MarketAxess: Leader In Electronic Fixed-Income Trading But Overpriced

A leading electronic fixed-income trading platform that connects broker/dealers and institutional investors.

Changelog:

Feb 12, 2025: Updated fair price valuation: $191.

Jan 27, 2025: Overview: Management change, New share repurchase program, Expansion of AI technology, Increased trading volume, and Integration of acquisitions.

Nov 19, 2024: Updated fair price valuation: $200.

MarketAxess (MKTX) is a leading electronic fixed-income trading platform that specializes in corporate bonds and other fixed-income securities. It provides institutional investors with access to global liquidity in U.S. investment-grade bonds, high-yield bonds, Eurobonds, and emerging market corporate debt. The company also offers pre- and post-trade services, including regulatory transaction reporting.

Previous publication:

Content:

💡 Investment Thesis

🧐 Company Overview

🏰 Economic Moat

🚀 Business Strategy

✅ Advantages

❌ Disadvantages

🏛️ Capital Allocation

🥇 Competitors

⏮️ Past

📶 Future

💲Current Valuation

🏷️ Fair Price

☑️ Checklist

✍️ Due Diligence

💡 Investment Thesis

MarketAxess is dominant in U.S. corporate bond trading. Has an economic moat with an extensive network of over 2,100 client firms, and provides innovative trading solutions like Open Trading. High margins, high ROIC. Financially, shows steady growth. A strong balance sheet with $530 million in cash and no long-term debt, focusing on organic growth and strategic acquisitions. However, rising operating expenses, the impact of higher interest rates on trading volumes, and increasing competition from rivals like Tradeweb present challenges.

I see the company as a bit expensive at the moment, despite the fact that it’s trading below its 5-year averages. The company's continued investment in technology and expansion into emerging markets offer growth opportunities — a good candidate for a watchlist. Investors should monitor the company's ability to maintain market share, manage expenses, and successfully execute its growth strategies. Any significant price pullback or demonstrated success in emerging markets could present a more favorable entry point for long-term investors.

⬇️ Download Quick Analysis in PDF

🧐 Company Overview

Incorporated: 2000

Sector: Financial Services

Industry: Capital Markets

Stock Style: Small Core

Market Cap: $10.41 Bil

Earnings Date: Oct 23 - Oct 28, 2024Founded in 2000, MarketAxess Holdings Inc. is a leader in electronic fixed-income trading. The company provides institutional investors with access to a global network for trading U.S. investment-grade bonds, high-yield bonds, Eurobonds, and emerging market corporate debt.

In addition to trading, the firm offers pre- and post-trade services, including regulatory transaction reporting via its Regulatory Reporting Hub.

To Read: Company’s Milestones

MarketAxess receives the majority of its revenue from commissions, which account for over 88% of total operating revenues. The company is known for its strong position in U.S. high-grade corporate bonds, where it controls an estimated 85% of the electronic market share. Additionally, MarketAxess has been steadily growing its presence in emerging market debt and Eurobond trading, expanding its global presence.

🏰 Economic Moat

Due to its network effects in the bond trading market, I can say for sure that the company has an economic moat. MKTX has developed an extensive network of over 2,100 client firms (as of 2023), which enhances liquidity and reduces trading costs. This network, combined with innovative solutions such as its Open Trading platform, helps MarketAxess maintain its dominance in U.S. corporate bond trading. The platform's ability to reduce implicit and explicit costs for traders has been a key factor in its success. Its wide margins and ROIC also solidify its competitive advantage.

The company's extensive use of technology is another key aspect of its moat. MarketAxess has been at the forefront of applying artificial intelligence (AI) and machine learning in bond trading. Its AiEX (Automated Intelligent Execution) tool has allowed clients to automate parts of the trading process, increasing efficiency and reducing costs.

🚀 Business Strategy

From my perspective, MarketAxess has a growth-focused strategy by leveraging acquisitions and technology to enhance its offerings. Over the years, MarketAxess has expanded into the U.S. Treasury and municipal bond markets through acquisitions, such as LiquidityEdge and MuniBrokers.

In 2023, the company acquired Pragma, a firm specializing in quantitative trading technology, which further strengthened its fixed-income and foreign exchange trading capabilities. The company also expanded its partnership with BlackRock in 2024, integrating MarketAxess’ credit trading protocols with BlackRock’s Aladdin platform, allowing for deeper client engagement.

These strategic moves align with MarketAxess’ goal of expanding its trading volumes and entering new markets.

Additionally, MarketAxess has made progress in geographical expansion. Although it has already built a strong presence in Europe and emerging markets, there are further opportunities to grow in regions such as Asia and Latin America. The company’s partnerships with local financial institutions and its growing international client base (which contributes 30-40% of its trading volumes) signal that these regions could provide significant growth opportunities in the coming years.

Core business segments:

Transaction Services: This is the principal segment of MarketAxess, where the company eases the trading of corporate bonds and other fixed-income securities through its electronic platform. It includes services such as price discovery, trade execution, and post-trade processing. The platform supports various trading protocols, including Request for Quote (RFQ) and all-to-all trading, allowing market participants to connect and transact efficiently.

Data and Analytics: The company provides a collection of data and analytics services that offer market insights, trading analytics, and pricing information to its clients. This segment enhances the trading experience for institutional investors by providing tools for analyzing market conditions, tracking liquidity, and understanding price movements, which can lead to better trading decisions.

Warehousing and Risk Management: This segment includes services related to risk management solutions for bond dealers and other participants in the fixed-income market. MKTX offers warehousing services, enabling clients to manage their capital efficiently while taking on positions in the market.

New Products and Services: As I have already written, MarketAxess continually seeks to expand its offerings beyond its primary trading platform. This includes exploring new asset classes, trading technologies, and additional functionalities that meet the evolving needs of institutional investors.

✅ Advantages

Its Open Trading platform provides significant liquidity to its clients, allowing for client-to-client trading without intermediaries. This not only reduces trading costs but also makes the platform more attractive to institutional investors.

MarketAxess benefits from its strong international presence, with 30-40% of its bond trading volumes coming from Eurobonds and emerging market debt. This international diversification helps the company mitigate risks associated with domestic market fluctuations.

The company's financial strength is a notable advantage. With $530 million in cash and no long-term debt as of mid-2024, MKTX has the flexibility to invest in growth opportunities while returning capital to shareholders. The company has also been actively buying back shares, with $250 million remaining in its repurchase program.

Use of automated trading systems, which have significantly reduced costs and increased trading efficiency for its clients. Tools such as the AiEX solution have allowed MarketAxess to offer up-to-date execution methods that make trading faster and cheaper.

❌ Disadvantages

The company's operating expenses have been rising consistently, with total expenses projected to increase by 9.6% year-over-year in 2024, largely due to investments in platform enhancements and additional headcount. This continuous rise in costs has put pressure on margins, which, while still strong, have seen some contraction. For instance, the company's EBITDA margin in the second quarter of 2024 was 50%, down from previous periods.

The current interest rate environment also presents a challenge. Higher interest rates typically lead to higher bond yields, making lower-yielding securities less attractive. MarketAxess experienced a notable decline in U.S. government bond trading volumes, partly due to rising yields and reduced demand. The volatility in bond yields has affected fee captures and trading volumes, particularly for high-grade and high-yield bonds, impacting the company's overall performance.

The growing competition in the electronic bond trading market. The firm’s competitors, such as Tradeweb and Trumid, have been rapidly gaining market share, particularly in the investment-grade bond space, where MarketAxess' performance has been relatively stagnant.

🏛️ Capital Allocation

Balancing capital allocation strategy combining growth investments with shareholder returns. The company has historically focused on internal development, but in recent years, it has also pursued acquisitions to strengthen its market position. The acquisition of Pragma in 2023 added quantitative trading capabilities, while earlier purchases of LiquidityEdge and MuniBrokers helped the firm diversify into the U.S. Treasury and municipal bond markets.

In terms of shareholder returns, MKTX has been proactive in buying back its shares and increasing dividends. In Q2 2024, the company repurchased $33.5 million worth of shares and increased its quarterly dividend by 2.8%. With $250 million remaining in its repurchase program, MarketAxess continues to prioritize returning capital to shareholders. Its cash reserves of $530 million, combined with its lack of long-term debt, provide the company with broad flexibility for future investments and shareholder returns.

🥇 Competitors

Major competitors are CME Group (CME), Intercontinental Exchange (ICE), and Tradeweb Markets (TW). CME Group dominates the futures market and has a significant presence in fixed-income trading through its BrokerTec platform. Intercontinental Exchange, best known for its equity and derivatives trading, has been expanding its presence in fixed-income trading but has struggled to make a major impact in the bond market despite several acquisitions.

Tradeweb Markets, however, poses the most direct competition to MarketAxess, especially in U.S. corporate bond trading. Tradeweb has rapidly gained market share in the investment-grade and high-yield bond markets, making it a notable competitor. Although MarketAxess remains the leader in U.S. high-yield bond trading, the rise of Tradeweb and other smaller platforms like Trumid could put further pressure on MarketAxess' market share. Maintaining its leadership in this increasingly crowded space will require continuous innovation and investment.

⏮️ Past

In Q2 2024, the company reported a 10% revenue growth, reaching $198 million, with $8 million from the Pragma acquisition. Diluted EPS was $1.72. Despite disappointing U.S. credit market share, international growth and new hires strengthened the company. Expenses rose 12%, and the company adjusted its full-year expense guidance to below $480 million-$500 million. An approved $200 million share repurchase program reflects confidence in future performance. The launch of the X-Pro platform and strategic hires are expected to drive future growth, emphasizing long-term trends over monthly fluctuations.

The company has outperformed (CAGR) both the industry and the S&P 500 in long-term periods of 10 and 15 years but underperformed in 3 and 5 years (negative CAGR). Also, has underperformed during YTD and 1-year periods.

🤔 If you had been subscribed to Patreon, you would already have access to the following: September major update of the Long-Term Pick Portfolio, a long-term-looking aerospace investment opportunity, and an opinion about the rise of the Philippines' outsourcing.

📶 Future

Four main strategic priorities for the company's future success (as the company sees it). The first goal is to grow their core fixed-income trading revenue (their main business). The second aims to make the client network experience better (to keep customers happy). Third, they want to bring in new technology and data solutions, showing they're trying to stay modern. Lastly, they want to build a high-performing team and culture, focusing on their employees.

X-Pro has already been given to their biggest clients and will soon be available internationally. High Touch Solutions uses AI to help with big, complex trades - they've already made trading better and plan to add more AI tools soon. Low & No Touch Solutions are for automatic, smaller trades - they've already made several automatic systems and plan to add more, especially for international markets.

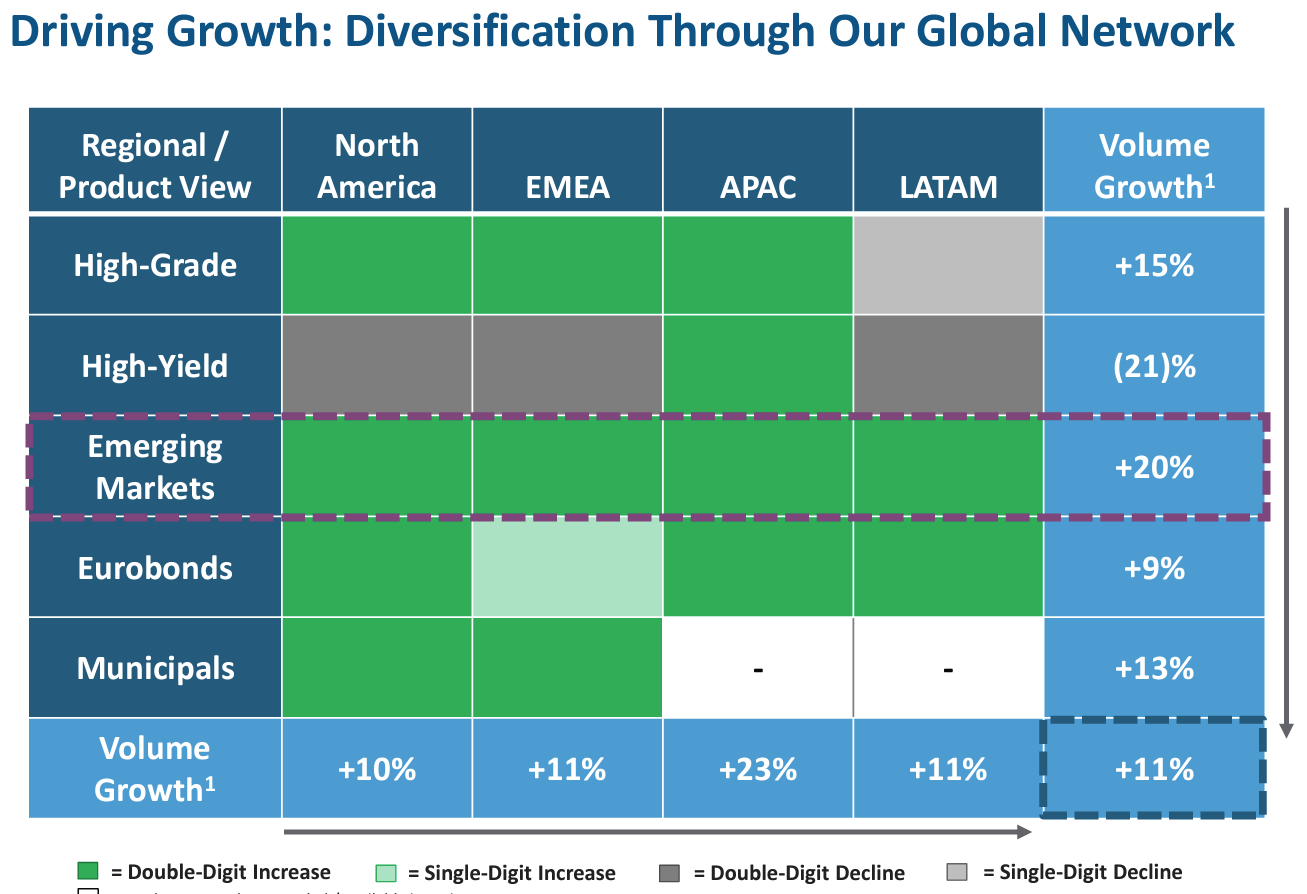

How different products are performing across various world regions. Green means good growth (double or single digit), while gray shows a decline. We can see an increased bet on emerging markets, I suppose it will continue in future. It seems the company is trying to compensate recent decline in North America (High-Yield) with concentrated expansion to EM.

From 2Q24 report:

• Emerging markets commission revenue up 22%

• Record 1,507 emerging markets active client firms, up 5%

• Record LATAM and APAC emerging markets trading volume, up 27% and 35%, respectively

• Emerging markets local currency trading volume of ~$90 billion, up 19%

• Record emerging markets RFM activity of ~$30 billion, up 45%

• Record emerging markets block trade volume of ~$28 billion, up 21%

A financial outlook covering three future fiscal years. Sales are forecasted to climb consistently each year, with a yearly increase of around ten percent. The EPS growth has an even more optimistic picture, as the growth rate accelerates significantly over the time period. While sales growth remains stable, the increasing pace of earnings growth suggests the company aims to become more efficient at turning revenue into profit.

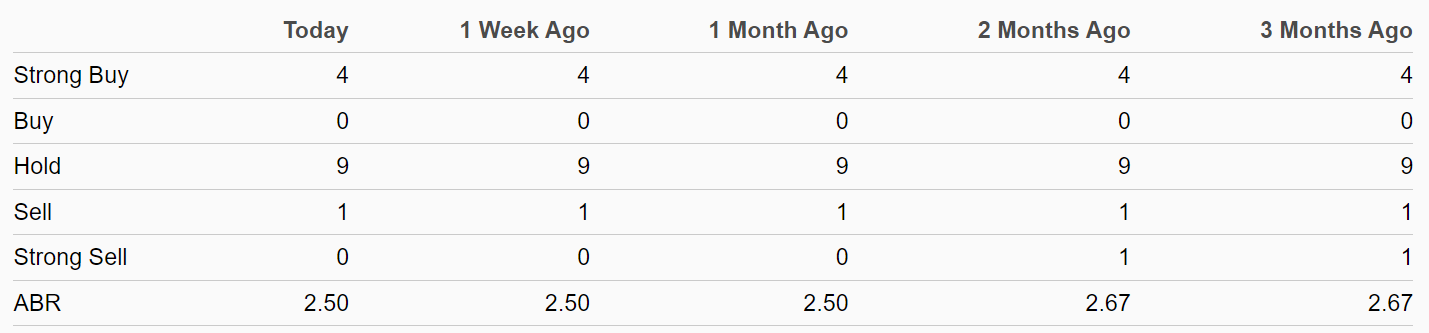

Let's consider the predictions of future prices by various analysts. Some are pessimistic, anticipating a drop, while others are optimistic, foreseeing gains. The current stock price exceeds the average target.

MarketAxess currently has an average brokerage recommendation (ABR) of 2.50 on a scale of 1 to 5 (Strong Buy to Strong Sell), calculated based on the actual recommendations (Buy, Hold, Sell etc.) made by 14 brokerage firms.

💲Current Valuation

To be honest, despite the fact that the current valuation is lower than its 5-year averages (except for PEG), I don’t like it — it's still too high. Especially, I don’t like the high PEG ratio. I suppose that the market embeds potential future growth in the price — see the section “Future”.

Compared to the industry, the company is trading with a significant premium.

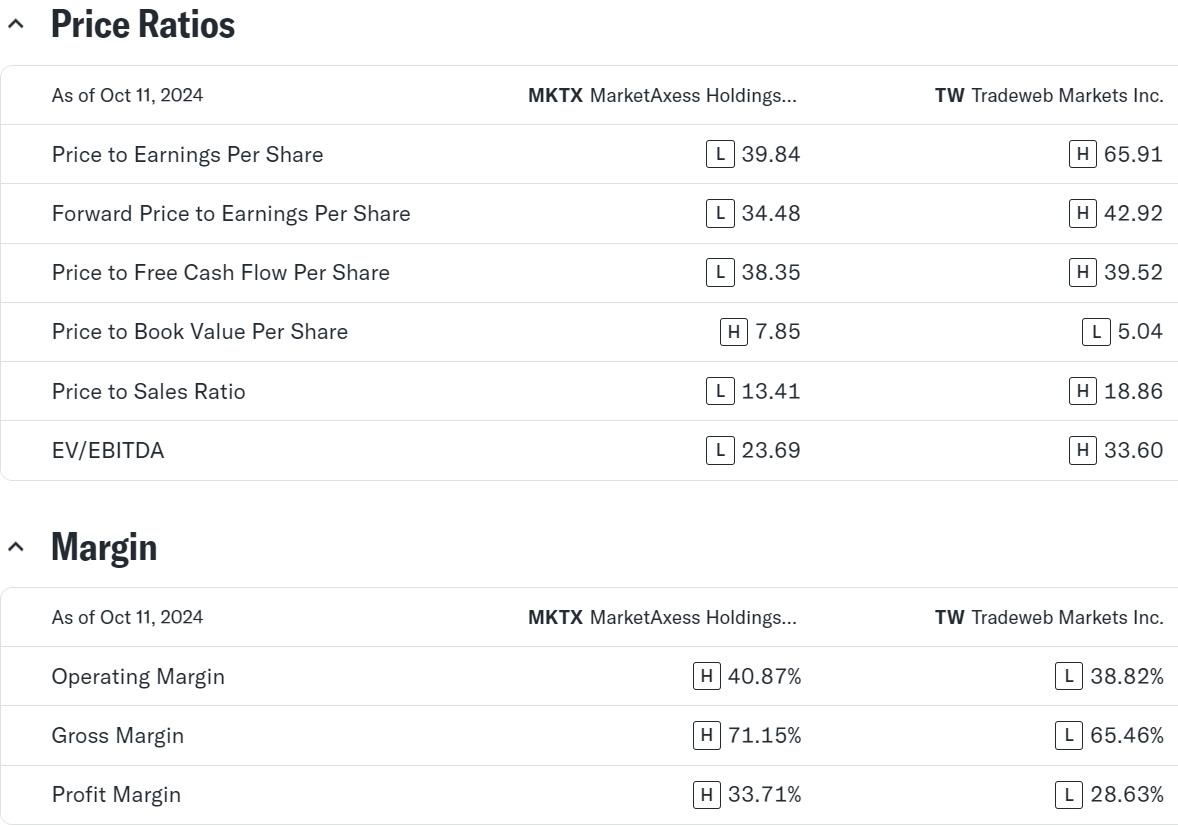

Also, I would like to compare MarketAxess with Tradeweb Markets, since the latest one is the most direct competition to MKTX, especially in U.S. corporate bond trading. Pay attention to highlighted metrics with [H]. TW is trading higher, but MKTX has higher margins.

Also, MKTX has higher equity returns:

🏷️ Fair Price

➡️ Updated fair price valuation: https://longtermpick.com/p/updated-valuations-nov-24-2

The Long-Term Pick's Fair Price (Base Case) for MKTX is $192.89. The current price of $278.10 is higher by 44.17%.

Fair-to-Current Price (%): -44.17%

Current Price/Fair Price: 1.44

I used:

Discount Rate: 12% (S&P 500 Next 5-Yr Growth Estimates is 11.87%)

Margin of Safety: 30%

Years: 5

Future EPS Growth Rate: 7% (Based on Yahoo Finance)

Future Dividend and Buyback Yield: 1% (I took the 5-year average value)

Total Future Annual Growth Rate: 7 + 1 = 8%

For the Base Case, the Future Expit P/E is 32. 5-Yr average P/E ratio is 48.08, the lowest P/E during the last ten years was 39.62. For the Bull Case, I just took the Base Case + 5, for the Bear Case I took the Base Case - 2.

When I was estimating the Fair Price, I was a bit impressed by how high the market estimated the company in the past - the average P/E ratio for the last five years is 48.08.

☑️ Checklist

Profitability:

✅ Gross margin at least 40%: 90%

✅ Net margin at least 10%: 34%

✅ Management (ROIC, ROCE, ROE, ROA): Yes (All above 10%)

❌ Piotroski F-Score: 6 of 9 (Not passed: Higher Current Ratio YoY, Less Shares Outstanding YoY, Higher Gross Margin YoY)

❌ Revenue surprises in last 7 years: No (2023; Based on TradingView's data)

❌ EPS surprises in last 7 years: No (2017 and 2021; Based on TradingView's data)

❌ EPS growth YoY 7 years in a row: No (2021, 2022)

Valuation and Advantage:

✅ Valuation below its 5-yr average: Yes

✅ Does it have a moat: Yes

Shares:

❌ Insider ownership at least 5%: No (1.79%)

❌ Less shares outstanding YoY: No

❌ Insider buys last six months: No

Price:

❌ 1-year stock price forecast is above 10%: -6.74%

❌ Next 5-Yr Growth Estimates (CAGR) is above S&P 500: No (7.05% vs 11.87%; Based on Yahoo Finance)

❌ DCF Value: $137.52 (Overvalued by 50%; 10 years, discount rate: 10%, terminal growth: 3%, equity model: FCFE)

✅ Short Interest below 5%: Yes (2.15%)

✍️ Due Diligence

Profitability:

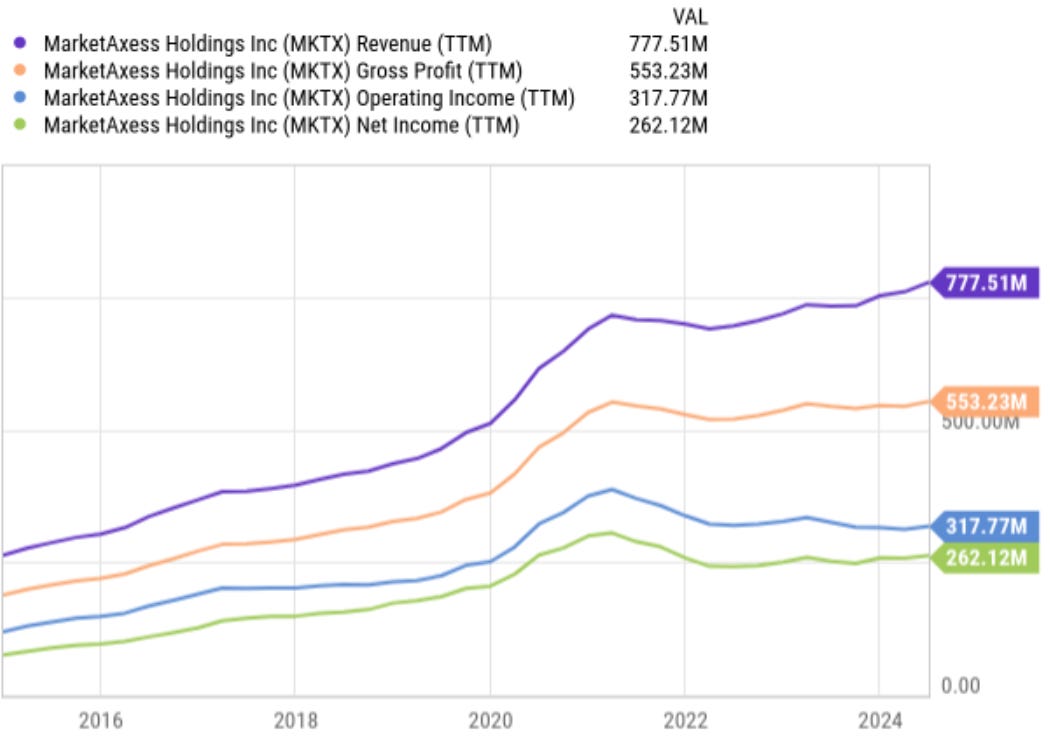

✅ Positive Gross Profit: 696.6m USD

✅ Positive Operating Income: 317.8m USD

✅ Positive Net Income: 262.1m USD

✅ Positive Free Cash Flow: 272m USD

✅ Positive 1-Year Revenue Growth: 6%

✅ Positive 3-Years Revenue Growth: 3%

✅ Positive Revenue Growth Forecast: 10%

✅ Positive ROE: 21%

✅ Positive 3-Year Average ROE: 24%

❌ Declining ROE: 29% > 21%

✅ Exceptional ROIC: 25%

✅ Exceptional 3-Year Average ROIC: 30%

❌ Declining ROIC: 36% > 25%

Solvency:

✅ High Interest Coverage: 125.75

✅ Short-Term Solvency

✅ Long-Term Solvency

✅ Low D/E

✅ High Altman Z-Score: 10.27

This is not a financial or investing recommendation. It is solely for educational purposes.

Thanks!