What Destroys Shareholder Returns

Investing in stocks requires more than picking companies with high growth potential. It’s important to watch out for risks like stock dilution, bad acquisitions, excessive debt, and others.

Dear long-term pickers,

After discussing my fair price estimate for Adobe (ADBE) with other analysts, I realized that my projected future 5-year EPS growth rate might be overly optimistic. As a result, I decided to revise my previous fair value estimate and lowered the growth rate to 11%. Additionally, I reduced the future exit Price/Earnings ratios. Despite these adjustments, my revised fair price is still almost 20% above the current market price.

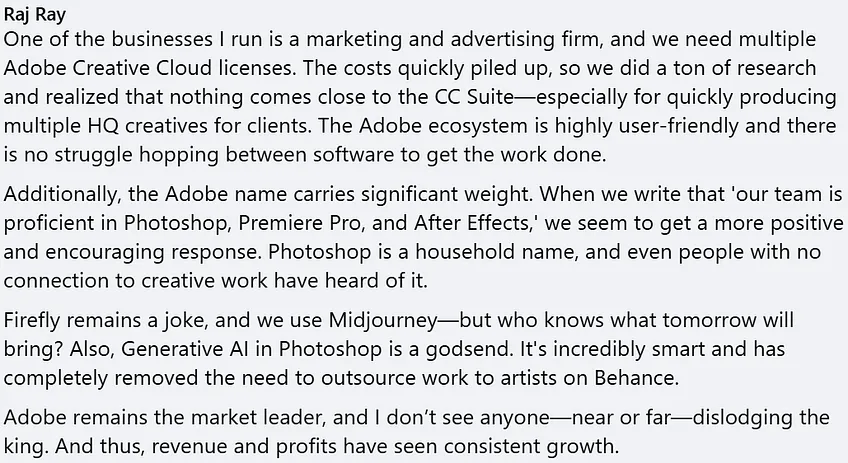

Please revisit the Fair Price section. Also, I received a comment from a real user regarding Adobe - see the image.

{kind=link}

Investing in stocks can be one of the best ways to build wealth over the long term. However, not every company creates value for shareholders. In fact, some make decisions that actively destroy shareholder returns. Whether it’s through dilution, poor acquisitions, or excessive debt, these mistakes can turn a promising investment into a loss. Let’s look at five common reasons for poor shareholder returns, with real-life examples.

Stock-Based Compensation

Stock-based compensation is a popular way for companies to pay employees and executives by giving them shares of the company instead of cash. It’s often used to attract and retain top talents, especially in tech companies. The idea is that employees will perform better when they have a personal share in the company’s success. However, this practice comes with a downside.

When a company issues new shares for compensation, it increases the total number of shares in circulation. This dilutes the ownership of existing shareholders, making each share worth less. While small amounts of stock-based compensation are manageable, excessive use can severely impact shareholder returns, especially if the company’s stock price doesn’t grow fast enough to offset the dilution. Investors often feel frustrated when their share in the company narrows, even if the business is growing.

Examples:

Palantir Technologies (PLTR): Palantir is known for spending heavily on stock-based compensation. In 2021 and 2022, it spent a lot of its revenue on stock-based pay, which significantly diluted shareholders, despite strong revenue gains.

Snap Inc. (SNAP): Snap consistently reported high stock-based pay for employees, resulting in heavy dilution.

Snowflake (SNOW): Snowflake’s generous stock compensation program kept the company unprofitable. Despite strong revenue growth, the heavy dilution raised concerns among shareholders about whether the company can deliver long-term value.

Bad Acquisitions

Acquisitions can be a great way for companies to grow. By buying another business, they can enter new markets, gain access to valuable technology, or grow their customer base. However, not all acquisitions work out as planned. If a company overpays for a deal or fails to integrate the new business properly, it can destroy value instead of creating it.

Poor acquisitions are often driven by management's overconfidence. Sometimes, executives are more focused on expanding their empire than on creating shareholder value. These deals not only waste money but also create operational headaches. In many cases, the company ends up writing off the acquisition as a loss, leaving shareholders to bear the burden.

Examples:

AT&T (T): AT&T’s $85 billion purchase of Time Warner was meant to create a telecom and media giant. However, the company struggled to integrate Time Warner and deliver the expected synergies. By 2022, AT&T spun off the business, admitting the deal was a failure. Shareholders paid the price as the stock underperformed during this period.

Microsoft (MSFT): Microsoft’s $7.6 billion acquisition of Nokia’s mobile phone business in 2014 is another classic example. The deal failed to make Microsoft a leader in mobile devices, and the company eventually wrote off the entire investment.

Quaker Oats: In 1994, Quaker Oats purchased Snapple for $1.7 billion, hoping to replicate its success with Gatorade. However, Snapple’s sales declined after the acquisition, forcing Quaker to sell the brand for just $300 million three years later.

High Debt Levels

Debt can be a useful tool for companies to fund growth, invest in new projects, or expand their operations. However, too much debt can become a serious problem. Companies with high debt levels are particularly vulnerable during economic downturns or when interest rates rise. Debt payments can eat into profits, limit the company’s ability to invest in its business, and even force it to cut dividends.

In the worst cases, excessive debt can lead to bankruptcy, completely wiping out shareholders. High debt also makes a company’s stock riskier, as any financial troubles can quickly spiral out of control. Investors should always check a company’s debt levels relative to its earnings before buying shares. Look at the following ratios:

Debt-to-Equity (D/E) = Total Debt ÷ Total Shareholders' Equity

What it shows: Indicates financial leverage and risk.

Ideal range: Lower ratios, typically under 2, suggest better financial health.

Debt-to-EBITDA = Total Debt ÷ EBITDA

What it shows: Measures the company's ability to pay off debt using operating income.

Ideal range: Lower is better, and under 3 is generally considered healthy.

Interest Coverage = EBIT ÷ Interest Expenses

What it shows: Assesses how easily a company can pay interest on its debt.

Ideal range: Higher is better, and above 2 is typically considered safe.

Examples:

Bed Bath & Beyond (BBBY): Bed Bath & Beyond borrowed heavily to fund its operations and store expansions. However, declining sales made it impossible to manage its debt, leading to bankruptcy in 2023. Shareholders lost everything.

Evergrande (3333.HK): The Chinese real estate giant accumulated over $300 billion in debt, hoping to dominate the property market. When sales slowed, the company defaulted on its debt in 2021, causing a major crisis and devastating shareholders.

Hertz (HTZ): Hertz took on massive debt to expand its rental fleet but was unprepared for the pandemic. When travel demand collapsed in 2020, the company filed for bankruptcy, leaving shareholders with huge losses.

Overpaying for Growth

Revenue growth is important for companies, but it needs to be profitable. Some businesses chase growth at any cost, spending heavily on marketing, promotions, or expansion that doesn’t deliver strong returns. This often happens when companies focus too much on market share or revenue numbers, neglecting the need for profits.

Overpaying for growth can lead to years of losses, frustrating investors who want to see sustainable returns. In some cases, the company eventually shifts its focus to profitability, but by then, shareholders may have already suffered significant losses.

Examples:

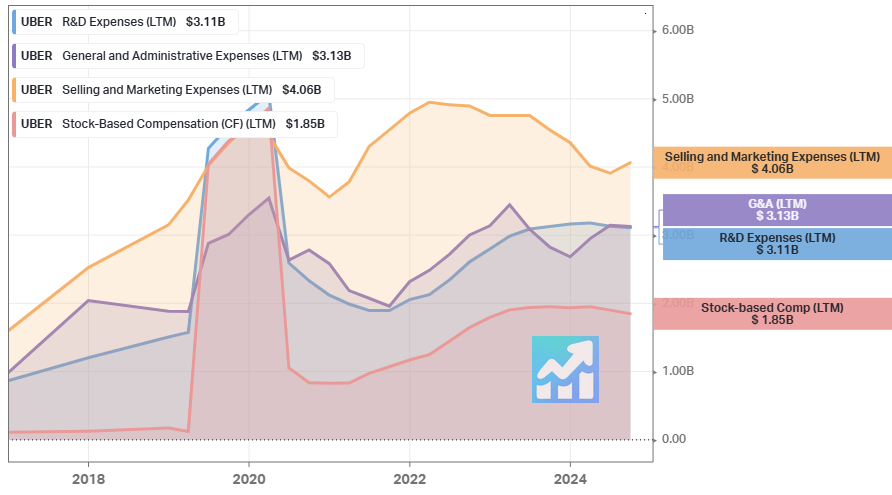

Uber (UBER): Uber spent billions of dollars on rider discounts and driver incentives to dominate the ridesharing market. While the company grew revenue quickly, it posted massive losses for years, delaying any real returns for shareholders.

Peloton (PTON): Peloton overestimated demand after the pandemic and spent heavily on production and inventory. When demand fell, the company faced significant losses, dragging its stock price down.

WeWork (WE): WeWork’s aggressive expansion strategy, combined with unprofitable leases, led to massive losses. The company’s valuation collapsed before its IPO, leaving early investors to deal with the fallout.

Poor Capital Allocation

Capital allocation is one of the most important jobs of a company’s management. Good capital allocation can drive long-term growth, while poor decisions can destroy value. Companies must decide how to use their cash—whether to reinvest in the business, pay dividends, buy back shares, or make acquisitions.

When management prioritizes the wrong projects or wastes money, it hurts shareholders. For example, overpaying for share buybacks when the stock price is too high or investing in unprofitable projects can waste valuable resources.

Examples:

General Electric (GE): GE spent heavily on acquisitions during the 2000s, many of which failed to deliver strong returns. These poor decisions forced the company into a painful restructuring process, hurting shareholders.

Intel (INTC): Intel’s failure to invest in advanced manufacturing allowed competitors like TSMC (comprehensive analysis) to take the lead in semiconductor technology. This misstep cost Intel valuable market share and slowed its growth.

Boeing (BA): From 2013 to 2019, Boeing spent over $40 billion on stock buybacks, leaving the company financially weak during the 737 MAX crisis and the COVID-19 pandemic. Shareholders suffered as the company struggled to recover.

Conclusion

Investing in stocks requires more than picking companies with high growth potential. To protect your returns, it’s important to watch out for risks like stock dilution, bad acquisitions, excessive debt, unprofitable growth, and poor capital allocation. These mistakes can erode shareholder value over time, even in promising companies.

Always take the time to analyze a company’s financials and management decisions. Ask yourself whether the company is making choices that benefit shareholders.

This is not a financial or investing recommendation. It is solely for educational purposes.

If you like the content, please hit the like icon, leave a comment, and share the publication with your friends and colleagues - this will motivate the author. If you're ready to support the project and get access to additional materials, visit this page.

thanks, Dan, very informative to learn

Despite these adjustments, my revised fair price is still almost 20% below the current market price. -> Think you mean ‘above’ and not ‘below’.