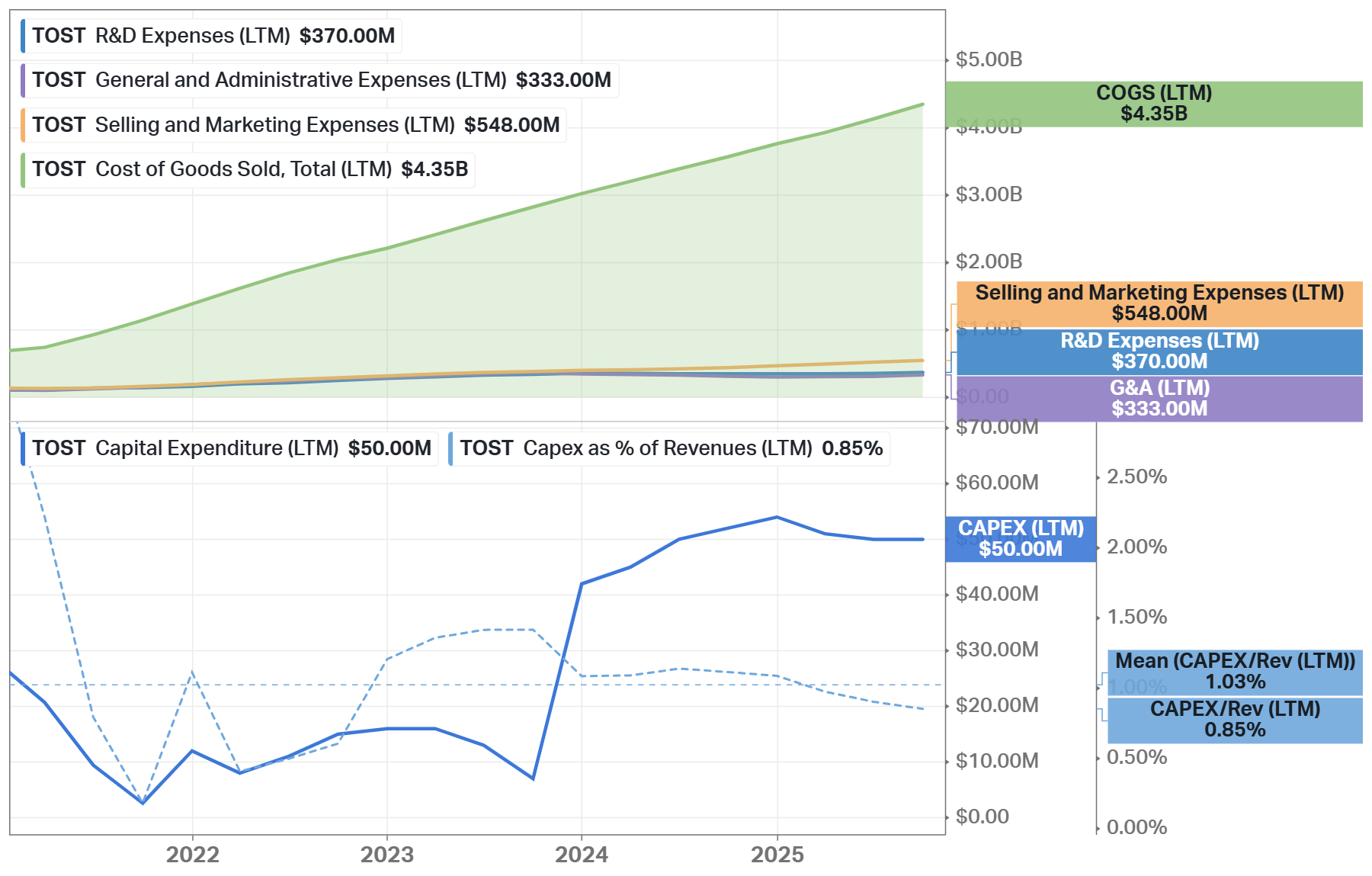

Capital is primarily deployed toward organic growth. Investments focus on research and development, sales capacity, and customer acquisition, including hardware subsidies that support platform adoption. These investments are justified by favorable unit economics and long customer lifetimes.

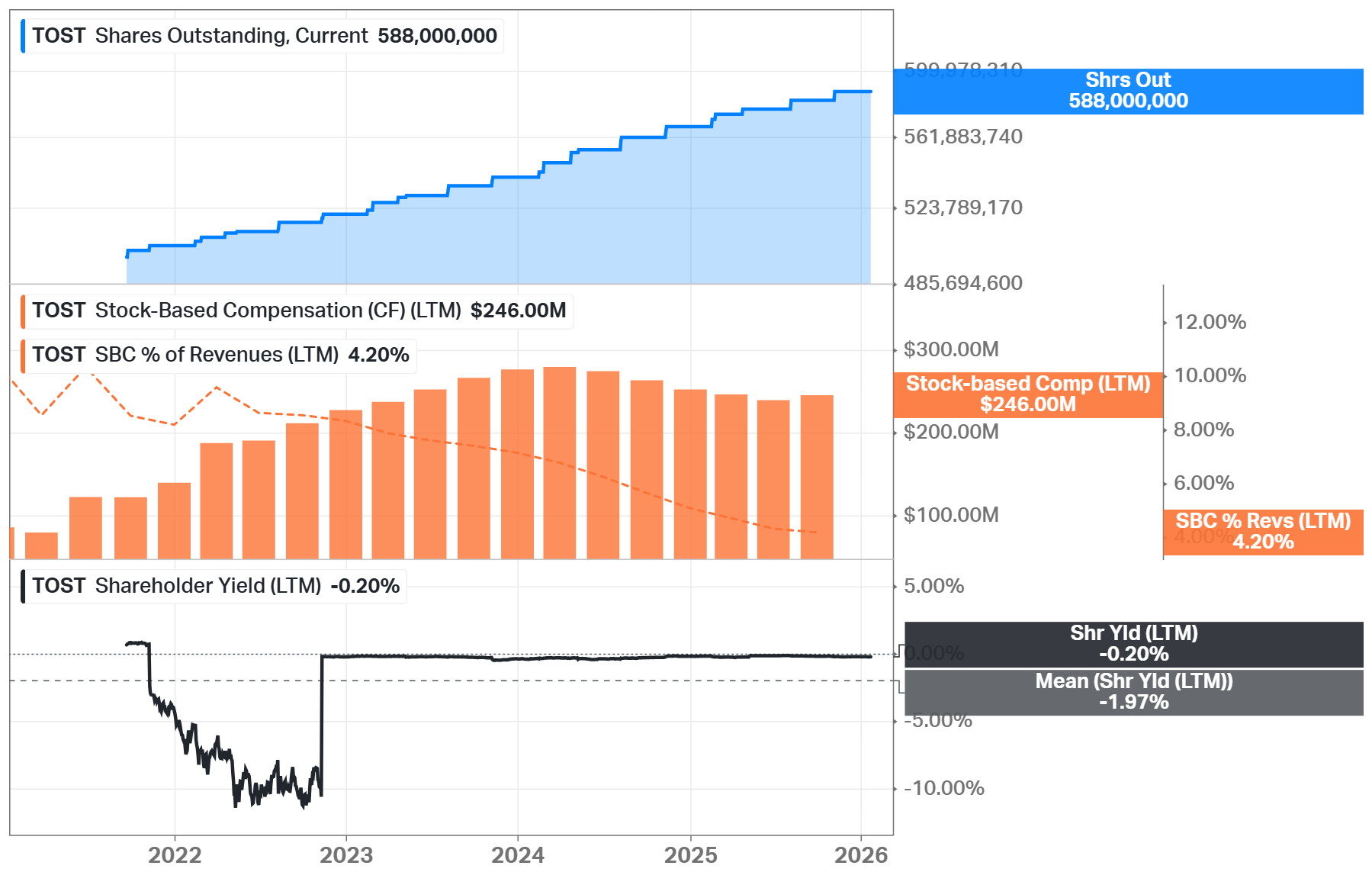

Toast also initiated modest shareholder returns through share repurchases, mainly to offset dilution. The company does not pay dividends. Acquisitions have been small and targeted, aimed at expanding product capabilities rather than scale-driven consolidation.

Advantages

Deep platform integration. The platform replaces multiple disconnected systems with one unified platform that supports daily restaurant operations. This simplifies workflows and reduces operational friction for restaurant owners and staff.

Data-driven insight. By processing large volumes of transactions, Toast can provide analytics and AI-driven recommendations that help restaurants improve pricing, promotions, and cost control. These insights increase platform value over time.

Strong customer retention. Retention near 90% indicates that restaurants that remain in business tend to stay on Toast. This stability supports predictable recurring revenue and long-term planning.

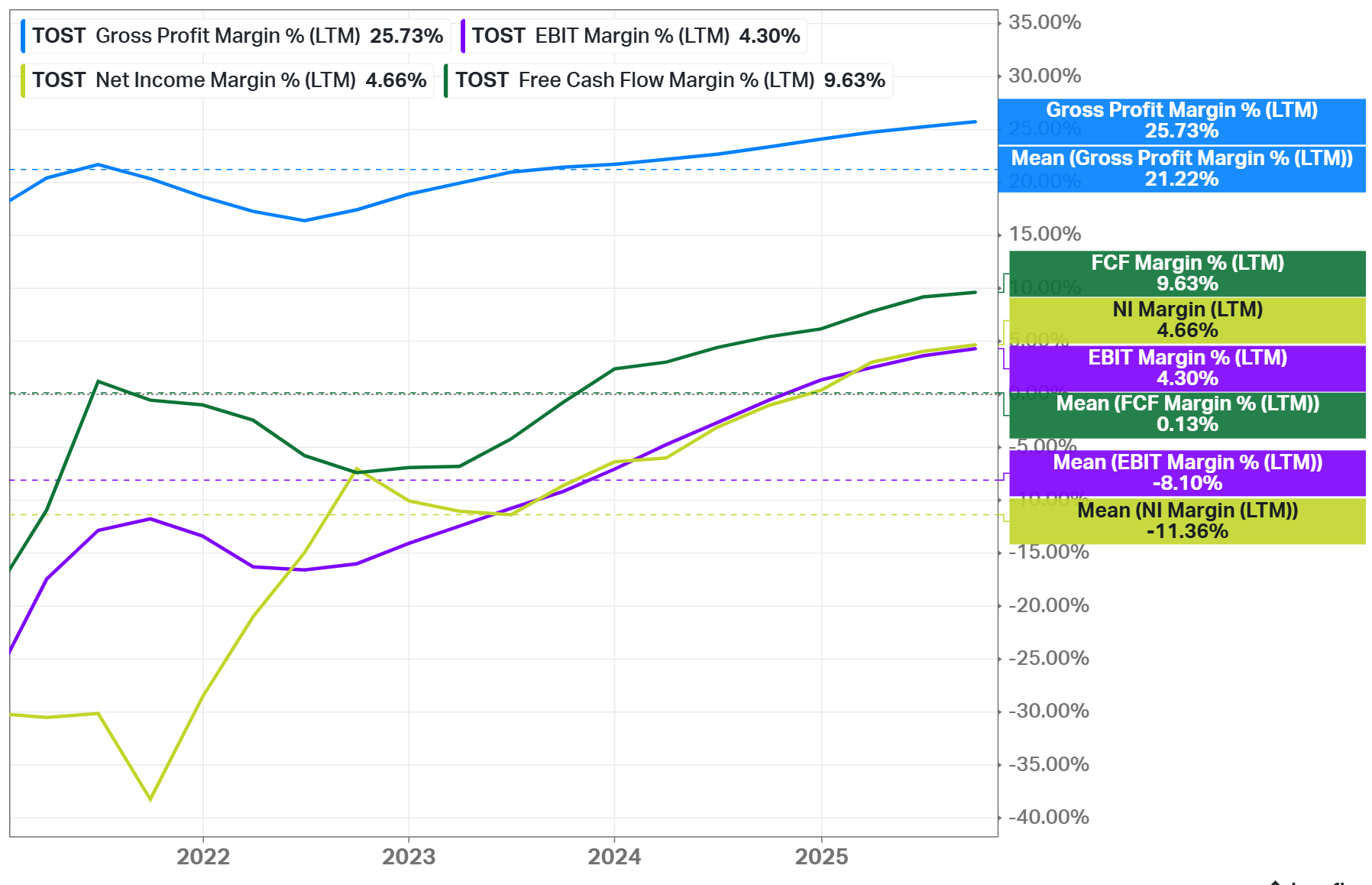

Improving operating leverage. High-margin software and fintech services represent an increasing share of revenue. As scale increases, profitability improves even if hardware growth moderates.

Validation from high-quality customers and partners. Adoption by enterprise operators and partnerships with companies like Uber and Coca-Cola strengthen platform credibility. These relationships support expansion into larger and more complex customers.

Disadvantages

Exposure to the restaurant industry risk. Restaurants operate with thin margins and high failure rates. Economic pressure can increase closures and negatively affect customer retention.

The slowing growth in the core market. As Toast increases penetration among U.S. mid-sized restaurants, incremental location growth becomes harder. Future growth depends more on new segments.

Execution risk in new verticals. Grocery and convenience retail differ from restaurants in operations and economics. Product-market fit in these areas is still developing.

Strong competitive pressure. Toast competes with large payment and software providers that have significant financial resources. This can limit pricing power and margin expansion.

Reliance on continued innovation. AI and marketing tools require sustained investment and customer adoption. If adoption slows, expected returns may weaken.

Competitors

Fiserv competes with Toast mainly through its Clover platform. Fiserv benefits from scale, long-standing payment relationships, and a broad merchant base. However, Clover is designed for many merchant types, which limits its depth in restaurant-specific workflows compared with Toast.

Block competes through its Square ecosystem, which is widely adopted by small businesses. Square offers simplicity and strong brand recognition, but it is not purpose-built for full-service and multi-location restaurants. Toast differentiates through deeper operational features tailored to restaurants.

To Read: Square vs Toast POS: Which is better for your restaurant in 2026

Adyen competes primarily in enterprise payment processing. It offers an advanced global payment infrastructure and a strong international reach. However, Adyen does not provide a full restaurant operating platform, which limits overlap with Toast’s core software-driven value proposition.

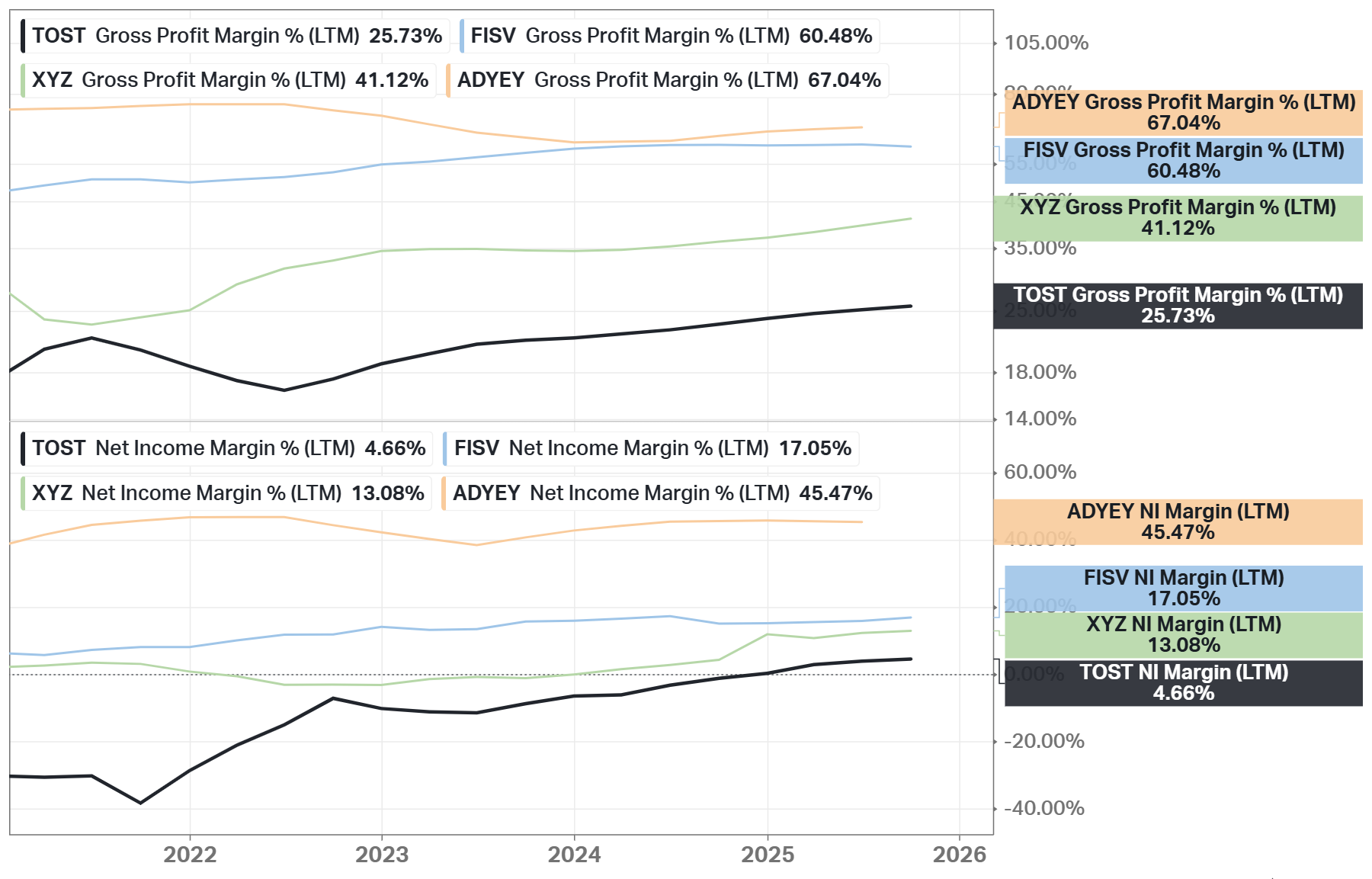

Toast shows higher expected earnings growth, which reflects a company still early in its profit expansion cycle. Lower gross and net margins indicate that the company continues to reinvest aggressively in customer acquisition, product development, and hardware subsidies, prioritizing long-term platform scale over near-term optimization. In contrast, competitors operate more mature models with higher margins and steadier returns, signaling efficient capital deployment but limited incremental growth opportunities.

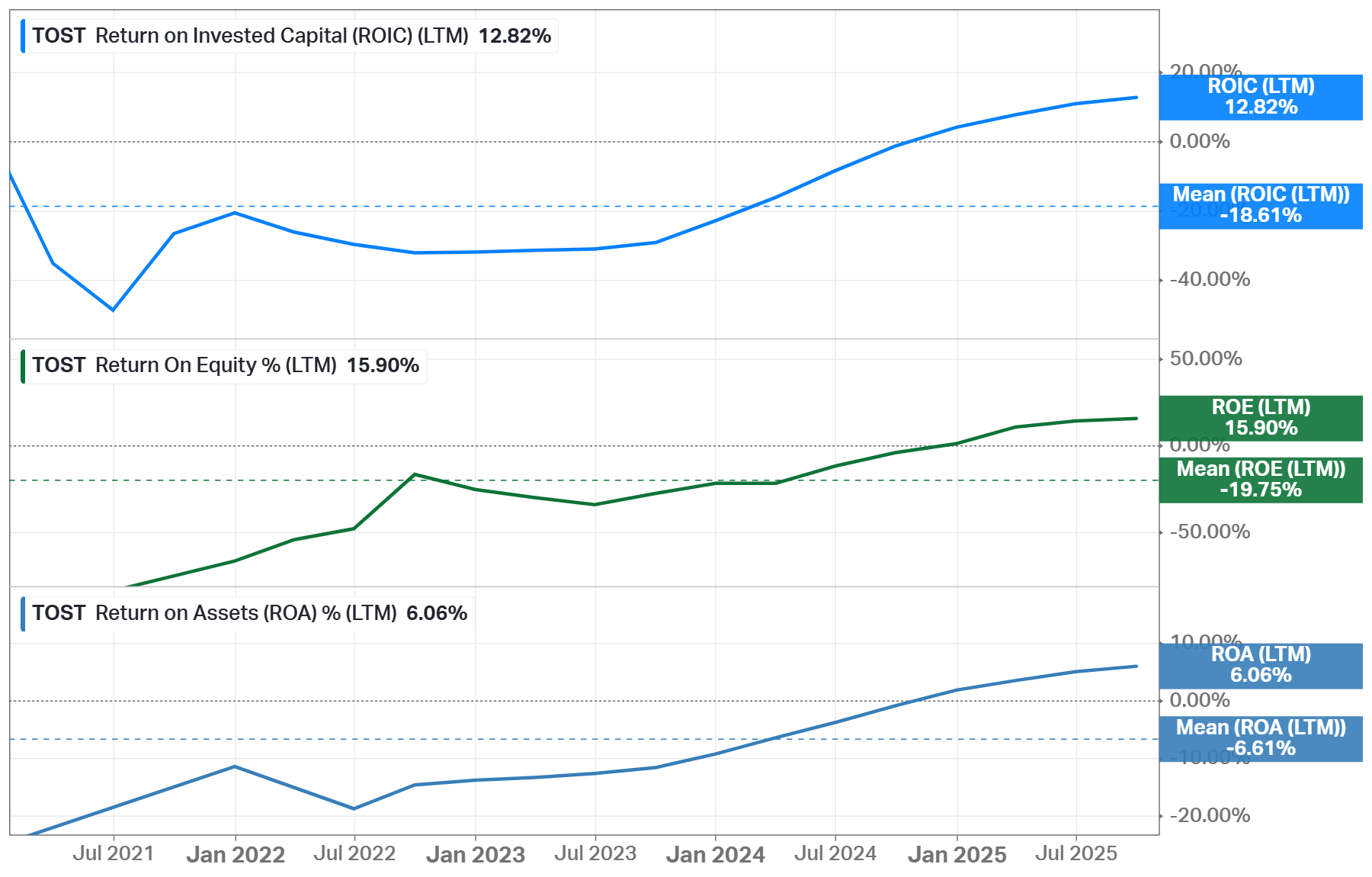

Toast’s improving ROIC suggests management is gradually converting growth into economic value, even if absolute efficiency still lags peers.

Past

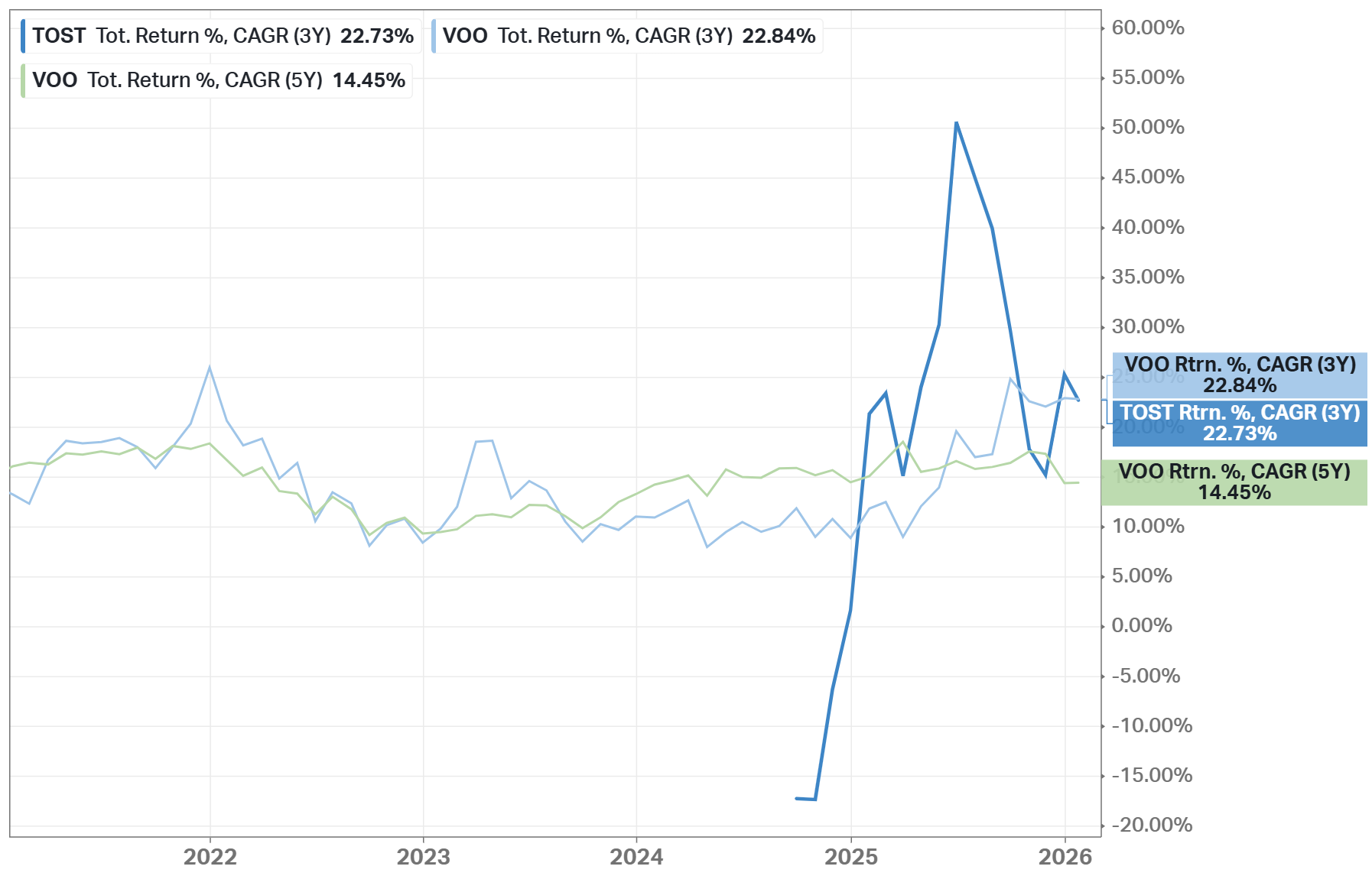

Here is the 3-year CAGR return for TOST, compared to the S&P 500 (VOO).

Below are some significant recent events.

Fortune Recognition: Toast was named a 2026 World’s Most Admired Company by Fortune, highlighting strong brand reputation and industry leadership among technology and hospitality peers.

New Jobs Expansion: In December 2025, the company announced it would create 120 new jobs in Dublin as part of a three-year investment to support growth in Europe and strengthen international operations.

Strategic Enterprise Adoption: Iconic restaurant brand TGI Fridays selected Toast’s platform for its entire U.S. presence, aiming to streamline operations and enhance guest experiences with integrated technology across multiple service channels.

Product Innovation — AI Insights: Toast expanded its platform with ToastIQ, an intelligence engine that delivers personalized prompts, recommendations, and automated workflows designed to help restaurants improve efficiency and revenue.

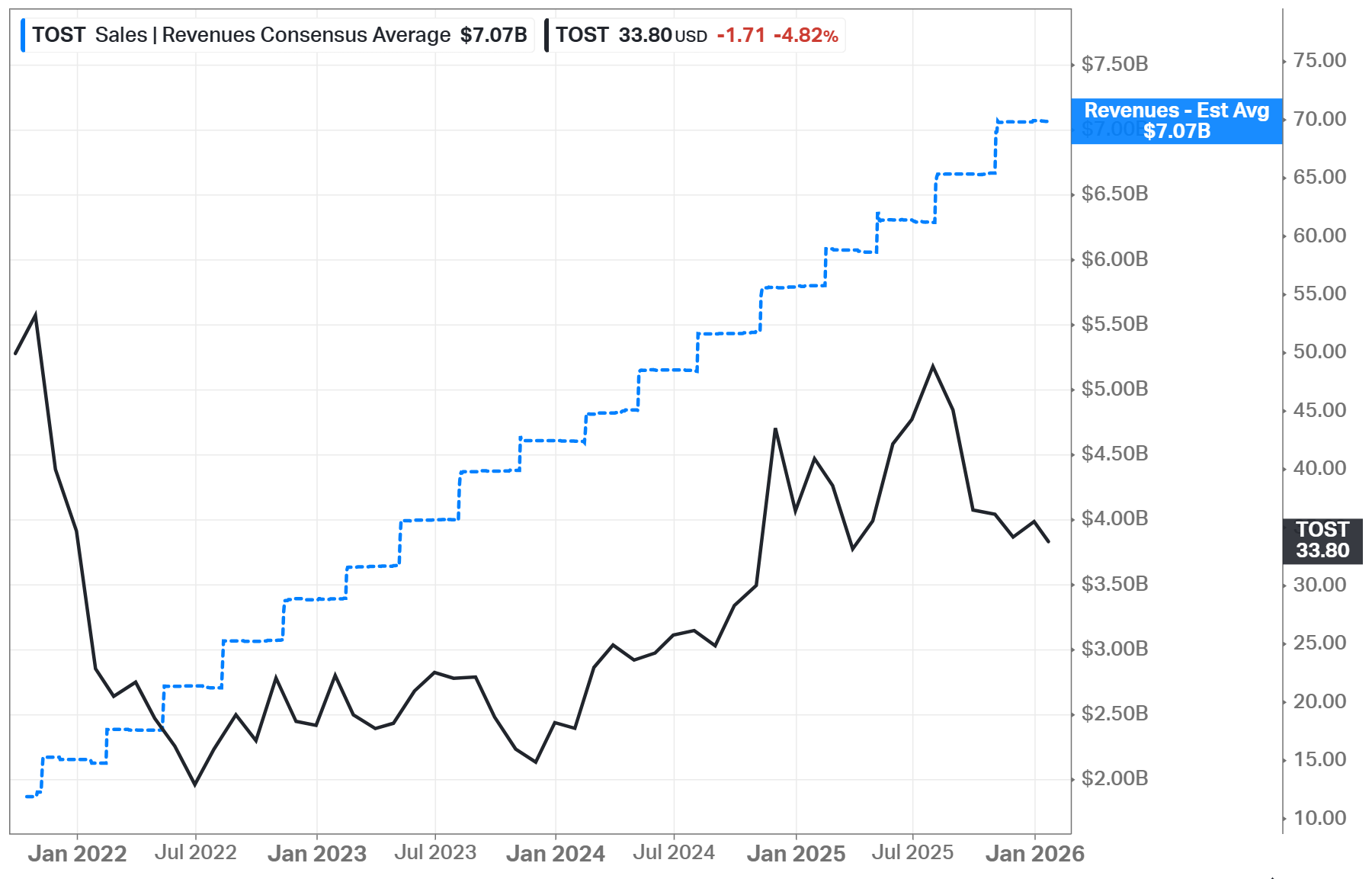

Future

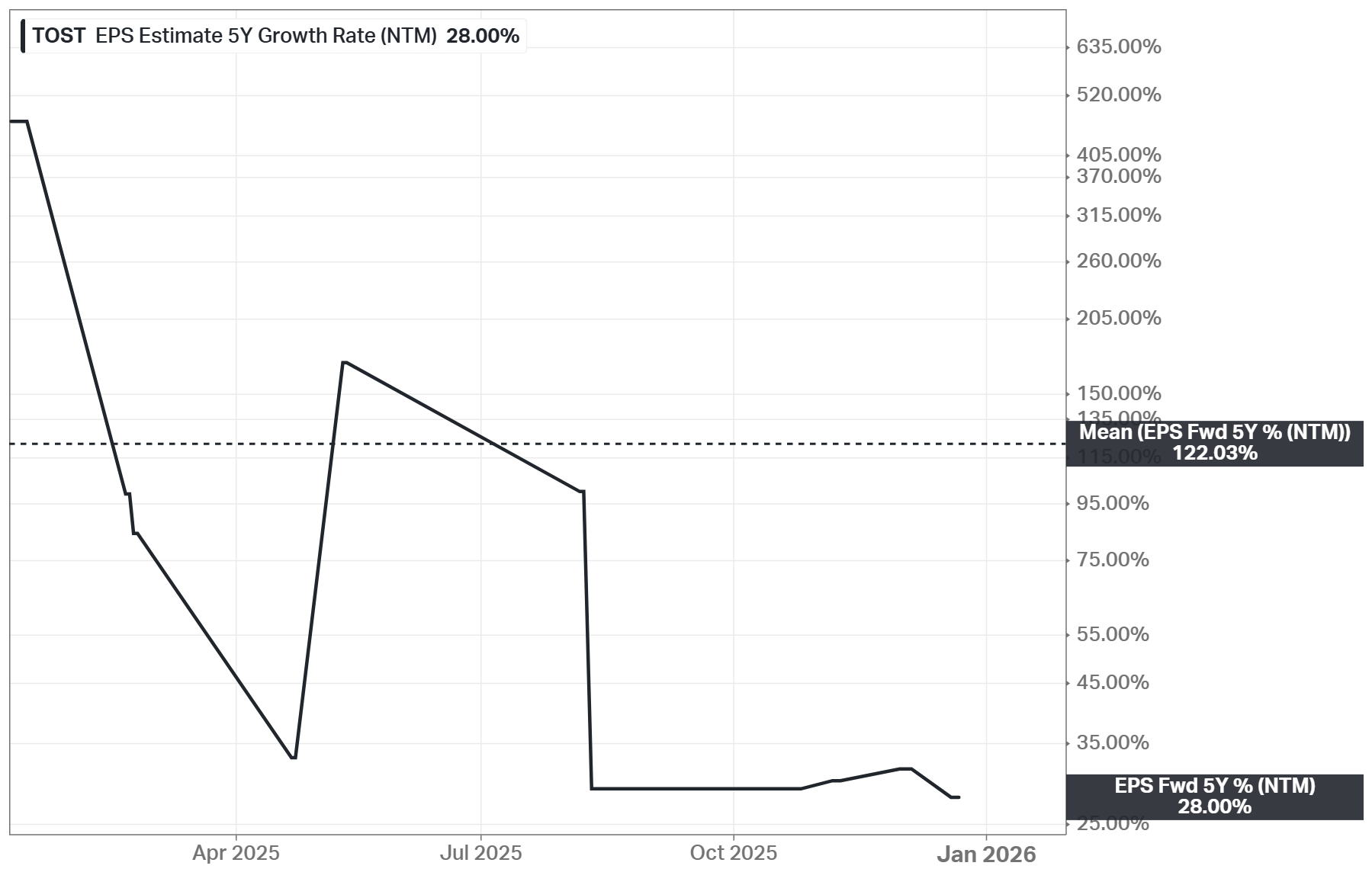

Here is the 3-year forecast for future sales and EPS growth. Note the high EPS growth prediction for fiscal year 2025.

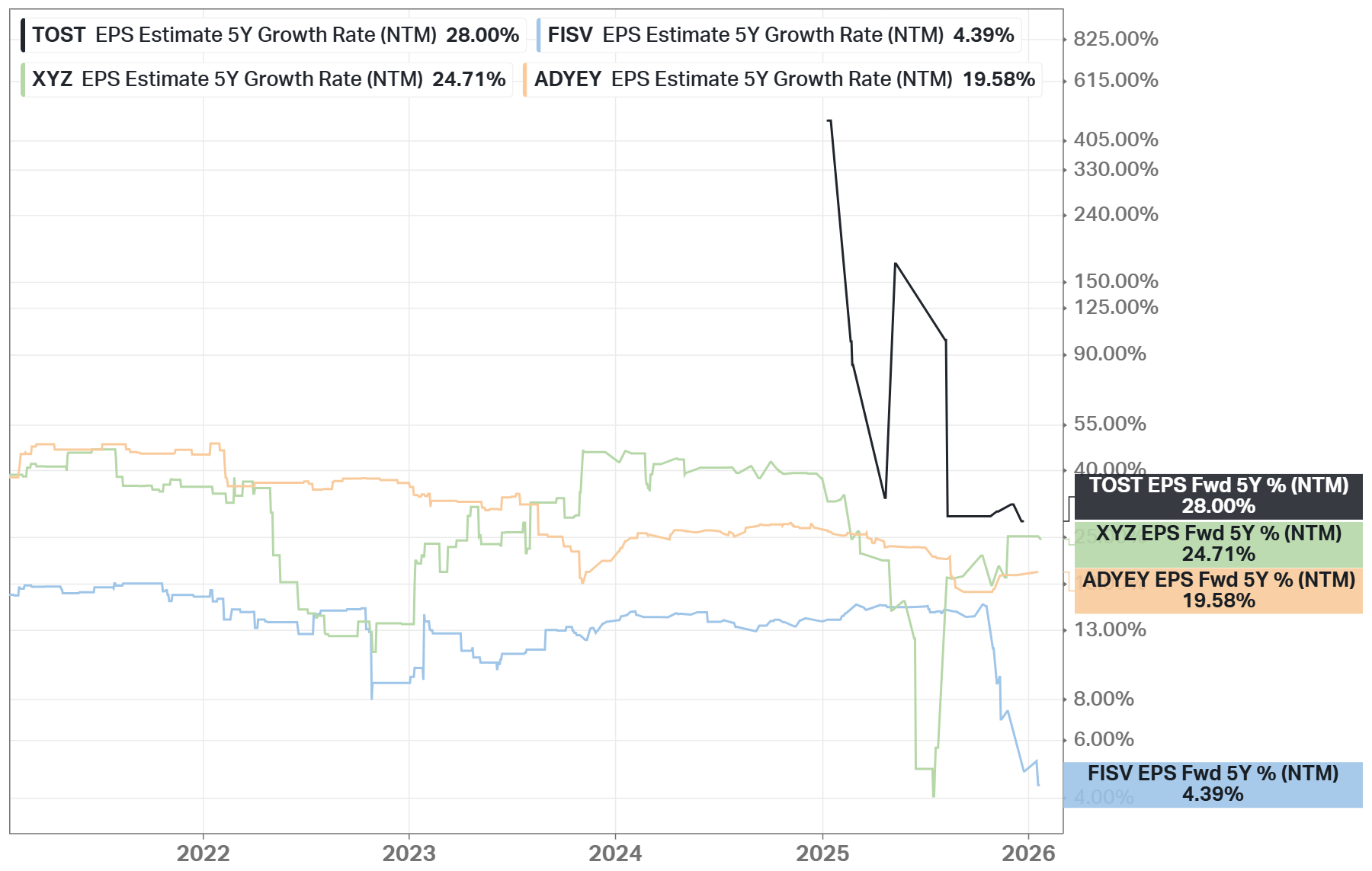

In addition, below is the EPS growth rate estimate for the next 5 years (CARG), the highest value among the competitors (section above).

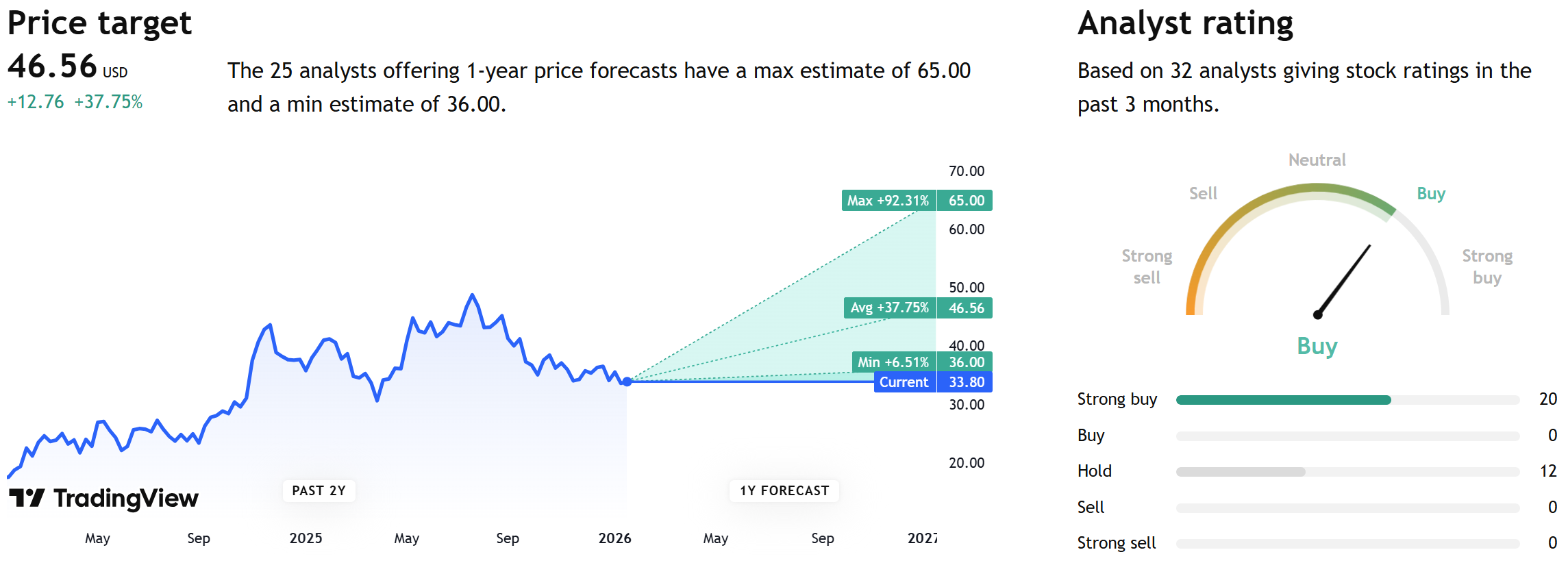

According to 1-year price targets provided by other analysts, the average target for TOST is $46.56, indicating a potential increase of 37.75%.

Current Valuation

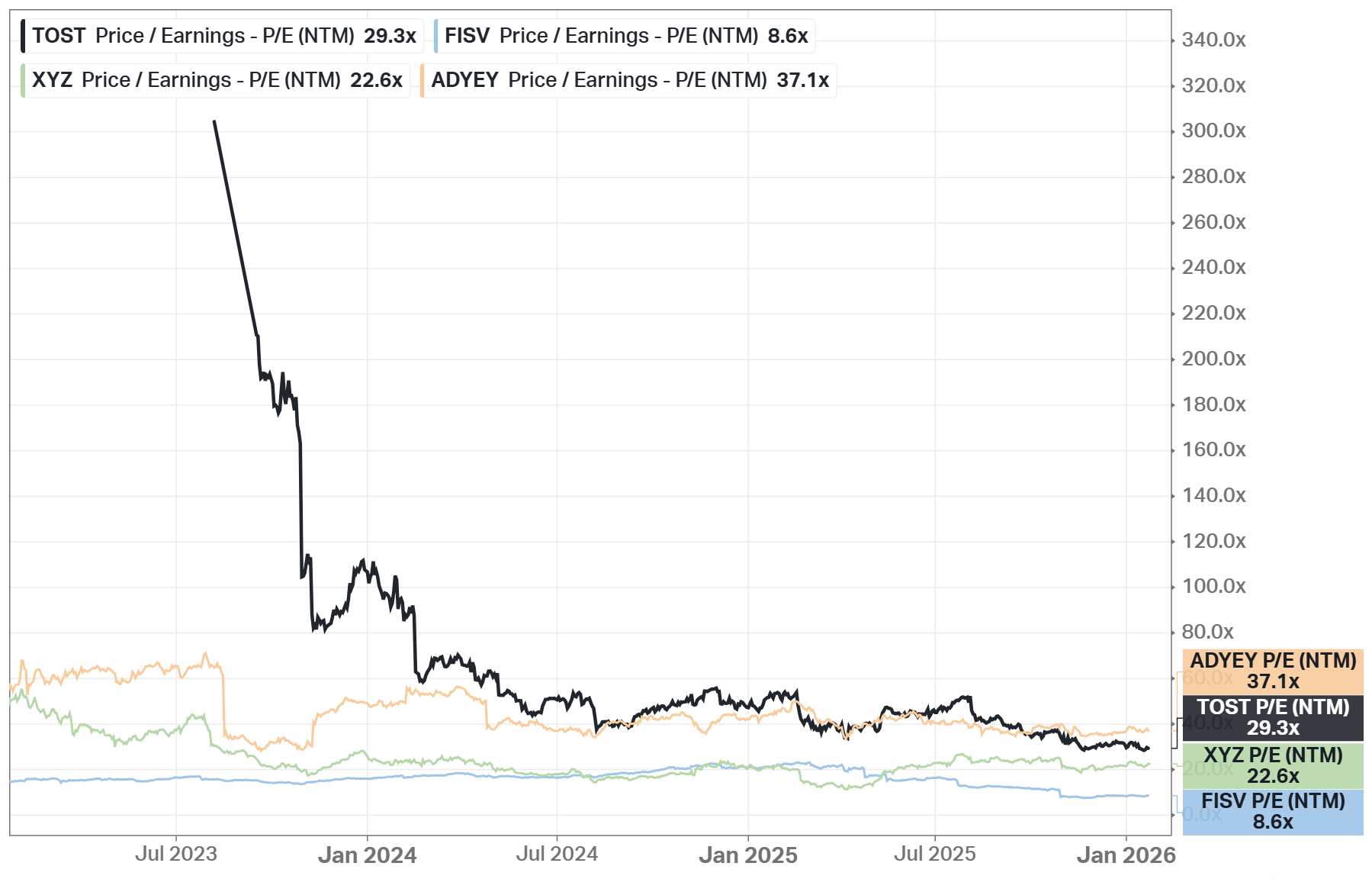

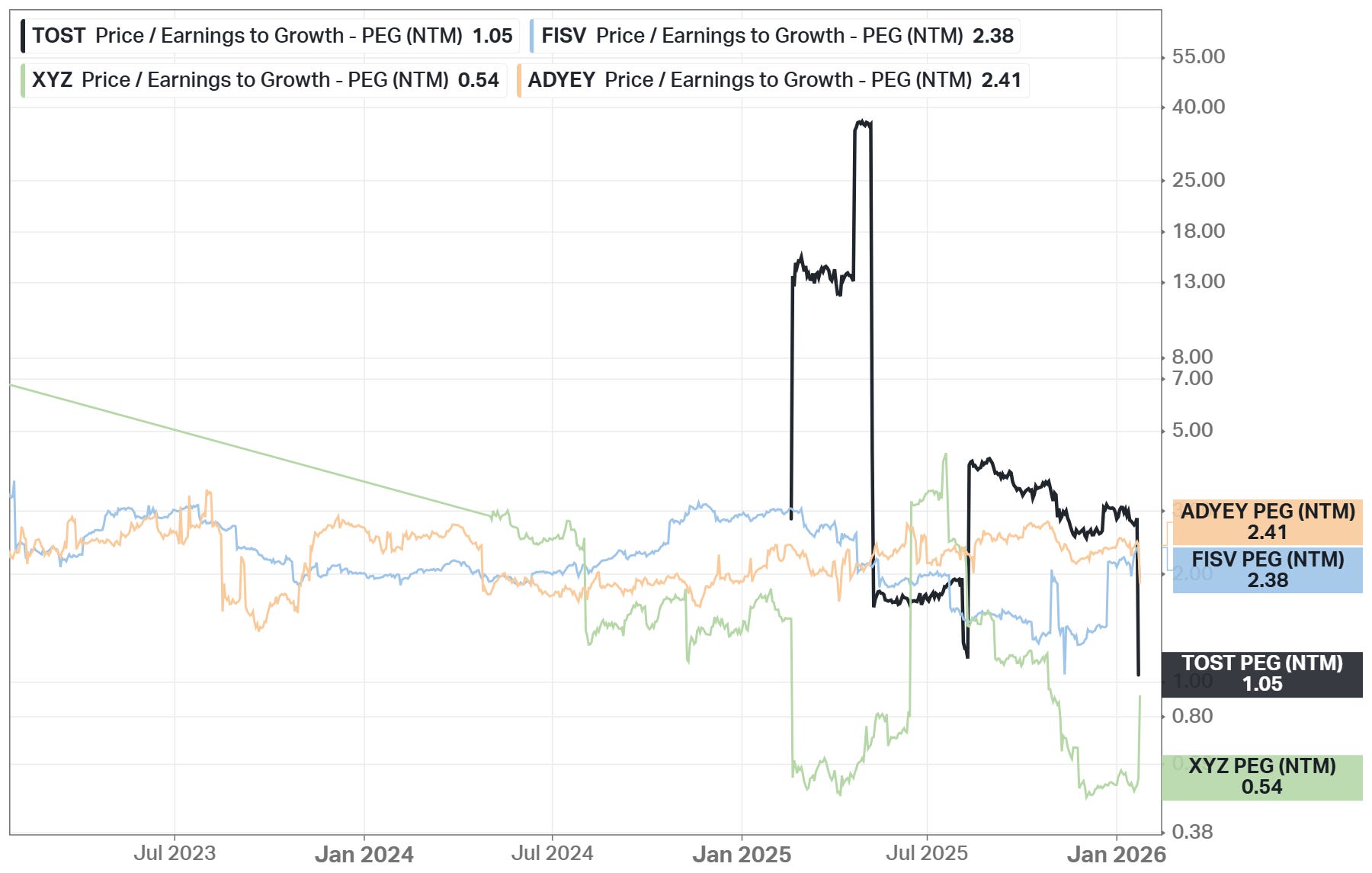

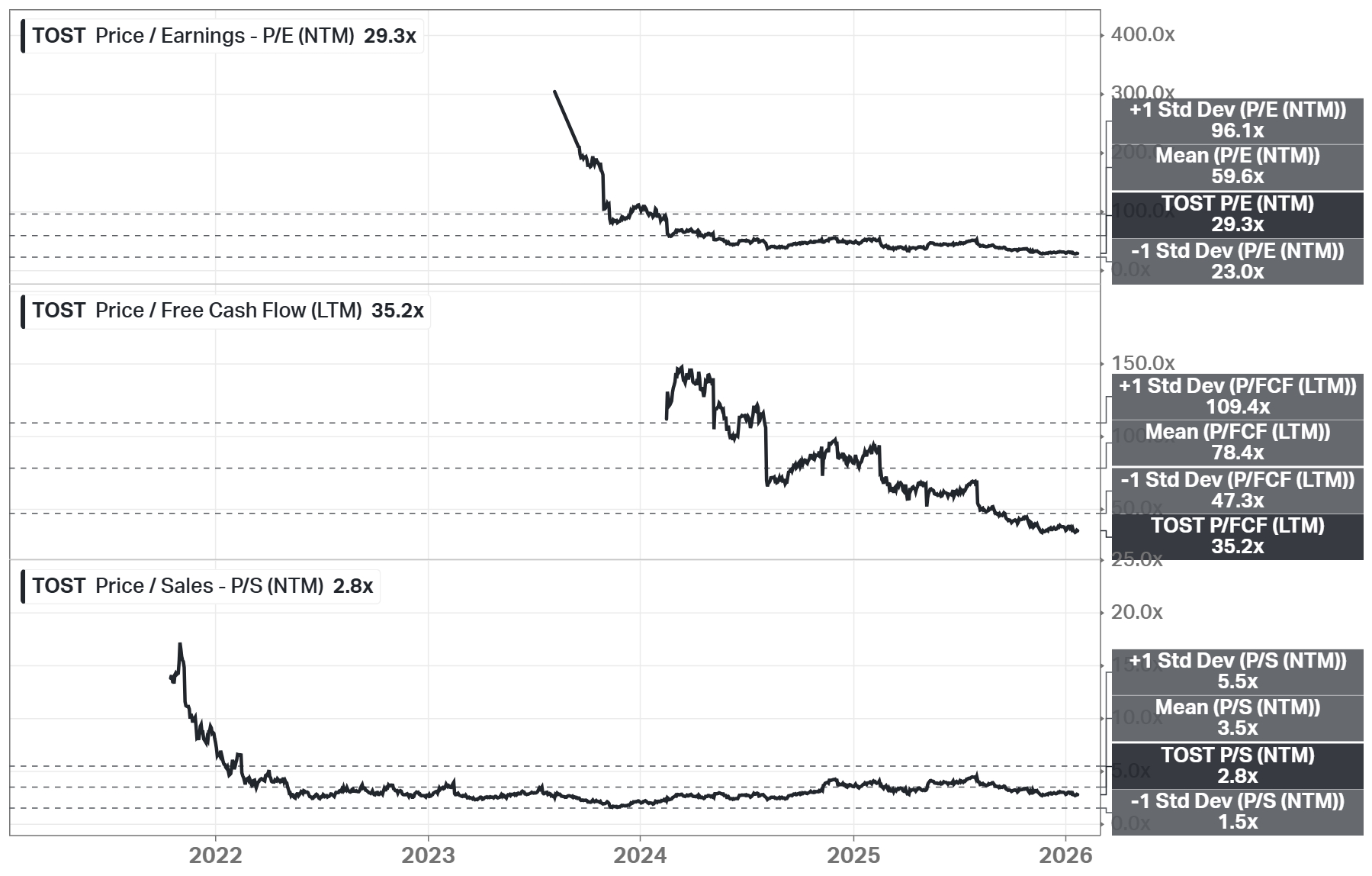

The charts below illustrate the current 5-year average valuation comparison. The company is trading below its 5-year averages, and the current PEG ratio stands at only 1.

Fair Price

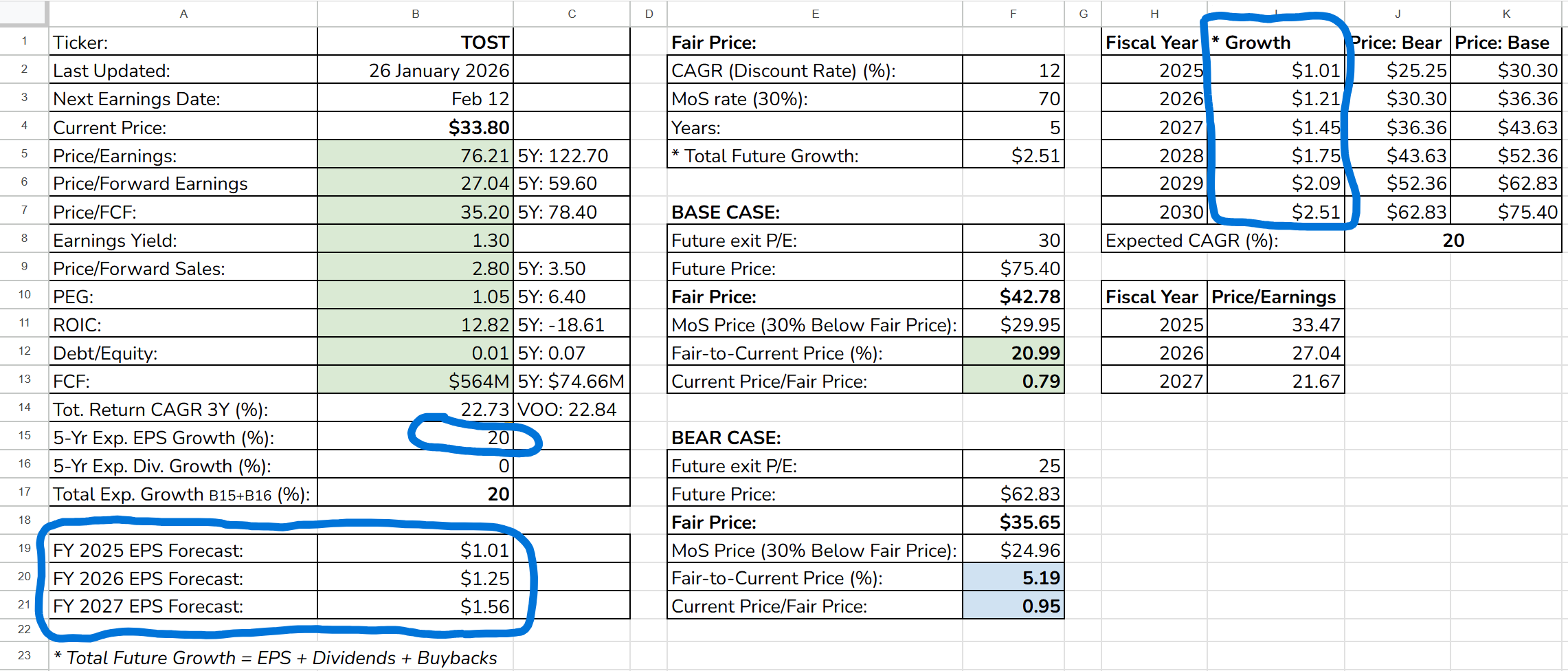

The Long-Term Pick’s Fair Price (Base Case) for TOST is $42.78. The current price of $33.80 is lower by 21%, so the stock is undervalued.

Fair-to-Current Price (%): 21%

Current Price/Fair Price: 0.80

I used:

Discount Rate: 12%

Margin of Safety: 30%

Years: 5

Future EPS Growth Rate: 20% (explanations below)

Future Dividend Yield: 0%

Total Future Annual Growth Rate: 20 + 0 = 20%

As the exit Price/Earnings ratio for the Base Case, I used 30, since this is a growth business and the future long-term EPS projection is close to this number (28%). For the Bear Case, I subtracted 5 from the Base Case.

Since my maximum forecast for future EPS growth is 20%, I chose to use this figure instead of the actual value of 28%. Even with the adjusted value of 20%, it’s important to note that my projected future EPS (as seen in the right section of the screenshot above) remains below the expected levels for the next three financial years (shown in the left section of the screenshot).

Due Diligence

Financial Strength (9 of 10):

✅ Debt-to-Equity: 0

✅ Cash-to-Debt: 103

✅ Piotroski F-Score: 8 of 9 (Not passed: Less Shares Outstanding YoY)

✅ Altman Z-Score: 14.74

Profitability (5 of 10):

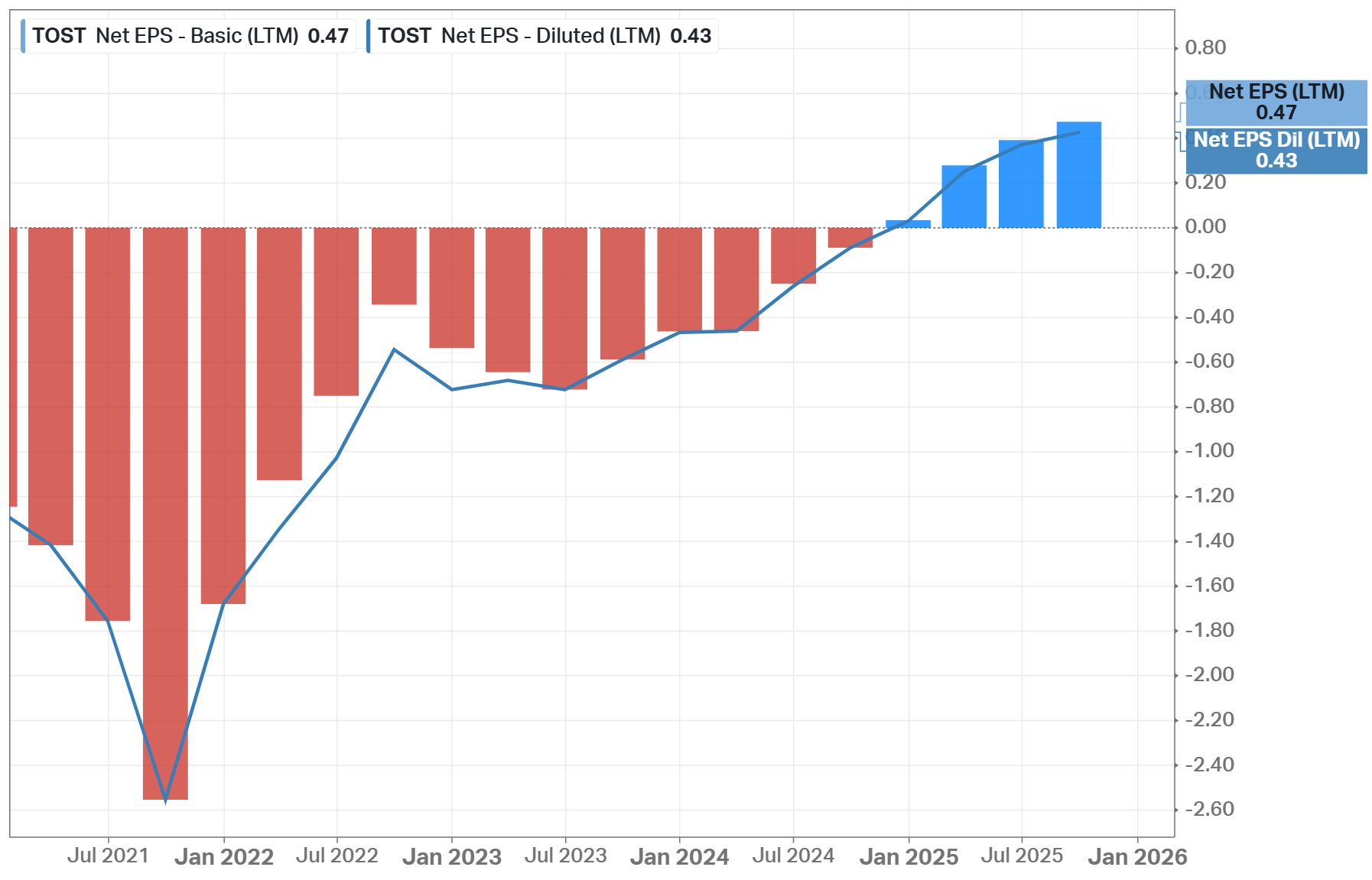

❌ Gross margin at least 40%: 25.73%

❌ Net margin at least 10%: 4.66%

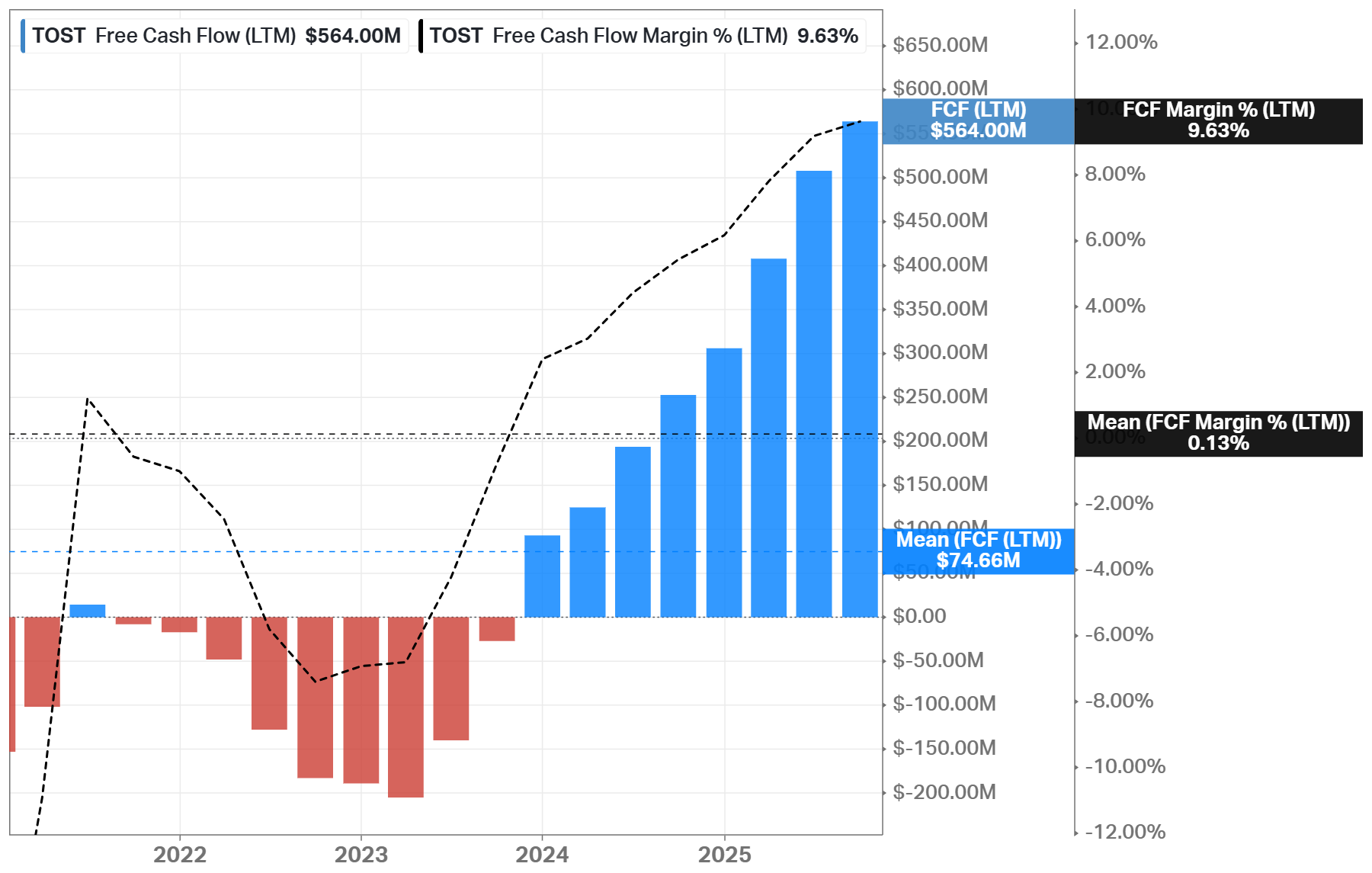

🟨 FCF margin at least 10%: 9.63%

🟨 Management (ROIC, ROE, ROA): Partially (All above 10%, except ROA)

❌ EPS surprises in the last 5 years: No (Missed in all years)

✅ EPS growth YoY 5 years in a row: Yes

Valuation (7 of 10):

✅ Valuation below its 5-year averages: Yes

✅ Valuation below the sector (XLK): Yes

❌ DCF Value: $31.46; Overvalued by 8% (10 years, discount rate: 10%, terminal growth: 3%, equity model: FCFE)

Advantage (7 of 10):

✅ Does it have a moat: Yes (narrow)

🟨 Outperformed the S&P 500 CAGR: Nearly (3-Year CAGR: 22.84% VOO vs 22.73% TOST)

Shares & Ownership (7 of 10):

✅ Insider ownership at least 5%: Yes (19.55%)

❌ Less shares outstanding YoY: No

❌ Insider buys last six months: No

🟨 Short interest no more than 5%: Nearly (5.19%)

Expectations (8 of 10):

✅ 1-year stock price forecast is above 10%: +37.75%

✅ Next 5-year EPS growth estimates (CAGR) is above 10%: Yes (28%)

Investment Thesis

Toast offers an attractive long-term investment case as the company transitions from rapid platform expansion toward improving profitability. The stock trades below its historical valuation and my fair price estimate. The current valuation reflects meaningful skepticism around margin conversion, which creates an opportunity if management continues to execute on operating leverage. At the same time, forward earnings growth expectations remain strong, suggesting that the market still underestimates the long-term earnings power of the platform.

The core strength of Toast lies in its integrated restaurant operating system, which combines software, payments, and hardware into one platform. This structure creates high switching costs and supports strong customer retention over long periods. While gross and net margins are still below those of mature peers, the business shows clear signs of margin improvement. This indicates that growth is increasingly driven by recurring, higher-quality revenue rather than volume alone.

The company operates with no long-term debt and holds a large cash position, which allows continued investment without financial pressure. Management has shown discipline by prioritizing organic growth, targeted innovation, and gradual margin expansion. Additionally, founder-led leadership and meaningful insider ownership align long-term decision-making with shareholder interests.

Taken together, Toast represents a transition-stage platform business with expanding economic value, where continued execution could drive meaningful upside over a multi-year horizon.

This is not a financial or investing recommendation. It is solely for educational purposes.

Koyfin was used for charts in this analysis. Use this URL to get a special pricing offer of 20% off all Koyfin plans.

Love this breakdown! I'm wondering if their expansion into enterprise means a shift in their core tech stack will be needed soon?